ATO - Atmos Energy: Raises Its Dividend While Giving Positive Long-Term Guidance

2023-11-08 23:00:54 ET

Summary

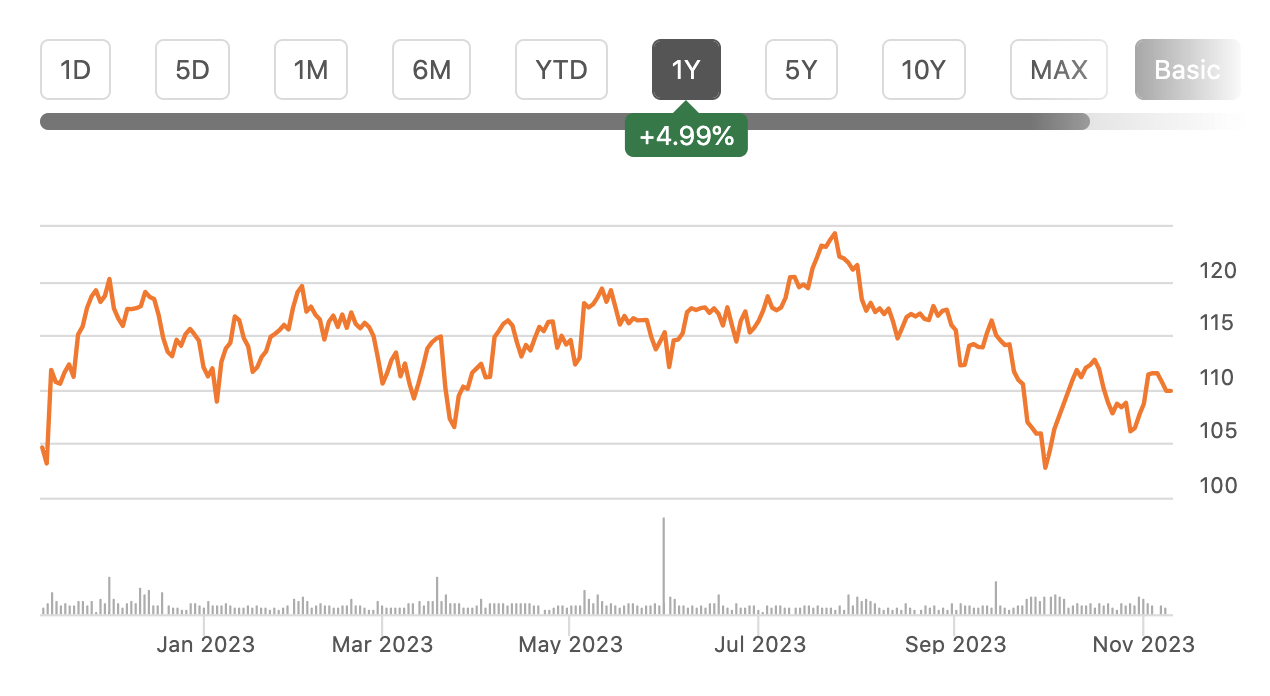

- Atmos Energy shares have risen 12% since my buy recommendation, consistent with the steady growth expected from its secured and regulated business model.

- The company reported solid earnings in its fiscal fourth quarter, with distribution operating income and pipeline operating income both increasing.

