AEXAF - Atos: Struggling Business With A Difficult Route To Competitiveness

2023-12-12 22:17:25 ET

Summary

- Atos’ financial performance has been underwhelming, with low growth and declining profitability. Atos’ acquisitions have failed, and its core businesses are progressively becoming less competitive.

- Management is seeking to restructure the company, but it is likely too late. We believe they are overestimating the value of both segments given the growth rates and trajectory relative.

- Looking ahead, we see significant execution risk with limited upside. Even if its weaker segment is spun off, the remaining company is far less competitive than its peers.

- We suggest investors avoid Atos and consider one of its many better-performing peers, some of which we have covered.

Investment thesis

Our current investment thesis is:

- Atos is struggling currently, reflective of a decade of growing competitive pressures. A large portion of the company appears worthless, with the remaining segment growing in the low single digits. Given the industry trajectory and the performance of its peers, we struggle to see how the business can be turned around successfully.

- Atos’ valuation appears low, particularly when considering the current economic downturn. This said, we consider the numbers deceiving given the imminent restructuring, Should a successful turnaround be achieved, this will allow for a significant upside.

Company description

Atos SE ( AEXAF ) is a global leader in digital transformation and information technology services. Headquartered in France, ATOS operates in various sectors, providing consulting, integration, managed services, and business process outsourcing.

Share price

Atos’s share price performance has been disastrous, losing over 80% of its value. This is a reflection of its declining competitive position and management's struggles to execute effectively, contributing to poor financial results.

