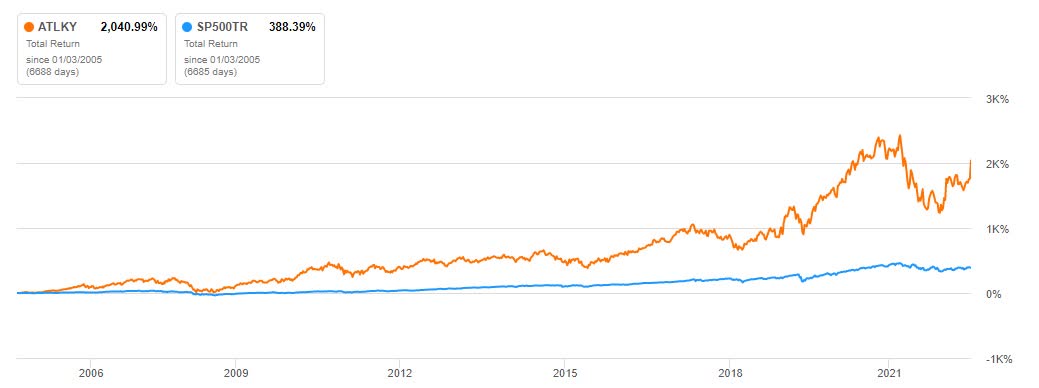

ATLKY - Atlas Copco: A World-Class Capital Allocator But Overvalued

2023-05-03 02:17:33 ET

Summary

- Atlas is a world-class capital allocator with tremendous growth opportunities.

- Well-executed management decisions in the past have resulted in astonishing operating margins in an industry not normally known for them.

- Only the high valuation is a bit much in my opinion, but quality usually has its price and Mister Market sometimes helps by offering better entry points in the future.

Thesis

{kind=link}

Atlas Copco ( ATLKY ) is one of those underappreciated, boring companies that produces spectacular returns for its shareholders every year. It is very shareholder-friendly, has a long-term focus, is trying to make the future better and is also a global champion in its markets.

Capital allocation is world class and the company has every opportunity to grow organically or through acquisitions. The only downside is that the company is always expensive due to its high quality. However, due to market fluctuations, there is always a time when you can get this company at a reasonable price.

If you are already a shareholder with a low average purchase price, just hold and enjoy the returns, but as someone looking to start a new position, I would take some time to wait for better entry prices with a lower multiple.

Analysis

Q1 2023 Atlas Copco Presentation

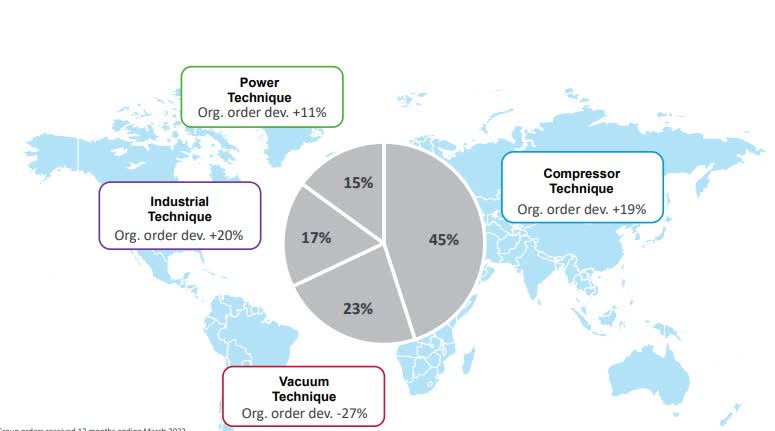

The Q1 results released last week were good as usual. Orders: + 5%, revenues: +18% and an improvement in ROCE from 27% to 29%. The long-term upward trend is clearly visible in the chart above, and all of this with an excellent operating margin of 20%+.

The record order intake in the last quarter was mainly driven by an increase in compressor technology sales. However, the company's long-term outlook, with its divisions focusing on energy efficiency, energy recovery, CO2 reduction, automation and solar energy, is perfectly positioned for the future.

The company is also growing organically and through acquisitions, with a significant part of its current growth coming from acquired companies . This shows that they are efficient in their M&A transactions.

The management team's capital allocation is excellent and clearly world class.

- Compressor technology: ROCE: 82% / Oper. margin: 24%

- Vacuum technology: ROCE: 24% / Oper. margin: 22,7%

- Industrial technology: ROCE: 18% / Oper. margin: 21,1%

- Power Technology: ROCE: 24% / Oper. margin: 19,1%

And from January to March they had the following results for the whole company: ROCE: 29% / ROE: 32% / Operating margin: 21,8%

Such a high return on capital, combined with the ability to invest in future growth, is one of the best foundations for exceptional future shareholder returns.