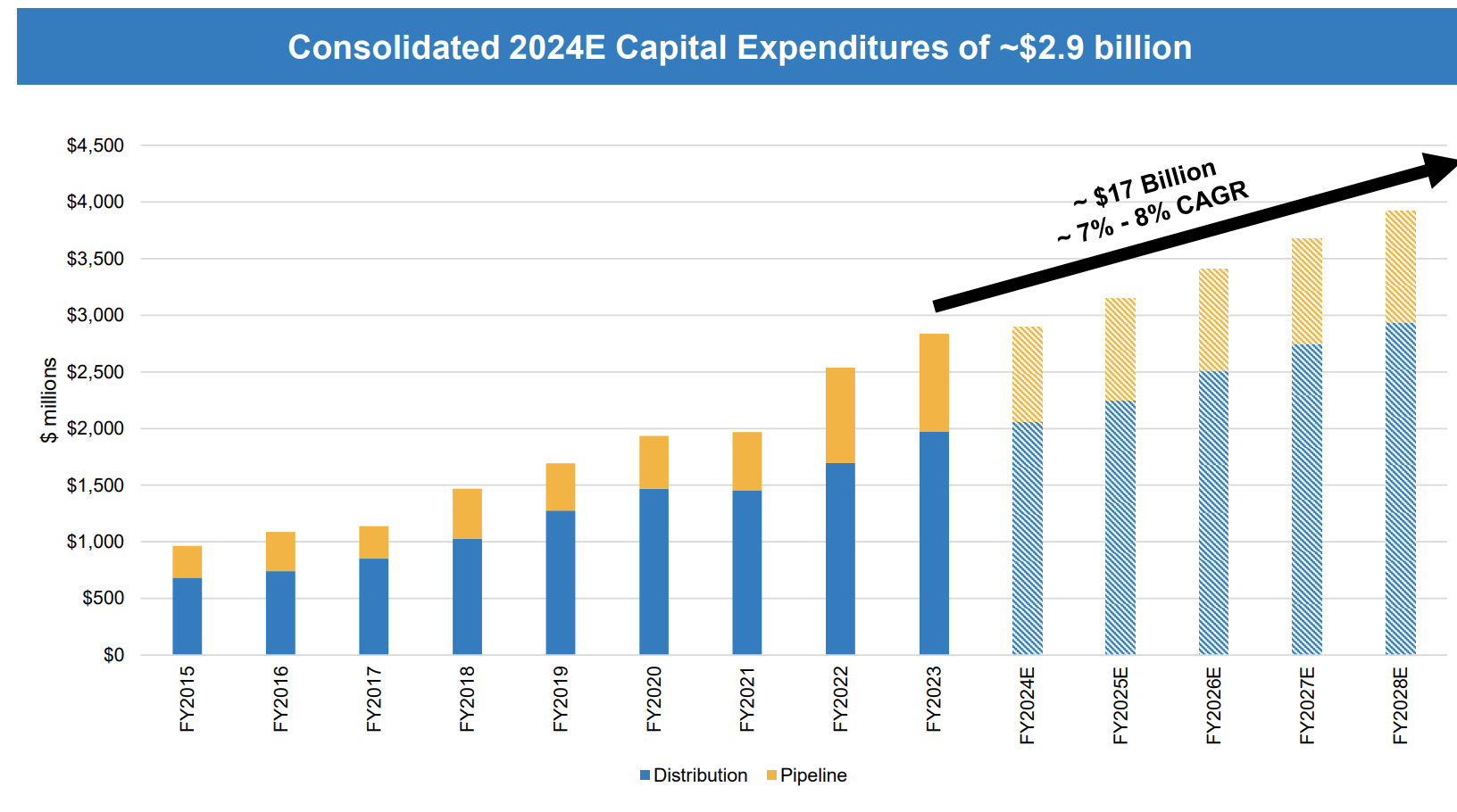

- Atmos plans to increase its rate base to $29 billion from $16.6 billion through $17 billion in planned capex, supporting future growth and dividend payments.

Shares of Atmos Energy ( ATO ) have risen returned 12% since I recommended buying them last year . While this has lagged the market’s 20% return, it is consistent with the steady growth I expect from Atmos’s secured and highly-regulated business model. On Wednesday, the company reported solid earnings, and I continue to view ATO as a company capable of generate high single-digit profit and dividend growth.

{kind=link}

In the company’s fiscal fourth quarter, Atmos earned $0.80 in GAAP EPS, beating consensus by $0.08. Atmos is a natural gas utility, storing, transporting, and distributing natural gas to residential and industrial customers across the South-Central United States with Texas accounting for the majority of its business. It gets about 2/3 of its operating income from distribution and about 1/3 from pipelines and storage.

