ATLC - Atlanticus Holdings: Turning The Corner And Poised To Deliver

2023-10-03 00:39:01 ET

Summary

- Our investment in Atlanticus has made for an interesting journey over the past several years.

- The company now seems to be turning the corner and moving on from a period of rising delinquencies.

- Throughout this period, ATLC has continued to generate positive earnings.

- More importantly to our analysis, the company’s cash flow has continued to be strong.

- We continue to believe that shares of Atlanticus present a multiple-of-money opportunity with limited downside.

Introduction

To say that our investment in Atlanticus Holdings Corporation (ATLC) has taken us on an "interesting" ride would be somewhat of an understatement. From our initiation of the position in the low single digits, to our first report three years ago when there was no Wall Street coverage and the company just was beginning to show signs of its future potential, to the ascent through $90 per share as the COVID stimulus boosted credit performance and earnings and the structural short position associated with its retired convertible notes was closed out, to the decline back to the low $20s per share as credit performance weakened in the aftermath of the curtailment of stimulus and significant inflation and the earnings/stock momentum faded, to today.

This begs the question: where are we today with respect to our investment in Atlanticus? When we look at the data today, we are encouraged by what we see. We believe that Atlanticus is turning the corner and is poised to reward investors who are able to take a patient approach. In this report, we attempt to explain why we believe this to be the case and encourage our readers to review our prior reports for additional context.

Credit Performance

While the headlines pertaining to the U.S. consumer are no doubt negative, we believe that, as usual, these are lagging indicators. Atlanticus has been talking about credit headwinds and their response to same for several quarters now. The results of this approach can be seen in their credit metrics, and we believe that this can be attributed to the 25 + years of operating history and large amounts of data that allow them to remain ahead of these trends.

We also note that this consumer slowdown seems to be affecting higher income consumers disproportionately as the wage and employment picture remains strong for the lower income consumers and, ironically, they seem to be less at risk from displacement from AI and other new technologies. As the more prime-oriented lenders experience greater headwinds and curtail their credit availability accordingly, we believe that this will create incremental opportunities for Atlanticus.

As Atlanticus has discussed, its customers have adapted to the higher inflationary environment, and with the economy now appearing to begin to cool in response to higher rates, these pressures should begin to ease, as well. This should also bode well for a return to the capital markets, which the company did not need to access during the recent spike in rates given its long-term fixed-rate capital structure (85% is fixed-rate) with significant funding availability, which was put in place during a more benign borrowing environment.

More specifically, when we review the details of the most recent 10-Q , we are encouraged by the improvement in the credit metrics, Two of the relevant tables are below:

Atlanticus Holdings 10-Q for the quarterly period ending June 30, 2023

{kind=link}

Atlanticus Holdings 10-Q for the quarterly period ending June 30, 2023

{kind=link}

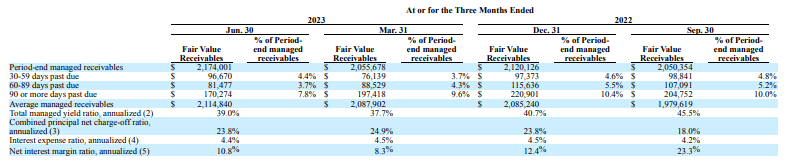

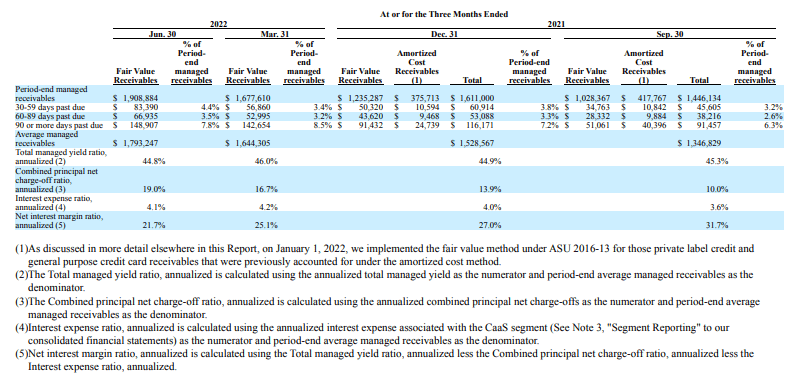

Importantly, in our view, the leading indicator of charge-offs, 90+ day delinquencies, improved meaningfully from 1Q2023 to 2Q2023. The first calendar quarter is typically a good month for delinquencies, as holiday shopping ends and debtors catch up with help from tax refunds, which makes this improvement more pronounced. In fact, the last time we saw 90+ day delinquencies under 8% was one year ago. In addition, charge-offs declined sequentially from 24.9% to 23.8%, and yield improved from 37.7% to 39.0%, resulting in the net interest margin expanding from 8.3% to 10.8% (all on an annualized basis).