Financial analysis

{kind=link}

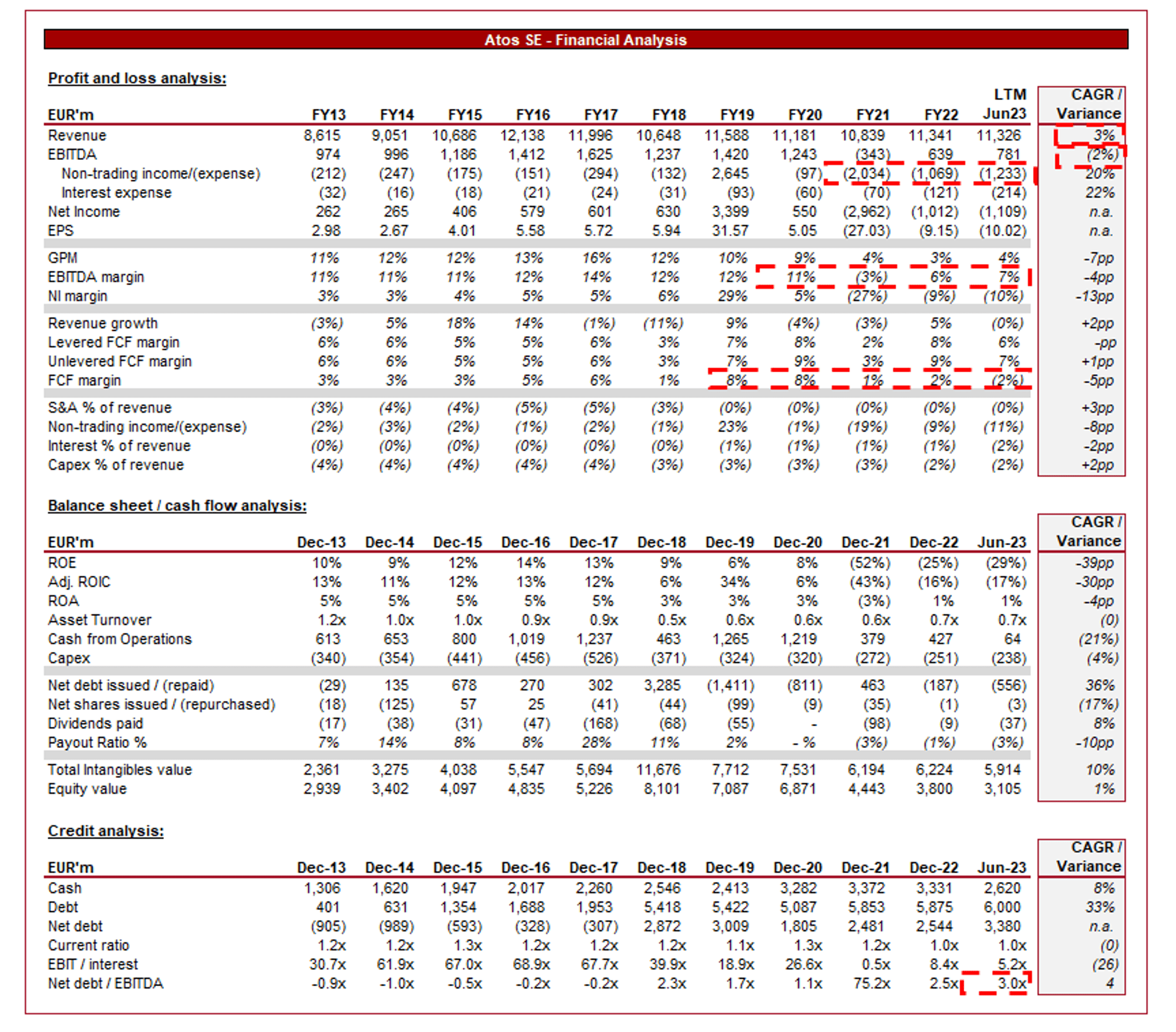

Presented above are Atos' financial results.

Revenue & Commercial Factors

Atos’ revenue growth has been disappointing (+3% CAGR), particularly when considering the industry growth experienced and the amount of M&A conducted (>€6b of cash spent).

Business Model

Atos provides a wide range of IT services, including consulting, system integration, managed services, and digital transformation solutions. It caters to diverse industries, with a significant global scale to provide a tailored service. This scale is important for collaboration with key players in the IT ecosystem (such as with AWS ( AMZN )), allowing for the development and delivery of competitive and comprehensive solutions to its clients.

{kind=link}

Atos focuses on assisting businesses in their digital transformation journey, which we consider a key growth area. This involves leveraging emerging technologies such as cloud computing, cybersecurity, data analytics, and artificial intelligence to enhance operational efficiency and competitiveness. With the increased digitalization of society and operations, management teams are increasingly seeking to incorporate these technologies to gain an advantage relative to peers. We expect these factors to drive industry growth in the coming years.

Competitive Positioning

In spite of the strong industry tailwinds, Atos’ growth has been disappointing, with the company losing market share and experiencing a reduction in size, even when factoring in M&A.

We attribute this to a number of factors, including:

- Market Saturation and Competition: The IT services industry experienced a significant increase in new market entrants as its attractiveness developed, contributing to high competition and several major players. Saturation in the market has contributed to a need to differentiate, which Atos has clearly failed at.

- Offshoring: As the industry has transitioned toward maturity, there has been a push toward offshoring staff to regions such as India and the Philippines. This has contributed to a “race to the bottom” for many “simpler” IT services, such as managed services, integration, and maintenance. We believe this has further depressed Atos’ competitive position from a pricing perspective.

- Execution Challenges: Atos has poorly executed its strategic imperatives, lacking the development of relationships with leading institutions that can drive long-term projects. Management has failed to make it an attractive proposition.

- Technological Disruptions: Rapid technological advancements have posed challenges to Atos as it is critical to keep up with emerging technologies and transition/up-sell existing clients to new platforms. We believe the Cloud adoption trend in particular has been underexploited by Atos relative to its peers and is a primary reason for its relative underperformance ( which is discussed later ).

- Integration Challenges from Acquisitions: Despite spending over €6b of cash on acquisitions, Atos’ current market cap is below this level. Management has struggled to incorporate and develop new businesses, which is notoriously difficult in the consulting segment given the dependency on people and relationships.

Atos faces competition from the Big 4, Capgemini ( CAPMF ), Accenture ( ACN ), and IBM ( IBM ), among many other IT-focused consulting firms. We believe all of these firms have performed far better and can illustrate this in their growth rate. It is inevitable that Atos has lost talent during this lost decade, further compounding the negative spiral experienced.

