TBC - AT&T Q2: Buy Before It Soars

2023-07-18 11:00:00 ET

Summary

- AT&T will be reporting its Q2 results next week.

- The Street's expectations seem to be extremely conservative and AT&T might handily beat them.

- This may be a good time to accumulate AT&T's shares.

All eyes will be on AT&T ( T ) when it reports its fiscal Q2 results next week. The telecom giant’s shares have been hammered down over concerns relating to its business and dividend sustainability. So, to gain clarity on these matters and to gauge how the company is progressing on these fronts, investors may want to keep close tabs on AT&T’s free cash flow, segment financials, its subscriber metrics and its management’s outlook for the quarter ahead. These key items will reveal the true extent of AT&T’s recovery and are likely to influence where its shares head next. Although, at the outset, AT&T seems like a good buy ahead of its Q2 earnings.

Subscriber Metrics

Let me start by saying that AT&T has been spending aggressively towards its nationwide 5G wireless and fiber broadband rollouts. Its capital expenditure amounts to a gargantuan $19.4 billion in the last twelve months alone, which is significantly higher than several smaller telecom companies combined. AT&T’s management went on this spending spree in the hopes that it’ll bring a mass influx of satisfied customers. So, the first order of business when AT&T reports its Q2 results, is to assess whether AT&T management’s plan is working, by measuring its customer stickiness.

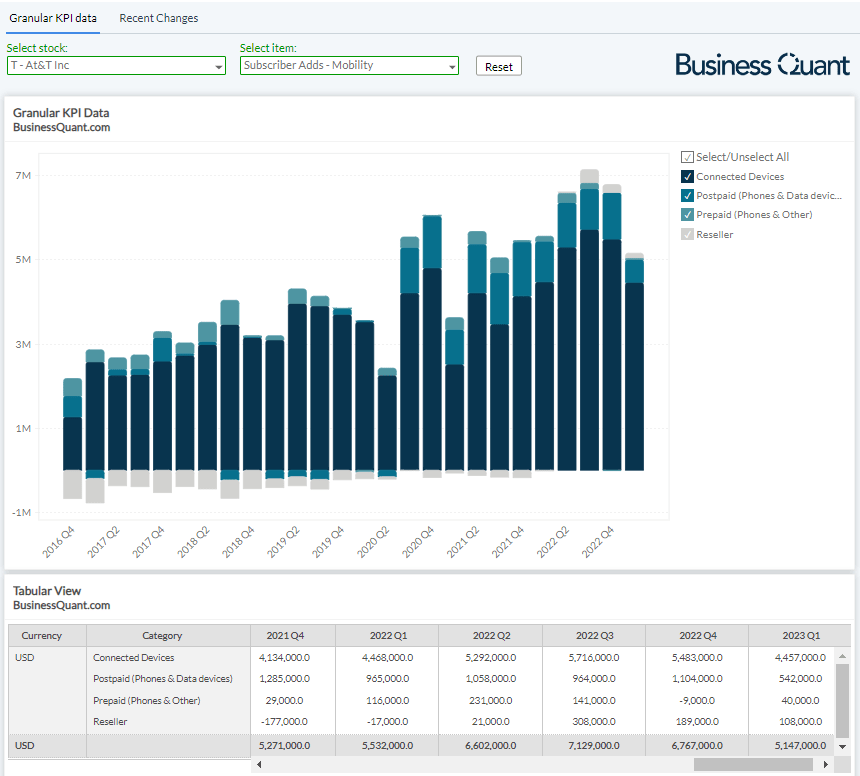

We can start by looking at AT&T’s wireless subscriber additions during the quarter. A higher number here would indicate that customers are increasingly switching to AT&T’s wireless network due to its relatively better value proposition (pricing, speed, coverage, customer support etc.). On the other hand, a sharp decline here would raise concerns around AT&T’s execution, competitiveness and even point to a saturating market. With that said, I personally expect AT&T’s subscriber adds to be in-line with its recent quarters in light of its nationwide 5G rollout, much ahead of its smaller peers.

