ATI - ATI: Improving Margin Profile Provides Support For The Premium Valuation

2023-09-26 09:52:52 ET

Summary

- ATI Inc. stock has delivered strong returns despite weakness in its largest division, Advanced Alloys & Solutions.

- Investors appear to be drawn by developments within ATI's other division, High Performance Materials & Components, on account of its sizeable exposure to the aerospace & defense sector (83% exposure).

- ATI's medium-term EBITDA margin outlook of 280bps worth of improvements is commendable, but it should still come in below management's FY25 target range.

- ATI is unlikely to benefit from rotation interest within the material space, but it could receive some support from a likely step up in buybacks during H2-23.

Stock On Fire Despite Weakness In The Largest Division

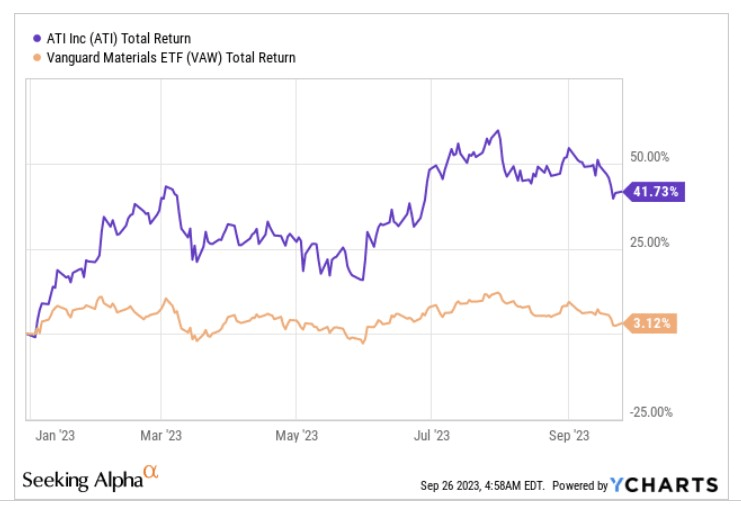

The stock of ATI Inc. (ATI) a mid-cap specialty materials company has been on fire this year, delivering 42% returns, and comfortably outperforming its peers from the broad materials sector.

{kind=link}

A few passive observers of ATI maybe perplexed by the stock's outperformance this year, given that its largest division by revenue - Advanced Alloys & Solutions or AAS ( 57% of FY22 revenue) has been suffering on account of weakness in the automobile, industrial, and energy end-markets. For context, in Q2, the topline dropped by 8% both sequentially and annually, whilst the segment EBITDA fell by greater margins of -13% sequentially, and -40% annually. On the Q2 call management even confirmed that recessionary conditions in the industrial markets would continue to put pressure in Q3, before stabilizing in Q4.

The AAS division mainly focuses on selling high-value flat products such as nickel-based alloys and because of the pass-through clauses in its contracts, the segment EBITDA does well when nickel prices are resilient. That hasn't been the case in recent months, and with Nickel prices weak through Q3, one could perhaps expect another $2-$3m headwind at the EBITDA level, just like we saw in Q2.

In addition to that, the company is also likely to undergo preventative maintenance outages in Q3 across various facilities which could hamper the smooth operations.

A&D Exposure Is Attracting The Bulls

Despite all these challenges, the ATI stock has demonstrated ample resilience this year, and much of that is down to what's happening in its second division - High Performance Materials & Components (HPMC) which is fast taking a larger share of the overall mix over time (it has been gaining 2% of the group sales mix every year since FY20 and this will only increase over time, given the strategic importance assigned by the management team).

Within HPMC, the excitement here is primarily centered around the segment's heightened exposure to the aerospace & defense (A&D) sector, which accounted for 83% of HPMC sales in Q2. Do consider that even AAS has some exposure to the A&D market, and in effect, the entire ATI group derives around 58% of its sales from this market alone (the long-term goal is to get it to 65%). ATI's strong linkage to this market should be appreciated, given the drastic fleet renewal shifts that will take place through this decade.