Margins

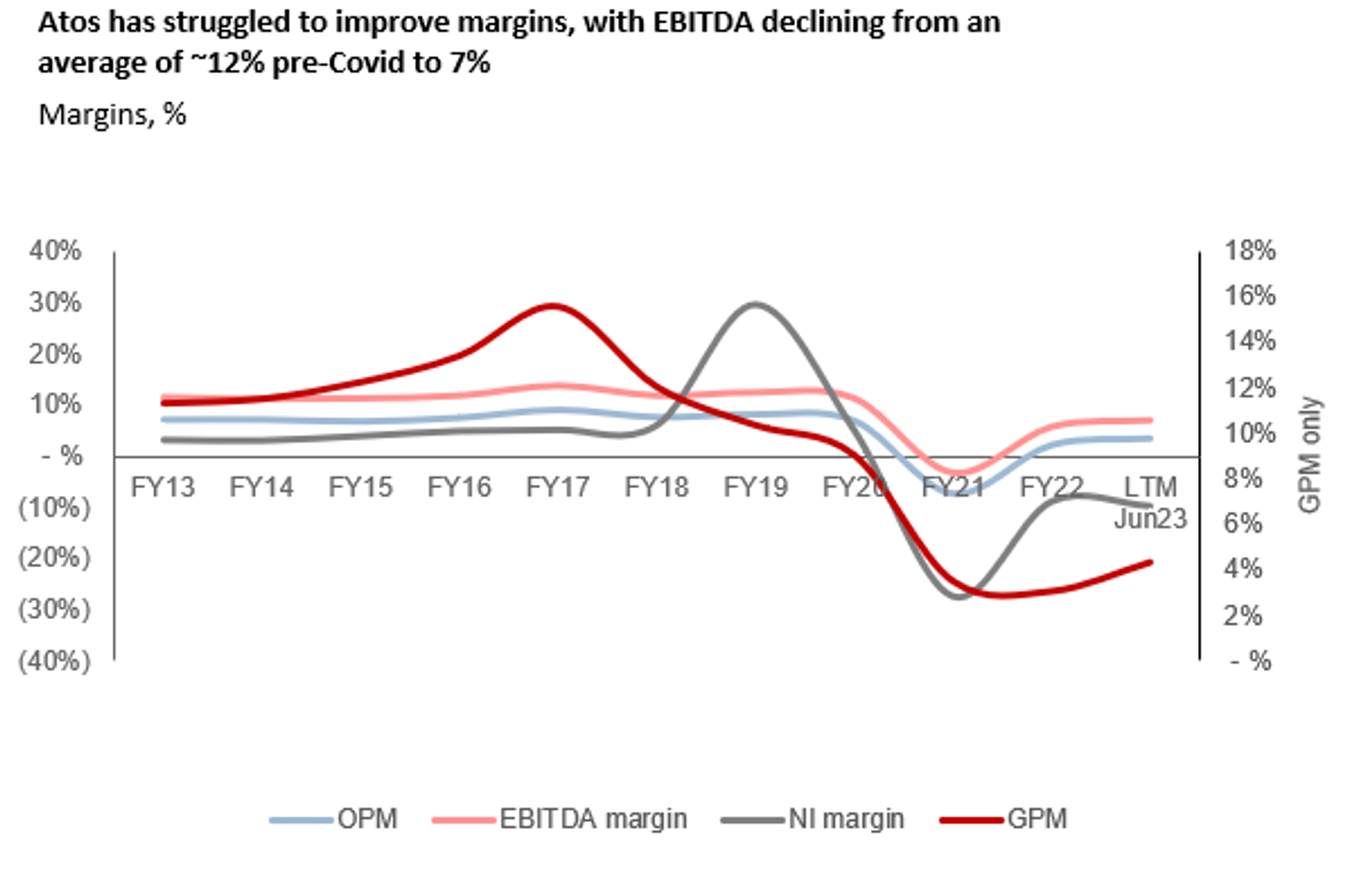

{kind=link}

Atos’ margin development has been disappointing despite the company’s growth in scale. We attribute this to Atos’ limited development in the market, contributing to pricing pressure as new entrants take market share. Further, the company has a bloated cost base, with limited progress in rationalizing non-core costs.

