PXJ - Atlas Energy Solutions: Massive Growth For Permian Basin Sand Leader

2023-09-21 14:32:47 ET

Summary

- Atlas Energy Solutions is the leading producer of fracking proppants in the Permian Basin.

- The company's financials show impressive growth, with net income and total sales increasing in Q2.

- Plans to expand its trucking delivery fleet and increase proppant production support a strong earnings outlook.

- We are bullish on the stock and see shares as undervalued relative to industry peers.

Atlas Energy Solutions Inc. ( AESI ) has quietly emerged as a leading supplier of proppants or "treated sand" for the oil and gas industry in the Permian Basin. This is a critical resource in the hydraulic fracking process used to maintain the fluidity of shale formations.

There's a lot to like about AESI as a pure play on proppant with its active open-pit sand mines recognized as tier-one assets. The related drilling site and delivery services are also an important part of the business. The company launched its IPO earlier this year while a combination of impressive financial trends along with the rebound of energy prices have helped shares rally by more than 40%.

Notably, valuation still appears attractive relative to oilfield services and equipment industry peers. An ongoing plant expansion is set to be a new growth driver going forward. We are bullish on AESI and see room for shares to climb higher.

AESI Financials Recap

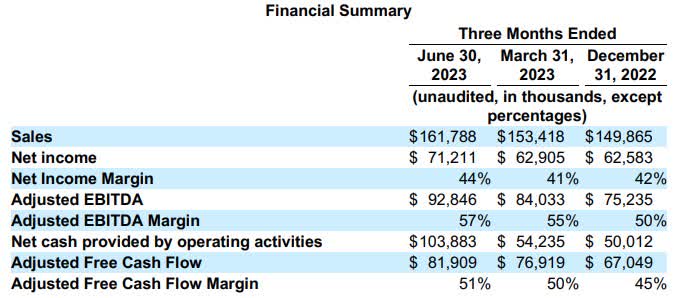

The company reported its Q2 earnings back in late July with $71.2 million in net income, up sequentially from $62.9 million in Q1. Total sales of $162 million, climbing by 5.5% from the previous quarter.

Within this amount, the volume of proppant sold was flat at 2.8 million tons while the average price declined by 5% based on regular market variability and seasonality.

On the other hand, the services side of the group based on the logistical services and proppant delivery was stronger, with a 45% increase to $36.6 million in Q2 benefiting from an increase in the number of trucks deployed and active jobs supplied.

The result here has been a shift higher in the adjusted EBITDA margin, reaching 57%, compared to 50% at the end of 2022, reflecting this higher proportion in the last-mile logistics operation as a value-added operation. The other trend that stands out is the adjusted free cash flow at $82 million in Q2, up from $67 million in Q4 last year.

{kind=link}

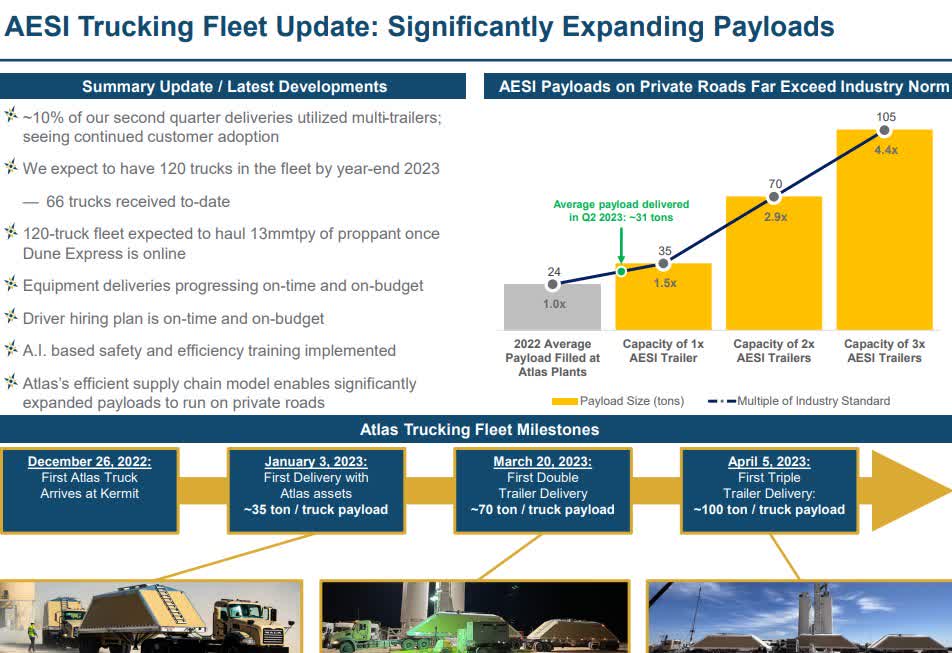

Looking ahead, that trucking fleet expansion coupled with increasing volume production of proppant is a major theme for the company. From 66 trucks delivered as of Q2, the plan is to have 120 trucks by year-end, with the ability to service more drilling customer sites more quickly. There is also a plan to utilize larger payloads and extended multi-trailers.

