BELFB - Atai Capital Management Q3 2023 Letter

2023-11-30 10:00:00 ET

Summary

- Atai Capital experienced a decline of 5.8% in the third quarter, bringing year-to-date returns to 6.5%.

- The intrinsic values of several businesses increased in the third quarter, but share prices remained disconnected from reality.

- Risk should be defined as the likelihood of a permanent loss of capital, not volatility. Volatility allows for the purchase of shares at a discount.

Dear Partners,

Atai Capital experienced a decline of 5.8% in the third quarter, bringing our year-to-date (YTD) returns to 6.5% net of all fees. This compares to a 13.1% total return for the S&P 500 YTD and a 2.5% total return for the Russell 2000 YTD.

While quarterly declines can certainly be frustrating, it’s important not to let ourselves be distracted by these quarterly fluctuations and instead focus on the health and performance of our businesses. I want to emphasize that we will likely face periods of significant declines over the years that far exceed what we’ve experienced this quarter, but that is simply the price of admission in our pursuit of outsized returns.

While the intrinsic values of several of our businesses saw an upward trend in the third quarter, the same cannot be said for their share prices; not only do they remain disconnected from reality, but they further distanced themselves from this reality throughout the quarter. This should not be considered an uncommon occurrence, though, and is the exact “value arbitrage” we try to exploit by purchasing shares at a discount to their intrinsic values. Returns have improved post the quarter but still trail the S&P 500 ( SP500 , SPX ) as of writing.

What Is Risk, And How Should We Think About It?

This is an incredibly nuanced question, but at its core, I believe risk can be defined as the likelihood of a permanent loss of capital. Before we explore that definition of risk more thoroughly, let's first identify what risk unequivocally is not – volatility.

If you were to attend almost any business school in the country, you’d more than likely be taught that risk can be equated to volatility, or at a minimum, you’d be taught a few useless but intellectually stimulating formulas such as the capital asset pricing model (“CAPM”), which utilize volatility as their input for risk. While labeling risk as volatility is convenient for college professors due to its measurability – which makes it suitable for teaching, grading, and use in formulas – it doesn’t change the fact that this definition of risk is asinine.

On average, individual stocks experience fluctuations of around 80% in any given year. When we pause to contemplate the fact that every share represents a fractional ownership in an underlying business, this notion that the fundamental value of most enterprises undergoes such substantial swings in a single year is nothing short of ludicrous. Moreover, volatility also disregards price and valuation entirely. For example, in theory, Google ( GOOG , GOOGL ) at $500 could have the same Beta (a measure of volatility) at its current price of $130. In this example, it doesn't take much common sense to recognize the flaw of using volatility as a measure of risk. Google is undoubtedly a great business, but at $500, it would be significantly more expensive than it is today, carrying a higher level of risk and lower prospective returns. The inverse scenario is applicable here as well, and If Google were to experience a swift 50% decline, a professor would likely tell you it’s now riskier, but I would argue that Google at $65 would represent a remarkable bargain today!

Still, none of the above examples (or numerous other examples) seem to stop plenty of “supposed” value investors from utilizing CAPM or frequently quoting their “risk” adjusted returns. These “value investors,” despite believing that they can purchase shares at a discount to their intrinsic values, are in direct contradiction to their own beliefs when utilizing formulas such as CAPM. Furthermore, by quoting risk-adjusted returns, they are essentially claiming that they can predict future volatility, which is inherently unpredictable and changes daily! This strange scenario serves as a textbook definition of cognitive dissonance, and it is deeply ingrained in many of Wall Street’s fundamental investors. So why is this? Why did colleges start teaching this dribble, and why does Wall Street love it so much? I’ll let Charlie Munger explain: “I finally figured out why the teachers of corporate finance often teach a lot of stuff that’s wrong. When I had some eye troubles very early in life, I consulted a very famous eye doctor. And I realized that his place of business was doing a totally obsolete cataract operation. They were still cutting with a knife after better procedures had been invented. I said, “Why are you in a great medical school performing absolutely obsolete operations?” And he said, “ Charlie, it’s such a wonderful operation to teach. ” Well, that’s what happens in corporate finance. They get these formulas, and it’s a fine teaching experience. You give them a formula, you present the problem, they use the formula. You get a real feeling of worthwhile activity. There’s only one problem; it’s all balderdash. ”

Adding onto Charlie’s story here, graduates exposed to these formulas and ideas eventually land roles in wealth management and subsequently end up managing portions of different university endowments. These endowments typically ascribe to an academic belief system, and because of this, many managers are usually held to that same belief system, and if they want any capital from the university, they’ll oblige – this is a perfect example of how incentives drive outcomes!

