ATER - Aterian's Silver Lining

- ATER is facing supply chain disruptions that have negatively affected its operations.

- The company holds a surplus of inventory and is looking to accelerate sales to restock at lower margins.

- Container ship prices are decreasing and the global supply chain appears to be stabilizing.

- Q3 and Q4 are typically ATER's strongest quarters due to seasonal demand for its products.

- ATER presents strong upside heading into 2023 as it recovers from supply chain disruptions.

Digital retail platforms that prospered during the pandemic have become increasingly impacted by shifts in consumer's discretionary spending as inflationary concerns move to the forefront. Despite missing Wall Street's GAAP EPS and revenue expectations, Aterian (ATER) offers a promising long-term outlook based on the improving landscape for supply chain logistics and the company's new strategy for building on preexisting products. I believe long-term investors have an opportunity to take advantage of the stock's lower value, resulting from inventory and demand issues, to benefit from what I expect will be a healthy recovery in 2023.

Overview

At the core of my investment thesis is the transition to e-commerce, which has been occurring at break-neck speeds. The COVID-19 pandemic only hastened its adoption and, during Q1 2020 alone, the growth of e-commerce in the U.S. achieved the same penetration as it had over the last 10 years . This led 75% of consumers to shift away from familiar brands and experiment with new ones - opening the door to new and emerging companies.

McKinsey & Company

Between 2021 and 2025, the e-commerce industry is expected to grow by almost $11 trillion - despite temporary shifts back to brick-and-mortar retailers following e-commerce's COVID-bump. The share of e-commerce across total U.S. retail sales was 14.3% as of Q2 2022, and I believe that this percentage will continue to increase with the shift toward e-commerce.

However, with wider adoption comes more competition. Amazon ( AMZN ) has encouraged the participation of third-party sellers on its site and as of Q2 they represent 57% of all units sold - a new high for the platform. Ease of access outside of the platform has resulted in a saturated commerce space, where new privacy laws limit the effectiveness of ad campaigns and the costs associated with customer acquisition continue to increase.

Given this increasingly competitive landscape, a technology-enabled consumer product platform like ATER has the potential to outperform competitors using data science to inform almost every aspect of its operations. Instead of focusing on the value of brand identity, ATER believes that a product portfolio developed from data and validated by social proof will create better performing products.

This is achieved using its cloud-based platform - AIMEE - which leverages data to identify unmet demand and streamline product management. Designed for the renaissance of e-commerce across Amazon, Shopify (SHOP), and Walmart (WMT), this technology has been instrumental to ATER's progress so far.

Achieving growth primarily through mergers and acquisitions, ATER has been able to expand rapidly and now includes 14 consumer brands as well as a portfolio of over 2,000 products. However, this growth has come at the expense of its short-term profitability. While ATER's business model benefited from COVID-era demand, it must prove adaptable to the post-pandemic landscape as well.

Cooling Consumer Demand

As a consumer products platform, Aterian is particularly sensitive to the effects of inflation on consumers' discretionary spending. Amazon - one of Aterian's sales channels - has reported a 4% dip YoY in its online sales , indicating that consumers are cutting back as their buying power is reduced.

This has put Aterian in a situation similar to major retailer Walmart, which had overestimated consumer demand leading to excess inventory in Q2. While Walmart was forced to lower its Q2 guidance as a result, Aterian has chosen to drop its full-year guidance and is projecting between $52 and $60 million in net revenue for Q3 - a drop of 23.6% to 11.8% compared to the same quarter last year.

Altogether, the performance of these retailers shows lagging demand across the board. But there are already signs of recovery. The University of Michigan's consumer sentiment index - a metric for reading consumer confidence levels - surpassed expectations, reporting 55.1 in its preliminary reading for August following July's improvement from a record low.

CEO Jamie Dimon of JPMorgan (JPM) also shared in the company's Q2 report that combined debit and credit card spending was up 15%. In the report, Dimon pointed out that spending on travel and dining remains robust as well - a sign that consumers are choosing to spend more on services.

