ALLIF - Atlantic Lithium: Construction To Soon Begin On Flagship Project

Summary

- Atlantic’s Ewoyaa Lithium Project has a reserve of 18.9Mt (Probable) and is slated to produce 255ktpa of SC6.

- The mine is scheduled to come online next year and is being financed, in large part, by Piedmont Lithium.

- A possible resource increase and the approach of production should help the stock.

Atlantic Lithium Limited ( ALLIF ) is an Australia-based lithium miner whose main asset is the Ewoyaa Lithium Project located in the West African country of Ghana. And while the mine has yet to begin production, Atlantic has been able to lock down most of the project's funding through an interesting financing agreement it struck with Piedmont Lithium Inc. ( PLL ) in 2021. The deal, which includes an offtake agreement for half of the Ewoyaa's production, has allowed Atlantic to continue developing the project without constantly having to tap equity markets for additional funding.

The mine looks set to begin production in 2024, and once fully ramped its output should be in league with that of Sigma Lithium Corporation's ( SGML ) Grota do Cirilo project, located on the other side of the Atlantic Ocean in Brazil. But in spite of that, Atlantic Lithium's valuation is a far cry from that of Sigma's, whose market cap is an order of magnitude higher than that of its Australian counterpart. In this article, we'll review Atlantic's operations and discuss the company's potential future valuation.

Background

As it currently stands, Atlantic's Ewoyaa property has a resource size of 30.1Mt (I&I) with an average grade of 1.26%. This past September, the company established its Maiden Reserve when it released a Prefeasibility Study in which it classified 18.9M of those tonnes as a Probable Reserve graded at 1.24%. And it plans to extract those 18.9Mt at a pace of 255ktpa over the next 12.5 years. The company will take the spodumene that it mines from Ewoyaa, concentrate it to a level of 6%, and sell that SC6 to both Piedmont and international markets. It's as simple as that.

The Ewoyaa Project is located in southern Ghana and is just 110 kilometers from the deep-water port of Takoradi, a port that currently ships bauxite as well as manganese and will presumably be quite capable of handling Atlantic's SC6 shipments. Ghana is a stable country as well as a mining-friendly jurisdiction and is already home to several mining operations that drill for gold, silver, crude, natgas, in addition to the aforementioned bauxite and manganese.

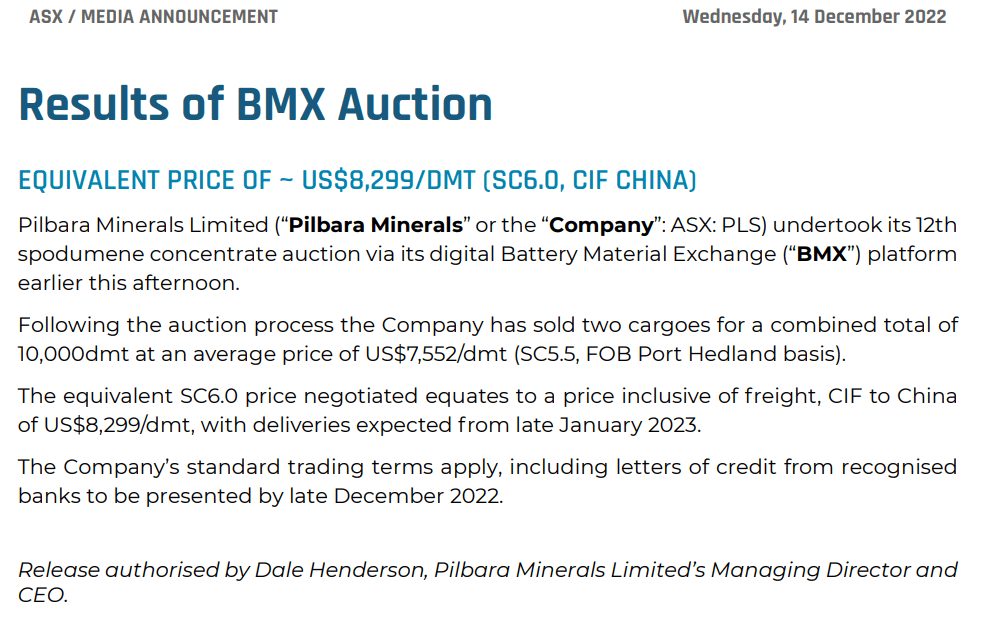

The PFS revealed some impressive numbers for the project. It put the IRR at 224% and the NPV8% at $1.3 billion, and those numbers are based on an Opex cost of $278/t and a Capex of $125 million. If SC6 prices can remain above $1,359/t, something that seems likely at least in the medium-term given current prices at the BMX Auction, the PFS foresees Atlantic hitting a yearly EBITDA of $248 million which is just slightly below the company's current market cap of $277 million. That's why the Payback Period on the project is less than 5 months.

December BMX Auction Results (pilbaraminerals.com.au) Investor Presentation

{kind=link}

However, the real cherry on the cake for Ewoyaa is the production start date: 2024. There are currently numerous lithium projects under development in both North and South America as well as Australia, but most of these are only due to start production in the back half of this decade or later. So, if Atlantic can get the jump on them and start production next year, it may be able to take advantage of an extended period of tight global lithium supply and the resultant higher prices. Also, the market usually begins to take greater notice of junior miners as they near production, and that should benefit Atlantic's stock price as 2024 draws closer.