Another reason why these formulas and ideas are continually used post-graduation is simple. These graduates were provided a set of tools, and to a man with a hammer, everything ends up looking like a nail!

So, what is risk if it’s not volatility? As mentioned, I believe that risk can be defined as the likelihood of a permanent loss of capital. The reasons for these potential losses differ significantly and are usually specific to each investment. Every investment has individual business risks that they don’t always share with other investments. Every business/situation is unique, and every business/situation should be treated differently – It’s worth noting that volatility fails to capture business risk.

I can’t quantify business risk in most instances, and trying to do so is mostly pointless in my opinion; there are usually too many of them, too many moving parts, too much that is unknown, and they are too different from each other for me to assign some risk score and compare that with my other opportunities. Instead, I qualitatively consider these risks when sizing positions and prefer only to bet big on ideas where I believe the chances of a permanent loss of capital are small instead of betting big on what might have the most upside. Because of this, our portfolio is typically weighted towards ideas where I believe the most substantial margin of safety exists rather than the highest IRR available to us.

I think it’s important that I clarify what a margin of safety is; many investors wrongly equate a margin of safety to how cheaply they can buy something and believe a lower price provides them with a more significant margin of safety and, therefore, lowers risk – I strongly disagree with this notion. While buying fifty cents for a dollar is undoubtedly the idea, that is only one component in the margin of safety equation; the other is business quality, more specifically, the quality of the cash flows the business generates and how likely we, as minority shareholders stand to benefit from those cash flows. Purchasing a coal miner at a 20% discount to its book value does you no good if coal prices fall 50%; purchasing a great business at a discount does you no good if there is a controlling shareholder who only cares about filling his own pockets, and buying a melting ice cube at a 25% cash flow yield does you no good if the business isn’t going to exist in three years and its residual assets are worthless. I could go on and on, but this component in the equation is one that many value investors seem to ignore or overlook entirely. Your margin of safety is NOT determined by the price you pay but rather by a combination of both price AND quality; making an investment without consideration for both is a recipe for disaster.

Instead of viewing volatility as a form of risk, I believe it’s better to view it as the mechanism that allows us to purchase shares of businesses at a discount to their intrinsic values. However, utilizing this mechanism is not without cost, and the compromise we make is enduring occasional short- term pain in our investments, which will experience unjustified significant declines as well. While the value of our shares would be temporarily impaired in these instances, the value of the businesses they are attached to is not. Volatility is a friend of the long-term investor, not a risk, and it allows us to purchase shares at a discount and sell them for their fair value or, better yet, at times, a premium.

Okay, so why am I giving you this long tangent on risk? Part of my job as a fund manager, more specifically, one running a concentrated long-only portfolio, is to help inform my fellow partners (and future partners) about my thought process and why I do the things I do. The goal of doing so is that you can hopefully sleep easier when we inevitably face substantial drawdowns. I have no idea when these drawdowns will occur, but they will happen, and it’s not your job to understand the businesses we own intimately; that’s what I’m paid for after all! However, since I am in the advantageous position of intimately knowing what we own, it will make these drawdowns more tolerable for me than many of you. Still, I hope that by continually being transparent and sharing how I think about things will make these times more bearable for you all as well. Having partners who understand our investment strategy and process is critical to the long-term health of this partnership, and rest assured that I will continually turn down those who are not a good fit!