{kind=link}

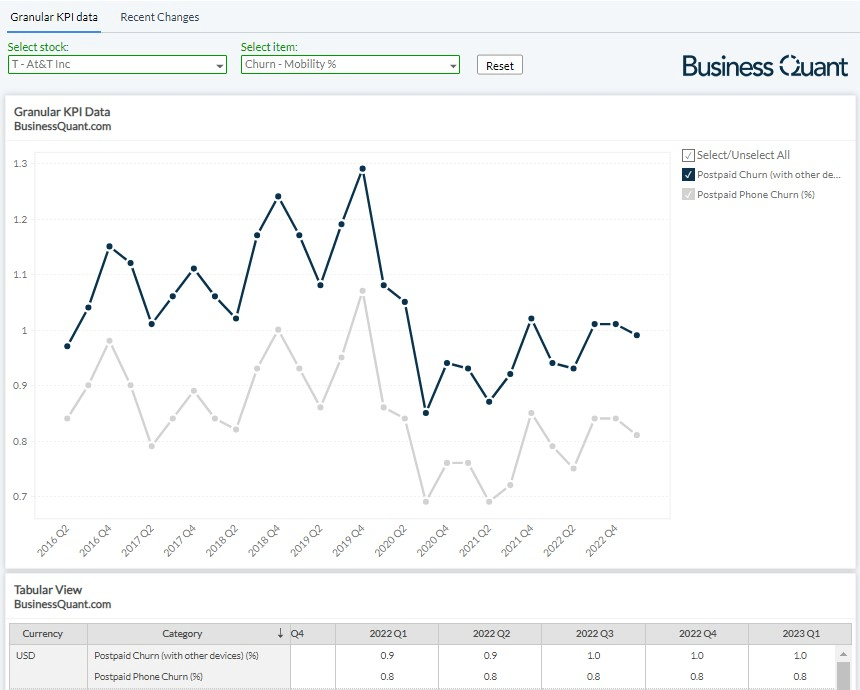

Secondly, pay close attention to AT&T’s churn rate. This metric essentially highlights the pace at which its subscribers are disconnecting their wireless connections. A sharp rise in the metric would indicate that a broad swath of AT&T’s subscribers isn’t satisfied with the mobility experience. Although, I think AT&T’s churn will remain flat or decline further in Q2. I say this because AT&T hasn’t hiked its prices across all its wireless plans, but Verizon ( VZ ) has. This means AT&T’s price-sensitive subscribers are less likely to migrate away to the next-best telecom behemoth, namely Verizon.

{kind=link}

With that said, let’s now shift attention to AT&T’s financials.

Free Cash Flow Trends

With AT&T’s aggressive capital expenditure to reinvigorate its growth engine, the company’s free cash flows have come under pressure of late. To put things in perspective, the company delivered non-GAAP free cash flow of $14.1 billion during FY22, but it was lower than its management’s initial guidance of $16 billion.

For FY23, AT&T’s management estimates that the figure will amount to $16 billion. However, its non-GAAP free cash flow in Q1 amounted to just $1 billion. This means it would be an uphill task for the company and its management to meet their GAAP free cash flow guidance in the next three quarters.

The problem here, for investors, is that if AT&T has a quarterly dividend bill of a little over $2 billion. Plus, it has upcoming debt maturities of over $4.2 billion that are due for this year. If AT&T’s free cash flow doesn’t pick up anytime soon, it may be forced to slash its dividend payouts in order to prioritize debt payments and/or cut back on its capital expenditure.

With that said, I had explained in a prior article how AT&T’s free cash flow was unusually distressed due to strong device sales during the holiday season. I don’t anticipate a drawdown of this magnitude to occur again in Q2 and, so, my guesstimate is that AT&T’s free cash flow will amount to over $2.5 billion in Q2.

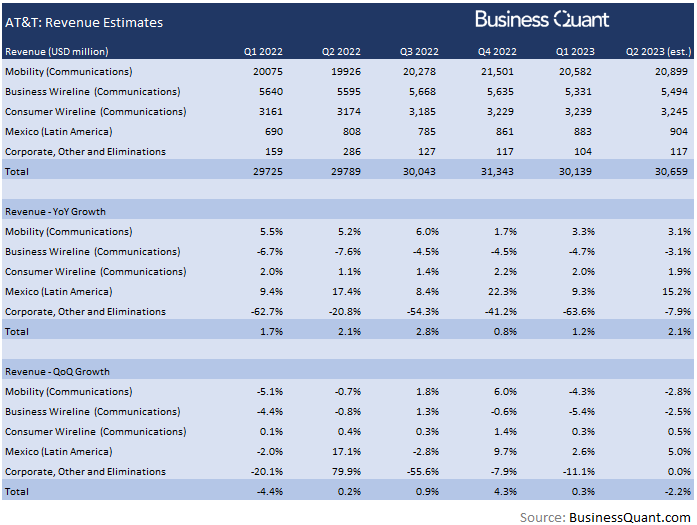

Revenue Estimates

Moving on, AT&T’s revenue is divided amongst five streams. Amongst them, Mobility is by far the largest revenue driver for the company, with its sales contribution exceeding 68% in the last quarter. It’s worth noting that AT&T’s Mobility business is seasonally strong in Q3 and Q4 as the holiday season approaches, but relatively weaker in Q1 and Q2. I expect this element of seasonality to prevail this time as well, and estimate Mobility revenue to decline 2.8% sequentially in Q2, with revenue amounting to $20.89 billion.

Next, AT&T’s Business Wireline business has been in a state of downtrend as legacy broadband disconnections, price cuts and growing competition have been rampant. Although the company is adding fiber business subscribers, the pace isn’t rapid enough to offset the overall decline in the business wireline segment. So, in light of this broad trend, I estimate this revenue stream to contribute roughly $5.49 billion to AT&T’s overall top line, down 2.5% sequentially.

Moving on, AT&T’s consumer wireline revenue is likely to remain flat compared to Q1. The segment has been growing marginally every quarter as the company has been able to bundle packages together, roll out fiber broadband in underpenetrated areas and be competitive with its pricing. Hence, I’m estimating AT&T’s consumer wireline revenue to grow 0.5% sequentially during Q2, with its revenue coming in around $3.2 billion.

