ASUR - Asure Software: Waiting For The Operating Leverage

2023-08-22 04:38:47 ET

Summary

- Asure Software sells human capital software solutions to small and mid-sized businesses, with a wide offering.

- The company has a healthy retention rate and recurring revenues make up a significant portion of its overall revenue, making the company low in risk.

- Asure's stock price has increased by 121% in the past year, making the stock's current price seem fairly priced in my DCF model estimates.

Asure Software ( ASUR ) is a United States -based company that sells human capital software solutions to small and mid-sized businesses. The company could see significant operating leverage in the medium term, as Asure’s revenues grow. Although the operating leverage is a promising prospect, I have a hold-rating for the stock as the stock’s year-long rally has priced in a good amount of growth.

The Company

Asure sells software that manages human resources with services that help with payrolls, taxes, as well as other human resources solutions. The offering is quite wide, as Asure has a wide list of offerings on its website:

{kind=link}

Asure has an extremely healthy retention rate, as the company claims in their Q2 earnings presentation to have a 93% net retention rate in the last twelve months. The company’s recurring revenues also represent 92% of the company’s revenues, lowering the company’s risk profile significantly.

The stock has had a massive run in the past year, as Asure’s stock price has increased by 121%:

{kind=link}

With the fast rise in Asure’s stock price, I believe it is worth looking at whether the company is worth the price.

Financials

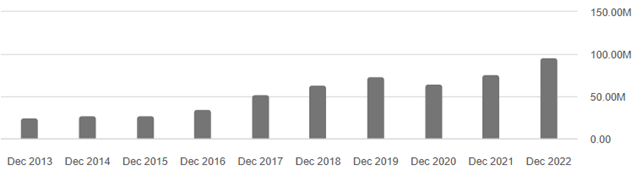

Asure has a trailing revenue figure of $114.68 million after Q2. The company is guiding towards a revenue of $118 million to $120 million for 2023, representing a growth of 23.1% to 25.2%. This growth is above the company’s historical figure of 15.8%:

{kind=link}

On an EBIT level, Asure still operates at a slight loss, as the company’s trailing EBIT stands at -$2.78 million after Q2. Although the figure is negative, the earnings show a clear positive trend, as in 2022 the company’s operating loss was -$11.31 million – the company’s bottom line shows signs of improvement. With the growth in revenues, I expect the company to realize significant operating leverage, in line with the company’s expectations:

{kind=link}

The company has a target of at least a 20% adjusted EBITDA margin. The margin would be clearly above 2022’s levels as in the year Asure’s adjusted EBITDA margin was 12.3%. Because Asure has significant amortizations, the company’s operating profits show a weaker earnings level compared to the company’s actual ability, as the amortization does not correlate with cash flows. For example, in 2022 the company’s amortizations were more than $14 million .

Asure has around $36.8 million in long-term debt , of which $6.6 million is in current portions. I see this as a moderate amount – Asure’s cash flows are quite limited for the time being as the company focuses on scaling, so enormous amounts of debt would be unhealthy. The outstanding amount should be safe for Asure considering their future cash flows. The company also has a cash balance of $21.6 million.

Valuation

As I believe that valuation plays a significant role in determining promising investment opportunities, Asure’s valuation plays a significant role in determining my rating for the stock. Currently Asure trades at a NTM EV/S of 2.58, above the company’s five-year average of 2.19:

Historical EV/S (Tikr)

Further, to analyze a fair value estimate for the stock, and to determine an EV/S ratio worth paying, I constructed a discounted cash flow model.

In the model, I estimate Asure to hit its current revenue guidance for 2023. Going forward, I have a growth of 15% for 2024, with the growth fading into a perpetual growth rate of two percent slowly, as seen in the screenshot of the model.

I expect Asure to achieve a positive EBIT figure in 2024, with the company’s operating leverage kicking in slowly. In the model the estimated EBIT margin rises into a perpetual rate of 14.18% - a figure that could even be on the low side considering the company’s business model and high gross margins. Finally, as the company has a fair amount of amortization that doesn’t affect cash flows, I’m expecting the company to convert its earnings very well into free cash flow.

These estimates along with a weighted average cost of capital of 8.36% make the following DCF model scenario, with a fair value estimate of $12.21, three percent above the current price:

DCF Model of Asure (Author's Calculation)

The fair value estimate would correspond to an EV/S ratio of 2.65 for the next twelve months. The used WACC of 8.36% is derived from a capital asset pricing model:

CAPM of Asure (Author's Calculation)

I estimate Asure’s long-term interest rate to be 6.25% - the rate is two percentage points over the United States’ 10-year bond yield , leaving room for a margin. I expect Asure to only leverage debt moderately with an estimated debt-to-equity ratio of 15%.

I use the mentioned United States’ 10-year bond yield as the risk free rate in the model. The equity risk premium of 5.91% is Professor Aswath Damodaran’s estimate for the United States, made in July. Tikr estimates Asure’s beta to be 0.72, a low amount due to Asure’s low revenue risk profile, as the overwhelming majority of revenues is on an occurring basis. Finally, I add a liquidity premium of 0.5% into the cost of equity, adding up to a cost of equity of 9.01% and a WACC of 8.36%, used in the DCF model.

Takeaway

At $11.89 a share, I believe Asure is priced fairly considering its future prospects. The company should see good amounts of operating leverage in the future, but in my opinion the company would need to see faster growth than forecasted to be an outstanding investment opportunity at the current price; for the time being, I have a hold rating for the stock.

For further details see:

Asure Software: Waiting For The Operating Leverage