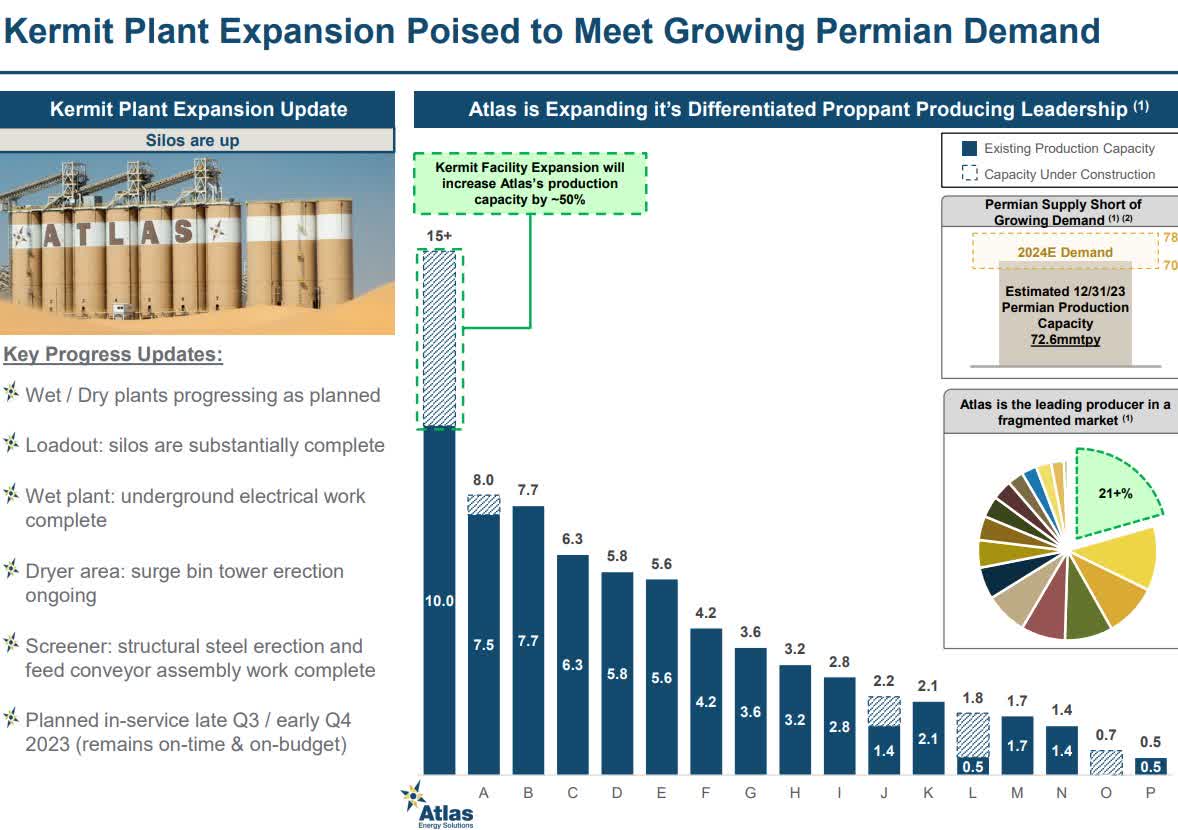

Keep in mind that there is also the construction of a "conveyor system" as a midstream type of infrastructure connecting approximately 36 miles to transport proppant to the Delaware Basin. The project with an investment of $400 million is expected to enter service by Q4 2024.

{kind=link}

In terms of the Kermit Plant ramp-up, the update is that by the end of Q3 and into Q4, the company will have upwards of 50% higher firm-wide capacity, which can meet an ongoing supply shortage in the Permian region by local producers. On this point, Atlas notes that it controls approximately 21% of the market in what remains a fragmented segment.

{kind=link}

On the balance sheet, Atlas ended the quarter with $351 million in cash and equivalents on a pro forma basis against $181 million in total debt. By this measure, the company maintains a net cash position with a leverage ratio under 0.6x.

In our view, the level of liquidity and underlying cash flow trends are well supportive of the company's regular dividend. For Q2, AESI distributed a payout of $0.20 per share, which includes a base amount of $0.15 and a $0.05 variable component. The annualized rate yields approximately 3.5% on a forward basis.