The remaining two segments, Mexico wireless and Corporate, are immaterial to AT&T’s overall financials as they contributed just 3.3% to the telecom giant’s overall sales last quarter. So, I don’t have a granular estimate of the same and have a broad guesstimate that they’ll collectively contribute a little over $1 billion in sales during Q2.

{kind=link}

This brings us to a company-wide revenue estimate of $30.65 billion. Bear in mind that I was extremely conservative with my estimates and yet, my revenue estimate is higher than the Street’s estimates that are currently spanning from $29.59 billion and $30.35 billion. Therefore, I opine that AT&T is poised to beat the Street’s revenue estimates in its upcoming Q2 earnings report.

Final Thoughts

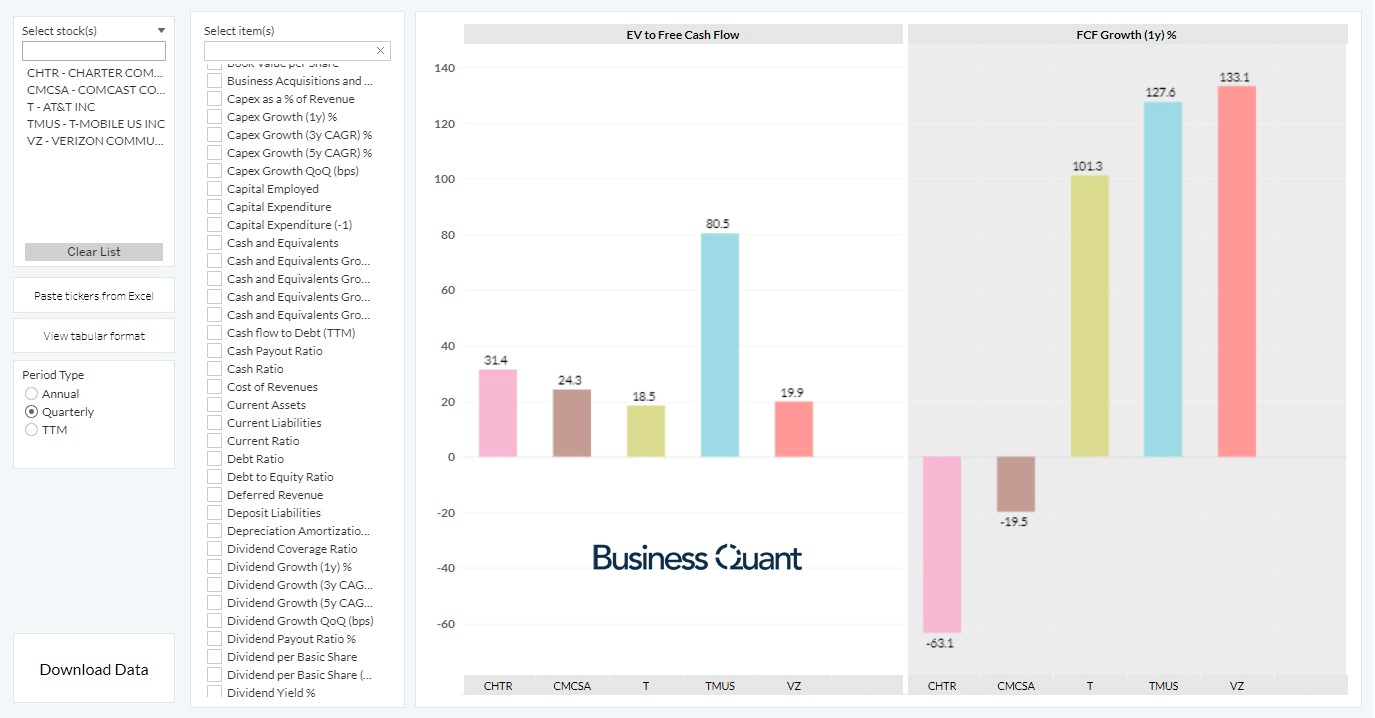

At the time of this writing, AT&T’s EV-to-Free Cash Flow multiple equates to a little over 18-times. This may seem high in isolation but it’s actually much lower than its closest comparables, in spite of growing its GAAP free cash flow at an elevated rate last quarter. So, I find AT&T’s shares to be undervalued when comparing it with its peers.

{kind=link}

When it comes to Q2 earnings, though, the prominent risk factor is that AT&T could fail to deliver on its free cash flow and revenue. This can fuel bearish speculation around the company’s growth prospects and its dividend sustainability. However, given the stock’s low valuation, it seems like most of the bad news is already priced in.

The company seems set to post healthy free cash flow growth in Q2, beat the Street's estimates and register healthy subscriber metrics. All this is happening whilst its shares are relatively undervalued. As a result, I contend that AT&T is a buy heading into its earnings. Good Luck!

For further details see:

AT&T Q2: Buy Before It Soars