ATI - ATI: Investments In Aerospace And Defense Make It Undervalued

2023-04-25 08:18:09 ET

Summary

- ATI is an American company registered in Dallas and oriented to the development, manufacture, and commercialization of specialty materials with high degrees of scientific knowledge.

- The recent sale of subsidiaries related to the standard stainless sheet products and more exposure to higher-margin products and aerospace & defense end markets will likely bring more FCF margins.

- I am quite optimistic about the fact that ATI expects to increase its titanium production by up to 35% from existing assets. The titanium market is experiencing a period of expansion.

ATI Inc. ( ATI ) continues to exit production of lower-margin standard stainless sheet products, and invests significantly in high margin activities or the aerospace and defense end markets. As a result, ATI is expecting to deliver significant FCF generation in the coming years. Like other analysts, I believe that future free cash flow will multiply in the coming years driven by smart divestitures and reorganization. Even taking into account potential volatility in the energy market or supply chain issues generated by the invasion of Ukraine, I believe that the stock is undervalued.

ATI Reports Long-Term Contracts With Large Clients, Offers International Exposure, And Works For Many Industries

ATI is an American company registered in Dallas and oriented to the development, manufacture, and commercialization of specialty materials with high degrees of scientific knowledge.

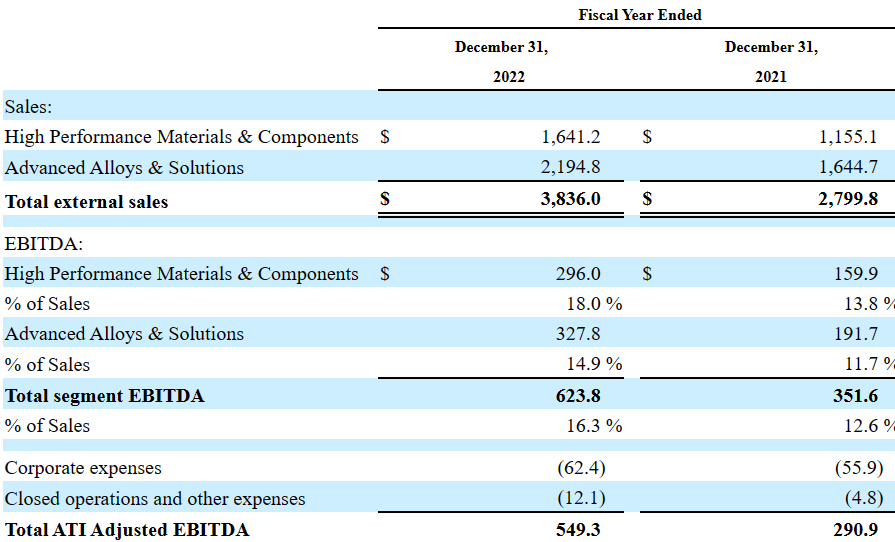

ATI divides its operations into two segments: the High Performance and Specialty Materials segment and the Advanced Alloy Solutions segment. The objective of the first of these segments is to maximize the growth of products for aerospace engineering systems and their components.

The advanced alloy solutions segment, on the other hand, focuses on the distribution of high-quality products and materials for similar markets, to which must be added participation in the production systems of some automotive manufacturers and companies dedicated to the power generation, mainly gas and oil .

