ATLC - Atlanticus Holdings: Significant Market Opportunity Well-Positioned For It

2023-07-24 00:02:23 ET

Summary

- Atlanticus Holdings Corporation is well-positioned to tap into a $1 trillion market that includes general-purpose credit cards, private-label credit, and healthcare finance.

- ATLC's revenues and managed receivables have increased significantly, with revenues up 13.6% and managed receivables up 22.5%, reaching $2.1 billion.

- Despite a 300% increase in share price, ATLC's valuation remains appealing due to significant EPS growth and a return on equity near 30%.

Introduction

Much of the appeal that I see with Atlanticus Holdings Corporation ( ATLC ) right now comes down to the fact they have a massive addressable market to tap into. They estimated it to be valued at over $1 trillion. These markers are General Purpose Credit Cards, Private Label Credit, and Healthcare Finance. Spending here is only increasing and ATLC has positioned itself very well in terms of capturing this market opportunity.

The share price has run up significantly in recent months and sits at an FWD p/e of 10 right now. The p/b sits perhaps slightly higher than the rest of the sector. The company however seems to offer some investors value through buybacks they are pursuing. In recent years outstanding shares have fallen around 4%. Going forward, I expect this to continue and am rating ATLC a buy right now as a result.

Company Structure

Atlanticus has been in operation since 1996 and focuses on providing credit and related financial services to clients in the United States. Apart from this the company also has various financial products in the line. Since its founding year, they have divided the company into two primary segments, Credit As A Service and Auto Finance.

The first segment places a focus on consumer loan products and private labeling, but also general-purpose credit cards. The second segment's operations revolve around purchasing service loans that are secured by automobiles. They do this through a network of independent automotive dealerships and automotive finance companies.

Market Opportunity (Earnings Presentation)

As I mentioned in the earlier part of the article, the TAM that ATLC can tap into is massive. The largest being around General Purpose Credit Cards, the market valued at $1 trillion. The company itself describes itself as a financial technology company that enables banks, retailers, and healthcare partners to be able to offer more variety and inclusive financial services to Americans.

Market Position (Earnings Presentation)

What seems to be setting ATLC apart from others is the fact they have a broad set of offerings, but also that from an investment point of view, they have a very solid track record of profitability. Driving customer growth is key for these fintech companies and ATLC is doing a fantastic job at that. In total ATLC has 3.2 million total accounts which they serve, in just the last quarter they added 220.000 new customers, an increase of 7%. But what makes ATLC such a promising play right now seems to be the fact that even though 7% of new customers came to the company, the revenues and managed receivables increased much quicker. Revenues were up 13.6% and managed receivables were 22.5% landing at $2.1 billion. These solid results have helped ATLC reach a very impressive ROE, nearly 30% using the trailing 12 months' results.

Fundamentals

With fintech companies, the main points to watch are the number of customers they are adding and how quickly. It's a very competitive landscape with some of the larger players being Stripe ( STRIP ). Taking market share is important and it seems ATLC is doing so right now.

With 3.2 million accounts serviced that nets ATLC a revenue per customer of $81. That amount is quite high and for the full year, it would mean $326 per account if the same revenues continue for Q2, Q3, and Q4. So far this has netted ATLC a ROA of 4.92% in the last 12 months and I see it as reasonable to assume that a higher rate will happen for the coming quarters.

Growth Rates (Seeking Alpha)

ATLC is a growing company in the financial sector. Seeing from the chart above the CAGR of revenues for the last 10 years is 22.27%, with a lot of that happening in the last few years. But it seems that for the second half of 2023, the economy in the US where ATLC has its operations is set to slow . Seeing this impact on the revenue will be crucial for Q3 and Q4. I think that if ATLC shows reliance and still is growing its customer base then a far higher valuation for the company should be applied.

