ATRC - AtriCure: Despite Reasonable Top-Line Growth No Change To Hold Thesis

Summary

- A reasonable period of top-line growth across the core portfolio last quarter, coupled with strong guidance for FY22.

- Despite this, operating losses continue to widen, and NOPAT is thin even when capitalizing on R&D.

- A combination of technicals, market positioning, and quant factors are unsupportive of ATRC re-rating any time soon.

- Net-net, we continue to rate ATRC a hold.

Investment Summary

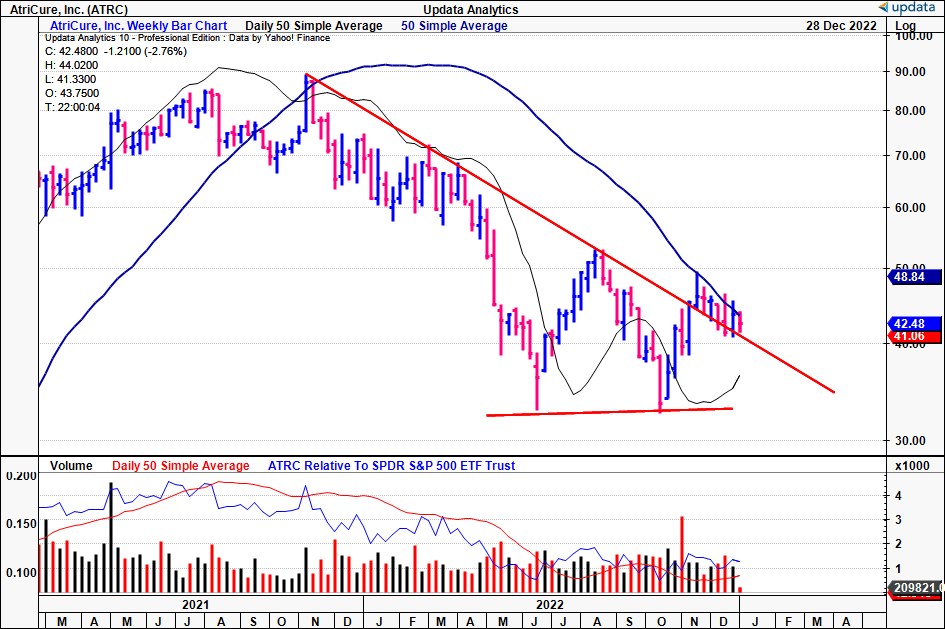

Investing in the med-tech universe comes with its perks and challenges. It's also a curious space, where unprofitable names can trade at quite substantial market values. Nevertheless, the sector hasn't been immune from the market turbulence of FY22. Since our last publication on Atricure, Inc (NASDAQ: ATRC ), the market has continued its punishment of the stock, and despite 2x attempted rallies across the year, each test has been met with rejection at key price levels [Exhibit 1]. I encourage you to read our previous publication by clicking here.

Hence, despite a reasonable performance at the top-line across its core portfolio in Q3 FY22, the stock failed to attract substantial buying volume. A central theme from the previous publication comes to mind. Last time, we noted: "Now with the Converge overhang settled, ATRC is at a turning point. However, it needs to extend its tentacles outside of ablation and diversify its top line with continued performance in its AtriClip platform, and recently, minimally invasive surgical instruments ("MIS") segment. Moreover, data from its operating performance suggests it has to overcome numerous idiosyncratic headwinds. Investors must ask themselves if they are willing to pay 5x forward sales for a period of impeding losses at or below the bottom line."

The overarching question still remains in situ, and extends to investor positioning in FY23. We believe ATRC still has a ways to go in order to see it re-rate to previous highs. Net-net, we continue to rate ATRC a hold for now.

Exhibit 1. ATRC weekly price action, with 2x attempted rallies rejected at each attempt.

{kind=link}

Q3 numbers an improvement, price response still mute

If we first turn to the company's latest earnings , we'd note there were pockets of growth exhibited throughout ARTC's core portfolio. Despite this, the price response for ATRC's stock was fairly muted, indicating that investors were expecting more from the company. Nevertheless, there were several talking points worth mentioning. To name a few:

- We saw that ATRC achieved revenue of $83.2mm, demonstrating growth of approximately 18% from a strong comps period in Q3 FY21. Specifically, the EPi-Sense product in the US saw a YoY increase in revenue of 12%, as well as a 300bps increase sequentially. In addition, the pain management franchise experienced reasonable growth, with the Cryo-Nerve Block therapy proving to be the fastest-growing segment. The therapy saw a 300bps increase in sequential revenue and looks to have gained leverage with the pace of new accounts, with over 500 accounts year-to-date as reported by management on the Q3 earnings call.