Bel Fuse ( BELFA , BELFB ) Case Study:

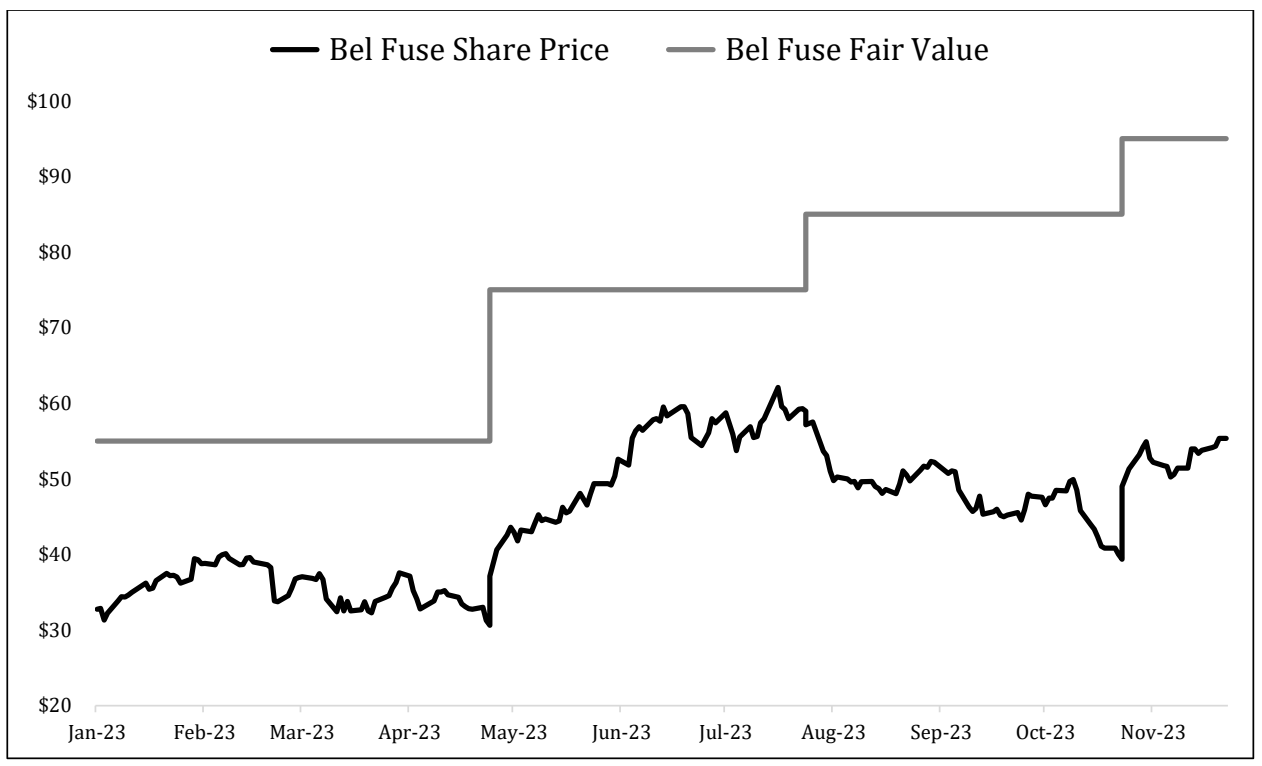

Since I just spent some time explaining how I think about risk and volatility, I wanted to provide you with a real-world example of why price fluctuations should be ignored; luckily, one of our portfolio companies makes for a perfect example. Below, you’ll find a year-to-date chart of Bel Fuse, and since the start of the year, Bel’s share price has experienced a 100%+ increase from trough to peak and two declines that were more than 30%. I would argue that Bel Fuse’s fair value is far above today’s share price, and the two 30% declines don’t represent Bel Fuse’s fair value declining or its risk increasing. Nevertheless, Bel’s shares apparently like to sell off materially heading into most of its earnings; these declines are on the back of what I can only assume are very negative expectations from the market, but as you’ll see in the chart, once Bel Fuse reports the share price quickly corrects as negative expectations are proven wrong time and time again, and the magnet that is intrinsic value continually pulls Bel’s share price higher over time.

