ATH:CC - Athabasca Oil: Trading At A 20% Free Cash Flow Yield

2023-08-15 10:30:00 ET

Summary

- Athabasca Oil sees improved financial results in Q2 due to reduced WCS differential.

- Operating income jumps from loss in Q1 to profit in Q2.

- Athabasca plans to reward shareholders with sustaining free cash flow and continuous share buyback program.

Introduction

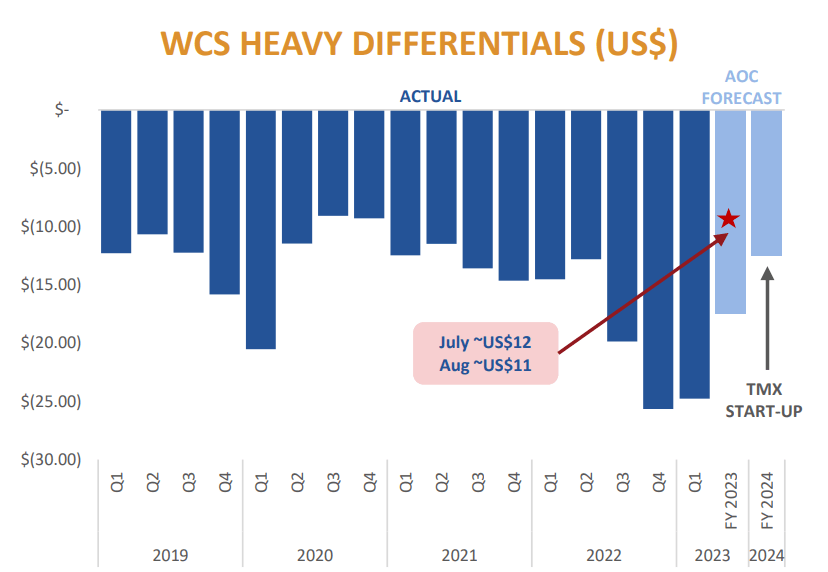

In an article published in December last year, I argued Athabasca Oil ( ATH:CA ) ( OTCPK:ATHOF ) wasn’t the best oil related idea as the heavy oil price was trading about 30% below the level Athabasca used in its full-year cash flow and budget guidance. An investment in Athabasca only made sense if you were betting on a lower WCS differential. And fortunately for the company, that has now materialized. While the differential was very high in the first quarter (at C $33.50 per barrel ), this decreased sharply to just C$20 per barrel during the second quarter.