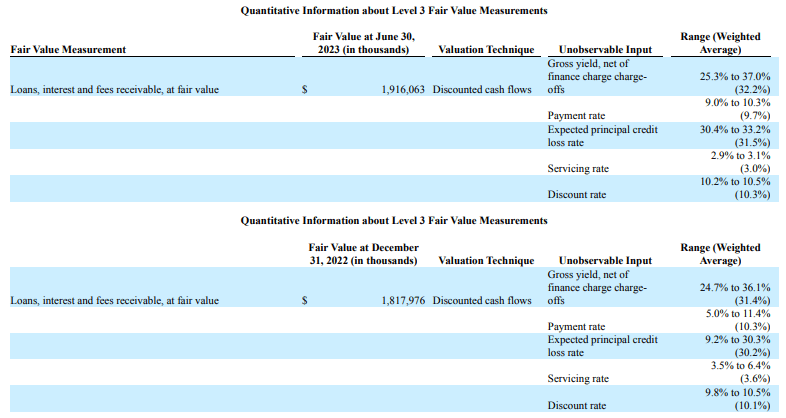

Despite these improvements in credit performance, management's accounting assumptions reflected an increase in loss expectations. As we can see from the below table, charge-off expectations as of June 30, 2023, stood at 31.5%, up from 30.2% as of March 31, 2023, and 770 basis points higher than actually realized in the preceding quarter. As we have discussed in prior reports, even during the 2008 financial crisis / great recession, Atlanticus' losses only briefly reached these levels before quickly receding (whereas the company now forecasts this loss level for the long term).

Atlanticus Holdings 10-Q for the quarterly period ending June 30, 2023

{kind=link}

As we have long discussed, we agree with management's cautious approach to loss expectations. However, investors should take note that if/when the realized losses stabilize this will result in significant earnings tailwinds (likely why those closest to these numbers - the CFO and CAO have been sitting on their significant stock positions along with the CEO and Chairman).

Management summarized Atlanticus' credit performance, credit outlook, and continued conservative accounting for loss expectations in its second quarter press release and MD&A contained in the 10-Q. Some sections that we found noteworthy are included below:

As we have observed the consumers we serve benefit from higher wages and adjust to higher cost of living, we have returned to quarter over quarter increases in new accounts served leading to our continued trend of year over year managed receivables and revenue growth.

…we included expected market degradation in our forecasts to reflect the possibility of delinquency rates increasing in the near term (and the corresponding increase in charge-offs and decrease in payments) above the level that historical and current trends would suggest.

We have noted recent recoveries in consumer spending behavior that have helped to increase the overall combined managed receivables levels and we currently expect this trend to continue further into 2023, although we expect the pace of growth to slow when compared to earlier periods due to tightened underwriting standards adopted during the second quarter 2022 (and subsequent quarters).

During 2023, we expect delinquencies to return to levels similar to those experienced in periods prior to COVID-19 and the related government stimulus programs. This expected decline in delinquencies in 2023, from those currently experienced, is predicated on the assumption that recent government efforts to curb inflation will be successful and our recent tightened underwriting standards implemented in the second quarter 2022 (and subsequent quarters), will prove effective at reducing account delinquencies.

The increase in the combined principal net charge-off ratio, annualized in late 2022 and the first and second quarters of 2023 is a reflection of the increased delinquencies noted in the latter part of 2021 and in 2022 as consumer behavior reverted to more historical norms and inflation, particularly as it relates to higher gas prices, negatively impacted some consumers' ability to make payments on outstanding loans and fees receivable.

