ATLKY - Atlas Copco: Look At This Rarely-Cheap A-Class Capital Allocator

2023-07-12 22:09:33 ET

Summary

- The article provides an in-depth analysis of Atlas Copco, a leading manufacturer of industrial tools and equipment, highlighting its strong profit margins and cost control.

- Atlas Copco's resilience is attributed to its asset-light operations, profitable aftermarket and service-oriented business, and ability to cut down on variable costs during downturns.

- Despite a positive outlook for the company, the article advises a "hold" position due to the company's typically high share price.

Dear readers/followers,

I work and update on a lot of companies in my role as an analyst, and I focus on European and Scandinavian companies above all. However, I haven't really provided a comprehensive analysis of Atlas Copco ( OTCPK:ATLKY ) - at least until now. In this article, I intend to give you the basics and look at what we have going for us if we're to invest in Atlas Copco. Because the company is really quite amazing - but it's also, usually, quite expensive.

Today is no different. That's why I actually go in here with a "HOLD" - but I'll also show you how I go about investing in this company - because I do invest in it, even today.

Let's get going here.

Atlas Copco - Timeless quality, timeless upside, timelessly expensive

Atlas Copco is a great company - and there aren't many businesses where I start out articles with such a statement.

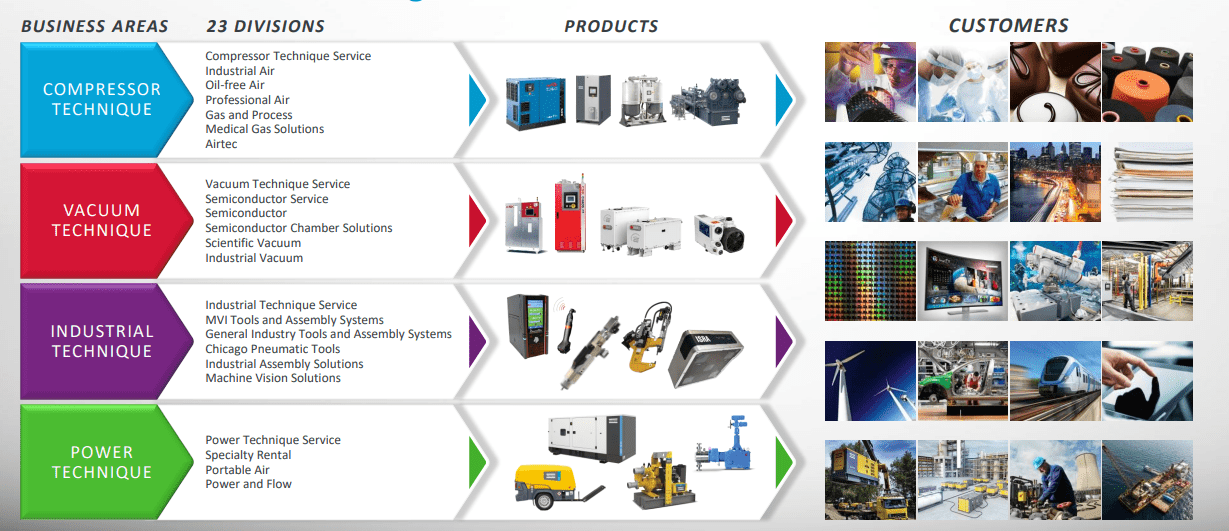

Atlas Copco is a broad play - very broad and diversified, as illustrated by the order specifics we see here.

{kind=link}

Atlas Copco IR (Atlas Copco IR)

It has over 150 years of corporate history, with main offices in Stockholm, Sweden, and generates revenues well in excess of 100B SEK on an annual basis. The company is categorized as a manufacturer of industrial tools and equipment.

Specifically, the company's niches involve air compressors (where it leads the market), construction tools, assembly systems, and others. Specifically, the company works in the areas of:

- Compressor Technology

- Vacuum Technology

- Power Technology

- Industrial Technology

Products include things like industrial compressors, gas/oil treatment systems, air management systems, and compressors/expanders. Vacuum systems, exhaust management, valves, power tools, portable compressors, pumps, paving equipment, construction equipment, demolition tools, construction tools and other sub-areas. The company's customers and end-market users, as you can see above, come from virtually every segment.

