SWX - Atmos Energy: Excellent Company But Forward Total Returns May Disappoint Vs. Peers

2023-09-22 12:42:11 ET

Summary

- Atmos Energy Corporation is a large natural gas utility operating in eight southern states in the U.S.

- The company has a strong financial position and has outperformed the U.S. Utilities Index year-to-date.

- Despite concerns about the future of natural gas, Atmos Energy is expected to handle any upcoming recession and has stable financial performance.

- Atmos Energy has considerably outperformed its peers YTD and has a substantially lower dividend yield so it may underperform going forward on a total return basis.

- The company has one of the strongest balance sheets in the industry and an attractive PEG ratio.

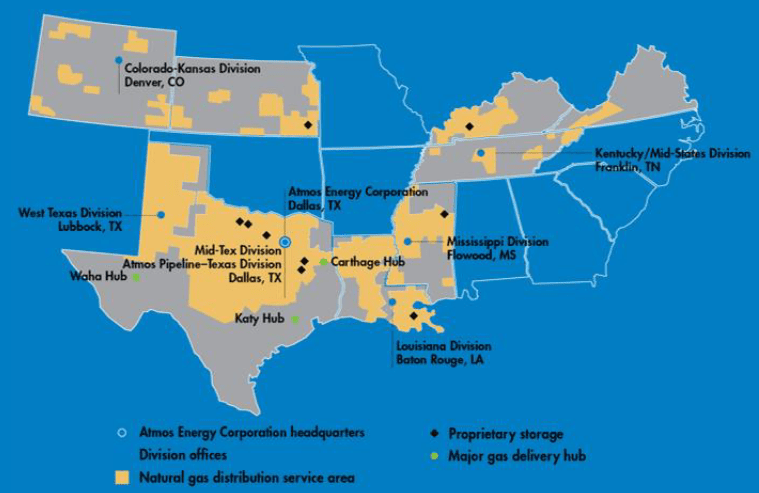

Atmos Energy Corporation ( ATO ) is a large natural gas utility that operates in eight states in the southern part of the United States:

{kind=link}

This makes the company one of the largest utilities in the United States. It is also one of the strongest financially, with an incredibly strong balance sheet and a reasonably attractive valuation. The company’s stock has also been performing reasonably well in the market, as it has substantially outperformed the U.S. Utilities Index ( IDU ) year-to-date. This is surprising because the market in general has not been particularly friendly toward natural gas utilities over the past few years.

As I noted in my previous article on Atmos Energy, there are some participants in the market that believe that the distribution of natural gas will be rendered obsolete by the government’s push towards net zero and electrification so have shunned these companies in favor of electric utilities. It is highly unlikely that natural gas will be phased out during any sort of time frame that most of us would consider reasonable, so the market may be handing us a good opportunity to purchase the company’s stock. Atmos Energy should also be able to handle any recession that may be coming within the next six months, as some economists and analysts are predicting.

Overall, a good case can be made for purchasing Atmos Energy today. Let us investigate further and see if the company could be a good addition to your portfolio right now.

About Atmos Energy

As mentioned in the introduction, Atmos Energy Corporation is a regulated natural gas utility that serves customers located in Colorado, Kansas, Texas, Louisiana, Mississippi, Tennessee, Kentucky, and Virginia. This is obviously a fairly large region that encompasses many of the southern states. However, with the notable exception of Texas and Louisiana, a good part of this service territory is not densely populated. As such, Atmos Energy only serves approximately 3.3 million customers, which makes it quite a bit smaller than many other utilities. For example, Eversource Energy ( ES ), which only serves three states in New England, has a higher customer count than Atmos Energy.

However, in my last article on Atmos Energy, I pointed out that its customer base is not necessarily the most important thing. After all, a larger company will typically have more shares outstanding so most things will be pretty similar between large and small companies when measured on a per-share basis. As of the time of writing, Atmos Energy has a forward price-to-earnings ratio of 18.43, which is very similar to the 18.33 ratio of Ameren Corporation ( AEE ) despite the fact that Ameren has a much smaller customer base. Thus, the company’s size is largely immaterial, or at least it should be when determining the investment potential and return that can be obtained by purchasing a company’s stock.