As delinquency rates continue to be elevated relative to historically normalized levels (i.e., those periods prior to COVID-19 and the related government stimulus programs), we expect combined principal net charge-off rates to continue to increase, when compared to comparable prior periods since the onset of COVID-19. These increased charge-off rates are expected to continue through the third quarter of 2023 before returning to historically normalized levels. This expectation is predicated on the assumption that recent actions by the federal government to reduce inflation will be successful. Our charge-off ratio has also been impacted due to (and will continue to be impacted by): 1) higher expected charge-off rates on the private label credit and general purpose credit card receivables corresponding with higher yields on these receivables, (2) continued testing of receivables with higher risk profiles, which leads to periodic increases in combined principal net charge offs, (3) recent vintages reaching peak charge[1]off periods, (4) our receivables growth during 2021 and early 2022, (5) the aforementioned tightened underwriting standards implemented in the second quarter 2022 (and subsequent quarters) that will slow the pace of growth in our receivables base, and (6) negative impacts on some consumers' ability to make payments on outstanding loans and fees receivable as a result of COVID-19 and the related economic impacts. Further impacting our charge-off rates are the timing and size of solicitations that serve to minimize charge-off rates in periods of high receivable acquisitions but also exacerbate charge-off rates in periods of lower receivable acquisitions. The potential impacts COVID-19 and related economic impacts, government stimulus and relief measures may have on our ability to acquire new receivables or the impact they may have on consumers' ability to make payments on outstanding loans and fees receivable could lead to changes in these expectations.

We will be watching these credit metrics in the quarters to come.

Current Results

Driven in large part by the conservative accounting, earnings per diluted share decreased from $1.08 in 1Q2023 to $1.02 in 2Q2023. However, level of free cash flow increased to $1.90 per diluted share. (LFCF is a metric we have defined and discussed at length in our prior reports. While still somewhat affected by the company's accounting assumptions (in that part of this calculation includes the book value of the loan portfolio, which is impacted by loss forecasts), we find this to be a better indicator of the company's current performance than looking at earnings alone in light of the accounting complexity.)

We note that the company has begun to provide disclosures that allow us to more easily calculate the actual face value of the loan portfolio quarter to quarter (so seemingly unaffected by the accounting elections). Using these numbers, we calculate a LFCF of $1.82 per diluted share (but note that this number is not comparable to prior periods). The LFCF result gives us comfort that $10 per share of earnings / LFCF remains realizable as credit performance normalizes (and growth continues, we will discuss that a bit more later).

It should also be noted that the company generated $108.1 million of cash from operations in 2Q2023, which is the highest we have observed for the company going back to 2018 (the company was much smaller then and in prior periods following its implosion in the aftermath of 2008 and recovery thereafter).