Given the limited progress during the LTM period, we expect Atos to normalize at a level below its historical average. More broadly, we suspect its declining competitive position will contribute to further downward pressure.

Recent trading

Atos’ half-year results have been disappointing, with top-line revenue growth of (2.5)%, +2.6%, +6.7%, and (0.3)% in its last four periods. In conjunction with this, margins have stabilized, although are not showing clear directional progress. The disappointment continues into its Q3 flash trading, with organic growth of (3)%.

Atos’ “Tech Foundations” segment continues to struggle, with negative organic growth and a deliberate reduction in size as Management seeks to reorganize the segment into a sustainable business. Most recently, Atos divested its Atos Italia segment. Eviden, on the other hand, is progressing well, although not to the extent we would consider it attractive. Organic growth was +2.3% in Q3 and differentiation is limited.

More broadly, the business is being negatively impacted by macroeconomic conditions, with the combination of inflation and interest rates contributing to uncertainty, contributing to conservatism among corporates.

Balance sheet & Cash Flows

Atos’ balance sheet position is not immediately concerning, with an ND/EBITDA ratio of 3x. However, with declining profitability and a negative outlook, Atos is in a negative spiral.

For this reason, Management has sought to restructure the business. Plans circulated involve splitting the business in two, with the weak side ( Tech Foundations ) spun out (€0.1b cash inflow and the transfer of €1.9b in liabilities) and focus transitioning to Eviden. This will partially involve raising equity from shareholders to financially balance the remaining business. There were also talks with Airbus for it to take a stake in Eviden which later fell through.

This is a messy situation and one that will likely be value destructive, owing to the poor financial performance and the funding requirements. We are also not entirely convinced this will elevate all of the issues with Atos, as the remaining business still faces significant competitive pressures and has not shown standout growth. This said, we must praise Management for its willingness to drastically change the business, which will at least improve its trajectory.