Atlas Copco is a market leader in Industrial products. What I mean by this is that it's in the top 85th percentile in all profit margin comparisons, and above the 94th percentile in several. The company manages over 42% gross margins on its revenues, a 21.5% operating margin, and a 16%+ net margin. Return metrics showcase 32.3% on RoE, and 23.27% on ROIC. Simply put, Atlas Copco knows what it is doing, knows how to allocate capital, and knows how to stay profitable in virtually every environment you can think of.

The company manages sub-59% COGS and a sub-21% OpEx.

{kind=link}

Atlas Copco revenue/net (GuruFocus)

For those of you familiar with industrial companies, those sorts of margins and that sort of cost control doesn't just happen. It takes meticulous focus and streamlining to achieve, as well as the obvious scale on the market.

The company manages a very focused and scalable organization with products that, for many parts, are recession resistant. Some are not - but many are.

{kind=link}

Atlas Copco IR (Atlas Copco IR)

The company's operations have resilience based on the degree of asset-lightness we see, as well as a profitable aftermarket and service-oriented business area that takes some of the load during a downturn. In a deteriorating business climate, the company can cut down on variable costs and reduce WC in order to reverse this when the climate improves. Atlas Copco has done this several times in the past, and will do so again going forward.

The company is also investing heavily in R&D going forward. Over 4% of total revenues now go to Atlas Copco R&D in the business, driving organic growth, and profitability and maintaining the company's leading market position.

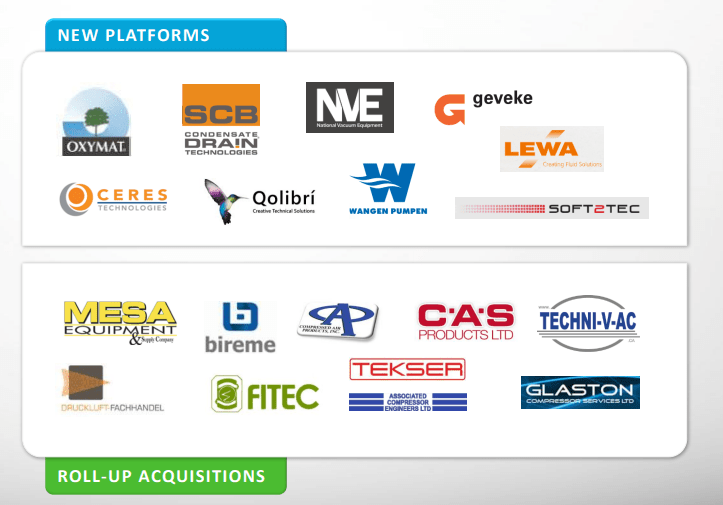

The company is also fairly M&A-heavy and continues to absorb smaller businesses - with 20 M&A's finished in 2022 alone. The company focuses on industry-to-industry M&A's with a geographically spread customer base that has leadership in niche markets and an already-strong base of customers and partners.

{kind=link}

Atlas Copco IR (Atlas Copco IR)

During this sort of business environment, the focus goes back to the service segment, with steady growth in earnings and revenues for the segment. The company has mostly failed, as of this point, to make it a significantly bigger share of revenues - but 35-36% is impressive, nonetheless.

1Q23 is the last set of results we have. And despite an overall superb 2022, the company's positives continue into 2023. The company saw several significant, strong ordered, strong development of its project-based business, and carbon-switching technologies ((ESG)) are still resilient, leading to significant revenue growth in gas/process compressors, power equipment, and vision solution.

Vacuum solutions were down - expected due to the segment correlation to the semi industry, which for the time being isn't that great. But growth for the service business was visible in all business areas for Atlas Copco, and this is of course a positive. We saw a 5% organic order growth, 18% in revenues, an operating margin that went down only 60 bps, and a profit that was up more than a billion SEK. operating cash flow was at more than 2x the YoY period, and ROCE was at 29%, up 2% from YoY. Remember, ROCE is essentially a measure of how much profit in terms of dollars (or currency) the company is generating per dollar (or unit of currency) employed. It's similar to ROIC, but in ROCE we subtract current liabilities from assets, resulting in shareholder equity +long-term debt. I like ROCE for the measuring of allocating capital and profitability. ROCE is a good measurement for capital-intensive business, which Atlas Copco happens to be.