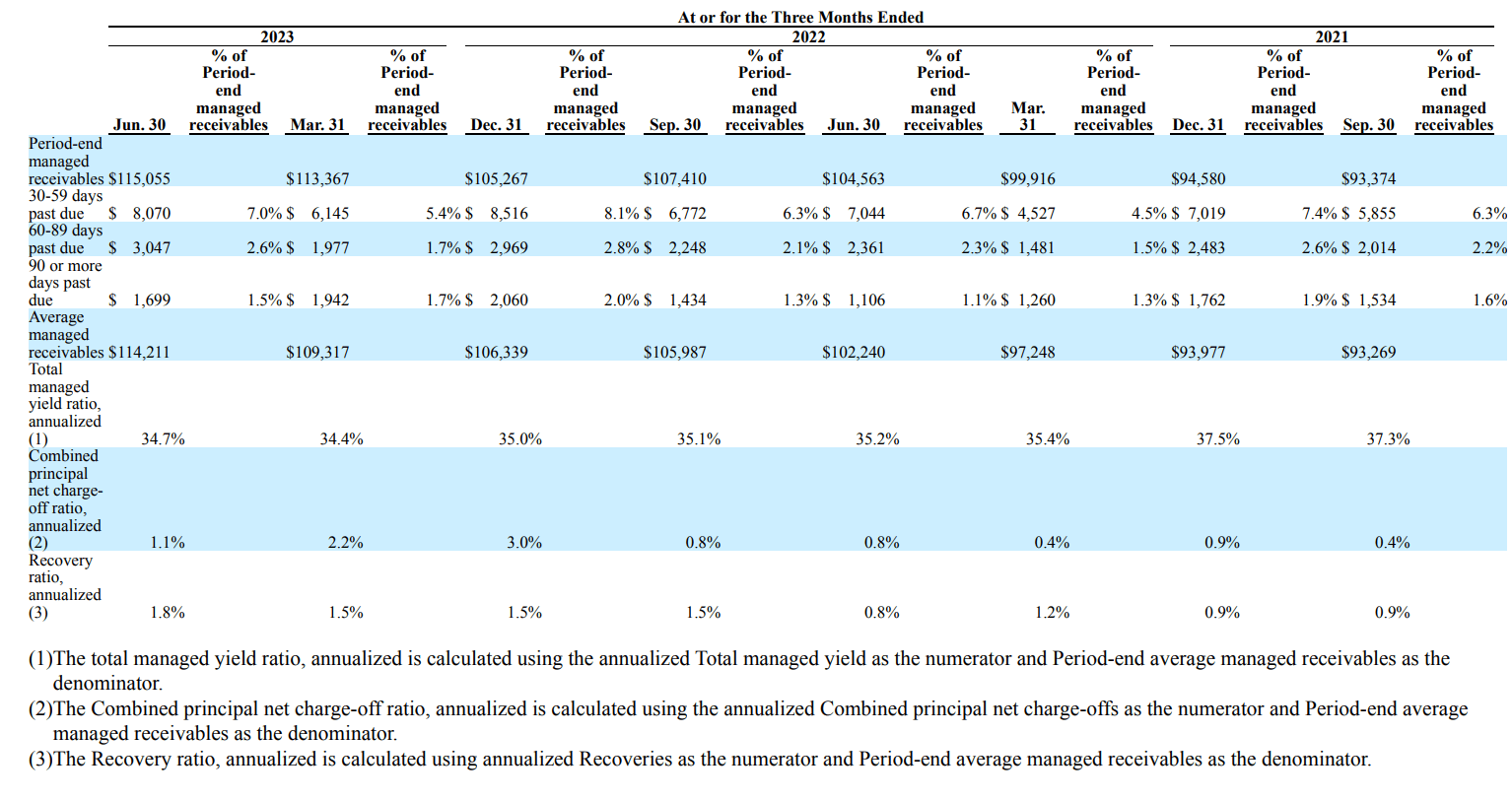

In addition, the wholesale auto lending business continues to be a niche but strong business (we would not be surprised to see this business get sold at the right time, if the tax consequences of doing so would not be prohibitive). As can be seen from the table below, in the most recent quarter, this division generated yields of 34.7% against charge-offs of 1.1%, which were less than the 1.8% recovered on the collateral.

Atlanticus Holdings 10-Q for the quarterly period ending June 30, 2023

{kind=link}

Balance Sheet

We believe that the balance sheet provides a further underpinning of value and additional downside protection to investors. As discussed in prior reports, we believe that Atlanticus is sitting on at least $20 per diluted share of cash (we say at least as, given the substantial liquidity on its non-recourse financing lines, this number can be managed for end of quarter presentation and could clearly be increased if management so elected). As a result of this $20 / share of cash, investors are paying less than $10 / per share for the business, which is currently running at ~ $4 / share of earnings (2.5x multiple) and ~ $7.50 / share of LFCF (1.3x multiple).