Outlook

{kind=link}

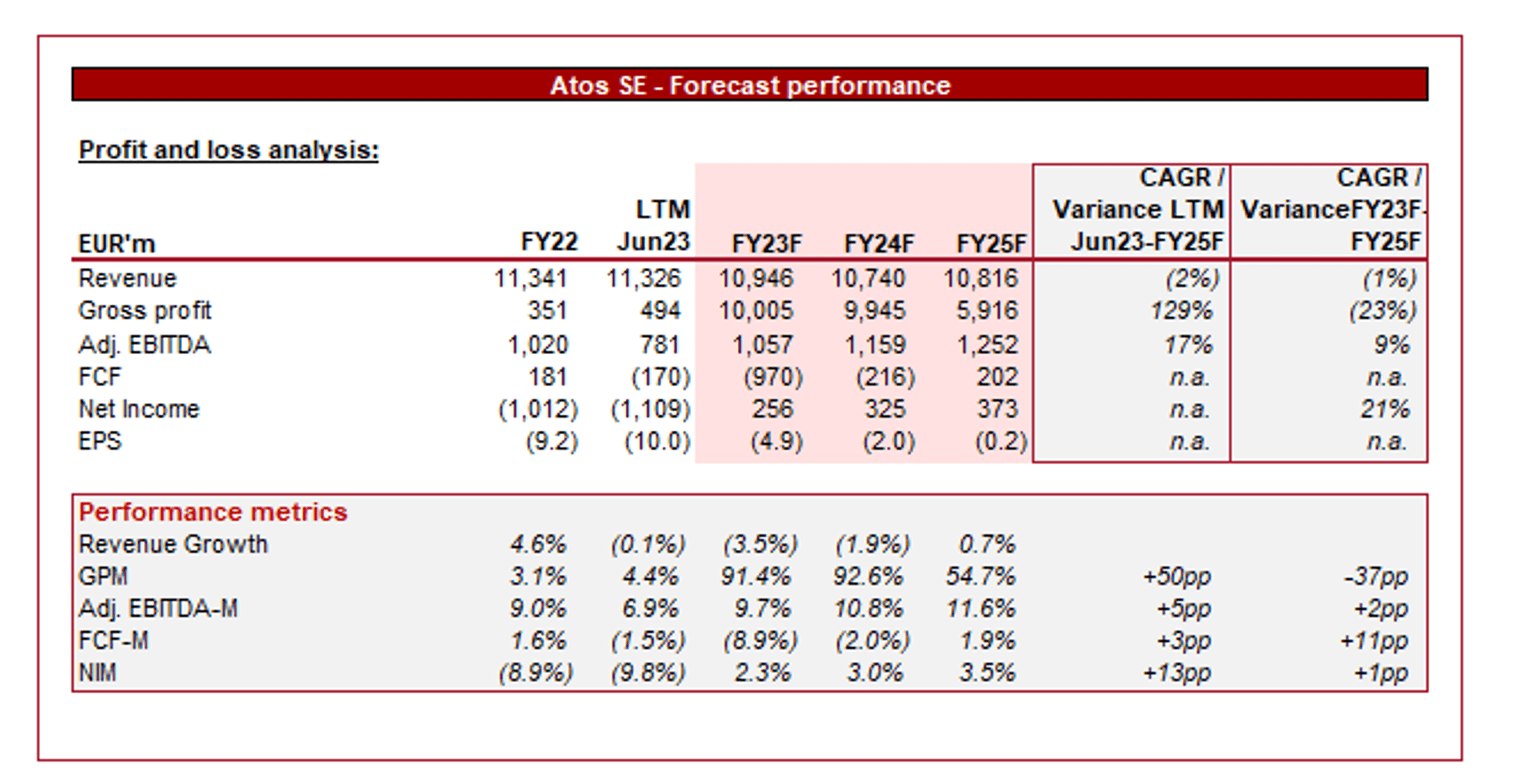

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting a decline in revenue growth into FY25F, alongside a sequential improvement in margins. Given the persistent fall experienced by Tech Foundations, revenue forecasts appear reasonable in our view (currently not pricing in a split, which is reasonable as Management will look to have further discussions with shareholders in the coming quarters).

Although we do not see margins returning to their pre-pandemic level, an improvement from the current position does appear reasonable, although will be based on the timing of economic recovery.