Silver Lining

While lagging demand for goods appears to paint a gloomy picture for ATER, looking back at its Q1 earnings call management pointed to a number of factors which form a different outlook. At the time, ATER's CEO Yaniv Sarig noted fears of a global recession but also pointed out that as demand cooled, there would be an improvement in supply chain and logistics costs. ATER's management took this as a positive, saying:

[...] for our business really getting back to growth and profitability is predicated on returning to normalized shipping costs. And unfortunately, the only way to get there is to reduce global consumer demand for products.

We are now seeing this situation play out as ATER noted in its Q2 earnings call a 31% YOY drop in the cost of shipping from Shanghai to L.A. While prices still have not stabilized at their pre-pandemic levels, relief is in sight. Higher demand for shipping containers during the pandemic led manufacturers to increase production, but average container prices and leasing rates have been declining globally since September-October 2021 .

As the containers become ready for use, oversupply will continue pushing costs down. This has already contributed to a 20% decline in freight rates since the beginning of the year. While macroeconomic factors such as inflation could affect the situation, it appears as if the costs of shipping containers are on track to continue declining this year. That puts ATER in a good position for 2023.

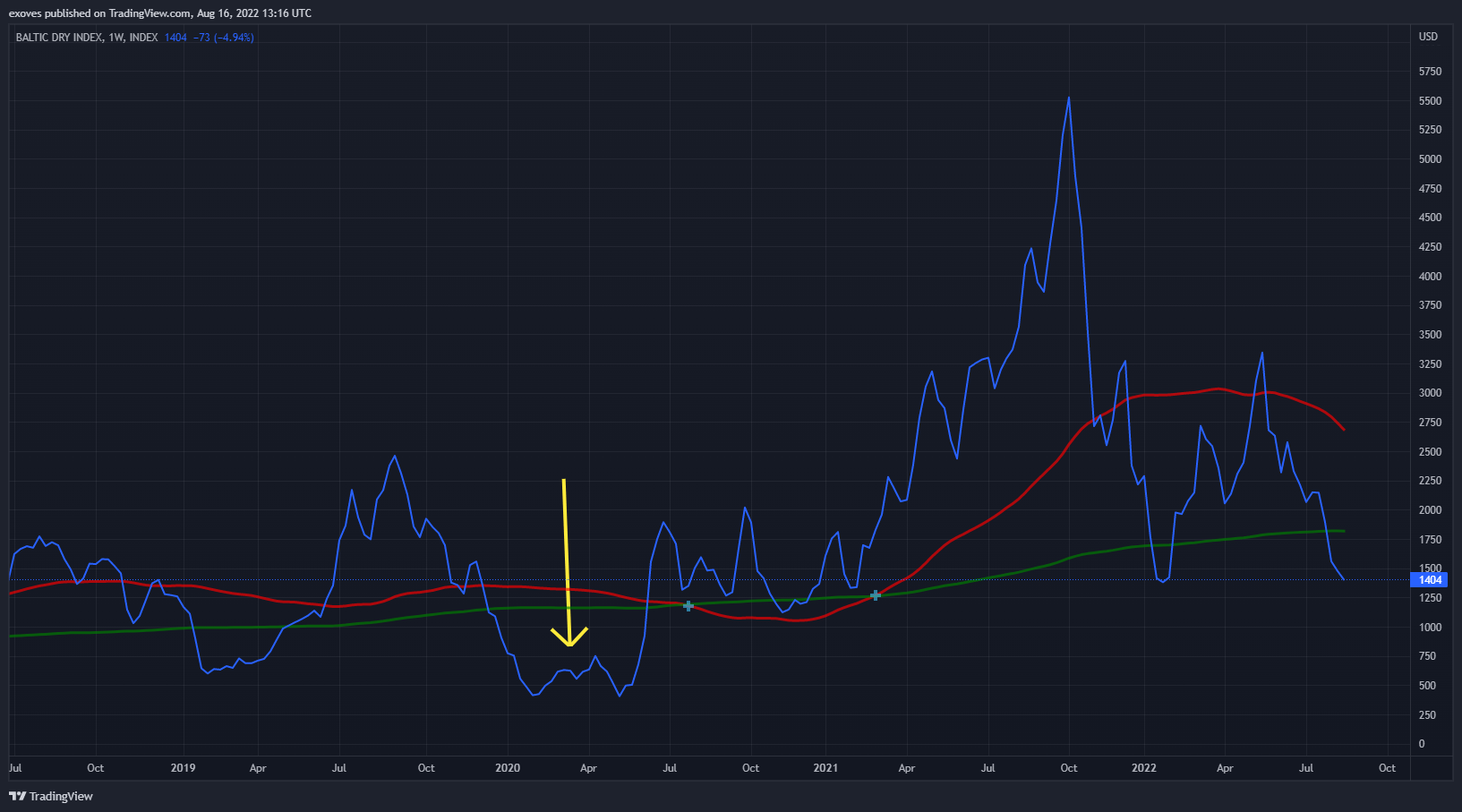

Because ATER's current financial distress is largely due to substantial increases in supply chain costs for shipping containers, continued improvements will put the company back on track for growth. These improvements could come sooner than expected since the Baltic Dry Index - an index of average prices paid for the transport of dry bulk materials - has dropped 58% since May 23.

{kind=link}

While this index is specific to bulk commodities used for manufacturing, it also reflects the transportation costs of containers within the international trade framework. The index has been stabilizing after reaching its peak in October 2021. Now, looking at the weekly time frame and accounting for seasonal shifts in demand, it appears that the index is nearing pre-pandemic levels.

However, there will be a delay before these changes are reflected in ATER's balance sheet. In order for ATER's margins to recover in 2023, it must sell its current inventory before restocking at a lower cost basis. Otherwise, the company's margins will not recover in 2023.

Inventory