A decent second quarter, thanks to a reduced WCS differential

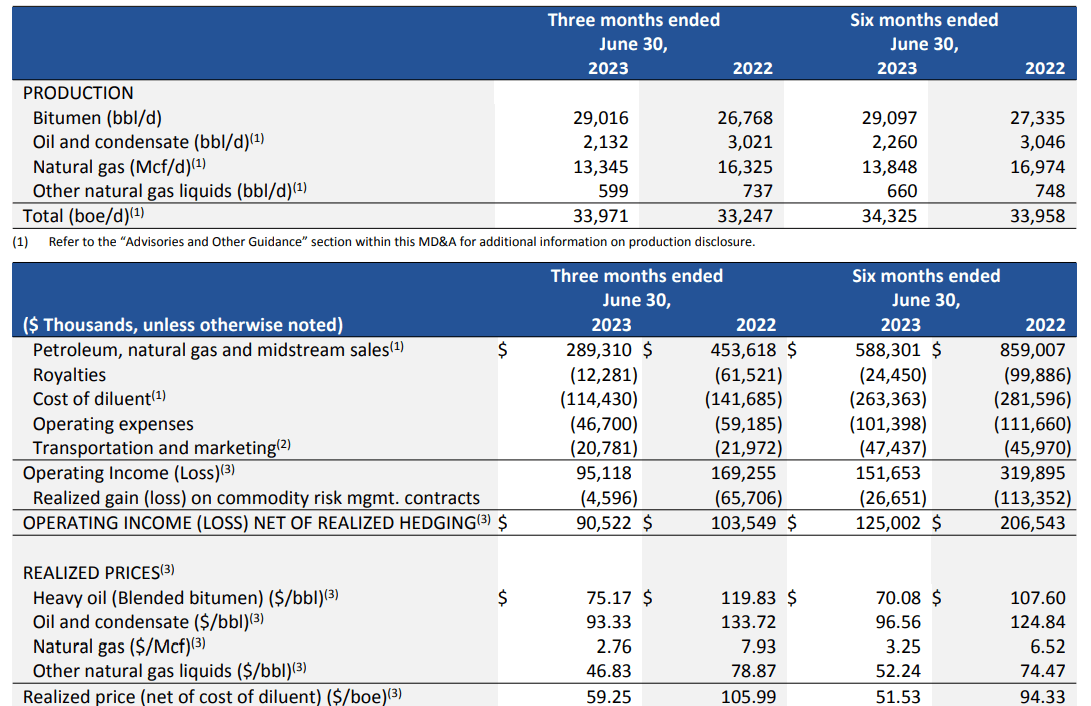

The impact of the lower WCS differential is very clear. Whereas the WTI oil price decreased from US$76 per barrel in Q1 to less than $74/barrel in Q2, Athabasca’s realized oil price actually increased thanks to the double digit decrease of the WCS differential.

{kind=link}

Whereas Athabasca’s heavy oil was sold at a realized price of just C$65.70 i n the first quarter of the year, the realized price increased to C$75/barrel in the second quarter of the year. And with an average production rate of almost 34,000 barrels of oil-equivalent per day, of which 29,000 barrels per day were bitumen, a C$10 price increase obviously completely changes the situation.

{kind=link}

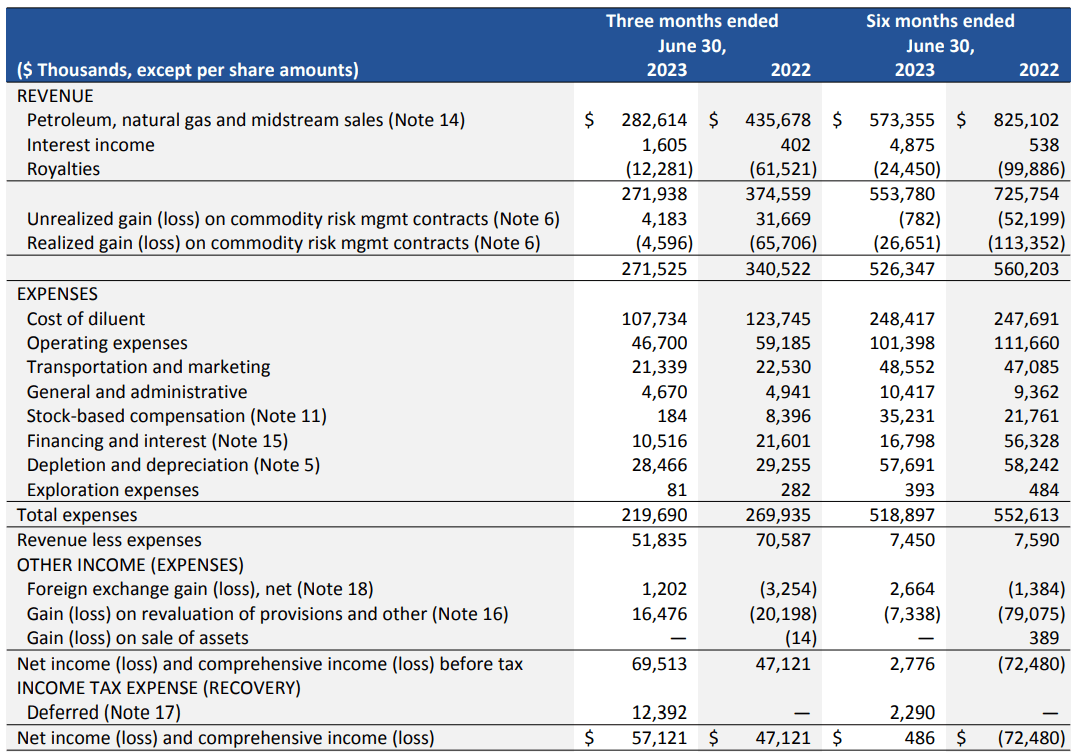

And the improved realized price is very clearly visible in the quarterly statements as Athabasca was able to keep its revenue relatively stable despite seeing a lower realized oil, natural gas and NGL price.