{kind=link}

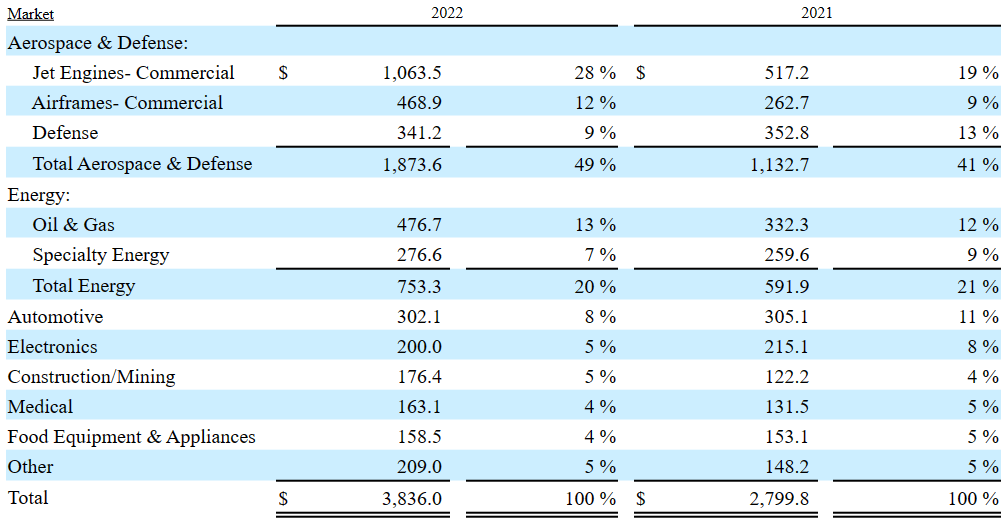

The main markets ATI serves are the military and defense industry as well as the power generation market, which represented close to 70% of the company's revenue in 2022. With that, I believe that the revenue is diversified because ATI works with clients in the automotives, medical, mining, and construction industries among others.

{kind=link}

It is also worth noting that ATI reports prestigious international recognition as 48% of its revenues in 2022 came from operations outside the United States. Besides, clients include large players like Boeing ( BA ), General Electric ( GE ), Rolls-Royce ( OTCPK:RYCEY ), Pratt & Whitney, Snecma, and Embraer (ERJ). With some of these customers, ATI maintains long-term contracts, and in the case of original equipment manufacturers, the company has managed to position itself as a substantial part of the development of its customers' operations. With long-term contracts, I believe that we can assume that ATI products will continue to receive demand in the near future.

Large Competitors In A Market With Significant Barriers To Entry

Regarding its competitors, ATI participates in a market with high competition and significant costs, which prevent small companies or independent manufacturers from entering easily. For the specialty materials segment, some of the main competitors are Berkshire Hathaway Inc. ( BRK.B ), Precision Castparts Corporation Howmet Aerospace Inc, Carpenter Technology Corporation ( CRS ), and Aubert & Duval. For the advanced alloy solutions segment, the significant competitors are Haynes International ( HAYN ), VDM Metals GmbH, subsidiary Acerinox S.A ( OTCPK:ANIOY ), North American Stainless, Outokumpu Stainless USA, LLC ( OTCPK:OUTFF ), and Cleveland-Cliffs Inc. ( CLF ).

Beneficial FCF Growth And EPS Growth Expectations

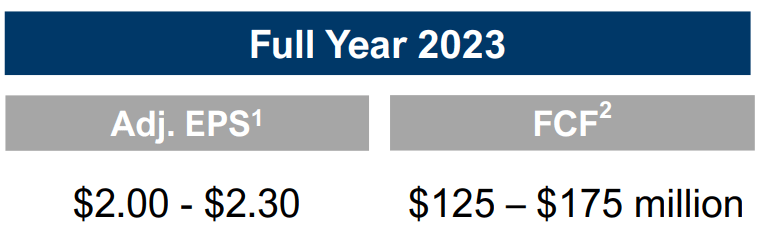

I believe that the guidance given in Q4 2022 is a good reason to pay special attention to the stock. ATI expects to deliver FCF close to $125-$175 million and an adjusted earnings per share of $2-$2.3. In the past, ATI reported negative FCF and lower EPS. Thus, I believe that the recent divestitures and investments are expected to bring significant FCF generation.

{kind=link}

I believe that analysts out there are optimistic about management. 2023 and 2024 net sales growth would stand at close to 9%-5% with double digit operation margin and growing EPS close to $2.81 in 2024.

Source: S&P

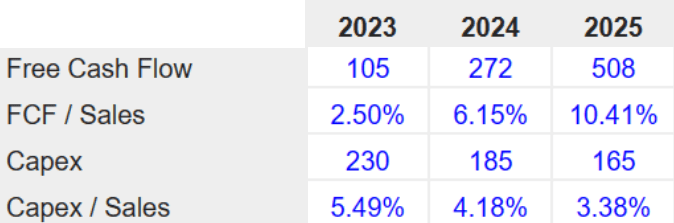

FCF expectations are also on the rise with 2025 FCF close to $508 million and 2024 FCF of $272 million. Finally, investors are expecting declining capital expenditures in 2024 and 2025.

{kind=link}

Other investment analysts are also expecting an improvement in the FCF. The new financial figures would imply financial ratios. Analysts are expecting 2023 EV / EBITDA close to 10.3x, EV /FCF of around 11x in 2025, and price to book of around 3.55x.

