TBC - AT&T: A High Yield Opportunity At A Bargain Price

2023-05-30 02:55:40 ET

Summary

- AT&T (and the other telecom giants) has taken a hit on the back of potentially stiffer competition from DISH.

- However, T remains cheap even despite this new potential headwind with an attractive dividend yield.

- The FCF is concerning, but it doesn't guarantee a dividend cut as long as they don't revise FCF guidance significantly lower.

Written by Nick Ackerman. A version of this article was included in our Cash Builder Opportunity weekly options expiration update originally posted on May 27th, 2023.

AT&T ( T ) and the other telecom giants Verizon ( VZ ) and T-Mobile ( TMUS ) were hit with the latest rumor that DISH Network ( DISH ) and Amazon ( AMZN ) are planning to partner up. T's first quarter was also showing a struggle for free cash flow generation. The FCF was well below what they needed to cover their dividend.

However, the stock is dirt cheap, and the yield can be covered if they hit their FCF target. Even if they have to revise FCF lower, as they did last year, there is some flexibility to maintain this 7%+ monster yield.

What's Happening With T?

Ugly FCF

With the superpower of hindsight, we know the earnings were one of the events putting downward pressure on the share price. The earnings themselves that T posted weren't abysmal in terms of EPS and revenue. Revenue missed slightly but was up a bit year-over-year. Any growth is generally a good thing with these telecom giants.

However, what truly hit investors was the free cash flow coming in extremely light once again. FCF of only $1 billion doesn't provide enough coverage to the dividend as it only supports about half of the payout.

T FCF Payout Ratio (T Earnings Report (highlights from author))

This was also a similar story last year when FCF was light too. However, it was much lighter this year as FCF declined significantly.

The silver lining is that if it works out as it did last year, FCF will start pouring in throughout the rest of the quarters. They had $2.811 billion in FCF for Q1 2022 and ultimately hit $14.1 billion for the full year.

For 2023, they are guiding for FCF to come in at $16 billion. That's a figure they said they are still expecting to hit for the full year.

Capital investments were $6.4 billion as we continue to make historically high levels of investments in 5G and fiber. Free cash flow for the quarter was $1 billion. This was consistent with our expectations and accounts for several seasonal and anticipated working capital impacts. We remain confident in our full year outlook for free cash flow of $16 billion or better. This expectation is largely due to the timing of capital investments, device payments, incentive compensation, which all peaked in the first quarter.

However, in 2022 they had originally forecasted for being in the range of $16 billion in FCF as well before revising it lower later in the year. Here's from Q1 2022 earnings call :

Given that Q1 is a seasonally low quarter for free cash flow and many of the factors impacting free cash are not expected to repeat, we remain confident in the guidance we provided to you during our Analyst Day to achieve free cash flow in the $16 billion range for the year and on a standalone basis.

Given the larger shortfall in Q1, it would seem that revising FCF lower in the coming quarters is likely. Still, they don't need to achieve the target they set out to cover the dividend. With 7.149 billion shares outstanding and an annual dividend of $1.11, that's a payout annually of less than $8 billion.

Of course, with lower-than-expected FCF, that would also mean less flexibility in paying off the debt and CAPEX spending. The debt here is certainly not insignificant.

Ycharts

The DISH News

These FCF concerns stemming from their quarterly earnings seemed to have kicked off the latest bloodbath in terms of the declining share price. However, more recently, news of a potential partnership between Amazon and DISH Network was the latest catalyst to kick off a new round of selling.

The report says that DISH would be selling its plans through AMZN. That means potentially millions of consumers will be exposed to ads on the Amazon platform every single day. That huge audience could propel DISH to be considered serious competition against the other three main telecoms. So it doesn't just impact T and VZ, but also T-Mobile ( TMUS ) - TMUS has become a thorn in the side of T and VZ as well.

For consumers, this is ultimately a positive. This is capitalism when there is competition. Competition can drive down prices of goods and services and provide the need to offer better quality and additional services to woo customers. That can mean lower profits as pricing power declines while simultaneously increasing costs.

Initially, shares of DISH jumped but have fallen back down to levels where they were previously. Conversely, it saw a drop from the three top telecoms. T, in particular, seemed to be the hardest hit.

Ycharts

I view DISH as a broken company. Their earnings have been declining and are still expected to decline rapidly.