Another factor that could help the stock would be a resource upgrade, and that may occur in the first half of 2023. That's because last year, Atlantic completed a 47k meter drill program, and about a third of that was outside the Mineral Resource Estimate. What that means is that about two-thirds of the drill program was infill; it was geared towards reclassifying the resource from the current Indicated and Inferred to a more definite Measured and Indicated classification.

And reclassifying a part, or all, of the resource would certainly be a positive development; however, what would probably interest markets more would be the results of the other third of the drill program, the exploration work done to expand the resource size. That information will be released in the first half of this year along with the Definitive Feasibility Study, but preliminary assay data has been encouraging and management has discussed the strong possibility of an increased resource estimate.

Financing

Readers may be wondering where Atlantic, which had a cash balance of about $16 million in November, is getting all the money to fund this development work. And that's where Piedmont comes in.

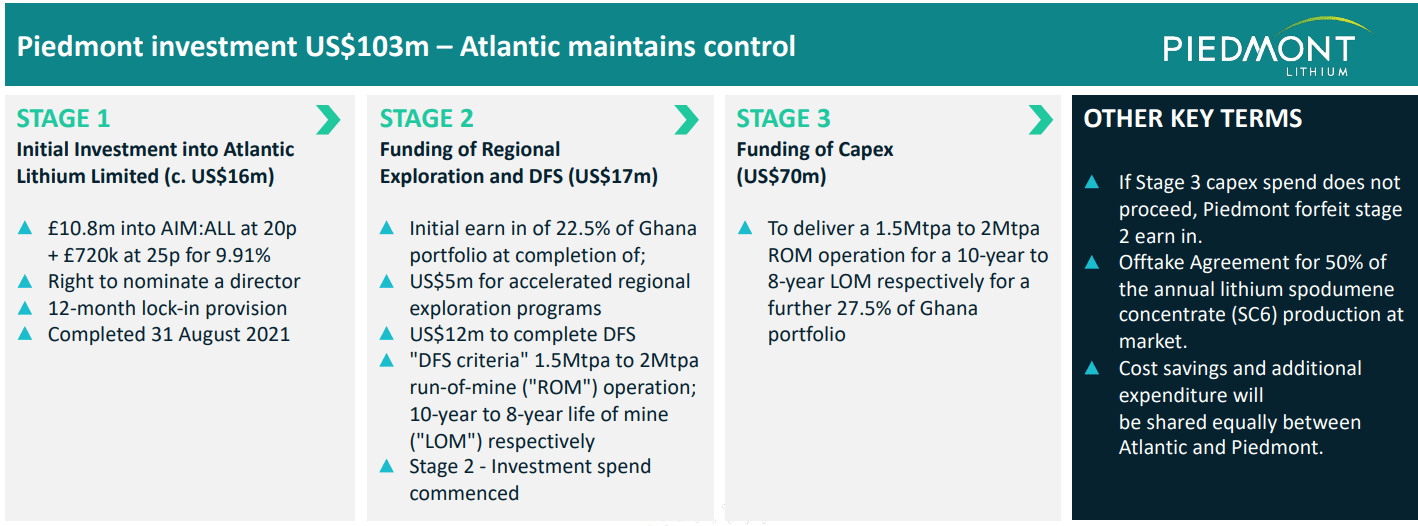

In July of last year, Piedmont's and Atlantic's management teams agreed to a complex multi-stage funding agreement, the broad details of which are included in the exhibit below.

{kind=link}

Essentially, what the agreement boils down to is that Piedmont, which currently owns about 9% of Atlantic's equity, will have the ability to earn a total equity interest of 50% of Atlantic's Ghanian spodumene projects in exchange for funding a large part of the buildout. This will include an offtake agreement for 50% of annual production at market prices on a life-of-mine basis. Piedmont will probably ship this offtake to its planned Tennessee Lithium plant for conversion to lithium hydroxide. Atlantic's management has indicated that any additional required funding can be secured by entering into an agreement with another offtake partner.

The Piedmont deal has both advantages and disadvantages for shareholders. Owning half of the company will give Piedmont a strong say in how Atlantic is managed; that's not necessarily a bad thing, but it is a factor of which current shareholders should be cognizant. On the other hand, striking a funding deal alleviated management from having to constantly run to equity markets every time the company was low on cash; that's a process that can sometimes be extremely dilutive.

Downside Risks

As with everything, there are risks inherent in Atlantic's plans. Any unforeseen construction problems and possible accidents could delay the completion of the Ewoyaa facility by many months. The feasibility of the facility, as well as the mine, are both predicated on SC6 prices remaining above $1,359/t. A sharp drop below that price could result in the company's project becoming uneconomical.

Takeaway

But despite these risks, Atlantic's stock looks like it has some upside potential. We should soon see an upside revision to the company's resource size along with the issuance of its DFS, and soon after that construction should begin on the mine. If everything goes according to plan, the stock price should begin rising as the start of production approaches.

For further details see:

Atlantic Lithium: Construction To Soon Begin On Flagship Project