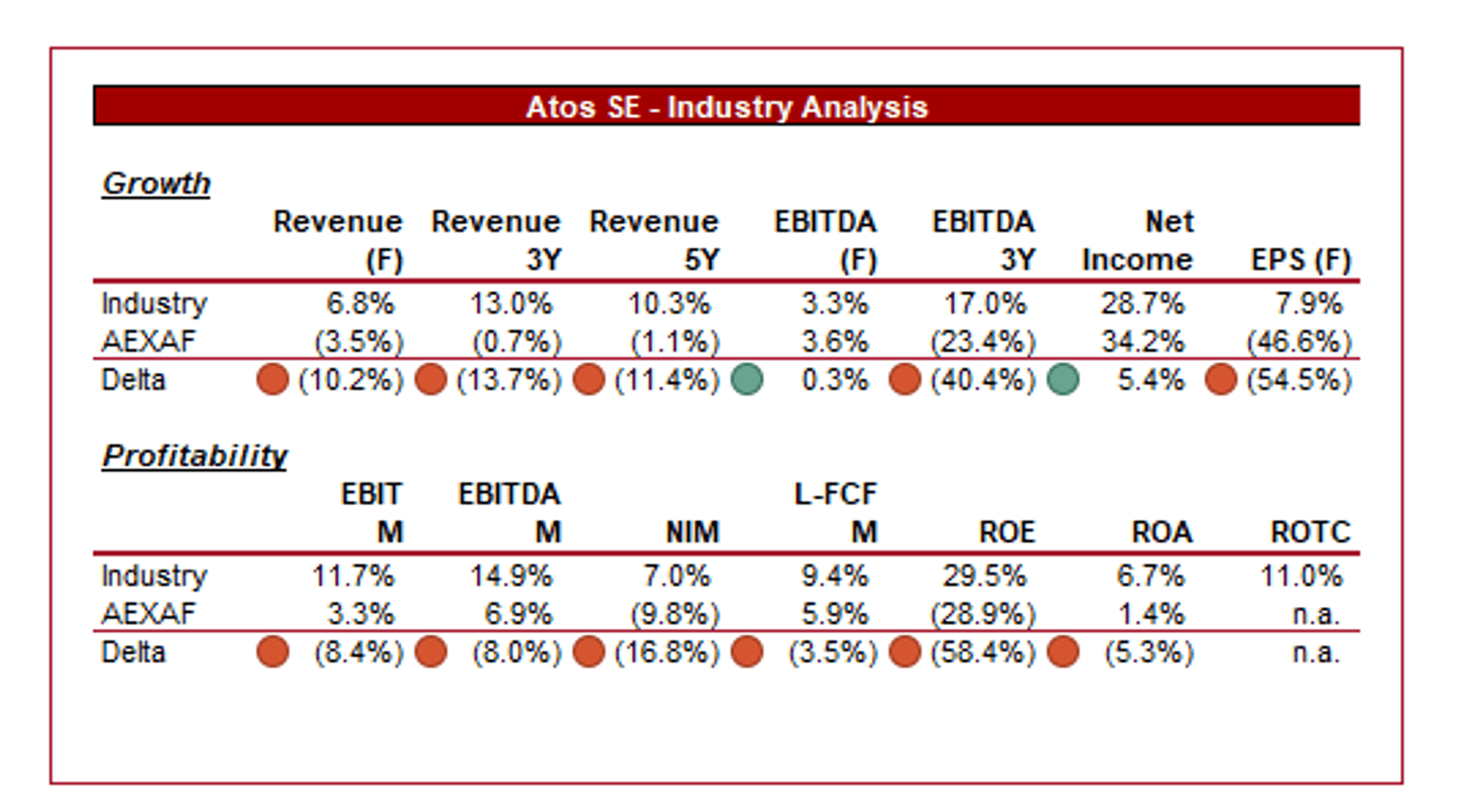

Industry analysis

IT Consulting and Other Services (Seeking Alpha)

{kind=link}

Presented above is a comparison of Atos' growth and profitability to the average of its industry, as defined by Seeking Alpha (21 companies).

Atos’ performance relative to its peers is disappointing, with lower growth and margins. We wholly attribute this to its competitive position, with clearly limited attractiveness in both its markets.

This is compounded by the size of the delta, given the numerous tailwinds the industry has experienced. There is no reason Atos should be experiencing negative growth over a longer period such as 5 years.

