ATLKY - Atlas Copco: Decentralized Industrial Player With Structural Growth Tailwinds

2023-11-01 08:56:50 ET

Summary

- Atlas Copco is a decentralized industry player with a diverse range of products and divisions, allowing for quick adjustments to regional strategies.

- Services make up a significant portion of the company's revenue, providing stability and customer loyalty.

- The company's M&A strategy has been successful in expanding into new markets and enhancing research and development capabilities.

Atlas Copco ( ATLKY ) is a decentralized industry player manufacturing compressors, vacuum techniques, industrial techniques, and power technique-related sustainable products. The company, well-known in Europe and based in Sweden, was founded in 1873. Their business has been growing through both organic and acquisition-driven methods, aiming for an 8% average revenue growth over business cycles. The decentralized organization enables them to adjust their regional product and marketing strategies quickly, and their products are well-positioned in several structural growth areas. I assign a “Buy” rating with a target price of SEK 155.

Diversified and Decentralized Player

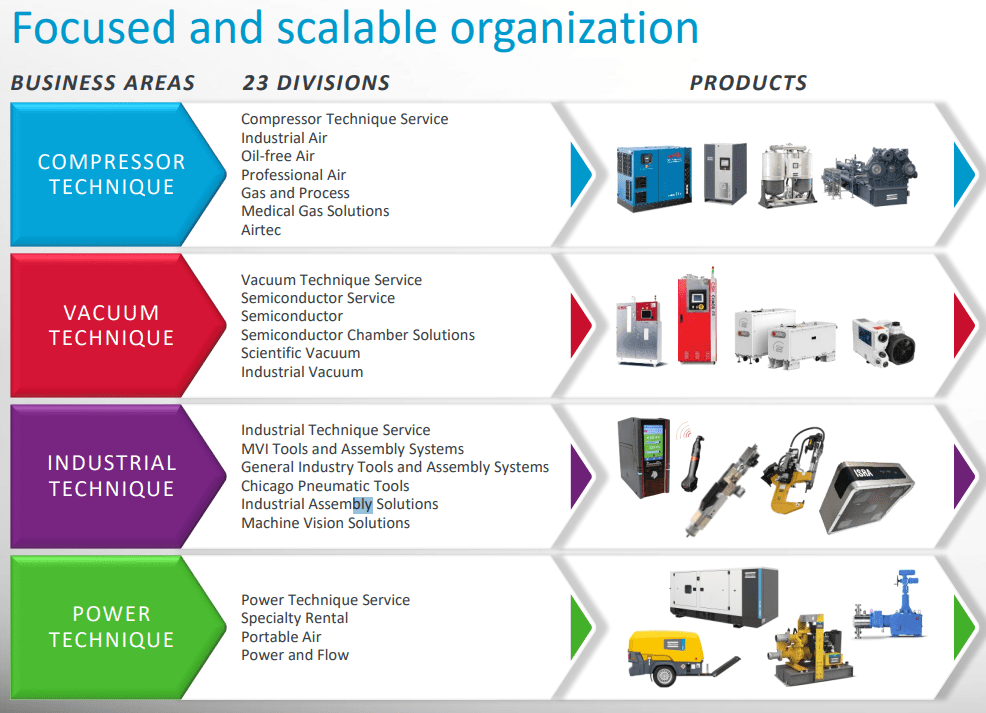

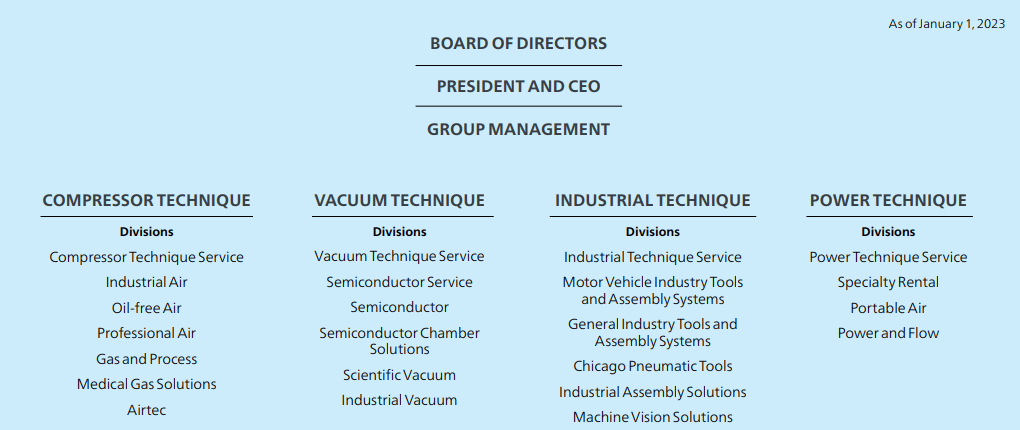

Atlas Copco is divided into four segments, comprising a total of 23 divisions. Each business segment has its own product research centers, distribution and manufacturing facilities, serving different end-markets.

{kind=link}

{kind=link}

These four business segments are supported by 23 different divisions. Each division operates as a separate unit, responsible for its own P&L, decision-making, and strategic initiatives. I believe the decentralized organization benefits Atlas Copco in several ways. Firstly, each business unit operates within its own cycle