Valuation & Comparison

{kind=link}

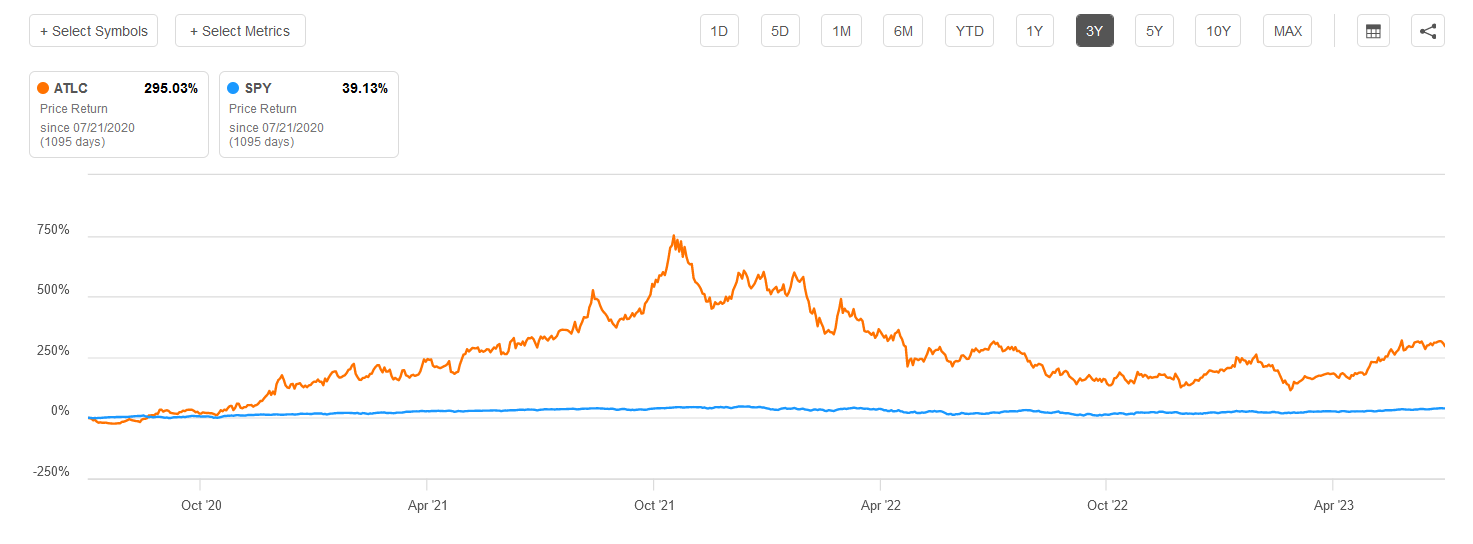

The performance of the share price for ATLC over the last few years has been nothing short of impressive. Up nearly 300% the hype around the business and its addressable market is setting them up to be a major source of returns for investors. Despite the run up the valuation doesn't seem out of line as ATLC has been able to back up the hype around it very well.

With the p/e at 10 and significant EPS growth, both historical and ahead makes the price is very appealing. Looking at how ATLC has been able to leverage the loans and deposits into higher earnings it's impressive, a ROE near 30% is fantastic and bolsters the buy case. What CEO Jeff Howard had to say about the last quarter further highlights the trajectory of which ATLC is heading.

During the quarter, lower levels of inflation and increasing wages appear to have allowed the customers we serve to regain stability in terms of credit activity. This stabilization in consumer behavior, combined with the underwriting and account management strategies we have undertaken, have resulted in improved asset performance".

Risk Associated

Regarding the automotive industry, it's essential to note that ATLC is not directly financing subprime customers; instead, it provides wholesale financing to auto dealers with credit enhancements. This approach has resulted in relatively low losses, with charge-offs staying below 1%, and 90-day delinquencies currently at 1.7%. While this segment may be relatively small compared to the overall operations, it has proven to be an excellent and well-performing business for the company.

Investment Opportunity (Earnings Presentation)

However, it's worth considering the broader implications of a slowing automotive industry on ATLC margins and operations. A sluggish automotive market can impact the overall circulation of capital in the industry. As auto sales slow down, auto dealers might face reduced cash flow and tighter margins, leading them to be more cautious with their wholesale financing and credit commitments.

Investor Takeaway

Investing in fintech might seem like risky business, but ATLC has proven that they can justify the hype around them, and with fantastic fundamentals and strong profitability the company should be viewed as a high growth company, yet one that is reliable and posts sustainable earnings. I am bullish on the outlook for ATLC and will rate them a buy.

For further details see:

Atlanticus Holdings: Significant Market Opportunity, Well-Positioned For It