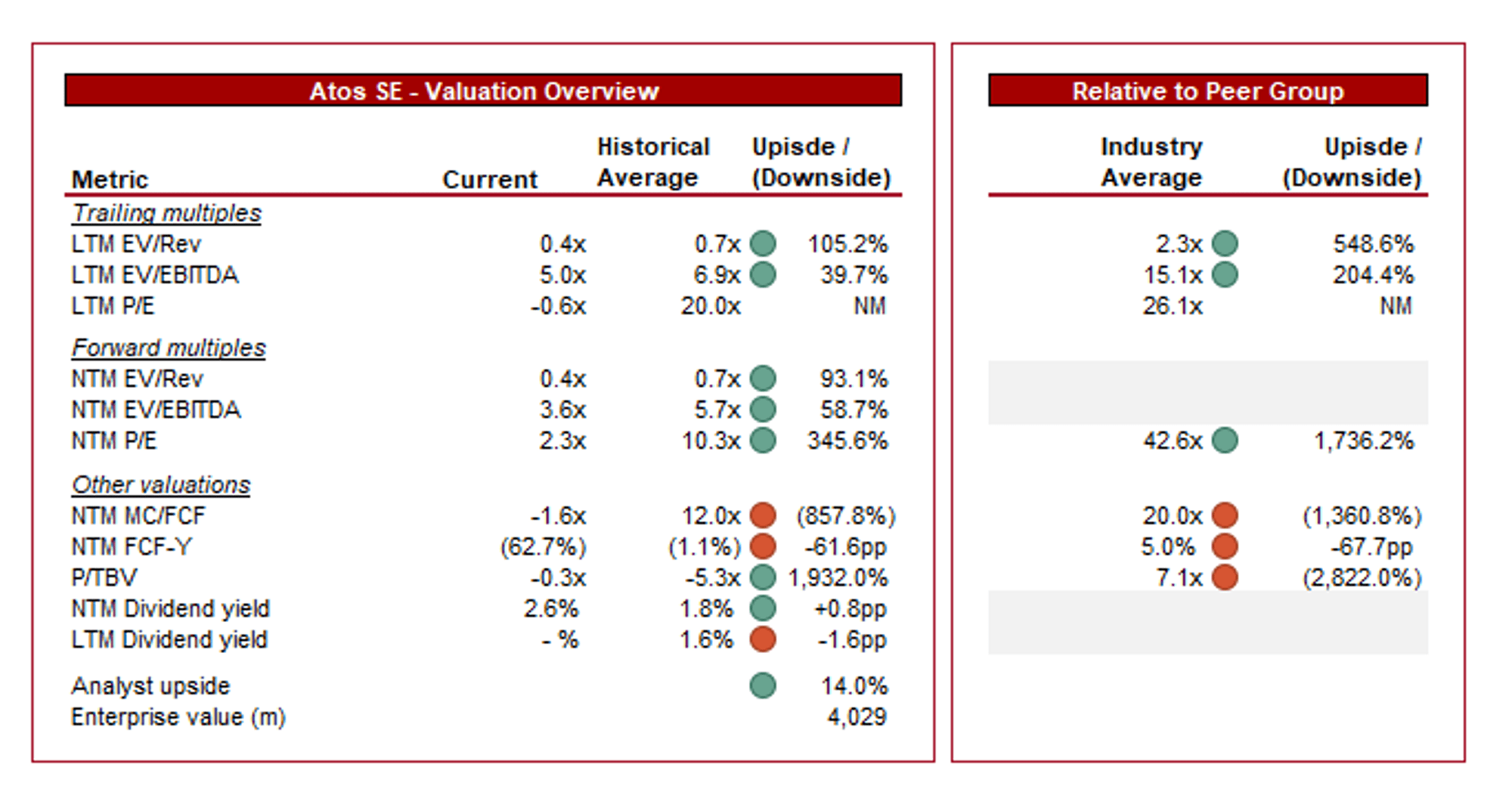

Valuation

{kind=link}

Atos is currently trading at 5x LTM EBITDA and 4x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is undoubtedly warranted. The company’s financial performance has materially declined and a substantial amount of shareholder value has been destroyed. We have limited faith in the current management team, with all efforts seemingly focused on “stabilizing the ship” rather than a resurgence.

Additionally, Atos is trading at a substantial discount to its peers. We do not believe this illustrates value currently given the limited growth achieved thus far. This is a fast-moving industry that is extremely lucrative, which both means high competition and the need for a razor-focused operation. Although the removal of Tech Foundations will likely help Eviden and the overarching trajectory, the standalone company will face new pressures as it seeks to improve its growth rate.

