ATLPF - Atlas Copco: Outperforming But Overvalued

2023-07-12 14:12:19 ET

Summary

- Atlas Copco is a Swedish industrial company founded in 1873 by Andre O. Wallenberg.

- Atlas Copco has a wide economic moat based on switching costs and the company is operating in a niche.

- Right now, the stock seems to be overvalued and not a great investment.

So far, I covered only one company from Sweden - the bank Svenska Handelsbanken ( SVNLF ). But inspired by the podcast "Business Breakdowns" which provided a list of high-quality businesses I started covering new businesses that might have a wide economic moat and are fitting the criteria to be great long-term investments.

And I was quite surprised that I was not familiar with the biggest listed company in Sweden by market capitalization - Atlas Copco AB ( ATLKY ). The company is also among the ten biggest listed companies in Sweden by revenue, earnings, and employees. Without doubt, Atlas Copco is a major business in Sweden that has been flying at least under my radar in the last few years.

In the following article, I will try to offset that "mistake" and analyze Atlas Copco and as always when covering a company for the first time, we start by describing the business.

Business Description

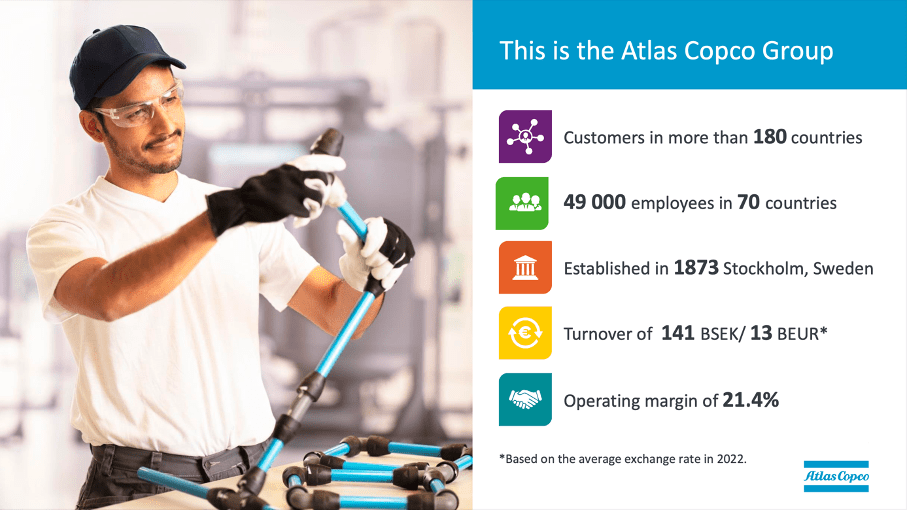

Atlas Copco was founded in 1873 by Eduard Fränckel alongside with Andre O. Wallenberg. In the first few years, Atlas dealt with the manufacturing materials needed for constructing and operating railways. In the following decades, the business diversified and today the company is operating in more than 180 countries and is employing about 50,000 people.

Atlas Copco Group Facts and Figures

{kind=link}

The company which is headquartered in Stockholm, Sweden is a global, industrial company manufacturing industrial tools and equipment, air compressors as well as construction and assembly systems for industries like the automotive sector or the semiconductor industry. The company is a world-leading provider of sustainable productivity solutions and is developing its products focused on productivity, energy efficiency, safety, and ergonomics. All in all, Atlas Copco is what Peter Lynch would describe as the perfect boring business, which is often a great investment.