and end-markets. Therefore, it is ideal for these separate units to manage their working capital and P&L independently, enabling them to adapt more quickly to their specific end-markets. As illustrated in the table below, the four segments have exhibited different growth patterns across various industrial and semiconductor cycles.

{kind=link}

Secondly, each division sets targets and creates action plans to enhance its strategic position within the group. These divisional targets should be more realistic and tailored to their specific products and services. Instead of adhering to a unified financial target, each division can adjust its operating costs according to its top-line growth prospects. Lastly, the decentralized organization enables better alignment of divisional performance with individual compensation structures.

{kind=link}

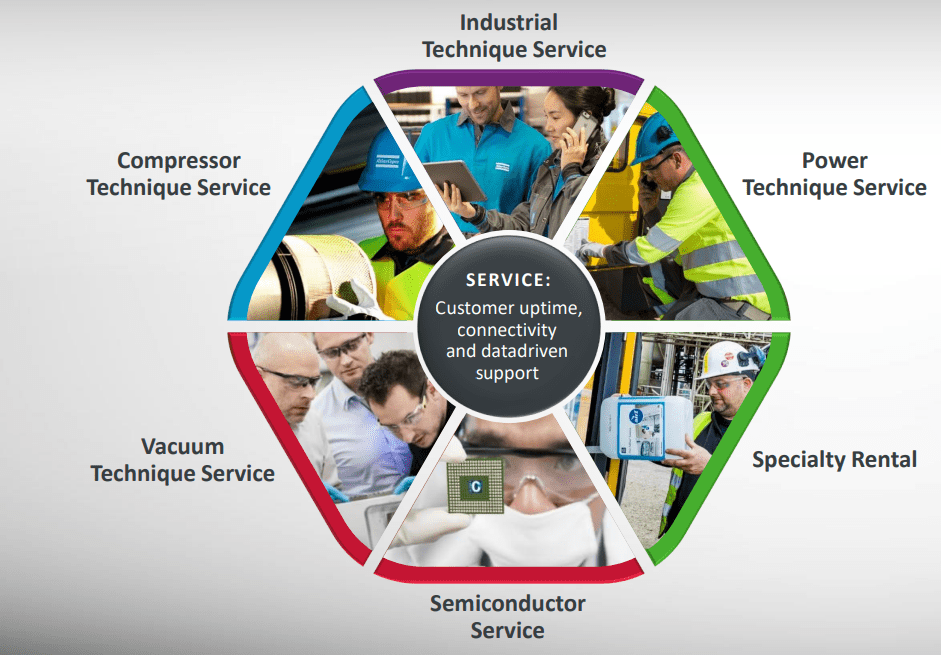

Services Revenue Brings Stabilities

Services represent approximately 35% of the total revenue, providing technical support for equipment, consumables, spare parts, as well as specialty rentals. In my view, the service component is crucial for the company. Services are highly recurring in nature, whereas equipment sales are influenced by end-market cycles. Additionally, equipment services can enhance customer loyalty, increasing product stickiness with their end-customers.

{kind=link}

In their power technique business, services have been growing at a compound annual growth rate of 9% from FY12 to FY22, compared to 3% growth for equipment sales. With the integration of industrial 4.0, more equipment is becoming connected, leading to an increased demand for services compared to standalone machines. I believe Atlas Copco will continue to expand their service business, making their business model more resilient during economic downturns.