As is, ATER is encumbered with $76.1 million in inventory on hand, which has negatively impacted its working capital. While this is a short-term concern, I believe ATER is already taking the steps necessary to resolve its inventory issues by accelerating the sale of goods that were previously shipped to its warehouse. Amazon's Prime Day offered the perfect opportunity for this and it appears that ATER has already reduced its inventory by selling some of its products at a less attractive margin. Despite this, July's Amazon event was ATER's best Prime Day yet, which is indicative of its products' strong performance.

I believe the company will not have a difficult time offloading its inventory during the remainder of 2022 since Amazon is planning a second Prime Day in the fall in addition to Cyber Monday, Black Friday, and the holiday shopping season. Meanwhile, the company is taking the opportunity to revise its product portfolio, which I believe will put it in a better position for pursuing growth in 2023.

Product Portfolio

ATER is in a stronger position than others thanks to its diversified portfolio of evergreen products. Currently, ATER has offerings in a variety of categories including home and kitchen appliances, heating, cooling, and air quality appliances, beauty products, essential oils, and kitchenware. While these items may not be essential goods, consumer spending is still strong enough that demand for these products will not vanish.

In fact, some of ATER's top products are gaining market share despite cooling demand. This could be part of the reason why ATER is planning to focus on certain categories by acquiring brands that will complement the inroads already made. I believe this is the right decision not only from a financial perspective, but also based on ATER's stronger performance in certain categories.

Tailoring its approach to capitalize on verticals where it has a strong position is a smart business decision, given that ATER is routinely confronted with higher upfront investments when entering a completely new category. It appears as if ATER is looking to reduce risk by anchoring its new products to its successful ones.

This is not to say that ATER has produced duds. Using AIMEE, the company is clearly targeting some of the top-selling categories on Amazon - one of which is the home and kitchen category. ATER's acquisition of Mueller positioned it to capitalize on this category, and based on the results of my Amazon search I see that at least 16 Mueller products are "Amazon Best Sellers" and many others are rated as "Amazon's Choice."

These are valuable metrics to consider because an Amazon's Choice badge can increase traffic and conversions for a product. According to a study of 37,000 Amazon products, this badge can increase its click through rate by an average 17% and boost conversions by an average 25%. Some claim that an Amazon's Choice badge can increase sales by as much as 200% . Similarly, a Best Sellers badge can increase traffic for a product by an impressive 45% and conversions by 3%.