What's Next For AESI

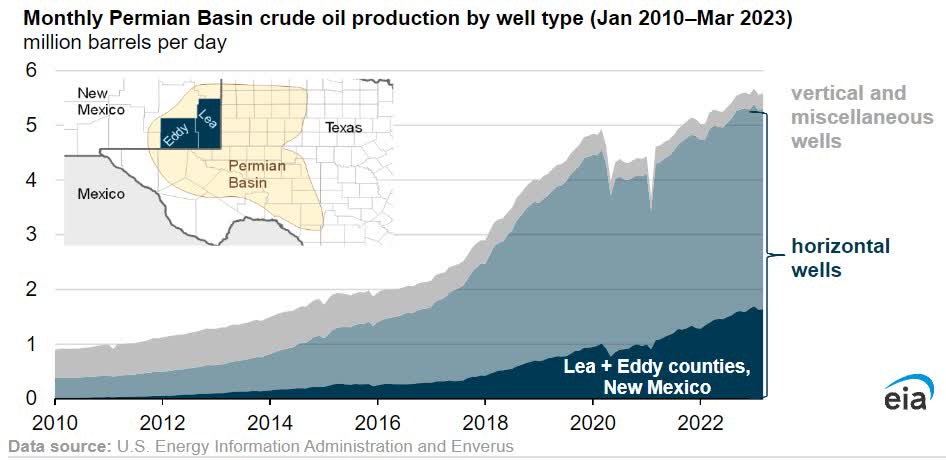

It's clear to us that AESI is presenting strong growth trends, benefiting from the renewed momentum in the energy market. Data from the U.S. Energy Information Administration shows that drilling activity in the Permian Basin continues to climb, particularly in the area into New Mexico covering Lee and Eddy counties where AESI services. The expectation is for continued growth.

{kind=link}

We believe this setup is a positive tailwind for Atlas Energy to continue expanding and meeting the needs of operators in the region. The ongoing rally in the price of oil has added a new boost of momentum to the industry that is poised to pick up exploration and production.

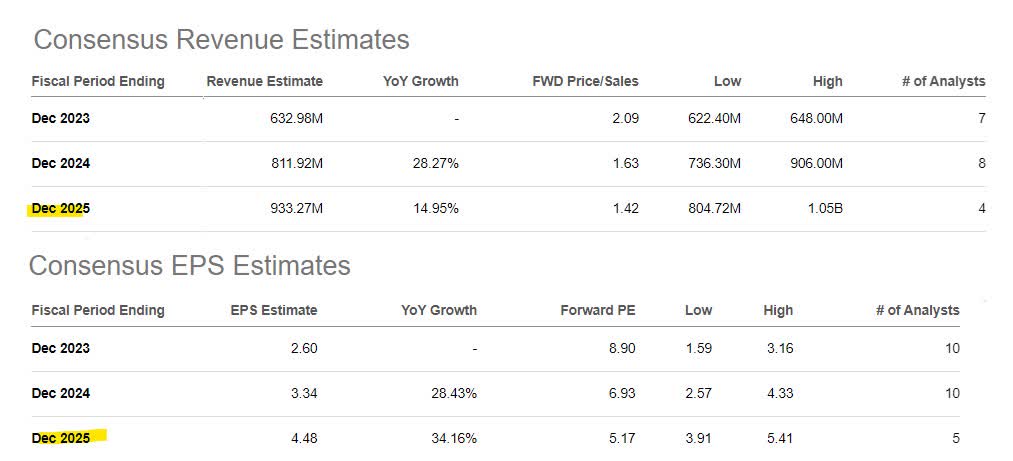

Considering the trucking fleet growth and sand plant expansion projects, the consensus is for AESU revenues to increase by 26% in 2024 with another 15% upside in 2025. The EPS forecast for 2023 at $2.60 has a path to accelerate towards $4.48 over the next two years. In our view, these estimates are well in reach as part of the bullish case for the stock.

{kind=link}

Is AESI Overvalued?