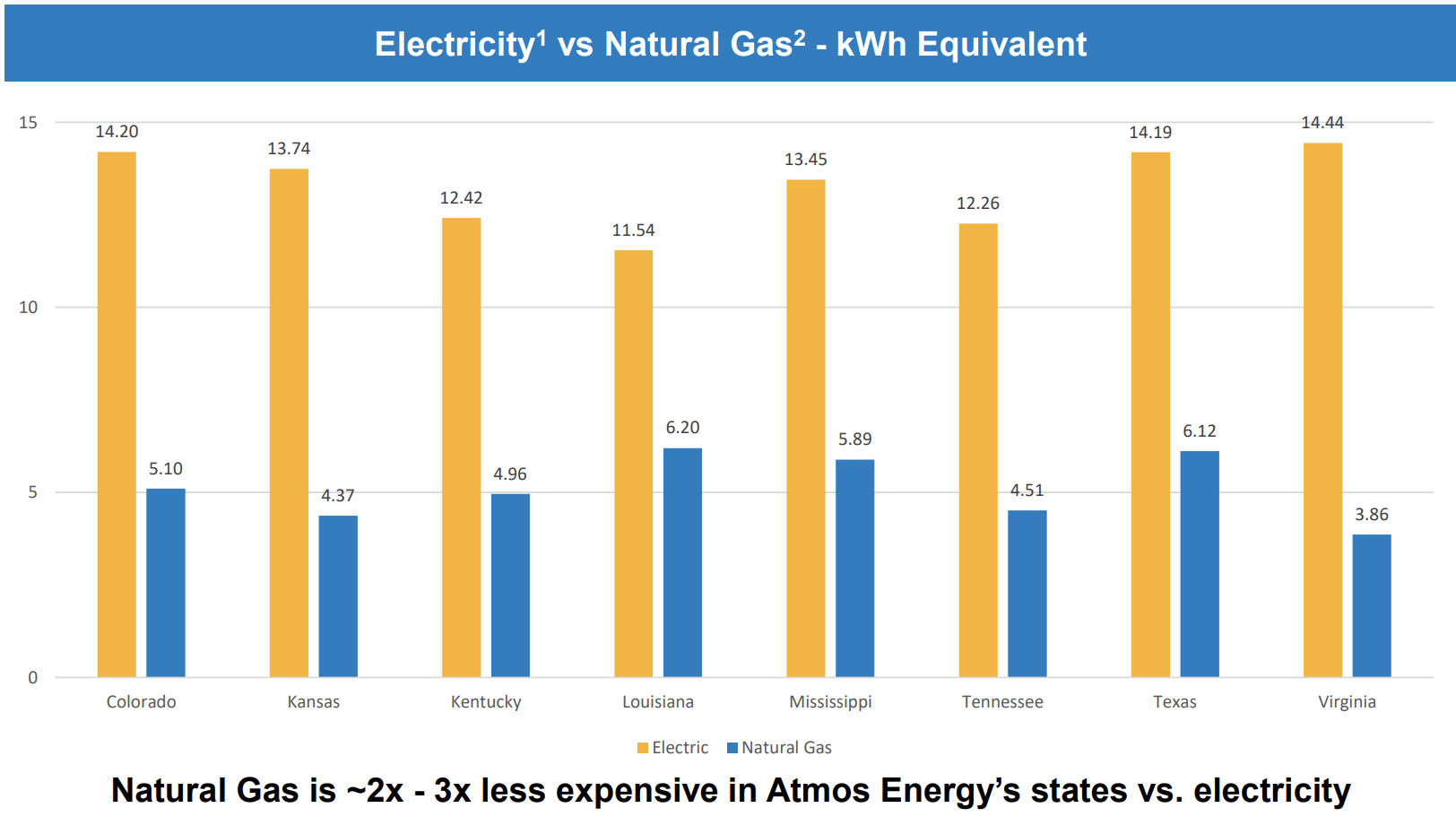

Atmos itself takes no commodity risk with those costs passed on to customers. Its rates are set by regulators with the company earning a guaranteed return on approved capital spending. As such, as investors, we want to see Atmos continue to spend on cap-ex, growing its rate base, and thereby increasing its earnings power. Because of the abundance of natural gas, even as Atmos has generated substantial regulatory increases, its cost to customers remains a fraction of electricity across the states it operates in, providing ongoing ability to get approval for rate increases.