However, others have pointed out that these badges can be manipulated by placing products in low-volume categories or through other gray area tactics . While Culper Research criticized the company for supposedly using such tactics to boost their reviews and gain badges, there is no proof that that is the case. But it is worth noting that these badges might not translate to tremendous success for the products.

For example, despite the performance of Mueller and ATER's other brands on Amazon, ATER's summary of 2021 revenue shows that its heating, cooling, and air quality products led the way with $73 million in revenue. Although these products see strong seasonal demand, considering the growing frequency of wildfires and hotter temperatures, this category could continue to report significant growth YoY.

While the company reported $58.3 million in revenue for Q2, I expect it to report higher sales in Q3 and Q4 due to the upcoming shopping seasons. Typically, there is an uptick in ATER's reported revenue during Q2 and Q3. In 2021, that jump was from $48.1 million in Q1 to $68.1 million in Q2 - a 41.5% increase. In 2020 the increase from Q1 to Q2 was 133%. While some of this higher demand was due to the pandemic, ATER benefits from the summer season thanks to its cooling and air quality appliances. This sales growth typically carries through to Q4 when the holiday season drives demand for small kitchen appliances. With this in mind, it appears that ATER is on track to report revenue growth in the coming quarters.

New Product Strategy

So far ATER has not released the finer details of its new strategy, but it appears to be centered around offering new sizes, pairings, and variations on existing products using AIMEE to identify the best opportunities. For Mueller I imagine this strategy could involve pairing different kitchen gadgets together, or creating a package for kitchen tools, etc. For hOmelabs, this could result in different sizes or variations of beverage coolers and freezers.

Annual Report

Going forward, I believe ATER will focus on strengthening its hold in the best performing categories such as heating, cooling, and air quality products as well as kitchen appliances. ATER is already preparing to launch a cool branded air purifier in partnership with a publisher brand and is considering additional product launches depending on supply chain easement. I believe this decision shows management's confidence in its new strategy as it accelerates sales of its old inventory.

Valuation

Currently, ATER has a market cap of $184.8 million, but according to its latest quarterly report its total assets amount to $313 million. Of this, $124 million are current assets such as its inventory, cash, and accounts receivable. The company's goodwill is valued at $119.9 million and its other intangibles amount to $64.9 million.

Over the last four quarters ATER has had sales of about $231.4 million, and its market cap is currently $184.8 million - giving it a P/S ratio of .79. However, other companies in the household appliances sector - such as Weber ( WEBR ) - have P/S ratios much higher than ATER's. With a market cap of $2.54 billion, WEBR has a P/S ratio of 1.33. WEBR's competitor Traeger ( COOK ) has a much lower P/S ratio of .49, given its $373 million market cap.

Despite being in the same sector, I believe these companies do not offer a very fair comparison for ATER given that they specialize in outdoor cooking equipment - a category that ATER does not compete in. However, they do provide some context for ATER's performance.

Another company in this sector, Cricut ( CRCT ), specializes in making cutting machines and crafting tools for hobbyists and small businesses. The company also sells its products through an Amazon store, but has a P/S ratio of 1.3 given its $1.4 billion market cap.

Two companies that ATER might compete with in terms of products are Helen of Troy Limited ( HELE ) and Hamilton Beach Brands Holding ( HBB ). The former is a global consumer products company operating in the health and wellness, home and outdoor, and beauty segments. HELE owns some well-known brands such as Hydro Flask, Vicks, OXO, and others, with products sold on Amazon. Despite its $3.2 billion market cap, HELE has had $2.19 billion in sales over the last four quarters, giving it a P/S ratio of 1.47. Meanwhile HBB, which produces a wide range of branded small electric household and specialty housewares appliances, boasts a P/S ratio of .26 given its $171.5 million market cap and $648 million in sales.

These companies are profitable whereas ATER is not. Therefore, ATER's relatively low P/S ratio could indicate that it has a low valuation in comparison to many of these profitable companies. In light of this, I believe ATER has the potential for greater growth once these supply chain issues stabilize.