For our purposes today, the most important thing is that Atmos Energy enjoys remarkably stable financial performance over time. This stability is true regardless of any problems in the broader economy. We can see this quite clearly by looking at the firm’s income statement. Here are its revenues during each of the past eleven twelve-month periods:

{kind=link}

For the most part, we do see a general trend toward growth and a very reasonable amount of stability here. However, we have seen the company’s revenues trend down during the past two-quarters relative to what the company had in the prior year quarter. For instance, Atmos Energy only had top-line revenue of $662.7 million in the third quarter of 2023 (the company uses an October to September fiscal year) compared to $816.4 million in the third quarter of 2022. Its second-quarter 2023 revenues came in at $1.541 billion compared to $1.649 billion in the second quarter of 2022. One big reason for this was, of course, the fact that the most recent winter was the warmest one since the 1980s. That resulted in the company’s customers needing to consume lesser amounts of natural gas to heat their homes than during a normal winter, adversely affecting revenues. The most recent quarter saw natural gas prices average much lower than during the corresponding quarter of 2022, which also adversely affected revenues.

However, both of these factors also affected the company’s input costs. After all, Atmos Energy has to purchase the natural gas that it distributes to the customers. The amount that it pays for natural gas goes down when customers consume less natural gas or when natural gas prices are lower. As a result, the company’s operating income does not show the same year-over-year weakness during the two most recent quarters:

{kind=link}

As we can see here, the company’s operating income almost always comes in higher during a given quarter than during the same quarter of the previous year. In fact, the only exception to this that I can see is that December 2021’s operating income came in a bit weaker than December 2020’s operating income. Otherwise, we see the general stability of the company’s income on full display here.

I explained the reason for the company’s relative stability in my previous article on Atmos Energy:

The reason for the relative stability of the company’s cash flows should be fairly obvious. After all, Atmos Energy provides a product that most people consider to be a necessity for our modern way of life. There are very few people that do not have some sort of heating system in their homes, and for people that are on a natural gas line, that heating system will almost certainly be powered by natural gas. As such, the company’s customers will generally prioritize paying their natural gas bills ahead of making discretionary purchases during periods in which money gets tight.

As I pointed out in a recent article , we are seeing numerous signs that money is getting very tight for numerous consumers. For example, the United States Census Bureau states that the child poverty rate in the United States doubled last year and total household debt is at a record level as people increasingly resort to their credit cards to maintain their spending in today’s highly inflationary environment. As I have pointed out numerous times before, it is uncertain when the American consumer will finally reach their limit and be forced to cut discretionary spending, but it will happen at some point. Atmos Energy should prove to be relatively unaffected by this though, since it seems unlikely that its customers will decide against paying their natural gas bill and risk being without heat in their homes. Thus, the company could serve as a core holding in a portfolio that can be relied upon to deliver slow and steady growth regardless of anything that is going on in the broader economy.

Growth Prospects And Total Return

As we saw above, Atmos Energy has generally managed to grow its revenue and operating income over time. The same is true for operating cash flow, as we can see in this chart that shows the company’s operating cash flow figures for the past eleven twelve-month periods:

{kind=link}

As I have pointed out numerous times in other articles on utilities that operate in Texas or other central states, Winter Storm Uri in February of 2021 had a severely negative impact on the utilities operating in that region. This skewed the company’s operating cash flows to highly unusual levels for that entire year due to the severity of the event. In the absence of this event, we would see the company’s operating cash flows exhibit much more stability over time. However, they will still fluctuate more than operating income due to the timing of payments and similar things. Overall, the point here is that the company’s cash flows should generally trend upward over time.

Atmos Energy is positioned to continue to deliver on its historic growth going forward. The primary way that it will accomplish this growth is by increasing its rate base. As I explained in the previous article,

The rate base is the value of the company’s assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase to the rate base allows the company to raise the prices that it charges its customers in order to earn this allowed rate of return. The usual way that a utility will grow its rate base is by investing money into upgrading, modernizing, or even expanding its utility-grade infrastructure.