The total revenue in the second quarter was approximately C$283M and after taking the royalty payments and net hedging losses into account, the net revenue was C$271.5M. Interestingly, the operating expenses also decreased quite substantially. As you can see below, the cost of diluent fell from in excess of C$140M in Q1 to less than C$108M in the second quarter. We see a slightly lower decrease in the pure operating expenses (down from almost C$55M to C$46.7M) and the combination of all these elements meant that the total expenses fell from almost C$300M to less than C$220M.

{kind=link}

That obviously had a positive impact on the operating income which jumped from a loss in Q1 to an operating profit of almost C$52M in the second quarter of the year. On top of that, the company recorded a gain on the revaluation of provisions (this is related to the fluctuating value of the warrant that was issued in combination with the 2026 note issuance) ) and this brought the pre-tax income to C$69.5 and the net income was a very healthy C$57M or C$0.10 per share.

That is an excellent result, and the cash flows were very strong as well. While the gain on the provision revaluation was a non-cash gain, the deficit on the balance sheet also means the company is dipping into its existing tax pools and its entire C$12.4M tax bill is deferred. Athabasca estimates it won’t have to pay a single dollar in taxes this decade.

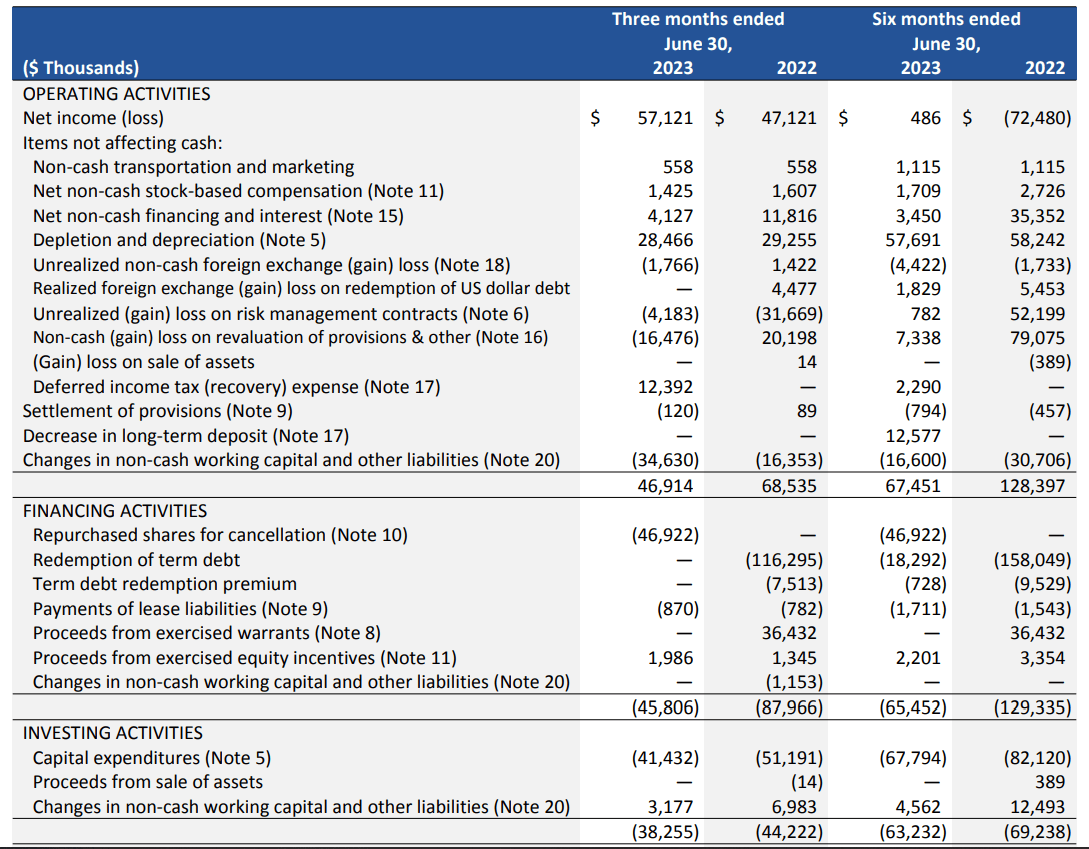

The operating cash flow was C$47M but this includes a C$34.6M investment in the working capital position while I should also deduct the C$0.9M in lease payments. This means the adjusted operating cash flow was C$80.6M. The total capex was just C$41.4M, which resulted in a net free cash flow result of C$39M.