M&A Strategy

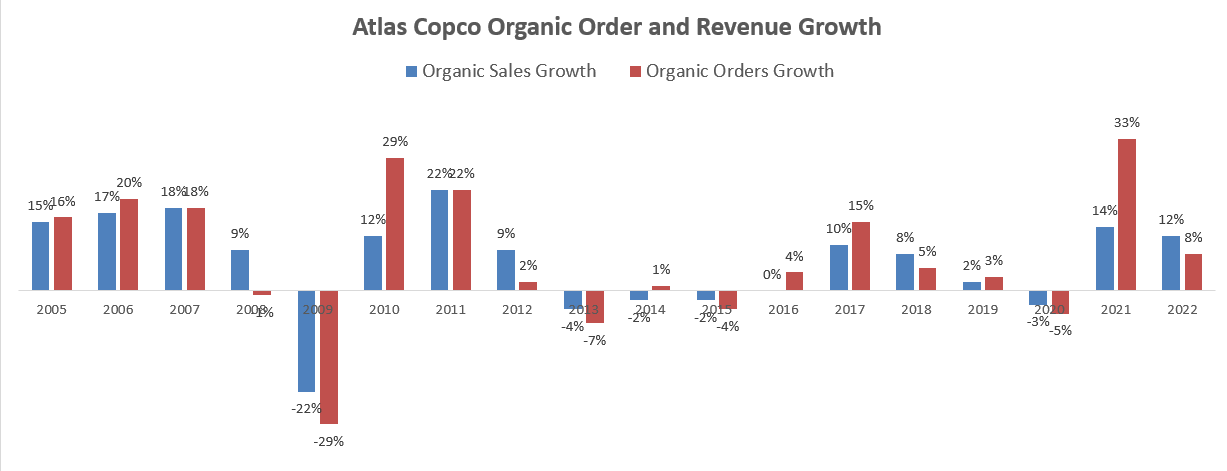

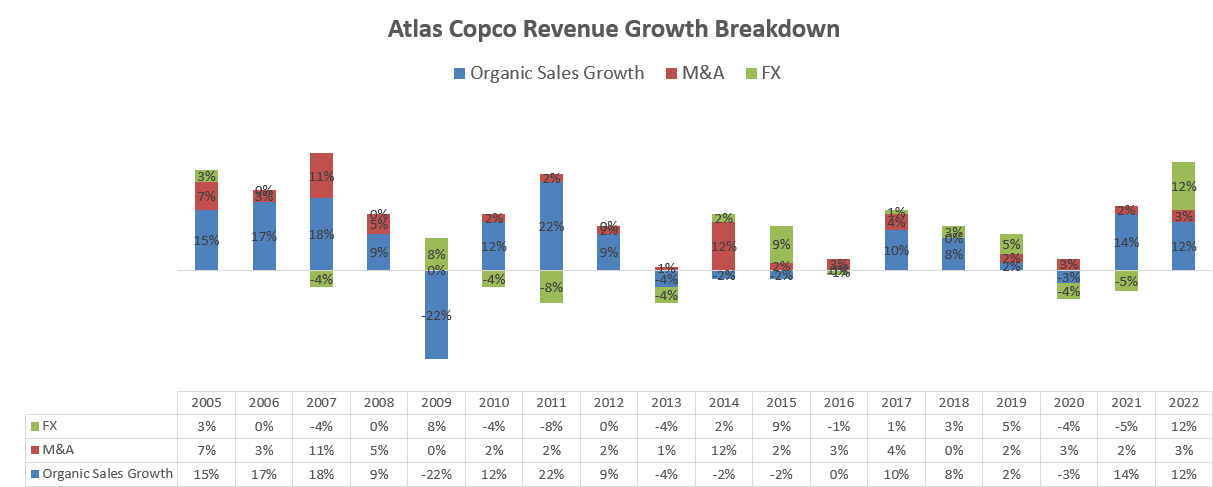

Atlas Copco's product strategy is focused on niche markets with unique value propositions for their customers. In addition to organic revenue growth, they have been using cash from operations for tuck-in acquisitions, resulting in a combination of organic and acquisition-driven growth, as illustrated in the chart below.