Atlas Copco Group Facts and Figures

{kind=link}

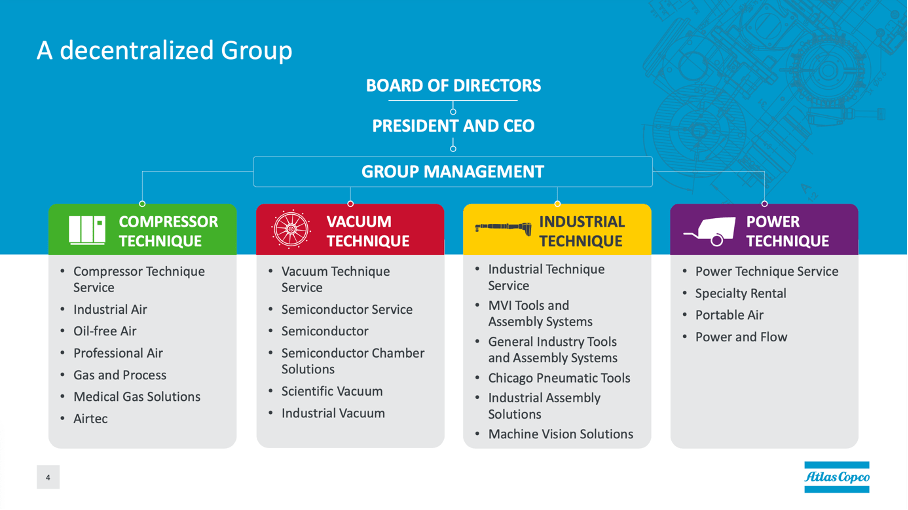

Since 2017, the company is operating in four different business segments and all four are focused on designing, manufacturing, and marketing a large range of products:

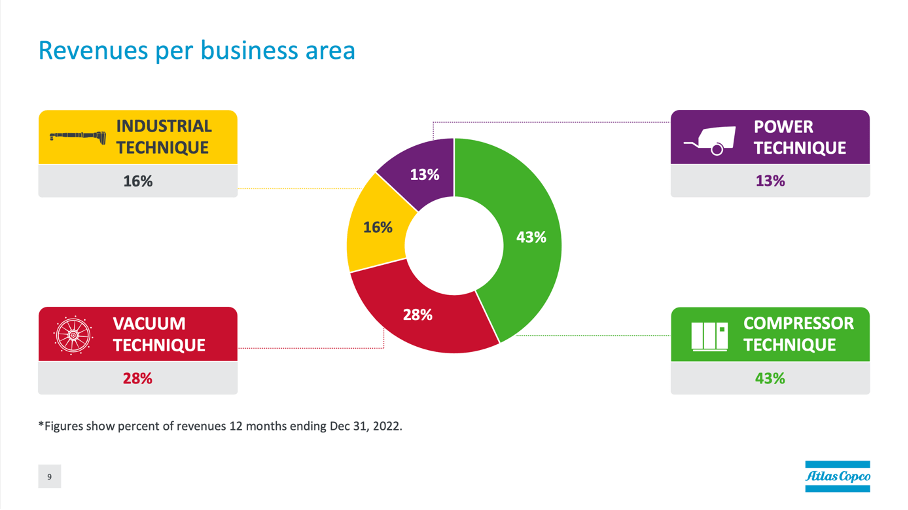

- Compressor Technology : This segment provides compressed air solutions such as air management systems, air and gas treatment systems, gas and process expanders or compressors and generated SEK 61.1 billion in revenue in fiscal 2022 (responsible for 43% of total revenue). Its operating margin was 23.6% in 2022.

- Vacuum Technology : This segment deals with valves, exhaust management systems, vacuum products and related equipment and generated SEK 38.9 billion in revenue in fiscal 2022 (responsible for 28% of the company's total revenue). Its operating margin was 21.6% in 2022.

- Power Technology : This segment supplies power, air, and flow solutions through various products that include generators, light towers, pumps or mobile compressors and it generated SEK 19.1 billion in revenue in fiscal 2022 (responsible for 13% of total revenue). Its operating margin was 18.5% in 2022.

- Industrial Technology : This segment offers quality assurance products, assembly solutions, industrial power systems and tools, software and services and generated SEK 23.0 billion in revenue in fiscal 2022 (responsible for 16% of total revenue). Its operating margin was 20.0% in 2022.

Atlas Copco Group Facts and Figures

{kind=link}

When looking at the group results for fiscal 2022, we see strong and impressive growth rates. Revenue increased from SEK 110,912 million in fiscal 2021 to SEK 141,325 million in fiscal 2022 - resulting in 27.4% year-over-year growth. Operating profit increased from SEK 23,559 million in fiscal 2021 to SEK 30,216 million in fiscal 2022 - resulting in 28.3% year-over-year growth. And diluted earnings per share increased 29.6% year-over-year from SEK 3.71 in fiscal 2021 to SEK 4.81 in fiscal 2022.