However, it's also worth noting that - as far as my research has shown - there are no public companies pursuing the FBA (fulfillment by Amazon) sellers market on U.S. exchanges. This is a niche that has grown notably in just a few years, and there are many private Amazon aggregator companies that have raised more than $500 million in capital. A few, like Thrasio, have raised over a billion dollars.

Packable, the parent company of Pharmapack - a no. 1 seller on Amazon - planned to go public through a SPAC merger with Highland Transcend Partners I Corp., but has since terminated that agreement . Anker - a Chinese electronics company that began as a third-party seller on Amazon in 2011 - did become a publicly listed company on the Shenzhen Stock Exchange.

Based on the tremendous growth in this area I am surprised to see ATER valued at a market cap of only $184 million. Clearly, a broad range of investors see notable growth in this sector and are investing heavily in private companies that buy out Amazon FBA sellers. Aterian is already competing in this arena, using AIMEE to inform its process. Despite its current financial struggles, I believe that the amount of capital raised by these private companies gives some insight as to ATER's potential. As ATER's CFO at the time of its IPO shared, "did go public definitely too early," which I believe has contributed to its poor valuation comparatively.

Risks

ATER's long-term attraction as a growth company with the potential to become a tech disruptor in the e-commerce space is largely predicated on the value of its proprietary technology - AIMEE. This platform connects to multiple e-commerce platforms to identify specific product and market opportunities, automate portions of the fulfillment processes, and conduct sales forecasting. AIMEE has allowed ATER to maintain a small team without facing obstacles related to scaling.

Overall, Aterian has spent the majority of $18 million developing AIMEE making it a considerable asset. However, the question for new investors is whether AIMEE will give ATER an edge over competitors. Since this space has become increasingly crowded, similar e-commerce platforms have been developed to meet businesses' e-commerce goals across the board.

Despite the success of ATER's products on Amazon, it remains to be seen whether AIMEE will be able to distinguish ATER from the pack over the long run. This is an especially relevant risk factor for ATER since it offers AIMEE as a managed PAAS (platform as a service). As it scales, ATER believes it could evolve this segment into a substantial part of its business, but for now believes the consumer business opportunity is larger. Surprisingly, its managed PAAS segment saw a YoY decrease of 68% which might indicate the platform's limitations as a standalone service.

Although the company continues to invest in its platform's development, if AIMEE fails to live up to its promise, then ATER will lose much of its allure as a potential e-commerce disruptor. Furthermore, mergers and acquisitions are an important part of ATER's growth strategy, but the company will need to raise funds to finance these deals. This puts shareholders at risk of more dilution even after ATER's total shares outstanding grew by 85% over the past year.

Overall, ATER is in a difficult financial position due to its MidCap credit facility. If the company is not able to secure additional outside capital, then it could be forced to change aspects of its operating plan or the scope of its business. The company might also seek to secure a waiver or forbearance from the lender so as not to breach its financial covenants.

Conclusion

While these concerns make ATER a risky investment, I believe the company offers significant upside after being beaten down by over a year of supply chain disruptions. It's noteworthy that institutional investors have been stepping up their investments in ATER since the start of the year, indicating that they see these supply chain issues as improving and ATER recovering along with them.

ATER has achieved YOY revenue growth since 2017 using its proprietary technology, and I believe the company can and will resume this growth after weathering the current storm. Supply chain issues appear to be resolving themselves and, as they do, ATER will have the opportunity to restock and sell its new inventory at better margins.

Typically, ATER has reported higher revenues in Q3 and Q4 thanks to seasonal demand. I believe this will help the company reduce its surplus inventory. Meanwhile, ATER will continue making inroads in high-value categories while reducing the costs it typically faces when launching a new product.

Given the improving outlook for global supply chains, I believe long-term investors have an opportunity to accumulate shares or average down below ATER's resistance at $2.73. However, the stock shows a strong support at $2.23, and if ATER breaks through that support without bouncing back from its all-time low of $2.10, this would be a warning sign for investors.

For further details see:

Aterian's Silver Lining