{kind=link}

If we had fallen victim to share price volatility and tried to discern risk from it, we might have made the poor decision of selling Bel Fuse as it declined, but instead, we did the opposite, and every time it traded down, we bought more. Usually, when a stock starts selling off on no news, you’ll see other investors saying things like “someone knows something,” or they’ll be frantically searching for a reason for the selloff. The truth is a lot of the time, there isn’t a reason, or the reason is extraneous. During those times, it’s essential to take a step back and remember there is a business attached to every share, and as long as the fundamentals are intact, we should have no problem telling the market it’s wrong by purchasing more shares at a discount.

Portfolio Commentary

We added two smaller ideas throughout the quarter and increased our size in a few existing positions. As for turnover, we sold out of a small position in Computer Task Group ( CTG ) after the company announced it was getting acquired. Activision Blizzard ( ATVI ) also exited the portfolio during the quarter; we captured most of the spread, selling our shares in the low 90s for an attractive IRR after a somewhat turbulent journey.

Enad Global 7 ( ENADF ) & Sunday’s Idea Brunch

I usually like to try to include a new idea or two in these letters, but that will likely slow down to one or none moving forward. Nevertheless, you can still anticipate updates on some of our previously disclosed positions. With that in mind, I don’t have anything new for you this quarter, but for those who missed it, we published a relatively comprehensive 66-slide deck on Enad Global 7 in mid- October – you can find a copy here.

Furthermore, in early November, we did an interview for Sunday’s Idea Brunch, where we talked about ALOT , EG7, BELFB , and what our research process usually looks like in the first hour – for those of you who missed it, you can find a full-length version here.

Conclusion

From my writings, you might discern my deep admiration for Charlie Munger. It saddens me to convey that he passed away at the age of 99 just yesterday. If someone were to ask me who my idol was, it would have been Charlie. He has had a tremendous influence on me as an investor and in life, and I will always be grateful for the seemingly endless wisdom he has shared over the years. He and his clever one-liners will be sorely missed – truly one of a kind.

As a reminder, we are open to new clients, and if you know someone who might be a good fit, please feel free to pass my contact information along – we do plan on increasing our fees for new clients sometime over the next year and will be sunsetting our Founder’s class fee structure.

As always, I am humbled by and grateful for the opportunity to invest your capital alongside my own, and I will continue to make every effort to compound that capital at attractive rates.

Cordially,

Brandon Daniel, Founder & Portfolio Manager Atai Capital Management, LLC

“ The first rule of a happy life is low expectations, and I was good at having low expectations. ” – Charles Thomas Munger

Disclaimer:This letter expresses the views of the author as of the date cited, and such views are subject to change at any time without notice. The information contained in this letter should not be construed as investment advice, and Atai Capital Management, LLC (“Atai Capital”) has no duty or obligation to update the information contained herein. This letter may also contain information derived from independent third-party sources. Atai Capital believes that the sources from which such information is derived are reliable; however, Atai Capital does not and cannot guarantee the accuracy of such information. References to stocks, securities, or investments in this letter should not be considered investment recommendations or financial advice of any sort. Any return amounts that are reported within this letter are estimated by Atai Capital on an unaudited basis and are subject to revision. Atai Capital’s returns are calculated net of a 1.50% annual management fee and reflect a client’s performance who would have joined the firm on its inception date. Actual Individual investor returns will vary based on the timing of their initial investment, the impacts of additions and withdrawals from their account, and their individually negotiated fee structure. Atai Capital believes showing returns net of a 1.50% management fee better reflects actual performance as of 11/29/2023 since no account that Atai Capital currently manages is charged a fee more than the stated 1.50% management fee. Past performance is no guarantee of future results. Index returns referenced in this letter include the S&P500 and Russell 2000. Atai Capital’s returns are likely to differ from those of any referenced index. These returns are calculated from the respective provider’s websites, S&P Global Homepage for the S&P500, and FTSE Russell Indices, Insights & Data for the Russell 2000, and include the reinvestment of all dividends in both cases. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Atai Capital Management Q3 2023 Letter