ICUI - Atrion Corporation: Too Pricey For Such Limited Growth

Summary

- Atrion Corporation has done well from a sales perspective very recently, but its overall financial performance in recent years has been disappointing.

- This is especially true of bottom line results that have shown no real growth.

- The firm is a stable operator that should be fine in the long run, but the stock is pricey for a company with limited growth.

One thing that I've come to notice is that many investors place a great deal of emphasis on whether or not a company is growing. Ideally, you do want to buy stock in a firm that is expanding. This adds value to the company in most cases, and it reduces downside should we eventually experience a decline in fortunes. On the other hand, there are times when purchasing stock in a company that lacks real growth can and does make sense. But when those scenarios do occur, it must be because shares of the business are trading at fundamentally attractive levels. To pair up the traits of an expensive stock with one that is for a business that's not really growing is a recipe for pain in the long run. Or at a minimum, it's a sign of mediocre returns down the road. One company that fits this description, in my opinion, is Atrion Corporation ( ATRI ). Although the company has experienced a little bit of growth recently, its overall track record, combined with how shares are priced at the moment, leaves a lot to complain about.

Not a great play today

According to the management team at Atrion, the company operates as a developer and manufacturer of products that center around a variety of, for the most part, medical causes. Examples include fluid delivery, cardiovascular health, and ophthalmic applications. Using data from the company's 2022 fiscal year, we can see that 46% of its revenue came from the fluid delivery products that it sells. These include valves designed to precisely fill, hold, and release controlled amounts of fluids or gases on demand for use in intubation, intravenous, catheter, and other applications. Customers in the anesthesia and oncology fields are its primary target.

The company also produces and sells cardiovascular products. These all center around the company's own proprietary open-heart surgery system called the Myocardial Protection System that helps to deliver essential fluids and medications to the heart. It also mixes critical drugs, and it controls the temperature and pressure of said fluids and medications. Other cardiovascular products that the company sells include cardiac surgery vacuum relief valves, inflation devices for balloon catheter dilation, and more. During the firm's 2022 fiscal year, this segment accounted for 37% of the company's revenue. And finally, we have the ophthalmic products that the company produces. These largely consist of specialized medical devices that disinfect contact lenses, as well as balloon catheters for both adults and children. Only 3% of the company's revenue came from these products in 2022. Another 14% of revenue comes from miscellaneous medical and non-medical products that the company produces. Examples here include inflation systems and valves that are used in marine and aviation safety products. They also produce components used in inflatable survival products and structures, and so much more.

{kind=link}

Between 2018 and 2021, the financial picture of Atrion was pretty unexciting. Revenue remained in a fairly narrow range of between $147.6 million and $165 million. It was really only in the 2022 fiscal year that we saw some improvement on this front. That year, sales came in at $183.5 million. The biggest growth for the company between 2021 and 2022 fell under the cardiovascular category. Sales here jumped 18.8% from $56.9 million to $67.6 million. Unfortunately, management did not provide as much detail as I would have liked as to why sales increased so much. But we do know that the company continues to benefit from the latest generation of its cardiovascular system, called MPS3, which was released in 2020.

On the bottom line, the picture for the company has looked very similar to what it has on the top line. The only difference is that 2022 did not see a surge in profitability. Instead, in the five years ending in 2022, net income ranged from a low point of $32.1 million and a high point of $36.8 million. In 2022, the number was $35 million even. Operating cash flow, meanwhile, has actually experienced a downtrend. In each of the past five years, the metric fell lower than it was the year before. Ultimately, it declined from $43.2 million to $28.8 million over the five-year window covered. If we adjust for changes in working capital, that decline disappears. Instead, we are left with a narrow range once again, with the metric hovering between $43.7 million and $50.7 million. And finally, when it comes to EBITDA, the same situation is true. Over the five-year window covered, the metric ranged between a low point of $47.3 million and a high point of $53.5 million. The good news is that the high point was actually in 2022.