Source: S&P

Balance Sheet: More Assets And Less Liabilities As Compared To 2021

The balance sheet reported in the 2022 annual report did not change that much compared to that in 2021. With that, the numbers appear a bit better than that in 2021.

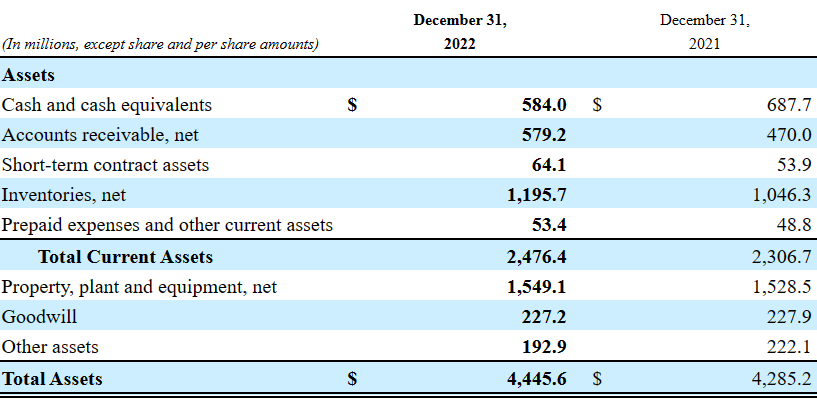

ATI reported more assets than in 2021, more property and equipment, and more inventories. In addition, the asset/liability ratio improved. In sum, I believe that the recent divestitures and investments announced did not seem to radically change the good financial health of ATI.

ATI reported cash and cash equivalents of $584 million with accounts receivable close to $579.2 million, short-term contract assets of $64.1 million, and inventories of $1.195 billion. Also, with prepaid expenses and other current assets close to $53.4 million and property, plant and equipment of $1549.1 million, total assets stood at $4445.6 million.

{kind=link}

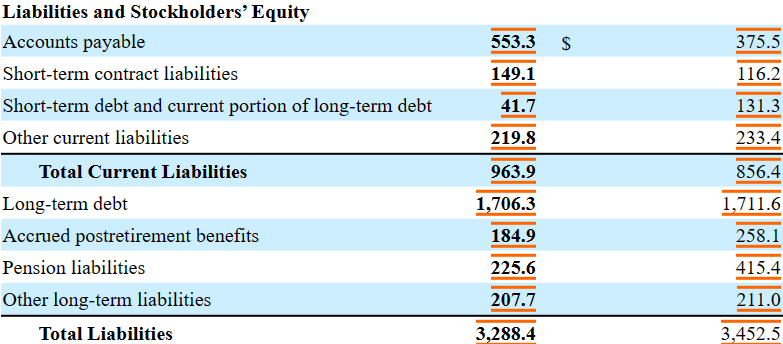

With regards to the list of liabilities, the company reported less long term debt than that in 2021 and less short term debt. It appears beneficial. Accounts payable stood at $553.3 million with short-term contract liabilities of $149.1 million, short-term debt and current portion of long-term debt of $41.7 million, and long-term debt of $1.706 billion. Pension liabilities stood at $225.6 million with total liabilities of $3.288 billion.

{kind=link}

ATI has a significant amount of know-how accumulated in the industry. In addition, the EBITDA and FCF appear stable. I understand that certain investors are a bit afraid of the total amount of debt. With that, I am not worried because I am expecting a lot of FCF in 2023, 2024, and 2025.

Assumptions Included In My Financial Model Are Larger Exposition To Higher Margin Activities, More Products For The High Performance And Specialty Materials Segment, And More Hiring

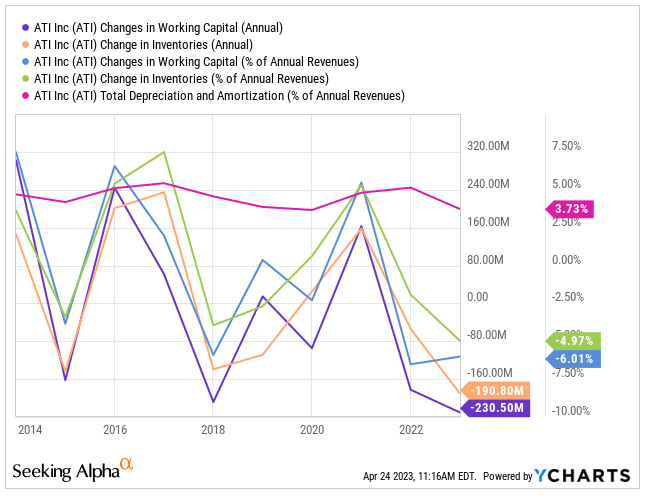

I believe that the development of new products mainly for the High Performance and Specialty Materials segment will likely accelerate revenue growth and free cash flow. Besides, I would expect that successful strategies for hiring for the development of operations could bring more output and CFO.