{kind=link}

Mergers and acquisitions play a crucial role for Atlas Copco as they facilitate expansion into new niche markets, broaden their customer base, and enhance their research and development capabilities. In the past five years, they have invested over SEK 35 billion in acquisitions, compared to SEK 82 billion in free cash flow. Their robust track record in tuck-in acquisitions and seamless integration can be attributed to their decentralized organization. Each individual deal has been integrated into the relevant division, consolidating their back-office, salesforce, manufacturing, and R&D centers efficiently. The decentralized structure allows them to swiftly integrate new businesses. For example, when Atlas Copco acquired Edwards Group in 2014, they bolstered their expertise in sophisticated vacuum products and abatement solutions, essential components in the semiconductor industry. The demand for vacuum products in the semiconductor sector has surged in recent years as more fabrication facilities have been established.

Growth Tailwinds

More energy efficient products: Atlas Copco has been actively developing energy-efficient products in recent years. For instance, they introduced Variable Speed Drive compressors two decades ago and launched the third generation of Variable Speed Drive compressors in FY22, achieving energy savings of up to 60% according to their FY22 annual report . In their semiconductor division, Atlas Copco is deploying the 3rd generation EUV system, which reduces energy consumption by 50%.

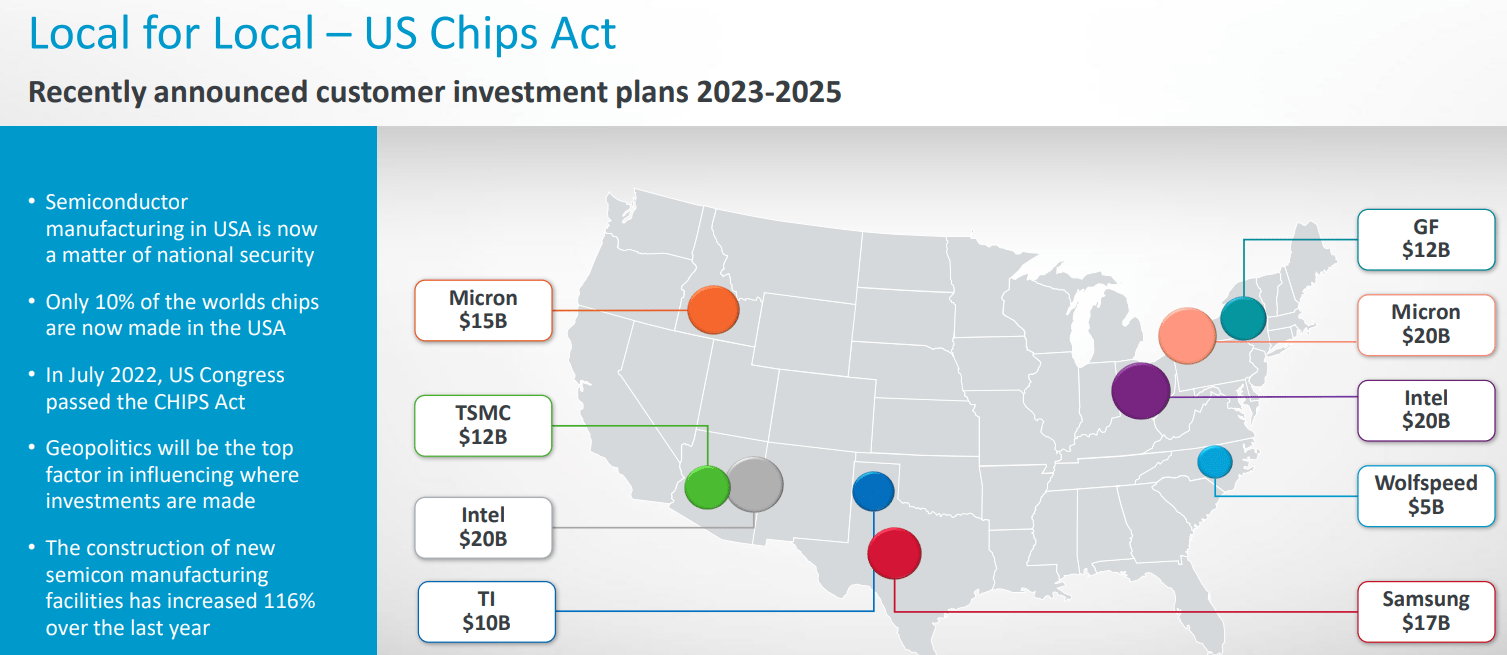

Semiconductor Vacuum: Regarding semiconductor vacuum technology, despite the cyclical nature of semiconductor capital spending, the industry is experiencing a significant upward trend. Atlas Copco is a leading provider of vacuum solutions for semiconductor fabs. Their vacuum technique business demonstrated impressive organic growth, with a 24% increase in FY21 and an additional 16% in FY22. Notably, according to the White House , companies announced $166 billion in investments in semiconductors and electronics, one year after the US Chips Act became effective. These new investments are expected to drive substantial demand for Atlas Copco's vacuum products, contributing significantly to their future growth.