In its August 2023 investor presentation , Atmos Energy included the following chart that states that it intends to invest approximately $15 billion into its infrastructure over the 2023 to 2027 period:

Atmos Energy

This should allow the company to increase its earnings per share at a 6% to 8% rate over the period. When we combine this with the company’s current 2.65% dividend yield, we can project an average total return of 8.7% to 10.7% annually. This is decent, but it is below the projected total return that some of the company’s peers should be able to deliver. The reason for the lower projected total return vs. the 11% or 12% offered by some of Atmos Energy’s peers is because of the dividend yield. Atmos Energy’s yield is well below that of other natural gas utilities:

| Company |

| Dividend Yield |

| Atmos Energy |

| 2.65% |

| Spire Inc. ( SR ) |

| 4.92% |

| New Jersey Resources ( NJR ) |

| 3.96% |

| NiSource Inc. ( NI ) |

| 3.70% |

| Southwest Gas Holdings ( SWX ) |

| 4.00% |

| Northwest Natural Holding ( NWN ) |

| 4.89% |

While not all of these companies are expected to deliver the same strong growth as Atmos Energy, their much higher yields result in them boasting more attractive total returns. This is something that could prove pretty important if the United States does enter into a recession, as such an event might be accompanied by a stock market decline. In that case, the dividend will become even more important as a component of total return.

Market Performance

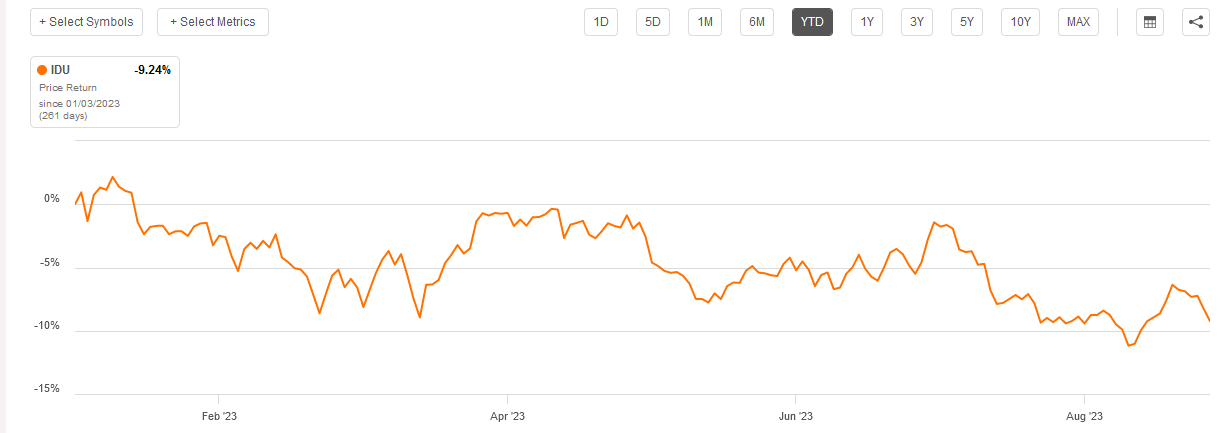

As mentioned in the introduction, one of the reasons why Atmos Energy has a lower yield than some of its peers is that the stock has not been punished nearly as much year-to-date. As I pointed out in a few recent articles, investors have been selling off utilities in favor of safer assets with comparable yields. As we can see here, the U.S. Utilities Index is down 9.24% year-to-date:

{kind=link}

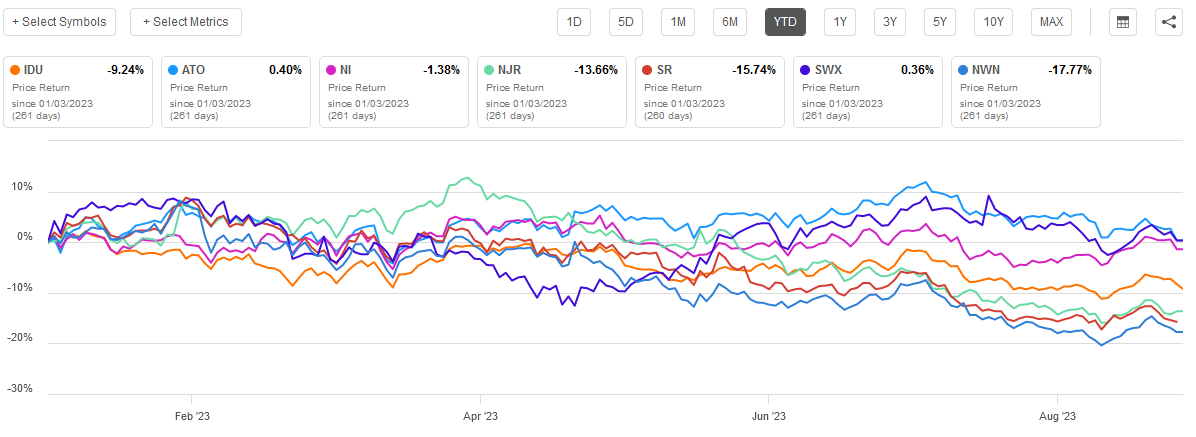

However, Atmos Energy’s stock price has been proving to be quite resilient in the face of the utility selloff. As we can see here, the company’s stock has not only substantially outperformed the utility index but also all of its peers year-to-date:

{kind=link}

The only company that even comes close to matching Atmos Energy’s price performance is Southwest Gas Holdings. Southwest Gas has actually outperformed Atmos Energy on a total return basis due to its much higher dividend.

The point though is that it is possible that Atmos Energy has become somewhat overvalued given current market conditions. While it is probably the best company of any of these, with the strongest balance sheet (as we will see in just a minute), the outsized performance cannot really be explained, and it may result in a correction at some point. Analysts at Wells Fargo appear to agree with me, as they just downgraded the stock citing strong outperformance relative to its peers.

Financial Considerations

As I stated in my previous article on Atmos Energy,

It is always important that we investigate the way that a company is financing its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is usually accomplished by issuing new debt and using the proceeds to repay the existing debt because very few companies have sufficient cash on hand to completely repay their debt as it matures. This can cause a company’s interest expenses to increase following the rollover in certain market conditions. As of the time of writing, interest rates in the United States are at the highest levels that we have seen in more than twenty years so this is a very real concern today. In addition to interest-rate risk, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company’s cash flows to decline could push it into financial distress if it has too much debt. Although utilities like Atmos Energy typically have remarkably stable cash flow, bankruptcies have occurred in the sector so this is not a risk that we should ignore.

One ratio that we can use to analyze a company’s financial structure is the net debt-to-equity ratio. As of June 30, 2023, Atmos Energy had a net debt of $6.4702 billion compared to $10.6024 billion in shareholders’ equity. This gives the company a net debt-to-equity ratio of 0.61 today. This represents a very slight improvement over the 0.62 ratio that the company had at the end of March 2023 so that is a good sign. After all, it tells us that the company is certainly not leveraging itself up.

Here is how Atmos Energy compares to its peers in this respect:

| Company |

| Net Debt-to-Equity |

| Atmos Energy |

| 0.61 |

| Spire Inc. |

| 1.54 |

| New Jersey Resources |

| 1.59 |

| NiSource Inc. |

| 1.65 |

| Southwest Gas Holdings |

| 1.50 |

| Northwest Natural Holding |

| 1.22 |

As has been the case every time that we have discussed this company, Atmos Energy boasts a considerably lower net debt-to-equity ratio than any of its peers. This is a clear sign that the company is not overly reliant on debt to finance its operations. Thus, we should not need to worry too much about the company’s leverage.