{kind=link}

Because its returns and rates are agreed to by regulators, Atmos generates very steady results, which is why I view it as an ideal name for income-growth investors. That was on full display in the fourth quarter. Distribution operating income rose nearly 50% to $54 million with a net $12 million increase from rate increases on capital investment and 4% from customer growth. For the full year, distribution operating income rose nearly 15% to $693 million thanks to strong rate actions.

Pipeline and storage operating income rose by $32 million to $100 million, of this there was $14 million in benefit from maintenance timing. Still, rate growth provided a $15 million tailwind. For the full year, pipeline operating income rose 15% to $375 million, again thanks to solid rate actions.

The company spent $2.8 billion in cap-ex during 2023. Importantly, 85% of its capital spending is related to safety and reliability. Atmos is not investing in speculative expansion; it is enhancing its own network, which is why regulators have approved projects and associated increases. Atmos begins to earn a return on 90% of its spending within six months and 99% of its spending within 12 months. In 2023, Atmos generated $263 million of regulatory increases; with $113 million to be implemented this quarter.

Alongside these results, Atmos raised its dividend by to $0.805, and dividend growth in 2024 will be 9% from fiscal 2023 levels. This marks forty years of dividend growth. A growing rate base means growing profits, cash flow, and dividend capacity. Critically, the outlook for 2024 and beyond is quite positive.

Next year, EPS should be $6.45-$6.85, per management guidance, providing 7.4% growth from this year’s $6.10. That is supported by $2.9 billion in capital spending, up just under 4% from this year. By 2028, given the company’s plans, it expects to earn $8.55, for a compounded growth rate of 6-8% over the next five years. Again, ATO is not a stock that will triple your money in a year, but it will consistently grow cash flow and dividend payments over the medium term, and that can play an important role in a balanced portfolio.

Atmos will generate this growth because it has $17 billion in cap-ex planned through 2028, increasing its rate base to ~$29 billion from $16.6 billion currently. As you can see below, it will be steadily increasing cap-ex by 7-8% in order to build this large rate base and grow revenue, maintaining a similar 2:1 business mix between distribution and pipelines.