{kind=link}

The largest segment, Compressors, has the best ROCE and operating margins and grows by 19% due to favorable environmental trends.

Q1 2023 Atlas Copco Presentation

They also continue to invest heavily in research and development, seeing innovation as a key building block for a better future. And I think R&D investment is always a good thing to see because it shows a long-term perspective and probably a better future for shareholders and the company.

{kind=link}

Here is a picture from one of their presentations where they talk a little bit about their acquisitions and in particular the point where they talk about acquiring leadership in niche markets I think is an important point for their success in M&A. This is a strategy that a lot of serial acquirers use and have had a lot of success with.

{kind=link}

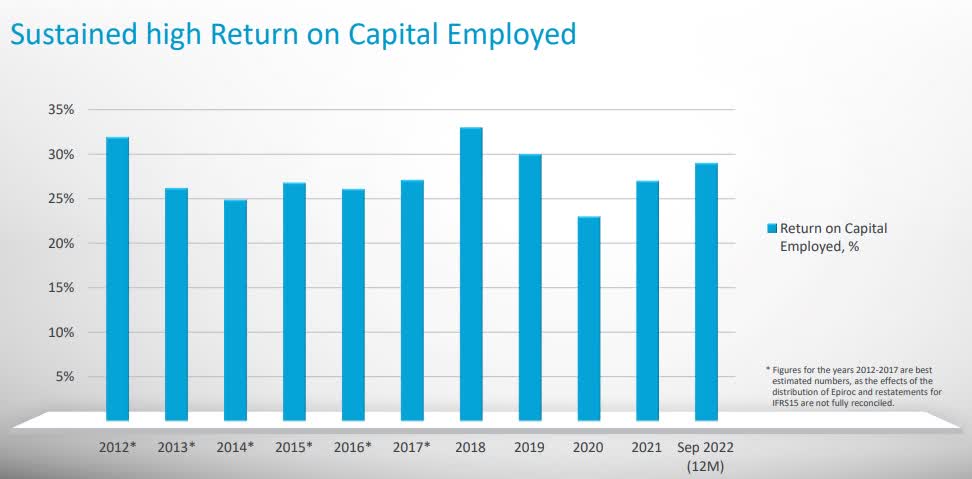

As Atlas has a strong focus on ROCE, they have published this data where you can see that they have a 10 year average of over 25%. That puts them in a group with very few companies over that period. And as I believe that shareholder returns will be similar to ROCE in the long term, this is a fantastic result for me.

{kind=link}

Another point that is rather unusual for a company like Atlas is that it is relatively asset light. This is also reflected in their very strong operating margins.

FY22 Investor Presentation

Normally I like it when companies are still founder-led and the founders have a lot of skin in the game, but unfortunately at Atlas the insider ownership is relatively low. But in Investor AB (IVSXF) they have one of the best and biggest Swedish companies as their main shareholder. Investor itself is also a very interesting company with outstanding returns.

{kind=link}

The biggest and perhaps only real criticism is the valuation. With an EV / EBIT of 22, it is quite expensive and I would like to see a multiple below 17 to build a large position. And the long-term chart shows that such multiples are available from time to time, and sometimes even cheaper. Any time the multiple is close to 13, it is a massive bargain for such a spectacular capital allocator.

Atlas' long-term plan is to return 50% of profits to shareholders as dividends and to achieve average annual sales growth of 8%. But they have a history of under-promising and over-delivering on sales growth. So double-digit annual shareholder returns should be possible over the long term if they meet their targets. Perhaps even in the 15-20% range over a 10-year period.

In addition, they have a strong balance sheet due to their cash position combined with their available credit facilities when we consider the maturity of their debt.

Conclusion

Atlas is a company with a high ROCE, which clearly demonstrates that it is a high quality allocator of capital; it also has very strong operating margins and a clear long-term focus. This, combined with its products that are critical to its customers' operations and its world-leading compressor technology, gives it a strong competitive advantage.

And as they are also investing in a better future for humanity, helping to create a low-carbon society and improving energy efficiency, this is clearly a good investment for investors and for society. The only downside is the relatively high valuation at the moment, but if the past is a good guide, there will be a better entry point somewhere in the future.

For further details see:

Atlas Copco: A World-Class Capital Allocator, But Overvalued