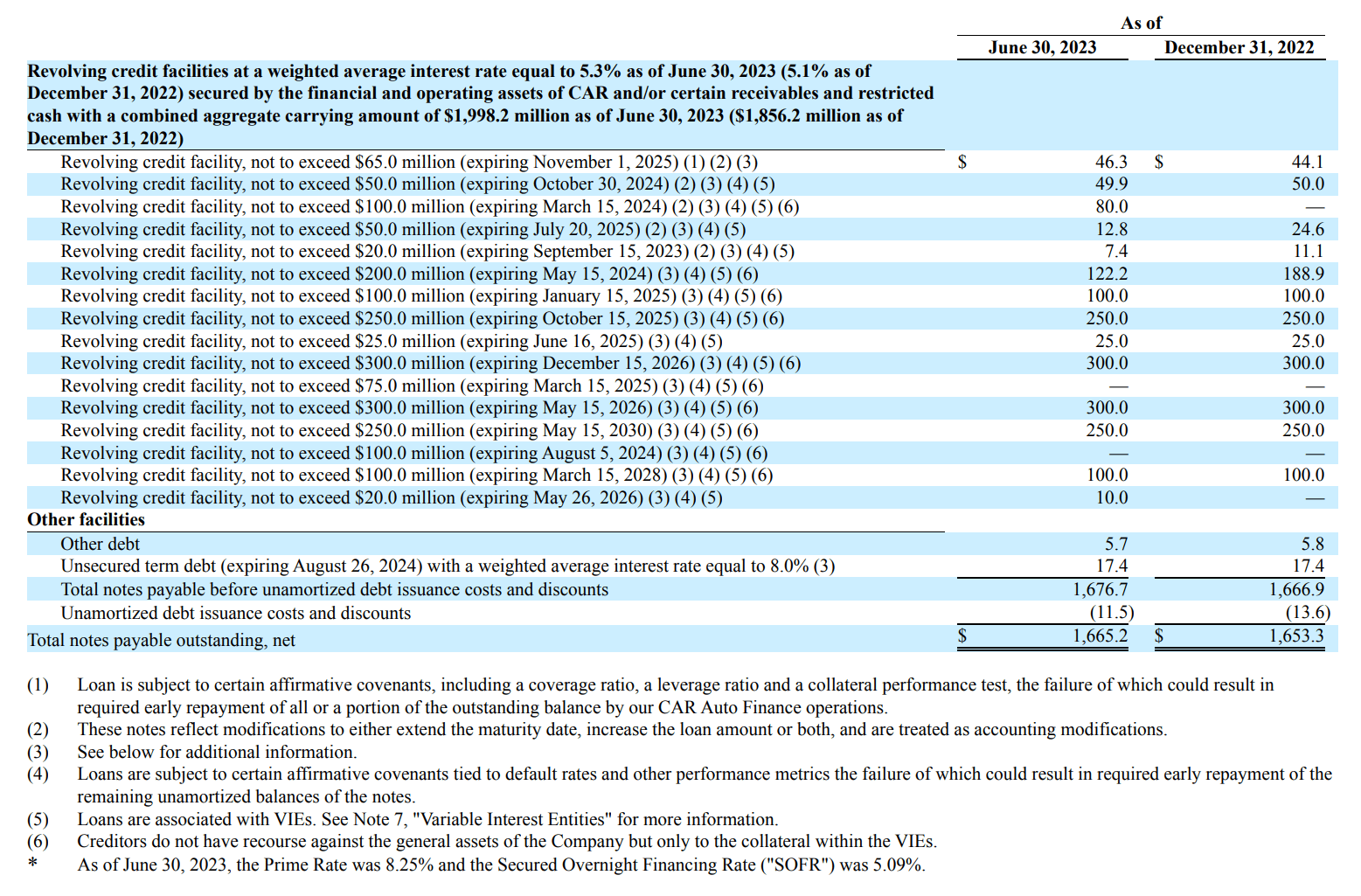

As discussed above, we think that management has done an excellent job of putting together a debt capital structure that has positioned the company well. We believe that this, like their management of credit risk, stems from their experience and the lessons learned from their near-death experience in 2008 ("good judgement comes from wisdom, and wisdom comes from bad judgement").

The debt capital structure is 85% fixed rate resulting in an annualized interest expense of 4.4% for the most recent quarter, which has barely changed for the past eight quarters, and is below the average SOFR rate for the quarter, which was north of 5%! The debt capital structure also contains substantial liquidity, with unused availability at June 30, 2023 calculated by us to be $345 million. In addition, a substantial portion of the debt is non-recourse to the holding company and contains liquidation tail periods. This data and other additional information on the debt structure (including debt maturities) can be found in the following table:

Atlanticus Holdings 10-Q for the quarterly period ending June 30, 2023

{kind=link}

We also think worth mentioning book value, which has been quietly but steadily increasing and now stands at $363.3 million (or $320.0 million to the diluted common shareholders when including the capital associated with the in-the-money convertible preferred and subtracting the $81.4 million of liquidation preference associated with the perpetual preferred) equating to approximately $17 per share, which we believe is significantly understated given what are effectively the large "reserves" on the balance sheet due to the conservative credit loss assumptions used in the company's fair value accounting, as discussed above. Nonetheless, we believe that this provides an additional underpinning of value.

Share Activity

With a large insider ownership position, reported to be 74% in Atlanticus' second quarter investor presentation , we continue to pay close attention to the share activity of key insiders and the company. We note that, as has been the case for some time, the important insiders (Chairman / Founder, CEO, CFO, and CAO) continue to hold their significant stock position despite the window being open for stock sales by insiders (as evidenced by a small stock sale by certain directors).