{kind=link}

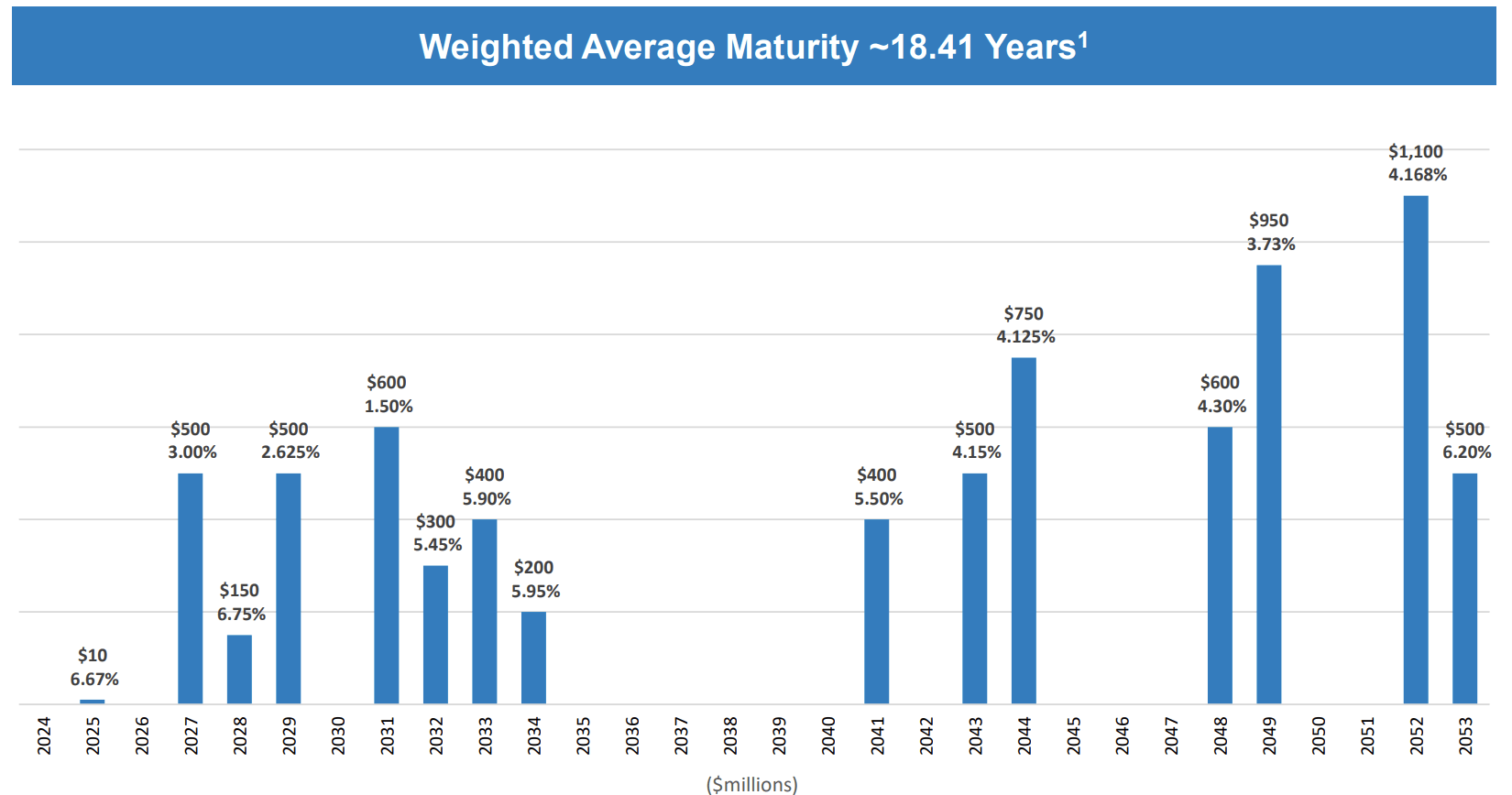

It funds cap-ex via a combination of cash flow, debt, and equity issuance. It has an equity forward on 4 million shares at $117.85, or 8% above current levels. Atmos has a history of selling equity at an accretive level, as with this sale. I would note the company’s EPS targets include the impact of dilution from issuance. Equity accounts for 61.5% of Atmos’s total capitalization. This is up from 54% last year as it has recouped costs related to brutal Texas winter storms that increased securitized debt. In this world of elevated interest rates, the fact debt accounts for less of its funding is a positive. Moreover, Atmos has no significant maturities until 2027, meaning it does not have to refinance debt at today’s elevated interest rates.

{kind=link}

Overall, Atmos delivered another solid quarter as its growing rate base enables higher operating income and growing dividends. With this 9% dividend growth, shares have a 2.9% dividend yield. Additionally, with its strong regulated business, safety-focused cap-ex spending plan, I view the plan for 6-8% growth as reasonable and consistent with the company’s history of execution.

At the midpoint, Atmos can grow its dividend by 7% over the medium, which combined with its current dividend yield, creates the potential of about ~10% long-term returns. For a noncyclical business that earns a regulatory-approved return on capital, I view this as an attractive long-term return. Atmos may not be a flashy stock, but with a growing number of customers and rising rate base, the company is well positioned to generate sustained, steady income growth. I expect about a 10% return over the next year and through 2028 and would be a buyer of ATO here.

For further details see:

Atmos Energy: Raises Its Dividend While Giving Positive Long-Term Guidance