{kind=link}

I think that makes them more dangerous competition because they have nothing to lose. They're junk-rated, and S&P Global recently moved them to a CCC+-rated company. Meaning that they believe there is a high probability they'll begin defaulting on their debt. A company that has nothing to left to lose but everything to gain can be aggressive. Any cash flow is likely a positive at this point to keep them afloat.

All this said we can expect to hear an official announcement on how this deal may or may not work in June.

Latest Covered Call Update

For the latest covered calls, we initiated this trade all the way back on April 12th, 2023. The trade was over 44 days in total, and we collected $0.24 in premiums. On an absolute basis, that doesn't sound like much, but on an annualized basis, it comes in right around 9.48%. That's well ahead of the dividend yield from holding the stock alone. However, even that is an enticing 7.16%.

While we originally took the assignment of these shares at $19, with a rising share price, we were able to write these puts at $21. We were in a position to make a bit of a bonus with capital gains potentially had the shares been called away.

Ycharts

One of the key risks here was writing the calls right before T was set to post earnings. That can work to our advantage by adding in more expected volatility and increasing the option premium we can receive. However, it also comes with the potential for a huge upside move. If earnings topped expectations across the board and guidance was strong, we could have easily topped the $21 strike price - at which point our upside becomes capped.

In total, we took the assignment of T at $19 with the August 12th, 2022, options expiration. We collected $0.24 in premium from initially selling the puts. We were then able to write calls shortly after that to net another $0.19 in premium.

After that, the market took a dive, and that brought T down with it. We went with a relatively longer trade as we entered another covered call position in October 2022 that didn't expire until January 2023. I generally like writing anywhere around 30 days roughly. In this case, it was 84 days or essentially a quarter, but we did collect $0.27 in premium or roughly the equivalent of the quarterly dividend.

Right after that, we were able to write more calls immediately to snag another $0.32 in premium. This then brings us up to the latest trade of collecting $0.24.

In total, we've now collected $1.26 in option premiums over 288 days. We also collected $0.8325 in dividends paid for the last three quarters during this period.

Conclusion

FCF and the DISH news seem to be some of the primary culprits in the latest weakness. However, as an income-oriented investment with substantial yield, higher risk-free yields could also be drawing some would-be buyers away. If you can get 5 to 6% in Treasuries now, that's clearly something an income investor should consider in the current environment.

With all the negatives working against T, that's certainly playing out in the company's share price. However, we saw a bit of this same share price action last year before shares ultimately recovered. Last year the stock hit lows in October, and that was when the broader market was also hitting a new low before ultimately bouncing back and recovering.

Ycharts

That said, as we've highlighted several times, the overall market is a bit fake this year. There is mostly a handful of mega-cap tech-related names that are driving the results. Perhaps the best way to highlight this is by comparing ( SPY ) with its equal-weighted counterpart, the Invesco S&P 500 Equal Weight ETF ( RSP ). Sure, T certainly has had an ugly 2023 performance, with most of that resulting in the last month or so declines.

Ycharts

What RSP highlights is that T isn't seemingly alone in terms of being a poor performer. If the mega-cap tech names driving the S&P 500 were equally weighted, we'd see flat 2023 YTD performance. Take those away completely, and we'd see more material declines.

T is also looking incredibly cheap.

{kind=link}

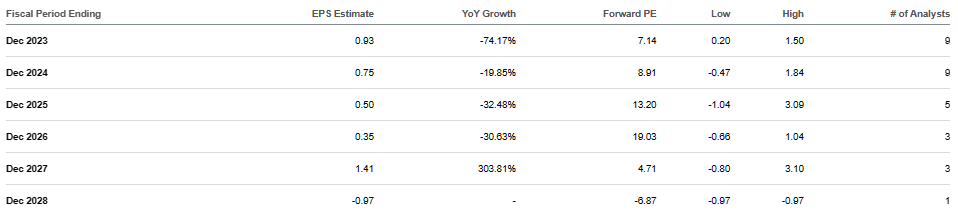

Historically, we've seen T trade in the 8.7x to 13.4x P/E range. At around mid-single-digits, that's quite a substantial discount. Earnings are expected to dip this year - that's why we are seeing the range trend lower on the chart above - but then earnings are expected to grow slowly after that. If earnings start growing, we'd see the channel range head higher or stabilize.

For further details see:

AT&T: A High Yield Opportunity At A Bargain Price