Source: Ycharts

ATI also has commitments to climate change regulations, which it derives part of its efforts from research and optimization of emissions in the production process. I believe that enough communication about these efforts may bring demand for the stock, which may have a beneficial impact on the cost of capital. In sum, it could be beneficial for the stock price.

I also assumed that the recent sale of subsidiaries related to the standard stainless sheet products and more exposure to higher-margin products and aerospace & defense end markets will likely bring more FCF margins. The company discussed these divestitures in a recent joint venture.

We announced a strategic repositioning of our SRP business, which included exiting production of lower-margin standard stainless sheet products, streamlining the production footprint of the AA&S segment and making certain capital investments to increase its focus on higher-margin products and its aerospace & defense end markets.

In 2022, we announced the termination of the Uniti joint venture, which is expected to be dissolved in early 2023, and in 2020, we indefinitely idled the manufacturing operations of the A&T Stainless joint venture. Source: 10-k

Finally, I am quite optimistic about the fact that ATI expects to increase its titanium production up to 35% from existing assets. It is worth noting that the titanium market is experiencing a period of expansion , which may benefit the cash flow statement of ATI.

{kind=link}

My DCF Model

I made several assumptions to design my cash flow model that readers may want to know. First, I assumed that future net income growth would be close to 6.27%, which is quite a conservative assumption.

The global advanced materials market size was estimated at USD 61.35 billion in 2022 and it is expected to hit around USD 112.7 billion by 2032, poised to grow at a CAGR of 6.27% from 2023 to 2032. Source: Advanced Materials Market Size To Hit USD 112.7 Bn By 2032

