CMPS - Atai Life Sciences: A Promising Venture In The Psychedelic Therapy Market Trading Below Cash Value

2023-11-29 18:55:54 ET

Summary

- ATAI Life Sciences is a biopharmaceutical company focused on developing psychedelic-based treatments for mental health conditions.

- The company has a diverse portfolio of drug candidates in various clinical trial phases, showing promising results.

- ATAI's stake in COMPASS exposes it to the promising COMP360 IP, currently in phase 3 with a delineated pathway to a potential FDA approval.

- ATAI trades below its cash and book value, making it an attractive speculative investment opportunity.

Atai Life Sciences N.V. ( ATAI ) is a promising clinical-stage biopharmaceutical company that creates and funds businesses focusing on developing psychedelic-based treatments. Psychedelics can potentially help patients with conditions such as Treatment-Resistant Depression ((TRD)), generalized anxiety disorder, PTSD, and substance abuse, among others. However, ATAI's approach with psychedelics is encouraging because initial results suggest that it has relatively low side effects and is highly effective even with a single dose. Thus, this makes ATAI a nice investment in alternative treatments for the current suite of antidepressants and medications. Consequently, given that ATAI trades below its cash and book value, I think it’s a good speculative investment at these levels.

Business Overview

ATAI Life Sciences N.V. is headquartered in Berlin, Germany, with offices in London and New York. The company was founded in 2018 to create, develop, and acquire businesses formulating psychedelic therapies to achieve mental health through decentralized drug development. ATAI's research on psychedelic-based therapies is derived from drugs like DMT, MDMA, and Psilocybin that produce changes in perception, mood, and cognition.

However, applying variations of these drugs is developed with therapeutic purposes in mind. For instance, psilocybin and DMT affect the 5-HT2A receptors, part of the serotonin system, and lead to altered consciousness states that could produce healing when complemented with the support of therapists in clinical settings. These drugs can be used to achieve improvements in mental health disorders like depression, PTSD, and abuse of substances. They are indicated, particularly in cases where traditional treatments have been ineffective, thus making psychedelics a potential new treatment field from which ATAI could benefit.

I.P. Portfolio and Financing

Currently, ATAI has the following affiliated companies : Viridia Life Sciences for the research of treatment-resistant depression with the VLS-01 / DMT drug that is in clinical trials Phase 2; Recognify Life Sciences, which studies cognitive impairment associated with schizophrenia and produces RL-007 / Compound a neuromodulator in Phase 2; DemeRx IB for opioid use disorder developing DMX-1002 / Ibogaine that is in Phase 1; GABA Therapeutics, looking for solutions for generalized anxiety disorder producing GRX-917 / Deuterated etifoxine that is in Phase 2; and EmpathBio for post-traumatic stress disorder with EMP-01 / MDMA derivative a drug in Phase 1.

This means ATAI currently needs something on phase 3 in its pipeline, which makes it a highly speculative and long-term investment prospect. This is because going from Phase 2 to Phase 3 often takes 3.6 years, and from Phase 3 to FDA approval, it takes another 1.3 years, on average . Hence, we can assume that given ATAI’s current I.P. portfolio, it’s still roughly 4.9 years away from generating meaningful revenues from its I.P. Naturally, this is an average estimate, and ATAI’s timeline might differ significantly. Yet, I think it’s a good reference point for assessing ATAI’s prospects.

