MNDY - Atlassian: Why I'm Not Chasing This

2023-04-04 09:20:58 ET

Summary

- Atlassian's business model is not resonating strongly with developers, at least for now.

- $1 billion buyback on the table, how to think about this?

- Atlassian's growth rates are a problem, but not the only problem.

Investment Thesis

Atlassian ( TEAM ) is a collaboration and workflow company. Its business model is highly sensitive to the undulations of the business cycle, I'll explain this assertion soon.

Today, it's difficult to imagine that at one point, Atlassian was a $400 stock. The software developer workflow solution company has evidently fallen from grace in the past 18 months.

And yet, despite the valuation cut, I am not compelled to get bullish on this stock. Here's why.

Why Atlassian?

The best way to describe Atlassian is as monday.com ( MNDY ) meets Asana ( ASAN ). Monday.com is a low-code developer software, while Asana is a collaborative tool. Meanwhile, Atlassian is focused on organizing, discussing, and completing shared work.

Its biggest advantage has arguably become its significant weakness. Allow me to elaborate, the business model has been organically grown and adopted by developers.

Developers love Atlassian for project management. Through different Atlassian solutions, developers with different skill levels can "plug-and-play" its highly versatile modules and get up and running with ease.

When there was plenty of free money, SMBs and start-ups could get up to scale with Atlassian rapidly. And everyone was happy. Today, that's not the case.

If you've read my work before, you'll have seen contention that the best way to follow the appeal of a growing business is by following the customer growth rates.

{kind=link}

As you can see above, the latest quarter, Q2 2023, saw customer growth of 12% y/y. While the prior year saw growth of 29% y/y, more than double the growth in customers. Simply put, there's a significant downgrade in the customer adoption figure.

How much of this is due to the macro environment? And how much is due to the highly competitive space that Atlassian's cloud offering is up against?

Indeed, recall, while Atlassian was mostly focused on its on-premises offering, with perpetual licenses, the business was thriving. It could be a coincidence, but there's no doubt that there's been a significant slowdown in customer adoption at Atlassian since Atlassian started to fade its focus toward its on-premise offerings.

Could it be that Atlassian has been too aggressive in attempting to shift its potential developers to its cloud offering, by proactively cutting maintenance and support to its on-premise platform starting next February?

Perhaps, I'm overthinking the reason, and it's not one single reason, but multiple elements coming together?

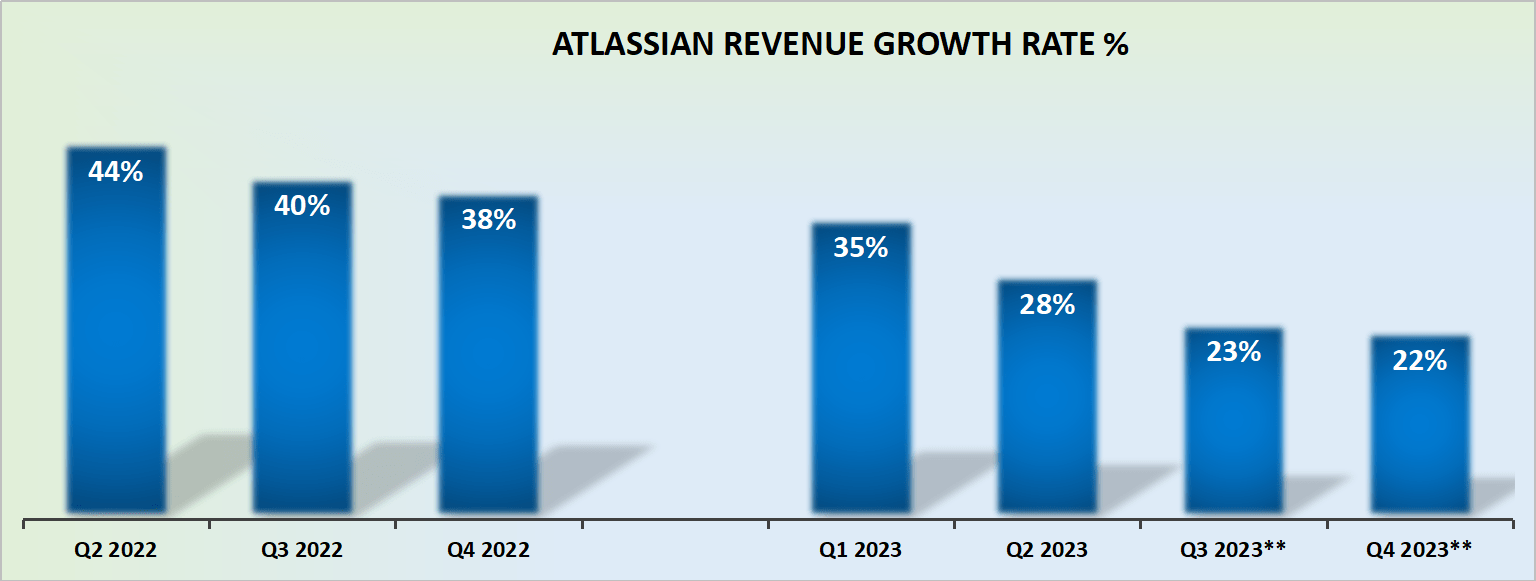

Revenue Growth Rates Are Maturing

{kind=link}

Nonetheless, the fact of the matter is that Atlassian's growth rates today are decidedly sub-30% CAGR.

Any new investor approaching the stock to invest for the first time, without prior endowment biases, is unlikely to believe that Atlassian's prospects are going to return to hyper-growth, meaning +30% CAGR, any time soon.

And if its growth rates were to be decidedly slowing down, investors will start to more actively question at which stage will the business start to become GAAP profitable?

Capital Allocation Decision

Contrary to many investors, I believe that buybacks are not a great use of capital. Allow me to explain. Buybacks make tremendous sense in certain instances. The way Warren Buffett praises buybacks is when a company is dramatically undervalued with stable outlooks, in that case, buybacks make terrific sense.

When a company is buying back significant amounts of stocks simply to stem shareholder dilution that is not a great use of capital. Or put another way, as Mark Leonard declares, buybacks are awesome, for those that want to cash out and exit the long-term trajectory of the business.

A business that isn't yet GAAP profitable, is not self-sustainable. That means that buybacks are a terrible use of investor capital. Management should work to stabilize operations in the first instance, rather than resorting to attempting to stabilize the share price.

The Bottom Line

I recognize that animal spirits have returned to the market of late. And that in the very short term, valuations don't really matter, all that matters is whether or not the Fed is done raising rates, so we can return to the 2020 playbook.

But I've learned from experience, even if the share price in the very short term appears to be showing signs of strength, without hesitation the market can turn, and we can rapidly see who is swimming naked. And just because a stock is down 50% or more from its highs, does not mean it can't continue to drop another 50% in the next 18 months.

For further details see:

Atlassian: Why I'm Not Chasing This