Dividend Analysis

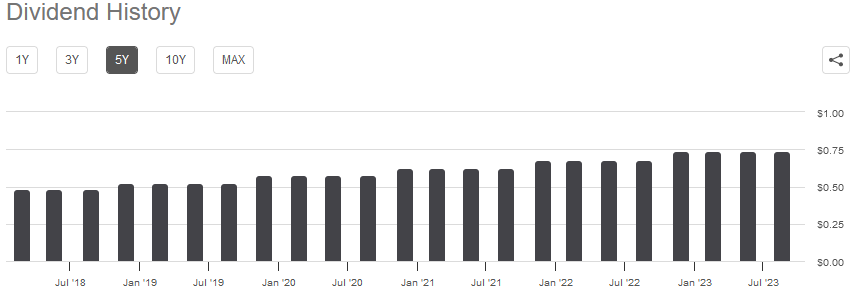

One of the biggest reasons why many investors purchase shares of utility companies like Atmos Energy is the high dividend yields that these companies tend to possess. Unfortunately, Atmos Energy does not do nearly as well as many of its peers in this respect. As we discussed earlier, the company’s 2.65% current yield is considerably below that of many other natural gas utilities, although it is still higher than the 1.51% current yield of the S&P 500 Index (SP500). Fortunately, Atmos Energy does have a long history of raising its dividend over time:

{kind=link}

As we can see here, the company has historically increased its dividend annually. This is nice in today’s inflationary environment because it helps to maintain the purchasing power of the dividend. It also should result in anyone buying the stock receiving a considerably higher yield-on-cost in only a few years.

As is always the case, though, it is important that we ensure that the company can actually afford the dividends that it pays out. After all, we do not want to be the victims of a dividend cut since that would reduce our incomes and almost certainly cause the company’s stock price to decline.

The usual way that we judge a company’s ability to afford its dividends is by looking at its free cash flow. During the twelve-month period that ended on June 30, 2023, Atmos Energy Corporation reported a levered free cash flow of $405.6 million. This was, unfortunately, not enough to cover the $415.7 million that the company paid out in dividends over the same period, but it did get pretty close. However, this may still be concerning as the company failed to generate sufficient cash internally to cover the dividends that it paid out.

However, it is quite common for utilities to issue debt and equity to finance their capital expenditures. These companies will then pay their dividends out of operating cash flow. This is done because of the enormous costs of constructing and maintaining a utility-grade infrastructure network over a wide geographic area. During the twelve-month period that ended on June 30, 2023, Atmos Energy Corporation reported an operating cash flow of $3.2698 billion. That was, obviously, more than enough to cover the $415.7 million that the company paid out in dividends with a substantial amount of money left over for other purposes. Overall, we should not need to worry about the company’s dividend safety very much.

Valuation

According to Zacks Investment Research , Atmos Energy will grow its earnings per share at a 7.25% rate over the next three to five years. This is in line with the 6% to 8% earnings per share growth that we calculated earlier based on the company’s projected rate base growth, so it should be pretty solid. If we assume that the company will grow its earnings per share at this rate, the stock has a price-to-earnings growth ratio of 2.54 at the current share price. Here is how that compares to the company’s peers:

| Company |

| PEG Ratio |

| Atmos Energy |

| 2.54 |

| Spire Inc. |

| 3.32 |

| New Jersey Resources |

| 2.69 |

| NiSource Inc. |

| 2.45 |

| Southwest Gas Holdings |

| 3.67 |

| Northwest Natural Holding |

| 3.99 |

Here we can see that Atmos Energy does not appear to be particularly overvalued relative to its peers. This is despite the fact that the stock has generally delivered a better performance than its peers year-to-date, which has greatly reduced the relative valuation of the other companies on this list. However, it is important to consider that this ratio does not consider the impact of the company’s dividend at all, and as we have already seen, all of these companies will deliver a much higher yield than Atmos Energy. That could actually result in Atmos Energy delivering a disappointing total return, despite its attractive valuation.

Conclusion

In conclusion, Atmos Energy Corporation is one of the best pure-play natural gas utilities in the United States. The company’s stock price over the last year has reflected that, and it has generally outperformed its peers. However, this may have resulted in the company’s forward total return potential being considerably lower than its peers. It might still make sense to buy the shares given Atmos Energy’s strong finances and the likelihood of a near-term recession, but overall the company may not be the best investment in the sector right now.

For further details see:

Atmos Energy: Excellent Company, But Forward Total Returns May Disappoint Vs. Peers