{kind=link}

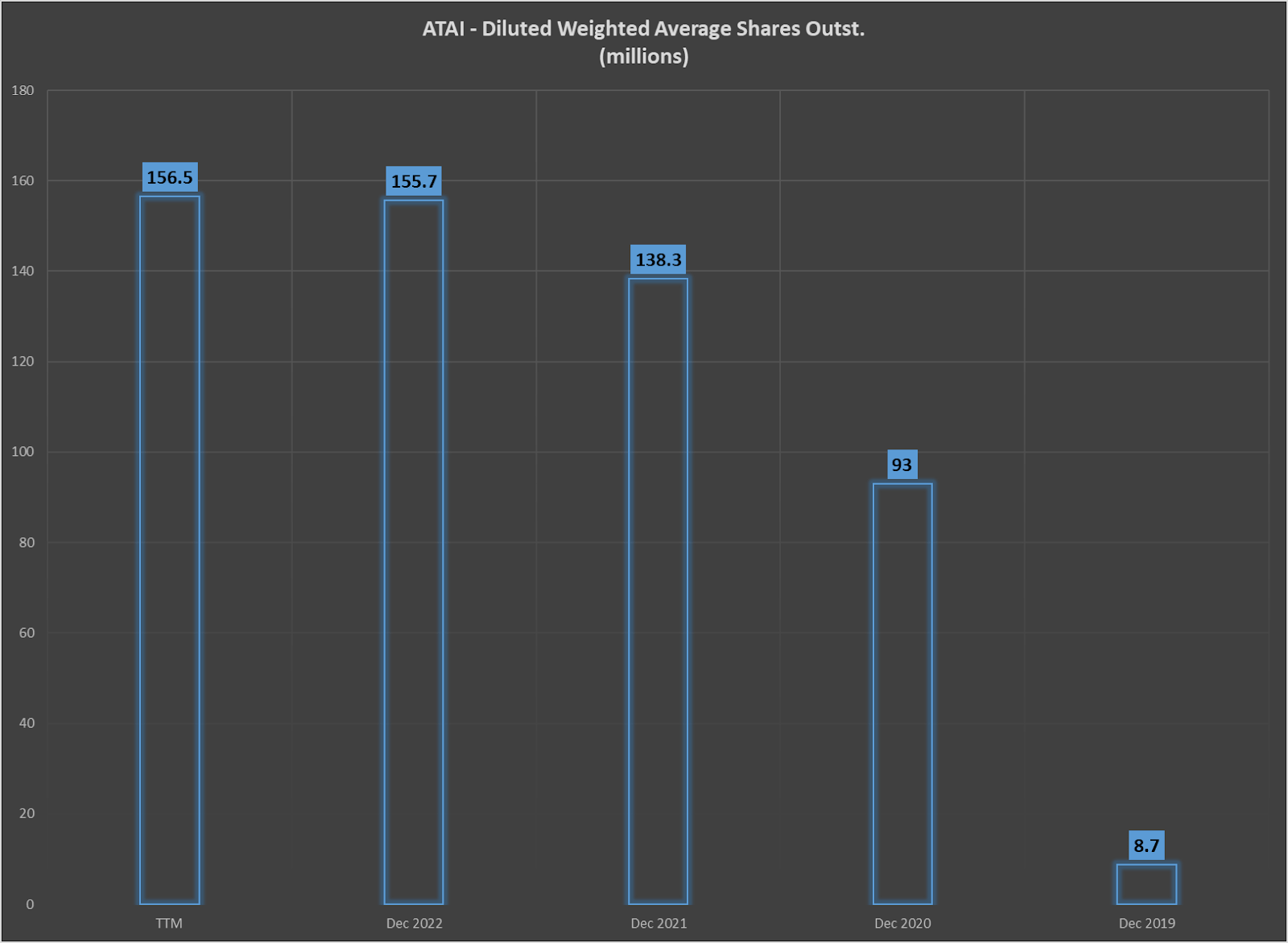

After all, since 2019, the company has mostly financed its operations through equity , diluting shareholders along the way. Thus, given that ATAI likely has more years without significant revenues ahead, it’s not out of the question that it’ll have to at some point. For context, in 2019, ATAI’s diluted weighted average outstanding shares were 8.7 million, but for the latest report, this number increased to 156.5 million. This is a whopping 18 times increase since 2019, a massive dilution for shareholders who have owned the shares since then.

Nevertheless, ATAI also finances COMPASS Pathways ( CMPS ) with limited equity interest. CMPS develops COMP360 / Psilocybin for treatment-resistant depression with clinical trials in Phase 3; for post-traumatic stress disorder is in Phase 2; and for anorexia nervosa also in Phase 2. Interestingly, here’s the only Phase 3 drug to which ATAI indirectly has CMPS exposure.

Source: ATAI Company Presentation November 2023

CMPS’s COMP360 is indeed a promising project, and as you can see in the figure above, it’s getting close to the finish line, with a mid-2025 finish for its phase 3 trials. Naturally, there could be setbacks, as with any other biotechnology company. However, COMP360 received a Breakthrough Therapy Designation from the FDA, a key milestone for the company. Moreover, ATAI owns roughly 20.8% of CMPS, which can be an extremely valuable asset if COMP360 is fully developed and successfully commercialized. After all, COMP360 appears to be an exceptionally effective treatment alternative for TRD and similar mental illnesses. For context, a single 25mg dose of psilocybin was enough to eliminate depression in over 50% of the patients in one of CMPS’s trials. This treatment involved therapy and daily selective serotonin reuptake inhibitors, which is a novel way of dealing with TRD. But more importantly, CMPS’s approach is remarkably well tolerated and shows negligible side effects, making it a fantastic alternative for TRD.

Future Viability and Market Growth

Furthermore, ATAI has an accumulated deficit of $532.6 million, and I foresee this figure will continue to increase until one of its products gets FDA approval. As such, ATAI plans to continue investing in research, clinical trials, and operations but claims to have a cash runway that should last until the first half of 2026, approximately 2.5 years from today. This is a silver lining for current shareholders, implying that ATAI will likely not dilute shareholders for at least another year.