The company also grew the dividend to 2.3 SEK/share. Atlas Copco will never be a high-yielder, I believe. Still, this does not make it fundamentally unattractive. The company makes up for this lack of yield, owing to its 1.54% current yield, with an A+ credit rating and a historical recession resistance that few companies can measure up to. It's one of the few businesses in industrials that has managed a 20-year average EPS growth rate of over 12.5%. You won't find that in many industrials in the sector. While some may argue that downturns have existed, I would say the sole downturn of actual note was back in -09 when we saw a near-40% EPS decline on an adjusted basis. Beyond this, Atlas Copco has seen mostly growth with only one single-digit or low-double-digit decline in the past 20 years.

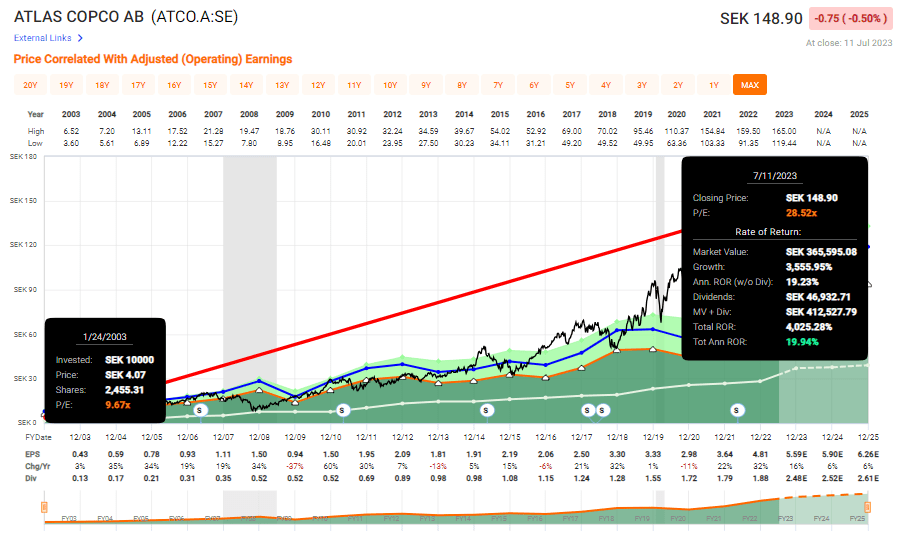

Investors in the company have done well for themselves - though this is actually an understatement, given the near 20% annualized RoR or the 4,000%+ ROR in 20 years.

{kind=link}

Atlas Copco 20-year RoR (F.A.S.T Graphs)

A lot to like here - and a lot of quality. Furthermore, you can clearly see the valuation tendencies inherent to the business. There is an up and down here where you determine "BUY" and "Trim" targets.

The company gives a very somber and simple guidance for the near term.

{kind=link}

Atlas Copco IR (Atlas Copco IR)

And this also goes hand-in-hand with my own expectations given the company's specific and current industrial/geopolitical macro situation. I expect the company to continue to outperform internally and externally, weighed down by a less-than-favorable FX situation as well as overall macro.

With that said, let me show you why Atlas Copco unfortunately isn't investable at this juncture.

Atlas Copco - Unfortunately not in a position to give you good enough conservative RoR