{kind=link}

Industrial Automation: Atlas Copco’s products are utilized in both automated and manual assembly solutions in the automotive industry, including vision systems for robot guidance and quality controls. The rising demand for industrial automation presents significant growth opportunities for their Industrial Technique segment. This segment specializes in selling machine vision systems, tightening tools, self-pierce riveting tools, and flow drill fastening tools.

Financial Analysis and Outlook

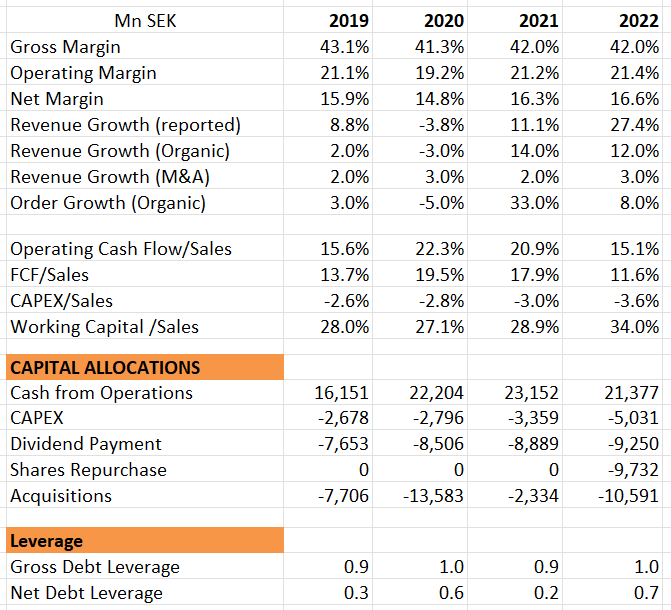

Compared to other industrial companies, Atlas Copco boasts an exceptionally high operating margin of over 20% and a gross margin of 42%. Their free cash flow conversion has exceeded 15% over the past five years, showcasing a remarkable performance attributable to their lean capital business model. Capital expenditure only accounts for approximately 3% of group sales.

{kind=link}

In addition, Atlas Copco maintains a robust balance sheet with a gross debt leverage of around 1x. In terms of capital allocation, they primarily allocate funds towards dividends and acquisitions, occasionally engaging in opportunistic share buybacks. They reported their Q3 FY23 results on October 25th, achieving impressive figures with a 10% organic revenue growth and a remarkable 21% growth in adjusted operating profit.

{kind=link}

The inventory has increased by about SEK 5 million compared to one year ago, although it remained almost flat compared to the previous quarter. The management indicated that they have been actively working on inventory management, recalibrating their stock levels to align with end-market demands. Additionally, they maintain a conservative debt level, with only 0.6x net debt leverage at the end of this quarter. Operating cash flow has shown a significant increase, rising from SEK 5.7 billion one year ago to SEK 6.5 billion this quarter. Overall, I believe this quarter reflects a robust performance, marked by strong operating margin expansion and substantial free cash flow generation.

Looking at the near-term outlook, the company has mentioned that customer activity levels are expected to weaken compared to Q3. This seems logical to me, given the prevalent demand weakness in certain end-markets such as electronics and general industrials. Many companies are currently in the process of destocking their inventories.

In the long-term, Atlas Copco aims for an average revenue growth of 8% through economic cycles. I find this target to be in line with their historical performance and overall strategic trajectory.