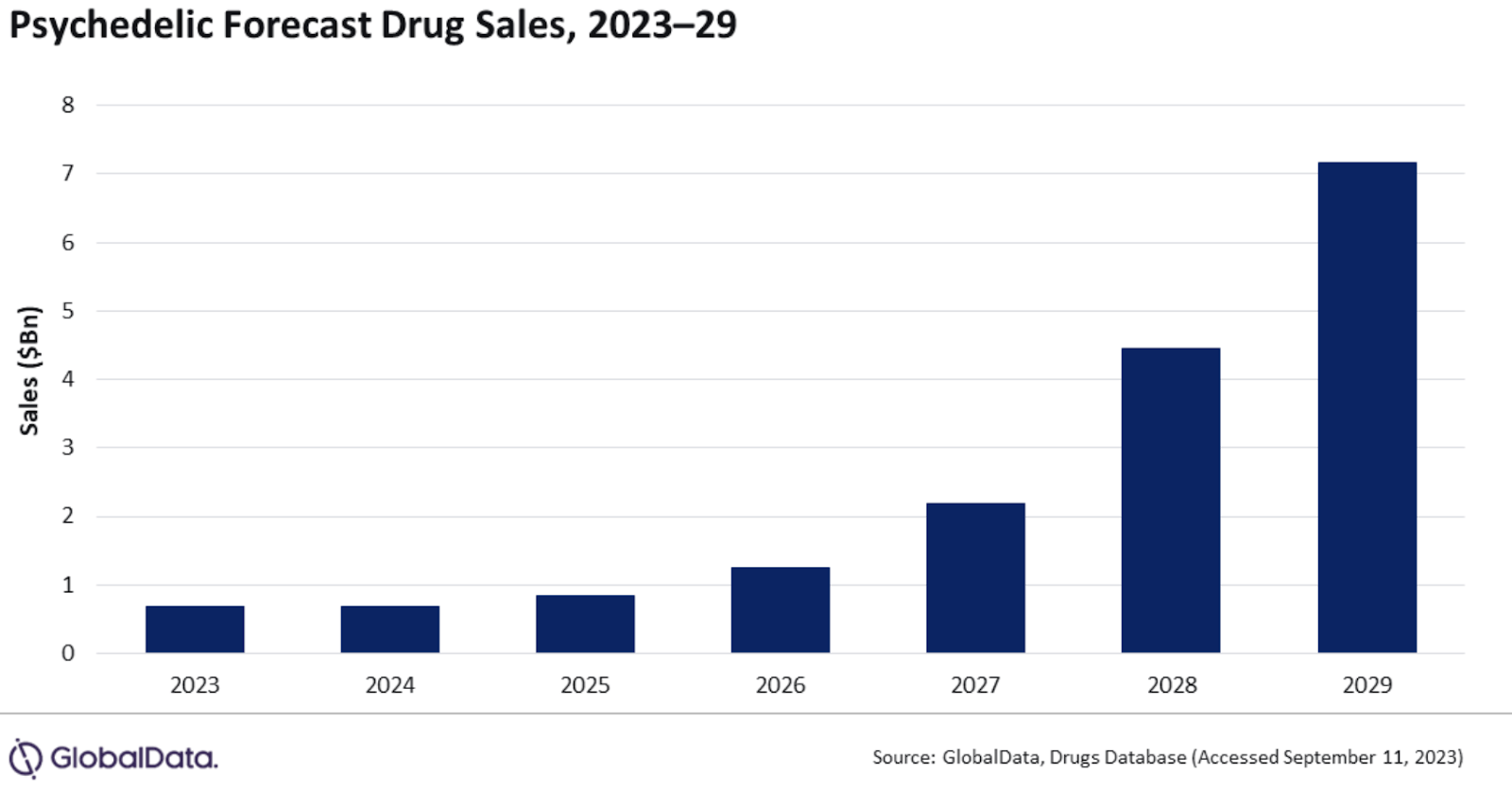

Moreover, given that COMP360 is in Phase 3 trials already and the average length to approval is 1.3 years at that stage, I’d argue that ATAI has enough time to see COMP360 through its eventual approval. It is worth noting that the psychedelic drugs market is just starting to grow. By 2029, it is forecast to be worth $7.2 billion globally, with a compound annual growth rate of 55%. Also, the FDA published a draft guidance on research for these types of drugs for the first time in June 2023, easing the regulatory framework as well.

{kind=link}

Moreover, the House Rules Committee is advancing two amendments as part of bills related to research into psychedelic drugs for mental health. The first one assigns $15 million to the Defense Department for psychedelic medical clinical trials, and the second mandates to the Defense Health Agency to ensure that active-duty service members who are suffering from Traumatic Brain Injuries and Post-Traumatic Stress Disorder can participate in clinical trials studying the effectiveness of psychedelic substances.