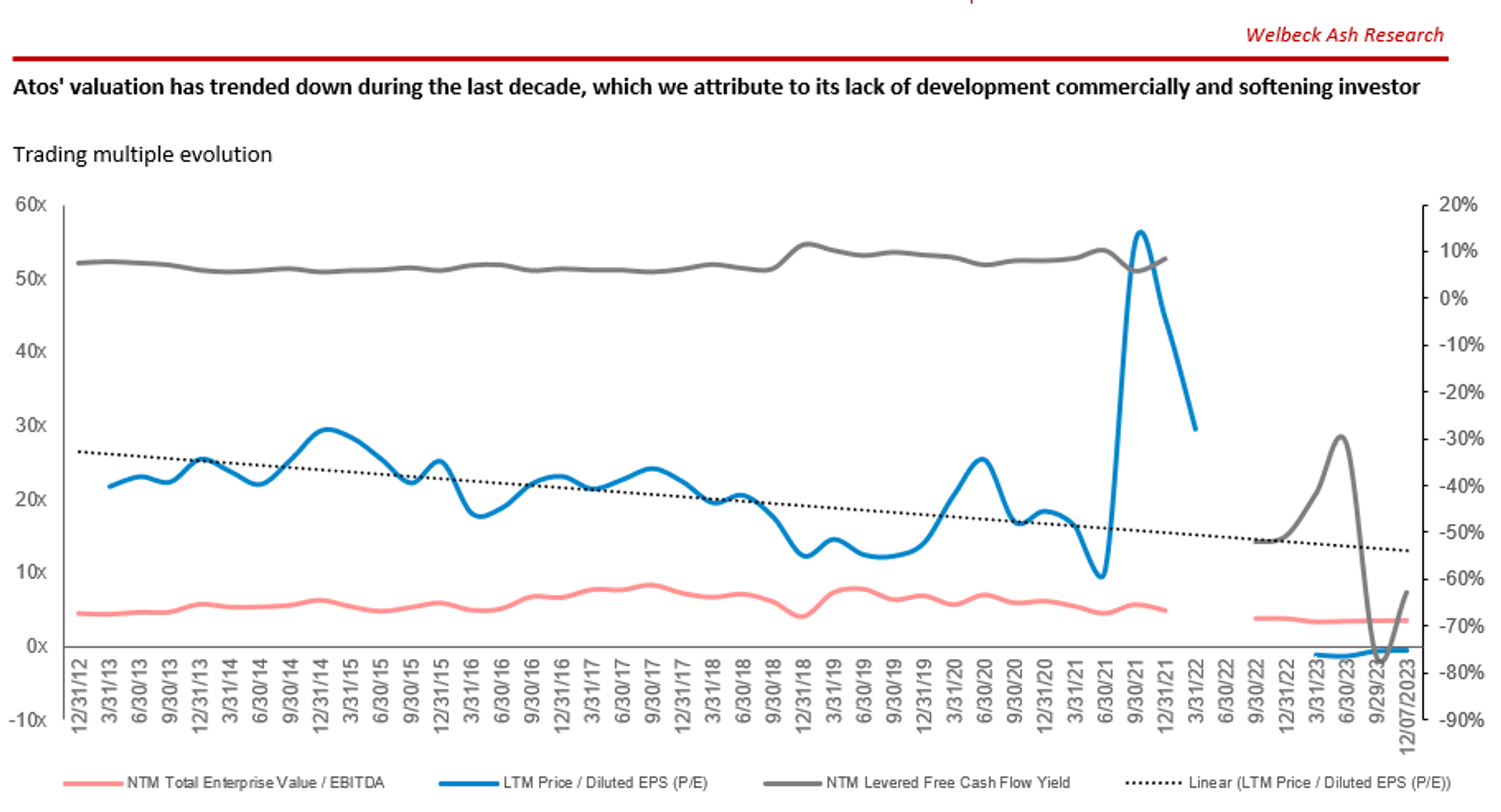

Valuation evolution (Capital IQ)

{kind=link}

Key risks with our thesis

The risks to our current thesis are:

- Successful penetration into emerging markets.

- Acceleration of growth by Eviden, likely driven by technological innovation.

Final thoughts

Atos is currently unattractive in our view. The company has experienced a decade of poor financial performance while operating in an industry that exhibits highly attractive characteristics.

Its scale, expertise, and relationships will likely mean a complete failure is off the cards, but we suspect further value destruction is possible as Management seeks to split the business. This said, if Management is able to successfully untangle the two businesses, and a renewed focus on Eviden contributes to greater growth, Atos could quickly become undervalued.

For further details see:

Atos: Struggling Business With A Difficult Route To Competitiveness