TBC - AT&T: The Capital Squanderer

2023-07-31 05:24:19 ET

Summary

- AT&T's poor capital allocation has resulted in negative returns for investors, with a lack of direction in its growth strategy and numerous unsuccessful M&A deals.

- AT&T's large amount in debt is worrying as interest rates move higher and bonds will need to be refinanced at higher rates.

- Future expected returns are in the single digits.

Warren Buffett has a great quote which describes the situation AT&T ( T ) is in well:

In any case, why potential buyers even look at projections prepared by sellers baffles me. Charlie and I never give them a glance, but instead, keep in mind the story of the man with an ailing horse. Visiting the vet, he said: 'Can you help me? Sometimes my horse walks just fine and sometimes he limps.' The vet’s reply was pointed: 'No problem – when he’s walking fine, sell him.' In the world of mergers and acquisitions, that horse would be peddled as Secretariat.

I'll go over why this quote describes AT&T so well. Firstly many investors put far too much emphasis on projections put out by the management of AT&T and history shows that those projections were way off and in the long run AT&T has massively underperformed the market. The biggest part of the quote that hits home is the story of the ailing horse. AT&T is an ailing horse in that there are times when it looks as if it will recover and outperform and it always ends up disappointing investors; investors will end up buying in at the top of the market when the horse walks just fine, then they end up selling a lot lower when the horse is limping; this cycle will repeat again and again.

AT&T's History Of Dreadful Capital Allocation

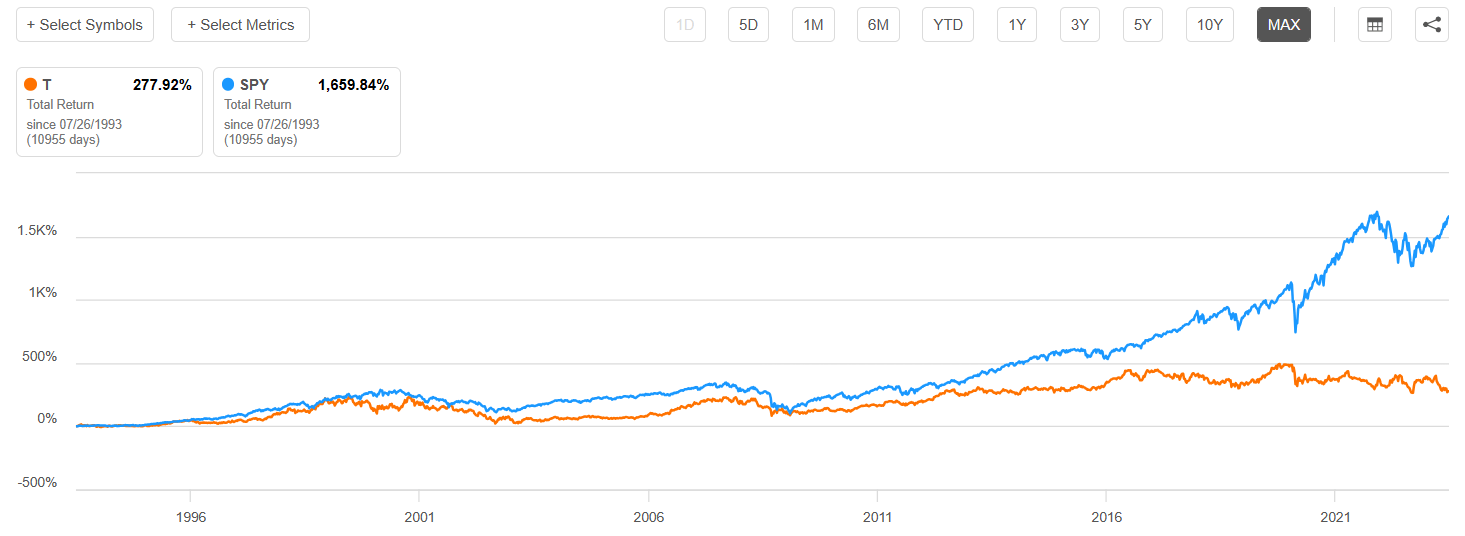

Below is a chart of the total returns of the S&P 500 against AT&T since 1993 (the farthest back Seeking Alpha's data goes):

{kind=link}

Seeking Alpha

The blue line is the S&P 500 while the orange line is AT&T. When a profitable company like AT&T, which wasn't overvalued by traditional valuation metrics in 1993, underperforms this badly it's a sign that there's been terrible capital allocation of the retained earnings.