- The cryoSPHERE probe also saw impressive growth, with volumes increasing by 68% YoY. In the open ablation business, growth of 20% was recorded in the quarter, with half of this upside attributed to procedure growth and the other half being due to an increase in pricing for the EnCompass Clamp.

- The appendage management business in the US saw a YoY increase in revenue of 18%. Overall, minimally invasive ablation sales reached $10.1mm, a 90bps increase from the previous year.

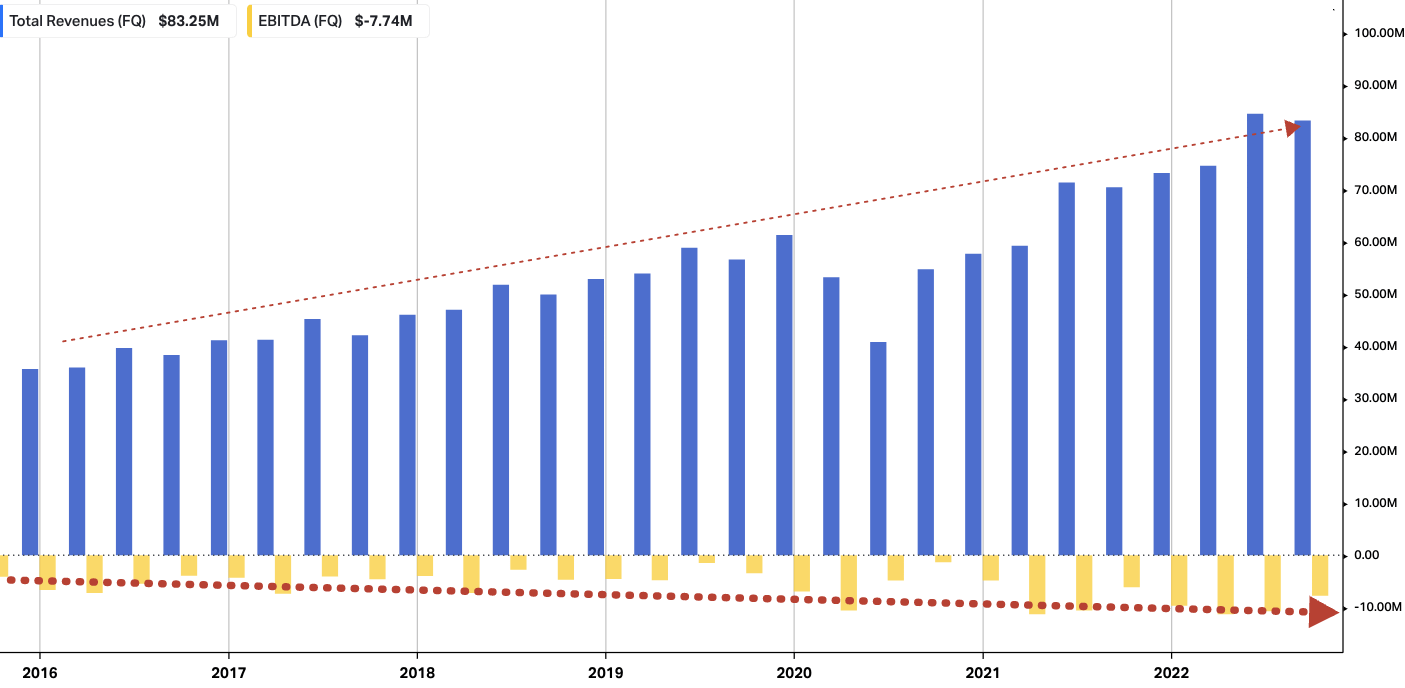

You can see the divergence in ATRC's top-line to operating level results in the chart below. Whilst revenue continues to increase at a steady clip, core EBITDA continues to navigate south. The question then turns to whether investors will reward this kind of setup looking ahead, with the suite of macroeconomic headwinds currently plaguing equity markets. Our best estimation is that they won't, given the selloff in ATRC this year to date.

Exhibit 2. ATRC quarterly operating walk-through, FY16-date. Note the divergence in revenue to core EBITDA. Question - will investors reward this looking ahead?

Data: HBI, Refinitiv Eikon, Koyfin

{kind=link}

Key markets recognized reasonable uplift for ATRC in Q3

Geographically, we noted that US revenue came in to $69.8mm, a 21.3% YoY increase. U.S. open ablation product sales saw a 20.5% increase over the previous year, while sales of appendage management products reached $27.6mm, a 18% uptick on Q3 FY21. Internationally, ATRC recorded revenue of $13.4mm, representing a 4.2% increase on a reported basis, and a 13.5% increase in constant currency terms. Overall, international markets were driven by accelerated uptake of AtriClip devices, flowing to a 19.5% YoY increase in appendage management revenue.