Key Risks

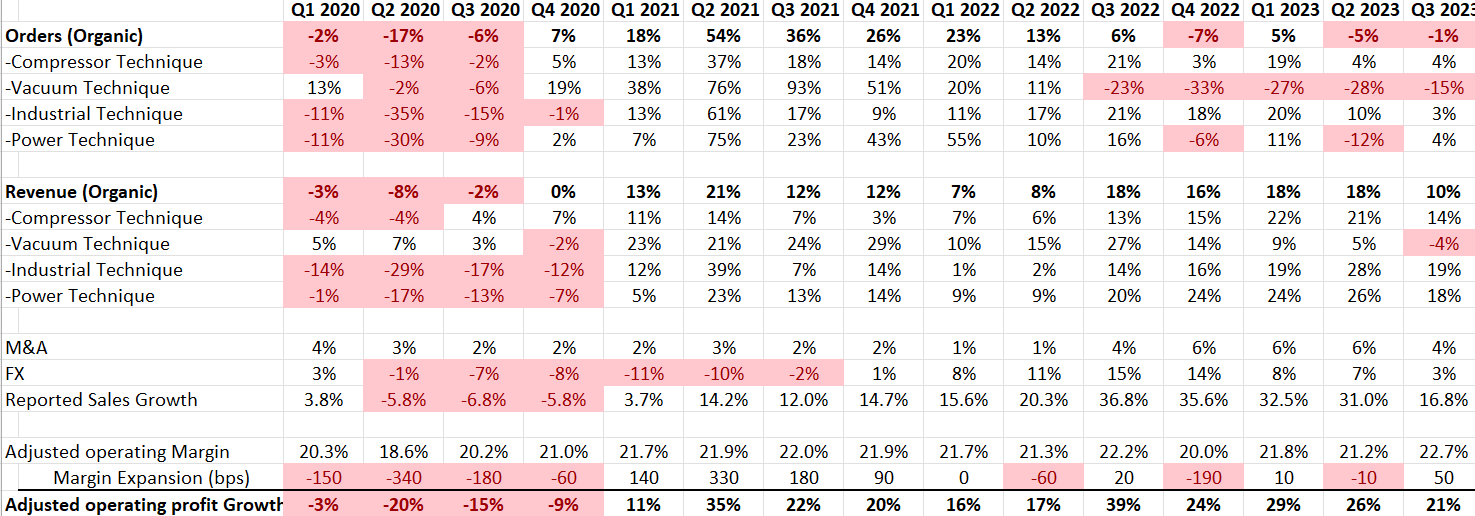

Atlas Copco's order growth turned negative starting from Q4 FY22 , and they reported a -1% organic order growth in Q3 FY23. The primary weakness was observed in their Vacuum Technique business. The management disclosed that they experienced soft demands in the industrial and life science end-markets, although services remained strong. According to their 2022 capital markets day presentation, electronics accounted for 65% of total orders in their Vacuum Technique business, process industry represented 21%, and general manufacturing constituted 12% of total orders. In my view, the overall industrial softness is inevitable given the current high-interest rates. Order growth serves as a leading indicator for their revenue growth, and it's anticipated that they might experience negative revenue growth in the upcoming quarters for their Vacuum Technique business.

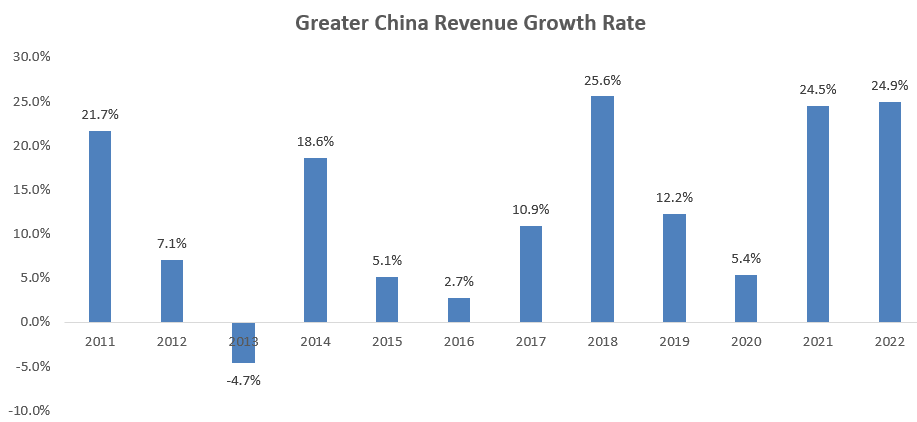

Greater China Exposure: Greater China currently represents more than 22% of the group's revenue, making it a significant market for Atlas Copco. Remarkably, the company's exposure to China is even larger than that of the United States. China has served as a substantial growth driver for the company in recent years, with impressive growth rates of 24.9% in FY22 and 24.5% in FY21. However, in Q3 FY23 , the company's management indicated a slowdown in the electric vehicle market in China. I believe this slowdown is indicative of a broader trend, as overall industrial activities in China have slowed down due to declining exports caused by the global high-interest rates. A combination of weak consumer consumption and sluggish exports in China could pose challenges for Atlas Copco's growth in this market.