To put numbers on it, the CAGR (including reinvested dividends assuming no dividend taxes) of AT&T's stock has only been 3.4%. Once we take into account dividend taxes and inflation the real rate of return ends up being negative.

To make this worse over the course of AT&T's history a majority of its profitability has been returned to shareholders via dividends , meaning that retained earnings actually created a deeply negative return. Seeking Alpha for example grades AT&T's dividend consistency as an F.

The reason for this value destruction is AT&T's many M&A deals and its lack of direction in its growth strategy.

For those who don't know the history behind AT&T, I'll provide a brief synopsis. AT&T spent the early and mid-20th growing itself into a monopoly by acquiring smaller telecoms. This built themselves into the biggest company in the world and due to their monopoly, they were able to have artificially wide margins and a lack of competition. In 1984 the government is pressured to break up what is perceived to be an anti-competitive corporation. They broke up the company by spinning off seven regional operating companies to provide competition to the parent company AT&T.

In my opinion, this was the beginning of the end for AT&T. Prior to this AT&T had a deep pricing moat and was able to grow by expanding its operations and acquiring other operations and doing so with a high return on invested capital. This allowed the company to compound its profitability. Once the company was broken up it lost this advantage and had no growth trajectory.

AT&T then tried to grow by acquiring other companies which it thought would be accretive, but the issue was the targets were not accretive and AT&T way overpaid. This can be seen when looking at its balance sheet and comparing it to its biggest competitor, Verizon (VZ).

When looking at AT&T's balance sheet it has $408 billion of total assets, $290 billion of total liabilities, and $101 billion of common equity.

In comparison, Verizon has $379 billion in total assets, $283 in total liabilities, and $95 billion in common equity.

When doing a basic comparison like this both companies seem similar since the three line items are very similar. The big difference here is the blemish on AT&T's balance sheet from goodwill.

AT&T's goodwill is $67 billion, while that of Verizon is $28 billion.

In an asset-heavy business such as telecommunications, there shouldn't be any goodwill on a balance sheet. The goodwill here represents that these two telecommunications companies paid far too much for acquisitions, many of which later ended up spinning off in AT&T's case.

To be fair to AT&T, Verizon's balance sheet also has many of the same issues, but just not to the extent that it does.

Both balance sheets also have a lot of "other intangibles" which represent non-physical items that should, in theory, offer value to the company. The reality is that both AT&T and Verizon acquired or merged with other companies that likely had this line item on their balance sheet so they simply inherited it, even if now the intangibles aren't worth what it states on the balance sheet. Again this is another sign of overpaying for acquisitions but in this case, it is overpaying for intangibles that are worth little in the future.

I'm not going to go into detail about each and every M&A deal that AT&T has done, but I will provide a list of major deals.

- 1991: Acquires NCR for $7.4 billion

- 1997: Acquires TCI and MediaOne for $100 billion

- 2005: AT&T merges with SBC Communications

- 2006: BellSouth gets acquired by AT&T

- 2011: AT&T wants to acquire T-Mobile, but regulators blocked the deal and AT&T pays a $4 billion breakup fee, $3 billion in cash and $1 billion in intangibles in spectrum rights.

- 2015: Acquires DirecTV

- 2016: Acquires Time Warner

These are some of the notable M&A deals that AT&T has done but keep in mind there are far too many to be listed here.

All of these deals offered little value to AT&T at best and a permanent loss of capital at worst. For readers who want more information on each of these deals, the hyperlinks lead to sources that provide a great starting point for deal-specific research.

Busted Business Model

My view is that the telecommunications industry as a whole has a busted business model.

Telecommunications has turned into a consumer staple commodity. This comes with both pros and cons. The main upside is that no matter what happens to the economy people will always pay for cell service. The downside of a commodity-like offering is that all the carriers have to compete on price. The three big carriers, AT&T, Verizon, and T-Mobile are constantly coming out with offers to entice consumers to switch. It has gotten to the point where consumers will sign a two-year contract with one carrier with a great deal, then once the two years are over they will look for another carrier offering the same great deal; the process is repeated again and again. Just as an example I've gone from Sprint to T-Mobile to Xfinity Mobile (which uses the Verizon network) over the last few years by continually taking advantage of new deals that they provide. I will likely switch from Xfinity if I can get a better deal elsewhere. In the manner that I have consumers continually shop around for the best deals at the detriment of the profitability of these firms.