European sales made up $7.3mm of this total, driven by increased activity in the UK and other markets, but offset by unfavourable exchange rates and slowed activity in the Netherlands and Germany. Asia and other international markets contributed $6.1mm in international sales, with notable strength in Australia and Japan, partially offset by activity in China in the previous year.

Moving down the P&L, ATRC's Q3 OpEx, it is worth noting that, in Q3 FY21', the company recognized a credit of $189.9mm due to a change in the fair value of contingent consideration, which was partially offset by an $82.3mm intangible asset impairment charge for the IPR&D asset related to the aMAZE trial . However, even when these items are excluded, OpEx increased 18.4% YoY to $72.4mm by Q3 FY22. Consequently, it booked a quarterly operating loss of $10.7mm.

The primary factor contributing to this increase in organic OpEx was a 34% YoY increase in R&D investment to $15.2mm, whilst it lost ~14.8% of leverage at the SG&A line. Even still, if we were to capitalize the R&D investment as an intangible onto the balance sheet, the operating income pulls into a narrow $4.45mm for the quarter. It brought this down to a GAAP net loss of $0.27 per share, well below the EPS of $2.15 the year prior.

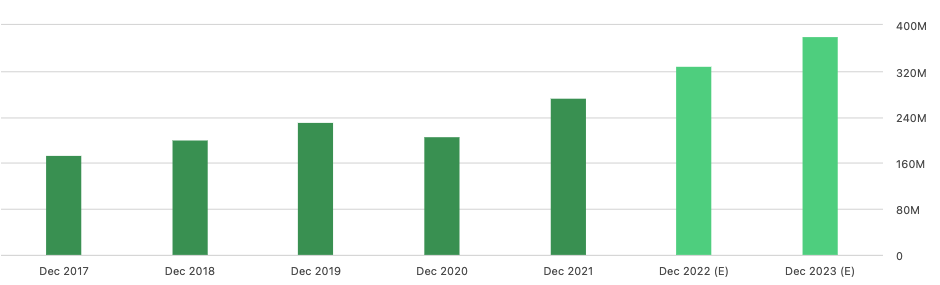

As we look to the FY22 full-year results, ATRC is forecasting annual revenue in the range of $328mm-$333mm, calling for YoY growth of ~20%-21%. The growth assumptions stem from the earnings momentum exhibited at the tail end of the year. With regard to Q4 estimates, the EnCompass launch is anticipated to drive positive growth in U.S. open ablation revenue. We'd also note that, in terms of adjusted EBITDA, the company projects a loss of approximately $4mm for FY22, pulling down to an adjusted loss per share of ~$1.10-$1.12. You'll see below that consensus revenue estimates agree with ATRC management, which could be a catalyst to share growth. However, we return to our previous question - will investors actually reward the top-line growth, without the corresponding increase in operating income and EPS?

Exhibit 3. Consensus revenue estimates point to strong revenue growth in FY23-24'

Data: Seeking Alpha. ATRC, see: "Revenue"

{kind=link}

Recent Developments for ATRC

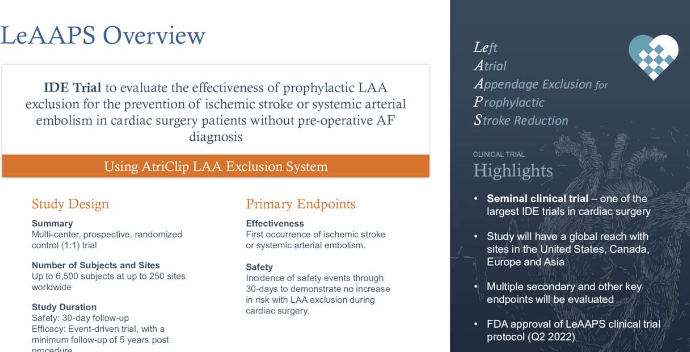

ATRC is also investigating an extended application for its AtriClip platform via the LeAAPS clinical trial. The trial will investigate the prophylactic use of AtriClip devices for cerebrovascular incident ("CVI", otherwise "stroke") reduction in cardiac surgery patients without a pre-operative atrial fibrillation ("AF") diagnosis. Specifically, it will examine the safety and effectiveness of performing left atrial appendage occlusion ("LAAO") on patients at high risk for AF who are undergoing cardiac surgery.

Exhibit 4. LeAAPS trial - longitudinal study, designed for 8-9 years study length.

Data: ATRC Investor Presentation, August 2022.