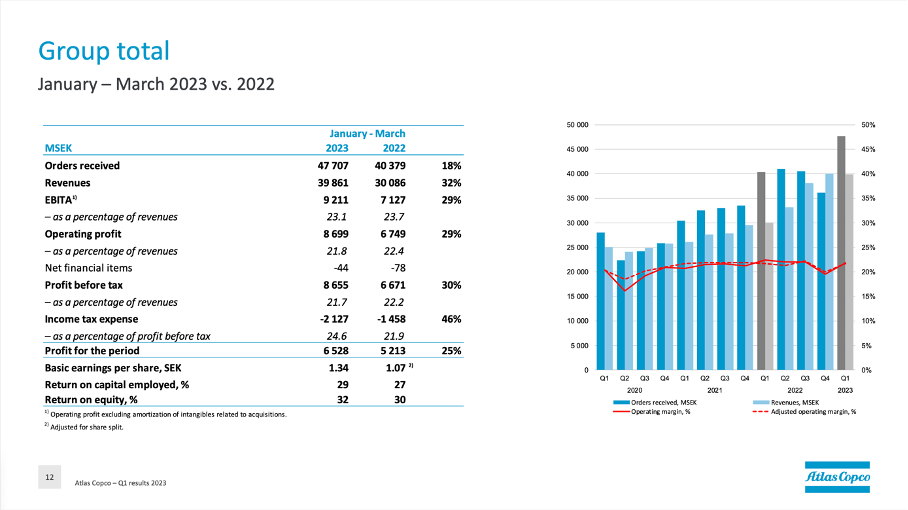

While these were exceptionally high growth rates for Atlas Copco in fiscal 2022, the first quarter results for fiscal 2023 were great once again. Revenue increased 32.5% year-over-year from SEK 30,086 million in Q1/22 to SEK 39,861 million in Q1/23 (with organic growth being 18%). Operating profit increased from SEK 6,749 million in the same quarter last year to SEK 8,699 million this quarter - resulting in 28.9% year-over-year growth. And diluted earnings per share increased 35.5% year-over-year from SEK 1.07 to SEK 1.45.

Atlas Copco Q1/23 Presentation

{kind=link}

Growth

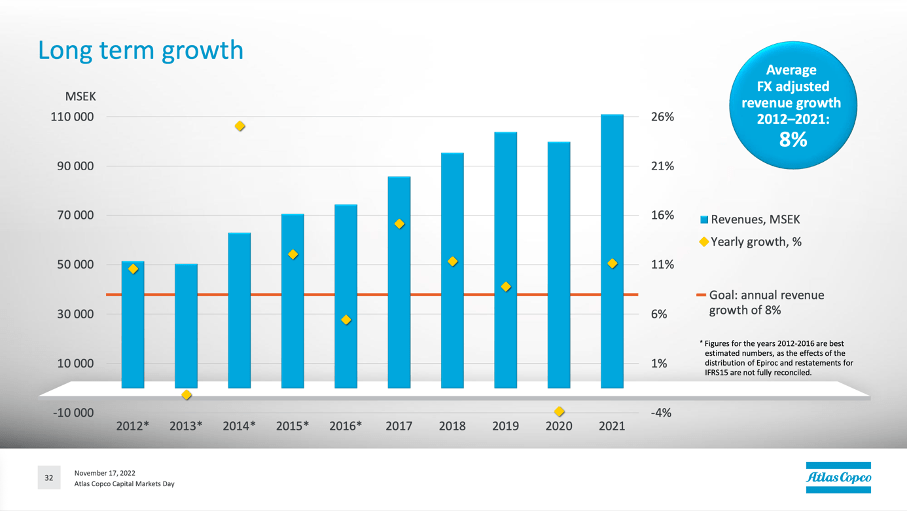

Growth rates in the last few quarters have been exceptionally high - and we should not expect similar growth rates in the years to come. But Atlas Copco has ambitious financial targets of 8% average revenue growth per year over a business cycle (as Atlas Copco has highly fluctuating growth rates).

Atlas Copco Investor Day Presentation

{kind=link}

When looking at the last decade, Atlas Copco could not achieve that target although growth rates were above the 8% threshold in many years. On average, revenue increased with a CAGR of 4.55% in the last ten years. Earnings per share increased with a CAGR of 5.35%. However, when looking at longer timeframes we see earnings per share increasing with a CAGR of 10.10% since 2000 and with a CAGR of 11.23% since 1990.

Atlas Copco Investor Day Presentation

{kind=link}

And we must take into account the possibility that growth rates are slowing down over time and Atlas Copco won't be able to achieve these high growth rates anymore.