Whilst supply chain pressures have still not entirely abated, narrowbody aircraft production levels are expected to step up after H1-24 and to prepare for that, one is already witnessing a strong surge in ATI's backlog. On a YTD basis, the order backlog is up by 20%, and on a qoq basis, it is up by 9%. When demand is strong for certain materials (like titanium specialty materials used in airframe applications or jet engines), you're also better prepared to be more stringent with pricing and thus you're also able to engender stronger drop through at the EBITDA level. For context, in Q2, HPMC's EBITDA margins were up by 350bps, and taking it to closer to its long-term target of 20-25%.

Medium-term EBITDA Outlook Is Admirable, But Not As Dazzling As Management Believes

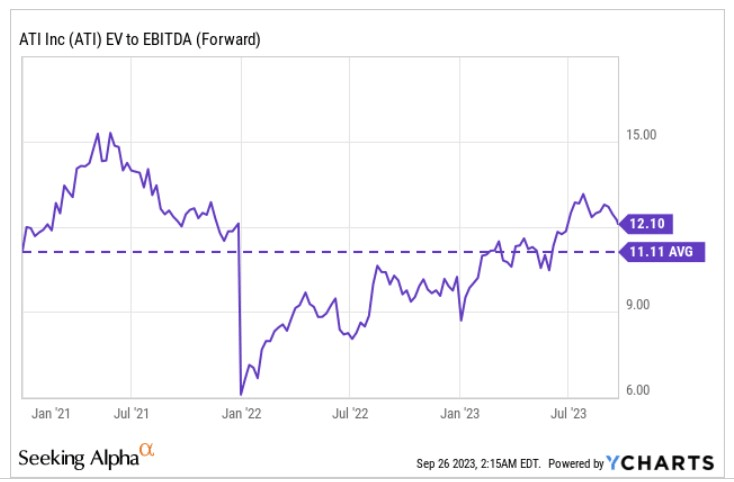

Needless to say, a growing proportion of HPMC in the overall sales mix will also catapult ATI's overall margin profile over time, and ongoing margin improvements will be key, if one is to make allowances for the stock's premium valuation. Note that currently, ATI's stock is priced at 12.1x forward EV/EBITDA a 9% premium over the stock's long-term average.

{kind=link}

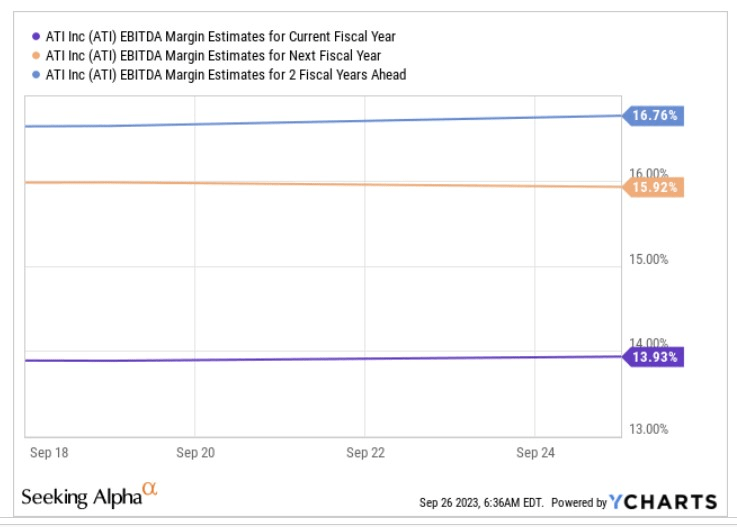

The growing A&D and HPMC penetration should no doubt facilitate ample EBITDA margin improvements over time, but it remains to be seen, if it will be as dazzling as management expects it to be. For instance, if one takes a look at how consensus estimates are positioned through FY23-FY25, you'd see that ATI could bring through aggregate EBITDA margin improvements of over 280bps through the next two years, taking it to a margin of 16.7% by FY25.