{kind=link}

Based on the share count of 585.7M shares outstanding, the net free cash flow result per share was approximately C$0.067. That’s lower than the reported net income but keep in mind the capex was relatively high for the quarter (about 50% higher than the depreciation and amortization expenses) and considering the full-year guidance calls for a C$145M capex program, the average quarterly capex is more than 10% lower than what the company spent in the second quarter.

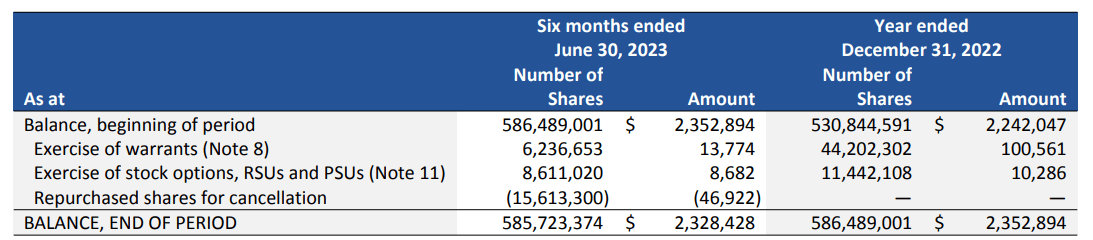

The entire free cash flow was spent on buying back its own shares. Unfortunately this doesn’t mean the share count is decreasing fast: the company had to deal with the exercise of options and warrants, and it only bought back slightly more than it has issued.

{kind=link}

As of the end of June, there were 99,999 warrants outstanding with each warrant exercisable in 227 common shares at C$0.94 per share. This means the total dilution from those warrants could be an additional 22.7M shares and although this will bring in in excess of C$20M in cash, it will take a while before Athabasca Oil sees a net impact from its share repurchase program.

Selling light oil assets will help the balance sheet

Subsequent to the end of the quarter, Athabasca disclosed it was selling light oil assets with a current production rate of 3,000 boe/day for C$160M. That’s an excellent multiple as it represents almost 8 times the net operating income while the price tag also represents almost C$55,000 per flowing barrel.

This means the balance sheet will now have a positive net cash position and this bodes well for its shareholders as Athabasca has pledged to use 75% of its sustaining free cash flow to reward its shareholders. According to the corporate presentation, the sustaining capex is just C$125M while the company expects to generate about C$400M in operating cash flow at US$70 WTI and a differential of US$15 per barrel.

Athabasca Oil Investor Relations

This still includes the light oil assets, so let’s deduct C$20M from the expected AFF and deduct about C$10M in sustaining capex from the light oil assets. This would reduce the AFF to C$380M while the net sustaining free cash flow should be C$285M or C$0.49/share (using the current share count). Using a WTI price of US$80, the AFF would increase to approximately C$550M (around C$530M excluding the light oil sale) for a free cash flow result of C$415M or C$0.70/share. This implies that in a scenario using $70 and $80 WTI, Athabasca is planning to spend C$0.37-0.52 per share on shareholder rewards with a continuous share buyback program likely absorbing the bulk of that allocation.

Investment thesis

I didn’t dare to invest in Athabasca to speculate on the WCS differential and that’s fine (as I had exposure through other heavy oil stocks like Hemisphere Energy ( HME:CA ) ( OTCQX:HMENF ) which I covered here ). But based on the current oil price, current WCS differential and share price, the stock still isn’t expensive at about 5 times its sustaining free cash flow result based on US$80 WTI.

The company still is a call option on the WCS differential: as long as the differential remains relatively stable, the stock is still cheap. And keep in mind that as soon as the 9.75% 2026 notes are retired, the company will save in excess of C$20M per year in interest expenses.

For further details see:

Athabasca Oil: Trading At A 20% Free Cash Flow Yield