Also, once consumers see a product or service as a commodity they are unlikely to change their mindset on it. The only way for AT&T's services to not be seen as a commodity is for them to build a moat around their offering. This means that they would need to offer something that their competitors can't and build an ecosystem around it. An example would be the iPhone and the ecosystem Apple has built around it. It is unlikely AT&T will be able to do this with the financial position they are in and with the legacy management they have.

As for M&A growth, we know that history shows that it hasn't worked well for AT&T. The only M&A growth that I see being accretive would be for them to merge with a competitor, which regulators are unlikely to approve.

Debt To Lower Shareholder Returns

Of course, no discussion of AT&T's M&A past can be had without discussing the massive debt it has created.

AT&T's balance sheet is very deceptive, in that a lot of the assets aren't really assets, just a sign that AT&T is overpaying for companies such as Goodwill which was highlighted above. This is why the total common equity comes out to $101 billion, but when we remove all intangible assets, the total common equity would actually be $-96 billion. This really shows the severity of the situation AT&T is in and how they are deeply underwater on their debt.

The biggest issue I see here is that most of this debt will have to be refinanced at significantly higher rates. Long-term debt is at $127 billion. High credit-rated corporate bonds are yielding around 7% while the risk-free rate is expected to be 6% just a few months from now. The ICE BofA B US Corporate Index Effective Yield is currently 8.23%. 8.23% interest on AT&T's long-term debt is $10.4521 billion per year in interest expense. TTM EBIT or Operating Income is $27.599 billion; once we subtract out $10.4521 billion per year in interest expense, we're left with $17.1469 billion in pre-tax earnings. That's $13.546 billion after a 21% corporate tax is subtracted, which brings the stock to around a 13% earnings yield. A 13% earnings yield is enough to sustain the dividend, but little beyond that.

My view is that AT&T will continue to pay the current dividend, but everything else will go into paying down debt. While it would be wiser to completely cut the dividend and completely focus on paying off debt, AT&T management is likely aware that if they do that then the stock price will further fall as at that point there is really no reason for most shareholders to own the stock other than the yield.

My long-term return expectation is just the dividend yield of around 7.65%. This is because as history shows retained earnings are wasted by management on the wrong growth opportunities or on buyouts, so I wouldn't count on any returns from that, in fact, we're being generous by not having a negative return on retained earnings. The best case scenario I see for AT&T is that they decide to return all earnings to shareholders via dividends or buybacks because history shows negative returns on retained earnings.

With corporate debt yielding above the long-term expected return I would expect a multiple contraction. AT&T's earnings multiple would need to further contract to bring expected returns into the double digits for it to be worth it for investors to invest in the stock rather than its debt which will likely yield around 8%-9%.

Also, if we compare AT&T to its main rival Verizon, Verizon trades at a lower P/E multiple while arguably having a higher quality balance sheet, so from a mean reversion perspective the multiple that AT&T trades at would need to go down to that of Verizon's.

For these reasons, even with the price this low, I wouldn't buy AT&T unless the price went significantly lower and in that case I'd treat it as a cigar butt trade.

The Bottom Line

The bottom line here is simple. AT&T is the horse that Warren Buffett describes. With the most recent earnings report, the horse seems to be going through a phase where it walks completely fine right now, but as history shows that could change at a moment's notice.

Until AT&T's management is able to put a large focus on paying off debt in the short term and a better capital allocation strategy in the long term, I wouldn't expect great long-term results from it. Also, as mentioned in the article AT&T lacks a moat and competitive advantage over others in the same industry.

When it comes to valuation AT&T is arguably still pricey as the expected return is only in the single digits once accounting for higher interest expenses going forward.

For these reasons, I wouldn't buy AT&T here, nor would I short it due to its price having already gone down a lot. Instead, the only play here is to potentially wait for the price to go even lower to the point where it gets into deep-value cigar butt territory and make a long trade from there. The only other out-of-left-field bullish play is that activist investors step in to completely sack the current board and start all management from scratch; in the near term this is unlikely to happen.

For further details see:

AT&T: The Capital Squanderer