Valuation Analysis

This leads us to ATAI’s investment profile. It trades at a market cap of approximately $182.61 million, with $208.99 million in cash and $18.97 million in debt. This implies a net cash position of $190.02 million and an enterprise value of negative $5.18 million. You read that correctly: ATAI currently trades below its cash value. Also, ATAI completed its last Series D funding round on March 3, 2021, raising $157M from thirteen backers. Lead investors included Apeiron Investment Group, Thiel Capital, and Woodline Partners. As previously noted, ATAI's primary income sources include equity offerings, debt, strategic collaborations, and licensing arrangements. These capital raises show backing from prominent investors and signal that ATAI is likely on the right track. Naturally, given the overall regulatory framework seemingly shifting in favor of psychedelics, I’d argue the stage is set for long-term success for ATAI.

In fact, just by looking at the market potential in the figure above of roughly $7.00 billion by 2029, along with COMP360’s promising results, one can quickly see that ATAI’s 20.8% on COMPASS appears to be undervalued. This is because I believe that most of the growth in this market will form precisely COMP360, as it seems to be a relatively safe and effective treatment for an extremely serious condition. It’s FDA Breakthrough Therapy Designation and current Phase 3 trials show it has a delineated path to eventual approval within a couple of years. This aligns with the market forecast of sector growth in 2025 and 2026, for which ATAI appears well positioned with CMPS.

ATAI appears to be excessively oversold and trades below its cash value, making it a potentially good entry point for new investors. (TradingView.)

However, “long-term” is the crucial attribute investors must be aware of when considering ATAI. The reality is that ATAI is still far from being ready to generate meaningful revenues, which is reflected in its price tag. Yet, for those investors looking to be positioned ahead of the potential wave of psychedelic treatments, ATAI is a nice ticket at a reasonable price. The mere fact that it trades below its cash value makes it simply too cheap for a company with multiple bets that could pay off massively in the coming years. As a result, this makes ATAI a relatively diversified investment vehicle and somewhat mitigates its risk profile as a biotechnology company. So, putting it all together, I think ATAI is a decent speculative “buy” for investors at these levels. It’s trading below its cash and book value and has multiple potentially game-changing products in its pipeline, so from a risk-reward perspective, it makes sense.

Investment Thesis Risks

However, it’s worth noting that ATAI is not without risks. This sector is still nascent, and the regulatory framework is evolving along with the research. This makes the investment proposition on ATAI highly speculative by nature. Moreover, note that ATAI is not the company that owns the I.P. Instead, it often owns stakes or has contractual arrangements that expose it to the upside of successfully developing the I.P. This has pros and cons. Still, for instance, assuming COMP360 is successfully produced, ATAI has a limited 20.8% stake. This means the upside from this, and many more of its other potential bets in the sector, won’t accrue entirely to ATAI. As a result, even if COMP360 is successful, it’s still possible that it may not be enough to move ATAI’s needle as a whole unless it’s a resounding success. And the same can be said for the rest of its I.P.

Furthermore, the I.P. risks related to psychedelic-based treatments could be a potential risk that might derail ATAI (and other companies in the sector). After all, much of the company’s value is derived from its ability to own the research they produce. Yet, psychedelics tend to be plant-based and have been used throughout cultures for centuries. So, considering them patentable is a gray area , which might expose ATAI to litigation risks. However, I deem this more of a tail risk.

Lastly, while ATAI's current price tag is below its cash position, it's also burning cash relatively quickly. The latest quarterly figures show a cash burn of approximately $18.45 million, which, if we annualize them, is $73.80 million. This results in a cash runway of 2.57 years using the latest cash balances. Thus, ATAI's valuation should be above its cash value at ceteris paribus by next year. On the other hand, a 2.57-year cash runway is encouraging because that should be enough time for COMP360 to start showing some tangible results.

Conclusion

Overall, ATAI is a promising company with a relatively diversified product pipeline. Currently, the most encouraging in its I.P. portfolio appears to be COMP360 through its stake in COMPASS. Moreover, investors can now buy into ATAI below its cash and book value, which is a compelling valuation argument. This is especially true in light of ATAI’s evident upside potential, which, despite being highly speculative, has a well-delineated path towards a potential FDA approval that should reward shareholders nicely with COMPASS. Hence, I think ATAI is a good “buy” at these levels, as long as investors are aware of the inherent risks and highly speculative nature that ATAI has.

For further details see:

Atai Life Sciences: A Promising Venture In The Psychedelic Therapy Market Trading Below Cash Value