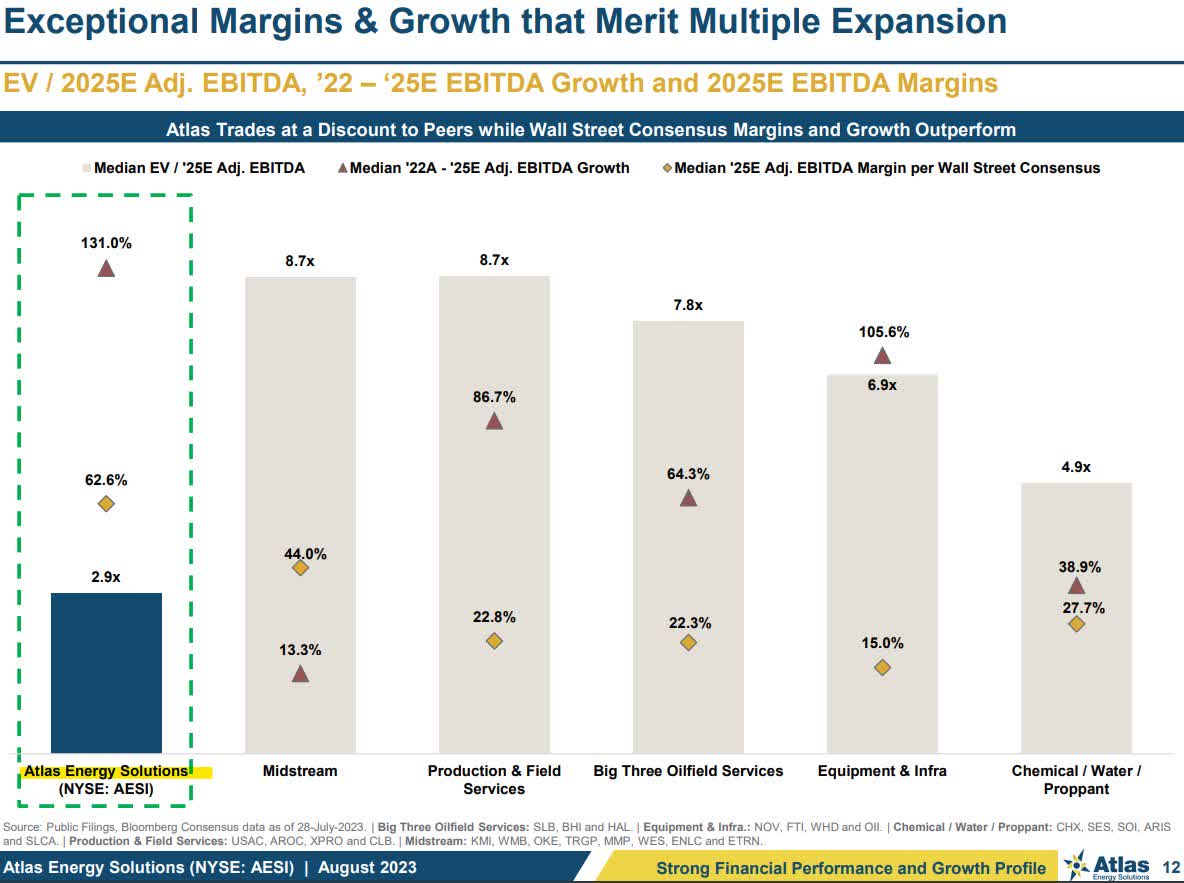

What stands out when looking at Atlas is its exceptionally high margins, which is a reflection of its efficient operational infrastructure and the profitability of the sand business. The EBITDA margin of 54% in Q2 is well above industry peers from major oilfield services providers, midstream players, as well as U.S. Silica Holdings, Inc. ( SLCA ) as a comparable category name.

Management notes that this combination of exceptional margins and the strong growth outlook presents an apparent undervaluation, considering an EV to EBITDA multiple of 2.9x using published 2025 consensus EBITDA estimates incorporating the strong growth outlook.

For context, the "Big Three" oilfield services companies which include SLB ( SLB ), Baker Hughes Co. ( BKR ), and Halliburton Co. ( HAL ) trade at an average multiple of 7.5x for this metric. Keep in mind that shares have rallied about 20% since this graphic was published in late July, meaning the spread has narrowed modestly.

Still, we believe there is room for valuation to continue climbing considering the strong operating and financial trends. On a trailing twelve-month basis, AESI is priced at an EV to EBITDA multiple of around 6x, which remains at a large discount to the same group.

Considering a consensus 2023 EPS at $2.60, shares are also trading at a forward P/E multiple of 9x or 7x into the 2024 estimate. Overall, we believe the stock is still undervalued.

{kind=link}

AESI Stock Price Forecast

We rate AESI as a buy with a price target for the year ahead at $27.50 over the next year, representing an 11x multiple on the current year consensus EPS. In our opinion, the growth trends and segment leadership justify a higher premium. As a recent IPO, our take is that the market has still not fully recognized Atlas Energy Solutions' fundamental quality and long-term earnings potential.

Naturally, the main risk here is the exposure to shifting macro conditions and potential earning market weakness. Sharply lower oil and gas prices would limit drilling activity in the Permian Basin and pressure demand for related proppant services.

Over the next few quarters, we'll want to see margins remain elevated while tracking cash flow trends. Monitoring points include updates on the Kermit plant construction as well as the Dune Express Highway conveyor.

For further details see:

Atlas Energy Solutions: Massive Growth For Permian Basin Sand Leader