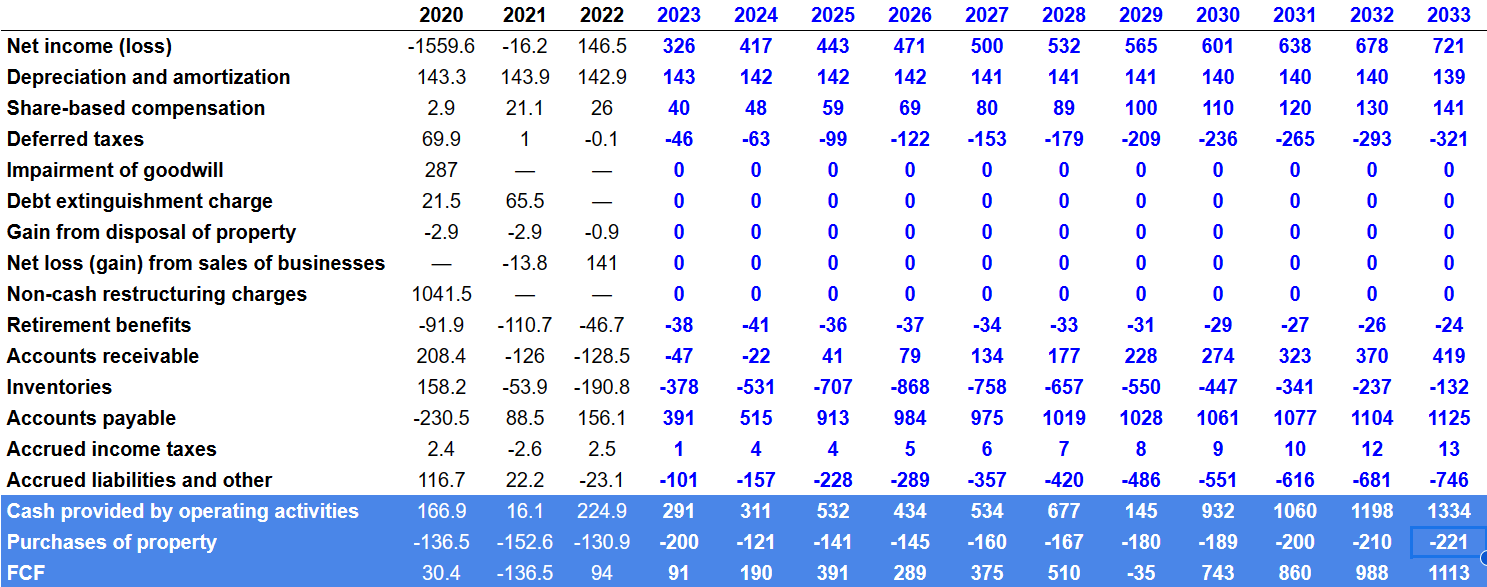

I did not include any impairment of goodwill, debt extinguishment charges, gains from disposal of properties, or net losses from sales of businesses. I consider that these items are not part of the daily operations of the business model. Finally, I used some of the financial figures obtained from previous cash flow statements to assess future changes in inventories, changes in accounts receivables, changes in accounts payable, and D&A .

{kind=link}

My numbers included 2033 net income of $720 million, depreciation and amortization around $139 million, share-based compensation close to $140 million, and deferred taxes of around -$322 million. Besides, with changes in accounts receivable of $418 million, changes in inventories of -$132 million, and changes in accounts payable close to $1.124 billion, I obtained 2033 CFO close to $1.333 billion, 2033 purchases of property of -$221 million, and 233 FCF close to $1.113 billion. I also want to mention that I expect increases in CFO from 2023 to 2033 driven by lower capex, increases in changes in accounts payable, approximately stable D&A, and growing changes in accounts receivable.

{kind=link}

If we use an EV/FCF multiple of 9x, the terminal FCF would stand at $10.018 billion, and with a WACC of 6.8%, the enterprise value would be close to $8.211 billion. If we sum cash and cash equivalents of $584 million, and subtract short-term debt of -$42 million, long-term debt of -$1707 million, and pension liabilities of -$226 million, the implied price would be $53-$54 per share.

Source: My DCF Model Source: My DCF Model

{kind=link}

The Stock Repurchase Program And The Net Operating Loss Carryforwards Could Enhance Stock Demand

Among the reasons to follow carefully the next developments of ATI and its stock price dynamics, we have the open market repurchases announced by ATI. In my opinion, the acquisition of shares by ATI could accelerate the demand for the stock. Besides, as soon as new investors learn about the program, the interest in the stock may also increase.

Open market repurchases are structured to occur within the pricing and volume requirements of SEC Rule 10b-18. The stock repurchase program does not obligate the Company to repurchase any specific number of shares and it may be modified, suspended, or terminated at any time by the Board of Directors without prior notice. In 2022, we used $139.9 million to repurchase 5.2 million of our common stock under this program. Source: 10-k

Finally, there is the fact that the company is not expected to pay state income taxes for some years because of accumulated net operating loss carryforwards. Less income taxes mean more money for shareholders, so it is another appealing feature that, I believe, is worth mentioning.

We do not expect to pay any significant U.S. federal or state income taxes in the next several years due to net operating loss carryforwards. Source: 10-k

Risks

ATI is highly dependent on some key customers with whom it maintains long-term contracts, subject to renewal in the future, which is a relevant risk. If one of the large clients decides to leave the company, the decline in FCF could bring the stock price down. Besides, negotiation with clients may also be complicated as ATI may not have a lot of bargaining power.

In the same way, part of the revenue of the alloy solutions segment comes from commercial activities with companies in the gas or oil power generation market. The energy industry is going through great changes due to the war situation in Ukraine. Prices and activities have been exposed to a high degree of volatility. ATI may be affected as supply chain risks may appear, and may also bring lack of materials needed for production.

I also found risks due to the organization of its workforce, climate change, and possible disruptions in the security system or the conservation of intellectual property. Any of these risks could impact future FCF expectations, which may lead to lower intrinsic valuation of the stock price.

My Takeaway

ATI reports long-term contracts with large clients and exposure to different industries. I believe that the recent divestitures and strategic repositioning of the SRP business to lower the exposure to stainless sheet products reflect brilliant strategy. Besides, In my view, new investments in high margin activities or the aerospace & defense end markets will likely accelerate future free cash flow. I did find risks from price volatility in the energy markets or dependency on some key customers, however the stock, in my view, appears undervalued.

For further details see:

ATI: Investments In Aerospace And Defense Make It Undervalued