For the next few quarters, we still can be optimistic as Atlas Copco's order intake is showing little signs of growth slowing down. Order intake was higher than expected and reached a record level, which was primarily a result of several significant orders and strong project-related business. In Q1/23, received orders were SEK 47,707 million - compared to SEK 40,379 million in the same quarter last year. In the last few quarters, the order received was clearly higher than generated revenue and we can therefore assume higher revenue in the coming quarters. But when order volume is collapsing, the trend can reverse quickly.

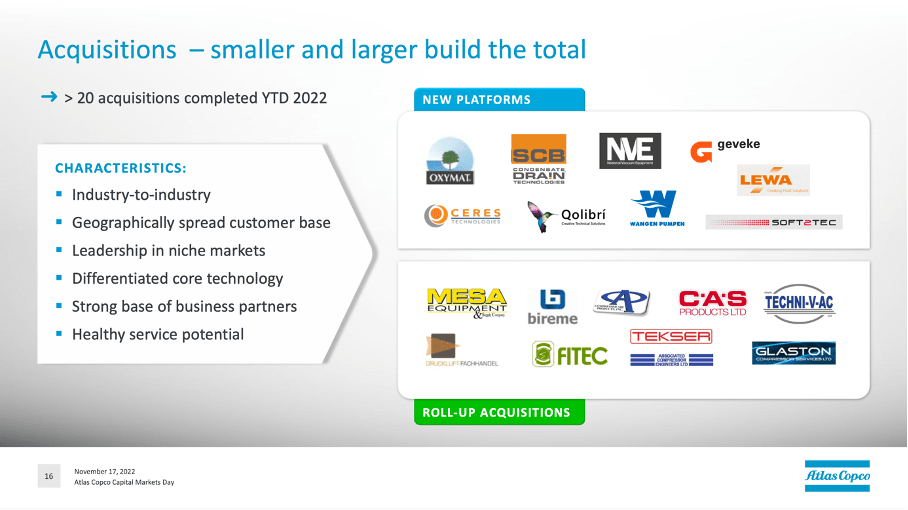

Growth by acquisitions

Atlas Copco is also growing by acquisitions and made about 20 acquisitions in 2022. And I usually like the strategy of making smaller acquisitions and strategically buying small businesses. Major acquisitions are often done for the wrong reasons (prestige, reputation, significantly increasing the company's top line). But making several small acquisitions is often working out quite well for companies.

Atlas Copco Investor Day Presentation

{kind=link}

And when looking at the company's balance sheet, Atlas Copco is certainly able to make further acquisitions in the years to come. On March 31, 2023, the company had SEK 29,375 million in long-term borrowings as well as SEK 2,975 million in short-term borrowings. When comparing the total debt of SEK 32,350 million to a total equity of SEK 85,968 million we get a debt-equity ratio of 0.38, which is certainly acceptable and no reason for concern.

We can also compare the total debt to the operating income of fiscal 2022, which was SEK 30,216 million. It would take only the operating income of a little more than one year to repay the outstanding debt. This is also underlining that Atlas Copco's balance sheet is no reason for concern. Additionally, Atlas Copco also has SEK 9,882 million in cash and cash equivalents, which could be used to repay about 30% of the company's outstanding debt.

Based on the balance sheet, Atlas Copco can make further acquisitions in the years to come - and especially small acquisitions like Atlas Copco is usually making are certainly possible.

Recession

When talking about growth and potential acquisitions, we should not ignore that Atlas Copco is a cyclical business and with the risk of a recession and bear market being rather high, a closer look at the performance during past recessions seems necessary.

In the past, we saw declining revenue during recessions and especially in 2009 (during the Great Financial Crisis) revenue declined and in the years between 2001 and 2005 Atlas Copco also struggled. And of course, there have been other years when Atlas Copco had to report slightly declining revenue compared to the previous year - for example in 2020, in 2016 or in 2013. When looking at earnings per share, we see declining numbers between 1989 and 1991, between 2001 and 2002 or between 2008 and 2009. Of course, earnings per share also declined in 2020. I think it is safe to say that Atlas Copco is not recession-resilient, but in most cases, the company could recover quickly after a recession. And in the last decades (at least since 1987) the company was profitable in every single year - aside from 2002 when Atlas Copco reported a loss per share of SEK 0.77.