{kind=link}

Specialty Rental: Atlas Copco offers specialty rental services within the Power Technique segment. The specialty rental business is highly cyclical compared to other business lines, as it is closely tied to overall construction activities. Rental products include mobile compressors, generators, light towers, and more. Consequently, their revenue growth rate can fluctuate significantly on a quarterly basis.

Valuation

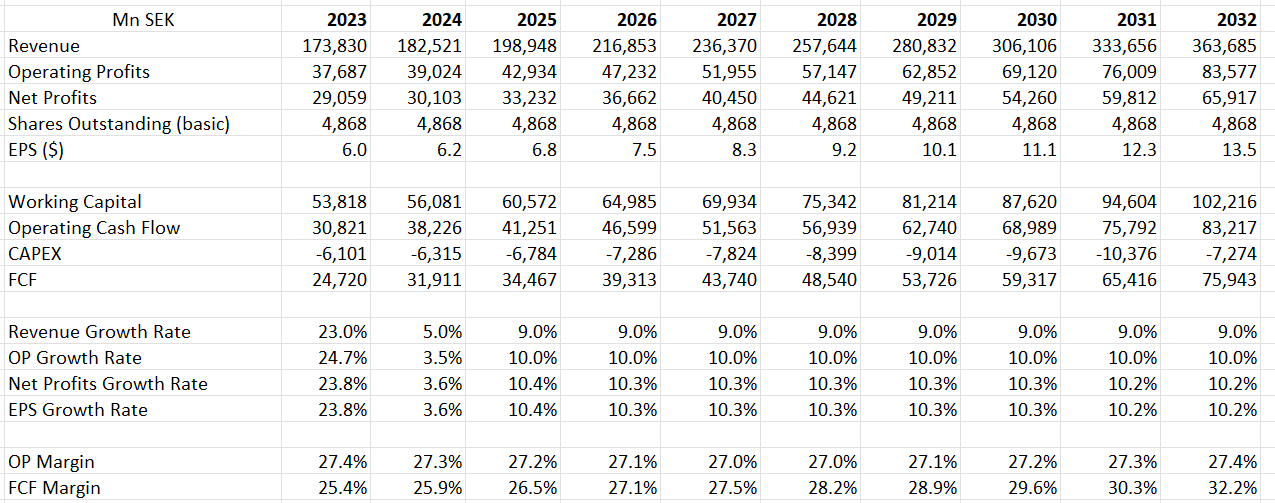

For the normalized growth rate, I have assumed a 6% organic revenue growth, which is the average figure over the past seven years. Atlas Copco is expected to experience a very strong organic revenue growth rate in FY23, driven by robust orders in the preceding periods. I forecast a 13% organic revenue growth in FY23, based on their performance in the first three quarters and accounting for some anticipated weakness in Q4 as hinted by their management. However, in FY24, I am assuming a modest 2% organic revenue growth, considering the negative order growth they have experienced since Q4 FY22.

Additionally, acquisitions are expected to contribute 3% to the revenue growth in my model. This assumption is based on the historical average of their acquisition-driven growth.

{kind=link}

On the margin side, I have assumed relatively stable margins over the next few years as I consider their current margins to be high compared to other industrial companies. I believe my margin assumptions are conservative. The model employs a 10% discount rate, a 4% terminal growth rate, and a 22% tax rate. After discounting all the free cash flows, the total enterprise value in my model is estimated to be SEK 772 billion. Consequently, the fair value of their stock price is calculated to be SEK 155 per share.

Verdicts

I like Atlas Copco’s decentralized organization, growing both organically and tuck-in acquisitions. Their products are well positioned in energy efficiency and industrial automation. I assign a “Buy” rating with a target price of SEK 155.

For further details see:

Atlas Copco: Decentralized Industrial Player With Structural Growth Tailwinds