MNDY - Atlassian: 2 Problems

Summary

- Atlassian's stock is likely to pop if interest rates only increase by 50 basis points.

- Atlassian's growth rates are already slowing down. And I suspect that its CAGR will slow down further in 2023.

- A discussion of Atlassian's profit margins looking ahead to 2023.

Investment Thesis

Atlassian ( TEAM ) is a team collaboration platform used by software developers, HR teams, and finance teams. The business is in a transition period, as customers migrate away from on-premise to its cloud-based Jira platform.

And while its customers went all in on their digital journey in 2020-2021, there was a massive demand for Atlassian and other collaboration platforms.

But as we now move into 2023, Atlassian has two material headwinds that will plague investors. Price anchoring and how it operates in a higher rate environment.

And with this in mind, that's why I struggle to get bullish on this stock.

Atlassian's Two Problems

I think Atlassian shareholders are likely to exhibit price anchoring to where the stock was this time last year. And with the stock down more than 50% in twelve months, investors are likely hoping to get involved in the name and buy the dip.

After all, who wouldn't want to buy the dip at the bottom of the tech bear market? Haven't we all heard the stories of how much money investors made by buying cheap stocks at the bottom of 2009?

However, this is the first problem. It makes no difference what the share price was. All that matters is what the future holds. More specifically, how the next 12 months are going to shape up. And on this front, I don't believe that Atlassian has positive prospects.

And this takes me to my second point. Over the next 24 hours, we are likely going to hear the Fed raise interest rates by 50 basis points. And this should cause beaten-down growth stocks to jump higher.

And not just higher, but significantly outperforming slower-moving, more mature, and stable companies. And here's the reason why this is going to happen.

Thinking Forward to 2023

As the Fed slows down its pace of hikes, this will be very welcome news to companies that are highly sensitive to interest rates. Companies where their future prospects are heavily discounted many years into the future.

So, that's the level one part of this thesis. The second level problem is that even if the pace of rate hikes slows down, we are still very likely to see rates around +4% for a prolonged period of time.

And in that event, yield-hungry investors will be moving elsewhere for their return.

To be clear, that's not to say that Atlassian's shareholders have anything in common with yield-hungry investors. But it is important to the overall flow of capital, away from ''high-growth'' tech names, to more stable and strong free cash flow generating companies. I'll soon explain why I wrote ''high-growth'' in quotes.

But before that, I want to reemphasize, that in 2023, there's going to be an alternative for investors. Investors will no longer have to crowd around fast-moving SaaS stocks. Other options are available.

And finally, I'll discuss the third consideration. What's the likely impact on Atlassian's profit margins when the macro environment slows down, while at the same time, as has been widely reported, service salaries inflation remains notoriously high?

No Longer a ''High-Growth'' Company

TEAM author's work

Atlassian is growing at less than 30%. It can no longer be classed as a high-growth company. And if it's not viewed as a high-growth stock, it's not likely to be rewarded with a high-growth premium valuation.

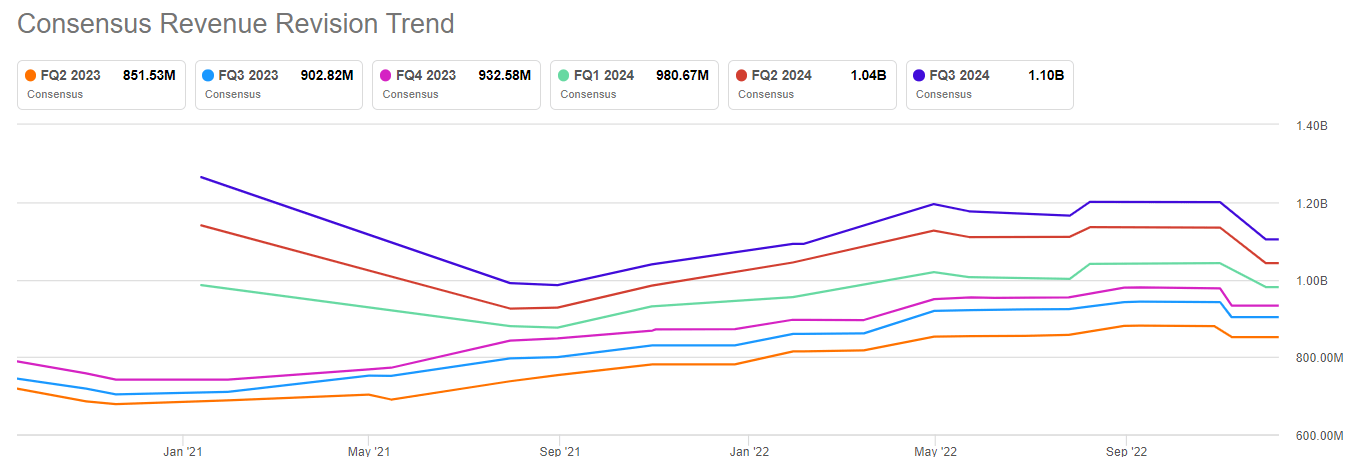

That being said, despite everything that we have so far discussed, it appears that analysts refuse to downwards revise Atlassian's revenue estimates.

TEAM consensus revenue estimates

{kind=link}

Analysts are holding the line and no analyst is willing to take career risk, by lowering estimates at this point. There's still a lot of uncertainty in the air, and unless there's concrete evidence that Atlassian is slowing down, i.e. Atlassian's guidance coming down, investors will continue to hold the line.

Put another way, analysts are reactionary. It's their incentive to act after the fact.

Next, let's discuss Atlassian's valuation for 2023.

TEAM Stock Valuation -- +100x Forward non-GAAP EPS

I know that it's bad taste to think about tech companies on bottom-line profitability. But having been through a bear market I've come to the realization that profits do matter.

Thus, I hope you'll forgive me for highlighting this aspect. Atlassian's shareholder letter guides for ''lower operating margin in FY23''. Consequently, I believe that analysts' expectations for $1.34 for fiscal 2023 will probably prove correct.

This implies that Attlassian is priced at around 100x non-GAAP EPS.

There's simply no way that a company priced at more than 100x forward EPS, as its topline is expected to slow down below 30% CAGR, offers investors much in the way of a compelling risk-reward.

The Bottom Line

For a long time, investors becoming enchanted and compelled towards companies that delivered enhanced productivity.

And even though these stocks have seen their valuations come down substantially, I remain unconvinced of the opinion that because they are down a lot necessarily means that Atlassian and its peers are cheap.

For further details see:

Atlassian: 2 Problems