Wide Economic Moat

One of the most important aspects I usually pay attention to is the wide economic moat (and the question if a company has one). For starters, Atlas Copco is mentioning its portfolio of strong brands, which could be the source of an economic moat around a business. But Atlas Copco is mostly operating in business-to-business and I believe brand names also play a large role in B2C. A strong portfolio of brand names is certainly helpful but that is probably not the competitive advantage we are looking for.

Atlas Copco Group Facts and Figures

{kind=link}

Another aspect worth mentioning is the decentralized structure of Atlas Copco. And although CEO Mats Rahmströhm is describing this as the company's competitive edge , it is not the source of an economic moat. Nevertheless, the commitment to decentralization is core for Atlas Copco and most decisions are taken within the divisions and that strategy seems to be working for Atlas Copco.

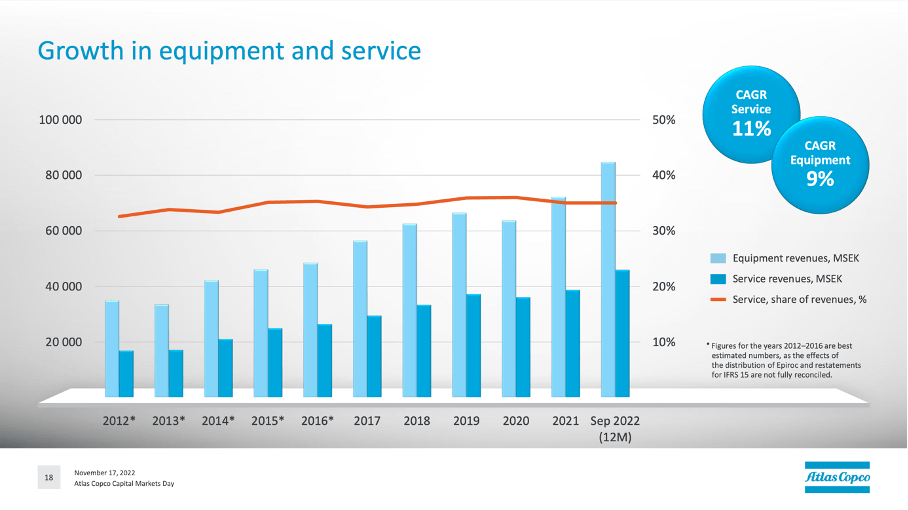

The economic moat is especially stemming from switching costs and cost advantages the company can generate by operating in a niche. And as Atlas Copco is a dominant player in its niche and number 1 in most business segments it is operating in, this is creating a cost advantage for Atlas Copco. Additionally, we are looking at rather high switching costs as customers won't switch to the product of a competitor once they bought a compressor from Atlas Copco for example. And in the following years, Atlas Copco can generate revenue by service sales - additionally to the initial sales of equipment. And Atlas Copco is generating about 35% of its revenue by service sales and it is very difficult (or impossible) for competitors to take away that revenue.

Atlas Copco Investor Day Presentation

{kind=link}

An economic moat of Atlas Copco can be demonstrated by looking at different metrics. First, the stock clearly outperformed major indices - the S&P 500 or Swedish indices - over the long run. In YCharts, we can only display the last 20 years, but the outperformance is already impressive.

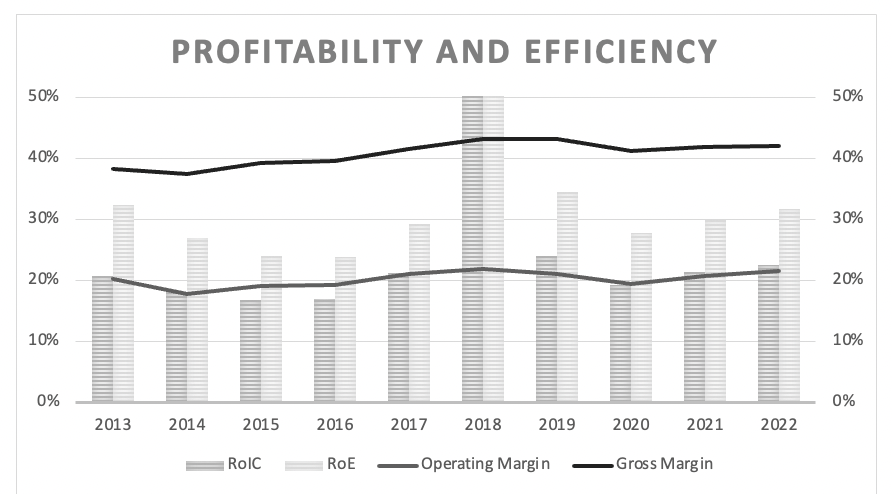

Aside from the stock performance we can also look at the gross margin and operating margin over time and see high levels of stability and consistency, which is another strong hint for an economic moat around a business as well as pricing power.