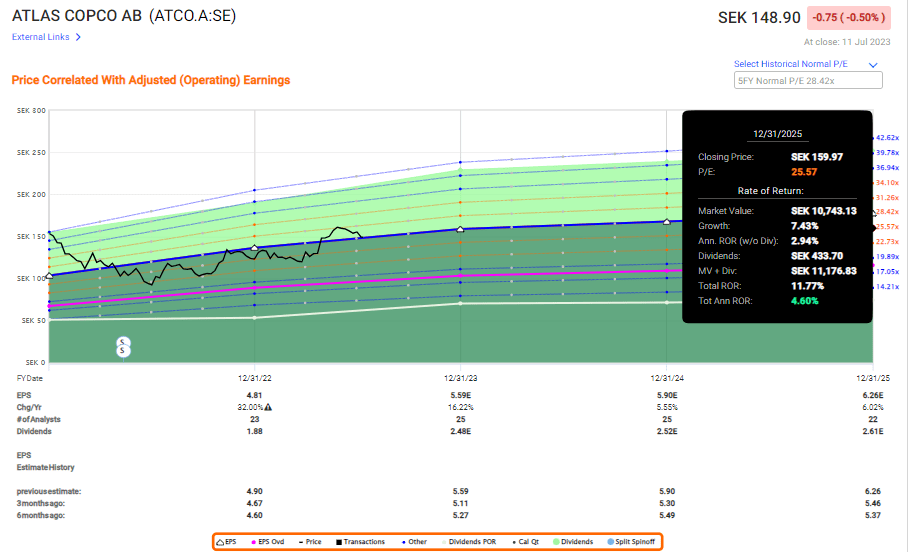

The one drawback to this company is that you should buy it when it's cheap, and the company has not been cheap for a long time now. The last time it was even close to significantly investable was during COVID-19. Atlas Copco trades at a conservative premium of 24x P/E, which I consider to be valid given both growth rates and overall company safety. At a 25x P/E, we have a potential RoR of 4.6% on an annualized basis given the current estimates, which by the way include nearly double-digit annual EPS growth on a forward basis. This is not good enough.

{kind=link}

Atlas Copco Upside (F.A.S.T graphs)

S&P Global analysts following the company give us the following estimates and targets. 22 analysts follow the company, 17 of which have either "HOLD", "Underperform" or "SELL" targets, going from 120 SEK on the low side up to 192 SEK on the high side, with the current share price of about 149 SEK. The average here is 154 SEK, which implies an S&P Global average upside of 3.4% - but only from 5 analysts giving it a "BUY". I would call that 3.4% essentially a rounding error, and extremely optimistic given the environment we're in, and are likely to continue to be in.

That doesn't mean that there aren't ways to invest in or "play" with Atlas Copco as a business and to make money of it.

My way? Cash-secured Puts. I have access to native Swedish options, which means that in the latest slight downturn, I was able to secure 90-day secured puts at a share price target of 110 SEK. Those are getting close to expiring here, and they'll obviously expire out of the money. Since we're in a downturn for the company again with slight drops, I'm getting ready to write more of these puts. When it comes to a company as conservative and as safe as this one, I've found the way that I want to approach is waiting for a down day of 2-5%, and during that day find 30-90 days put option that annualized between 8-15%. With that company, and many other companies like it, that has been possible - and this is how I approach it.

When it comes to what I would pay for the common share, I would say the price where I would become interested in investing in the common would be around 115 SEK/share. This represents a conservative 23-25x P/E average, depending on what current forecast ranges you look at, and I wouldn't want to go much higher than that.

Atlas Copco has the sort of consistent profitability and revenue growth which makes it a great potential investment. But it is also priced in accordance with this assumption - and all we do is look at historical data to see that it's certainly not always priced at such premiums. In terms of negatives and risks, I find very few. I noted that the company's asset growth is actually currently faster than its rev growth on a per-share basis, which tendentially can be seen as a negative. Also, it's issuing new debt (but has less than 30% LT debt/cap). It's operating margin is declining - but it's declining from record levels.

So any risk you can throw at this company can usually be met with a counter-argument. I find that unless we see a fundamental deterioration in any one of the company's core business segments, I do not expect any sort of massive downturn or risk for the business.

Here is my thesis based on this.

Thesis

- Atlas Copco is an internationally-leading company in several key fields related to industrial tools, machines, vacuum technology, and other attractive fields. The company is fundamentally sound at an A+ credit rating, has a 1.4%+ yield, and has delivered 4000%+ RoR over the past 20 years. It's a beyond-solid company.

- However, investors should beware of the overvaluation in such companies, as the company currently trades at premiums of over 24, and is being forecasted to premiums of 28x P/E. I would say the company deserves 24x P/E, but I want a double-digit upside based on this. I am not getting that at this valuation.

- Because of this, I give you my introductory price target of 115 SEK/share for the native ticker and tell you that I am investing in Atlas Copco mostly through the use of attractively-handled cash-secured PUTs with annualized RoRs of over 8%.

- Atlas Copco is a "HOLD" here.

Remember, I'm all about:

-

Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria:

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company fulfills all of my quality-criteria but none of my valuation criteria here. It's a "HOLD".

For further details see:

Atlas Copco: Look At This Rarely-Cheap A-Class Capital Allocator