{kind=link}

This study builds upon the findings of LAAOS III , in which investigators studied the use of surgical LAAO in patients undergoing valve or coronary artery bypass graft surgery with documented AF or atrial flutter and a CHA2DS2-VASc score of 2 or higher [indicating an increased risk of stroke]. The international, multi-center trial, which enrolled 4,811 patients, found that LAAO reduced the risk of stroke or systemic embolism, the primary endpoint, by 33% overall in patients with AF or atrial flutter. After the first 30 days following the procedure, patients who received LAAO were 42% less likely to experience a stroke over long-term follow-up compared to those who did not receive LAAO.

Therefore, the LeAAPS study will focus on understanding the benefits of this strategy in patients who do not have documented AF, but are at risk for stroke. The trial aims to enroll up to 6,500 patients at approximately 300 centers in the US, Canada, and Europe, with follow-up occurring every 6 months. One arm will receive the clip, and the other won't. The push to get the study underway came after ATRC completed a feasibility study, which showed a dramatic improvement in stroke rate in non-AF patients at 1 year in the feasibility study. In total, ATRC anticipates this to be an 8-9 year trial overall. More details on the study can be found from the transcripts of ATRC's talk at Morgan Stanley from September 2022.

Valuation

In the absence of earnings and profitability, we've turned to a combination of technical studies, market positioning and quant factor gradings to gauge price visibility looking ahead.

Last time we saw the stock was priced at ~5x sales, whereas it trades at ~6x forward sales at the time of writing. Note, this is ~50% above the sector median.

You'll see below that we have downside targets to $36.5 from point and figure analysis. These are prudent studies to use given they remove the noise of time, and just look at price action. This is the second $36 target thrown off in 2022 and therefore we are looking to this number more seriously.

You'll see the stock is trading beneath a series of inner and outer resistance lines on this chart as well.

Exhibit 5. Downside targets to $36.5.

Data: Updata

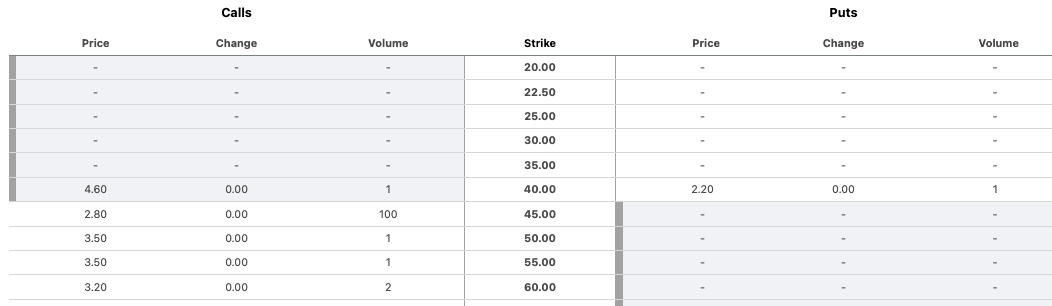

In terms of market positioning, we checked the ATRC options chain for contracts due for expiry in January 2023.

You'll see that the bulk of volume is centred on calls at the $45 mark, a tick above the current market price. There's some interest up to $60, however not enough to suggest a large position at this level. Nevertheless, investors look to be confident at the $45 price interval.

Exhibit 6. ATRC options chain for January 2023. The bulk of volume is centred on calls at $45 on the price ladder [Note: only calls and puts that are currently in the money are shown].

Data: Seeking Alpha, ATRC, see: "Options"

{kind=link}

Hence, we've got a price range from technicals and market positioning of $36-$45. In either sense, there's minimal upside from either number based on the current market price.

This sentiment is supported by objectively by Seeking Alpha's quantitative factor grading, that rates the stock lowly in terms of valuation. This supports a neutral view on ATRC in our opinion, given the fact there's three separate inputs suggesting the same.

Exhibit 7. ATRC quantitative factor grading suggesting the stock is correctly valued at its current valuation.

Data: Seeking Alpha ATRC quote page

In short

Despite ATRC building momentum around its core portfolio and extending applicability of its clip segment, we are still cautious on this name for now. Corporate fundamentals are increasingly important at present, as the distribution of potential outcomes for the global economy are leaning to a recession at baseline. Growth at the top-line might not be enough to see ATRC re-rate to the upside in our opinion. By estimation, it may be a while before we see investors return to unprofitable med-tech names en masse, especially as discount rates increase and global liquidity dries up. Further, with noted headwinds for ATRC mentioned in our previous publication, combined with the company's lack of profitability, add to this sentiment. We therefore reiterate our hold call on ATRC.

For further details see:

AtriCure: Despite Reasonable Top-Line Growth, No Change To Hold Thesis