{kind=link}

Not only can Atlas Copco report stable margins over time but also an extremely high return on invested capital. When looking at the numbers during the last ten years, the return on invested capital was around 20% in most years with 2018 being a positive exception. And only a handful of businesses can achieve such a high return on invested capital over a long timeframe.

And finally, we can look at the shareholder structure and identify Atlas Copco as a "family-run" business. Atlas Copco was founded by Andre Oscar Wallenberg, who also founded the Stockholms Enskilda Bank in 1856, and his family created an empire in the last 150 years. Sometimes the Wallenberg family are also called the Swedish Rockefellers and without doubt a Swedish business dynasty. Today, the Wallenberg empire consists of - among others - the Foundation Asset Management AB, Wallenberg Investments AB and Investor AB (IVSXF).

And Investor AB is the largest shareholder of Atlas Copco and is holding 17.0% of the capital and has about 22.3% of the voting rights. It would be even better if the Wallenberg family had the majority of voting rights as businesses controlled by an individual (or a family) tend to do better and are often great investments in my view, but the Wallenberg family holding about a fourth of voting rights is a good starting point.

Intrinsic Value Calculation

A final step in every analysis is to determine if a great business - and Atlas Copco is a great business - is also a great investment. And a great investment is not only characterized by a great business model, but also by a reasonable price one must pay for the business.

When looking at the price-earnings ratio of 28 right now, Atlas Copco does not seem cheap right now. Not only is a P/E ratio close to 30 rather high on an absolute basis (and can only be justified by high growth rates), but the stock is also trading above its 10-year average of 24.18. Aside from the P/E ratio, we can also look at the price-free-cash-flow ratio (which is in most cases the better metric anyway). At the time of writing, Atlas Copco is trading for 36.6 times free cash flow and clearly above the 10-year average of 24.89. The P/E ratio as well as the P/FCF ratio paint the picture of a rather expensive stock that is not a good investment.

And this assessment can be backed up by using a discount cash flow calculation to determine an intrinsic value. As always, we calculate with a discount rate of 10% and use 4,868 million outstanding shares. For 2023, we assume the free cash flow to decline 50% compared to FCF in fiscal 2022 (which was SEK 17,717 million) to account for the negative impact of a recession. And as Atlas Copco recovered rather quickly after recessions, we assume a similar free cash flow in 2024 as in 2022. For the following years till the end of the next decade, we assume 8% growth (similar to the company's long-term targets) followed by 6% growth till perpetuity. When calculating with these assumptions we get an intrinsic value of SEK 95.66 for Atlas Copco.

In a second calculation, we can be more optimistic and assume a similar free cash flow in 2024 as in fiscal 2021 (which was SEK 21,182 million). With all other assumptions being the same, we get an intrinsic value of SEK 114.05 . But even when calculating with optimistic assumptions, the stock seems to be overvalued and Atlas Copco is trading clearly above its intrinsic value.

Of course, we could be even more optimistic as Atlas Copco is expecting 8% revenue growth in its long-term targets and assuming improving margins over time, earnings per share growth could be even higher. However, the reported growth rates in the last decade do not support such optimistic assumptions.

Conclusion

Atlas Copco is not only the largest company in Sweden by market capitalization, but it is also a high-quality business with a wide economic moat and a company that outperformed over several decades. However, I don't want to buy an industrial company right before a potential recession and Atlas Copco is also trading for a premium - increasing the risk of a steep sell-off in the coming quarters even more.

For those already invested in Atlas Copco, the stock remains a "Hold" and I don't think shorting a high-quality business is a good idea, but I also don't think buying Atlas Copco right now is a smart move as we might be getting better prices in the coming quarters and years. During the recession in the early 1990s or the Great Financial Crisis, the stock declined more than 60% and a similar scenario is possible this time.

For further details see:

Atlas Copco: Outperforming, But Overvalued