{kind=link}

However, that would still be well over 100bps lower than what ATI management expects to hit by FY25 (management's target is to hit group EBITDA margins of 18-20% by that year)

Closing Thoughts - Technical Commentary

{kind=link}

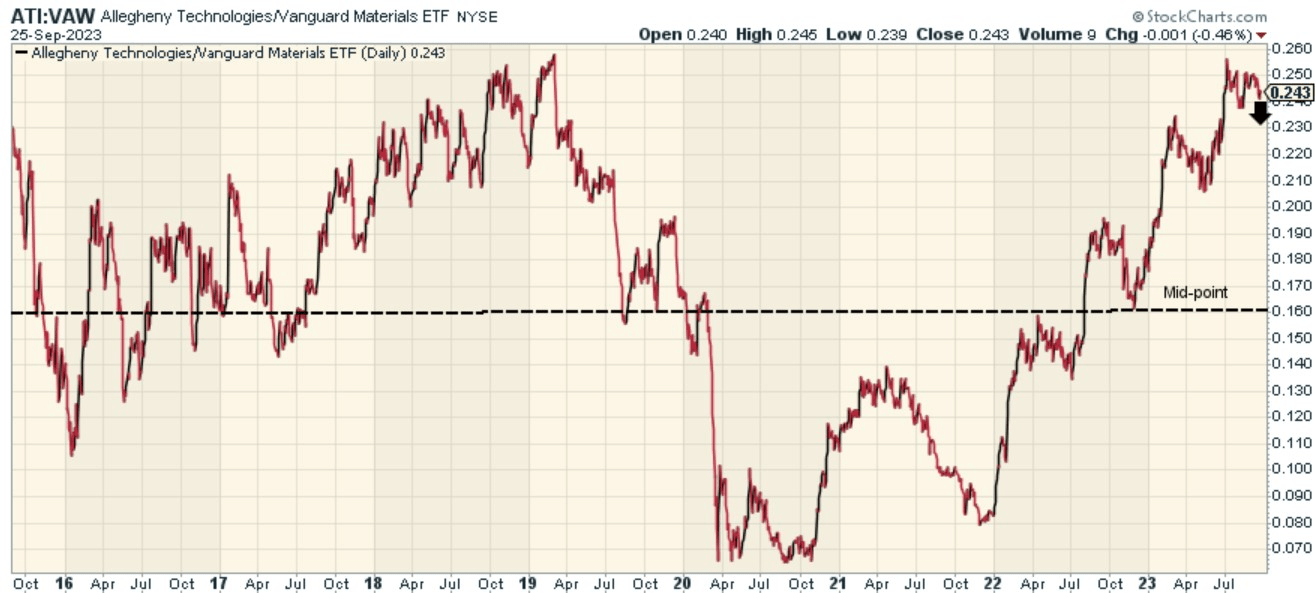

The chart above gives you a sense of how ATI is placed relative to its peers from the materials' space. We think ATI could have worked as a very attractive mean-reversion play back in early 2022, but currently, the relative strength ratio of ATI versus its peers is trading at the other end (incidentally it had hit similar levels in early 2019 after which we saw a pivot) of the long-term range.