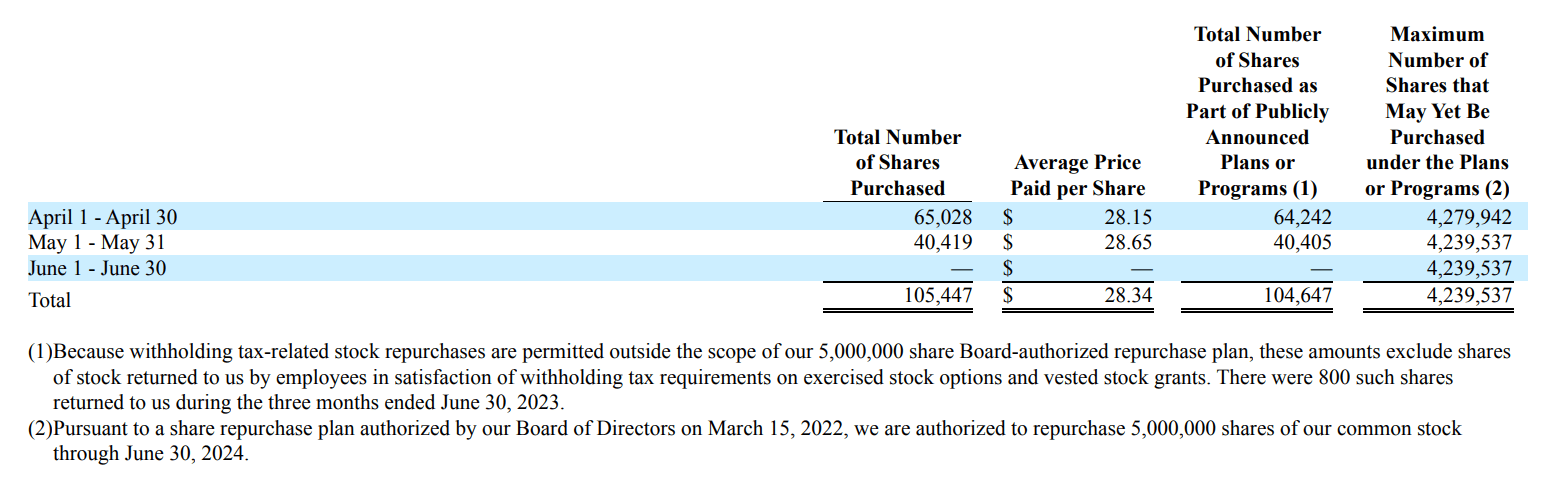

In addition, the company continues to retire shares, with 105,447 repurchased in the quarter as seen below:

Atlanticus Holdings 10-Q for the quarterly period ending June 30, 2023

{kind=link}

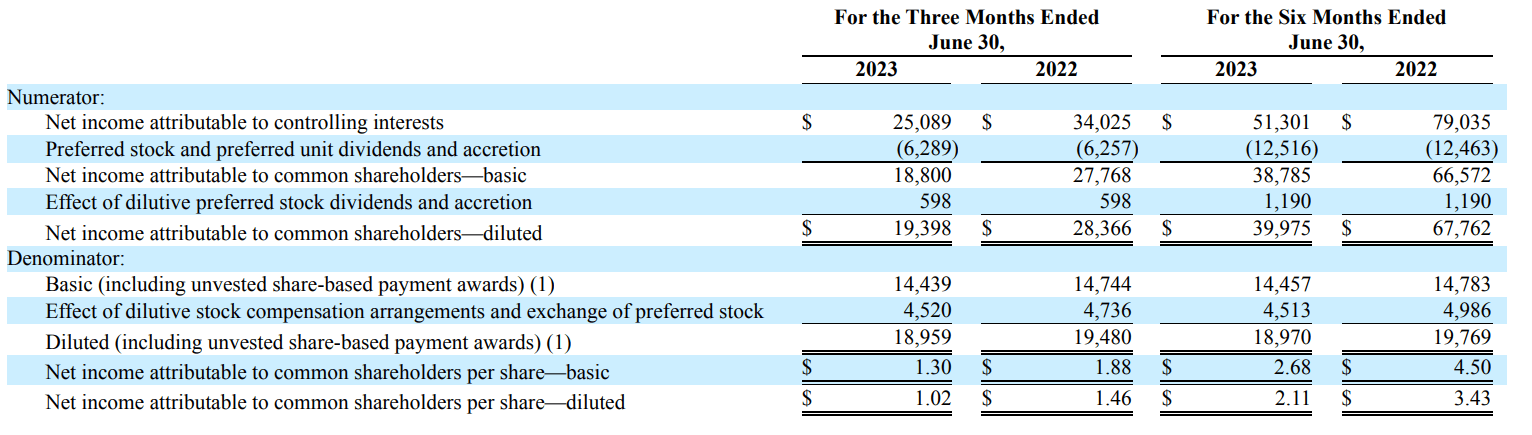

This steady progress has reduced the fully diluted shares as seen below:

Atlanticus Holdings 10-Q for the quarterly period ending June 30, 2023

{kind=link}

We continue to pay close attention to this activity.

Growth

In addition to what we believe is an attractive valuation based on the current results, we believe Atlanticus is poised to continue to grow in light of its early action to address credit performance, platform, balance sheet, market opportunity, and other factors discussed in this report. Management also is striking an optimistic tone on the topic of growth, which we believe is the result of having addressed credit headwinds early on and more opportunities due to the overall tightening credit environment in the industry.

We are seeing growth across each of our product offerings. Our retail credit offering grew through new client roll outs as well as period over period growth from existing clients. Our general purpose managed receivables also grew year-over-year, even as the total number of customers served by that business line declined due to our tightened underwriting beginning in the second quarter of last year. General purpose receivables growth was due to higher credit line utilization as the portfolio matures, as well as an increase in the number of new customers on a quarter over quarter basis. In total, we added over 350,000 new accounts on behalf of our bank partners in the quarter, up from approximately 220,000 in the first quarter of 2023."

Risks

We also believe it is important to reassess the risk with respect to our investment. In addition to reviewing the risk factors outlined by the company in its public filings, we note the following as being at the top of our list.

Credit. In our opinion, the most significant risk to our investment in Atlanticus is its credit performance and the company's management thereof. We have discussed our views in detail above and continue to pay close attention to these metrics.

Regulatory. There is constant noise here as there seemingly always has been and likely always will be. For example, a bill in the Senate, that would limit interest rates federally, has been reintroduced and is making some headlines. This bill has failed before and we don't see passage at this time as likely. Our view is that access to credit for non-prime customers is a necessity to life, without which their circumstances would be much worse as they would then be forced into adverse outcomes (loss of home, car, job), predatory unregulated borrowing options, punitive overdraft fees, etc. Nonetheless, we are monitoring the regulatory environment closely.

Insider activity. We continue to be concerned that insiders, who already own 74% of the company, will grow tired of the public market costs and requirements (including detailed disclosures available to their competitors) and/or will see opportunity to buy-in the remaining shares outstanding. We are concerned that the insiders could use market fears of recession or other company-specific or macroeconomic concerns to justify a price below the true value of the shares. So far, Atlanticus' share repurchase actions have been through voluntary share buybacks, etc., which we believe benefit the remaining shareholders. But we worry about something more coercive that could occur as it seems clear that management continues to see value in excess of market prices. We will be watching this carefully.

Conclusion

All told, we remain optimistic regarding our investment in the common shares of Atlanticus. We believe the company is positioned to generate $10 / share of earnings / level free cash flow on an annualized basis in a normalized credit environment (investors can refer back to our more detailed report on our internal expectations , which we continue to update for our internal purposes). As discussed above, management continues to repurchase shares, which continues to help the denominator aspect of the earnings equation.

We believe the company is well-positioned to generate attractive returns and to grow its business. Despite the headlines, the reality is that there is large number of consumers that need access to the sort of credit Atlanticus provides. We also believe that as a result of its experience, data / systems, management, balance sheet, and the other factors discussed above, the company is well positioned to access this growing trillion-dollar + market as measured by the ABA. We want to be owners of companies in this position.

As such, when coupled with the approximately $20 / share of cash (which could be increased by drawing down on the availability of its non-recourse lines), we continue to believe the stock can be worth $80 or more per share. When contrasted with the downside protection of the cash on hand, we continue to find this to be quite compelling.

For further details see:

Atlanticus Holdings: Turning The Corner And Poised To Deliver