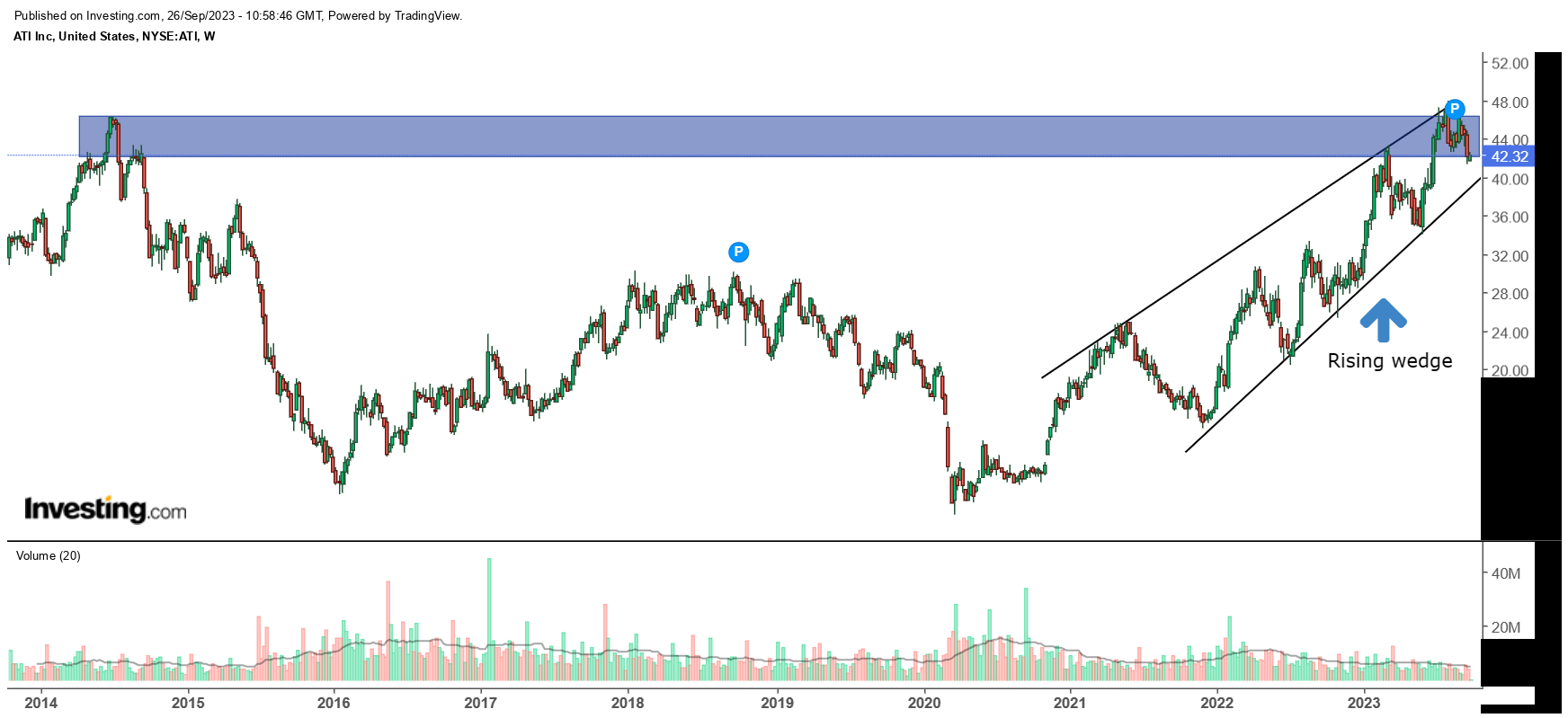

Then, on ATI's weekly chart, we can see that until July, the stock has been trending up in the shape of a rising wedge pattern, and the price action appears to have climaxed at around the $43-$47 levels, a level it had struggled to clear back in 2014. We are currently in the midst of seeing a two-legged pullback, and one would hope to see some bottom formation and a recouping of the uptrend once the stock hits the lower boundary of the wedge, which is around the $40 levels.

{kind=link}

The stock may also likely receive additional support from a step-up in buyback activities (the company did not engage in any stock buybacks in Q2) as it looks to complete $75m worth of buybacks through H2-23. We are more confident about buybacks ramping up as ATI may likely generate excess FCF in H2 as working capital as a percentage of sales which stood at 39% is poised to come down to 30% by the year end.

For further details see:

ATI: Improving Margin Profile Provides Support For The Premium Valuation