{kind=link}

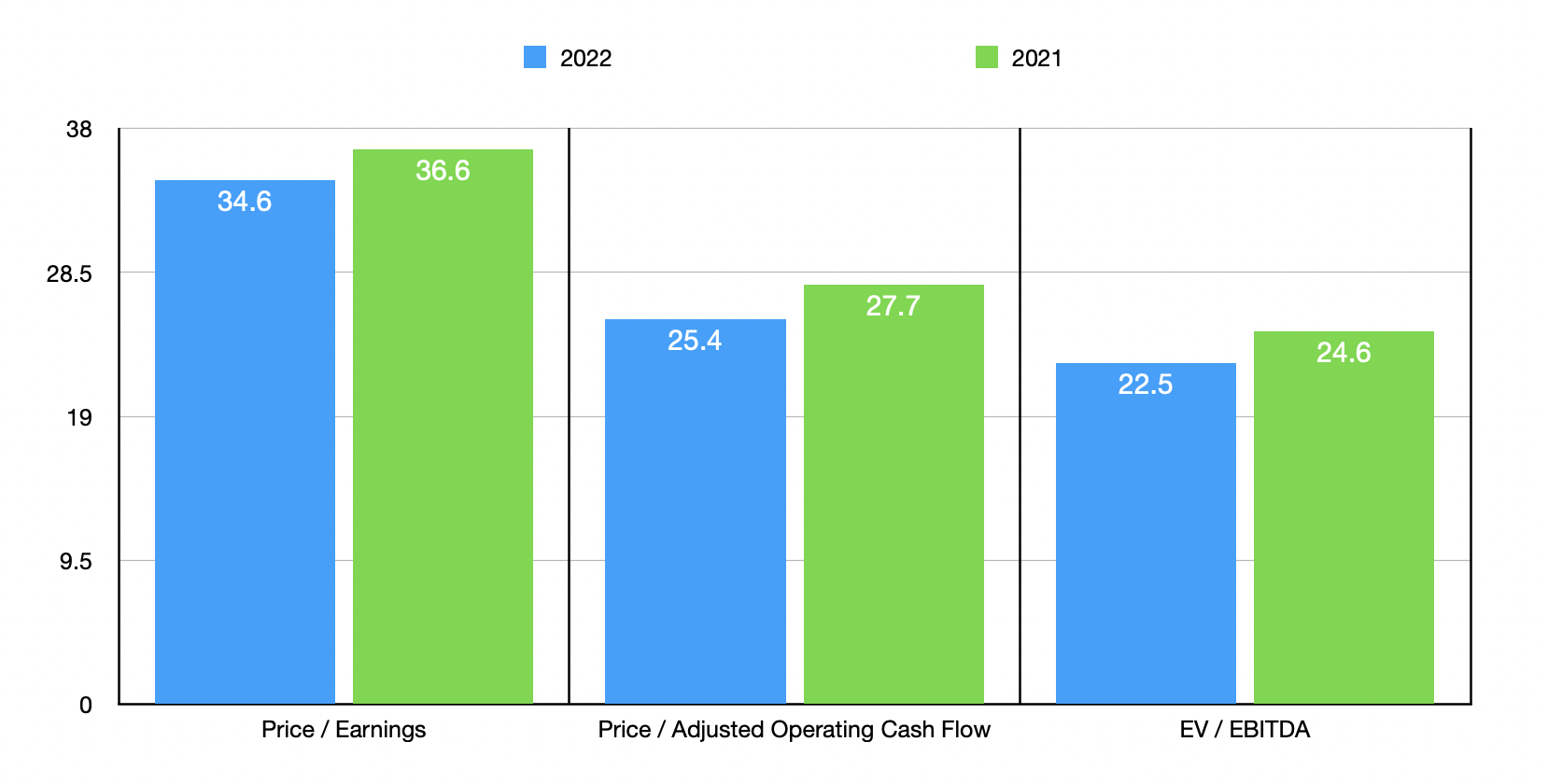

Management has not really provided much in the way of guidance for 2023. Clearly, sales have finally started to show some growth. But bottom line results aren't keeping up. This would be fine for an investment prospect if the company was trading at really low levels. But sadly, that's not the case. Using data from 2022, the company is trading at a price-to-earnings multiple of 34.6. The price to adjusted operating cash flow multiple is 25.4, while the EV to EBITDA multiple comes in only slightly lower at 22.5. The good side to this is that, as the chart above illustrates, the pricing is better than if we were to use data from 2021. But in general, this is the kind of pricing that you expect from a growth business, not one that's failing to expand. As part of my analysis, I did compare the company to five similar firms. On a price-to-earnings basis, these companies range from a low of 19.3 to a high of 360.7. Using the price to operating cash flow approach, the range was from 12.5 to 230.9. And finally, using the EV to EBITDA approach, we get a range of between 9.5 and 30.8. In all three scenarios, two of the five firms were cheaper than Atrion.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Atrion Corporation |

| 34.6 |

| 25.4 |

| 22.5 |

| Avanos Medical ( AVNS ) |

| 26.9 |

| 14.7 |

| 11.8 |

| FIGS, Inc. ( FIGS ) |

| 50.1 |

| 230.9 |

| 25.8 |

| Merit Medical Systems ( MMSI ) |

| 54.2 |

| 35.5 |

| 23.1 |

| Dentsply Sirona ( XRAY ) |

| 19.3 |

| 12.5 |

| 9.5 |

| ICU Medical ( ICUI ) |

| 360.7 |

| 186.6 |

| 30.8 |

Takeaway

Unique companies like this that occupy a particular niche intrigue me and, in general, I want to be bullish about them. On the good side, we know that the business has at least been stable, even throughout the COVID-19 pandemic. That counts for something, as does the fact that shares look to be trading around the middle point of the range of what similar businesses are trading for. But beyond that, there isn't much here to enjoy. Given how pricey shares are and the absence of real growth, particularly on the bottom line, I do believe that the company only really makes for a 'hold' candidate at best at this time. If shares were any pricier than they are, especially relative to similar firms, I would probably take a bearish stance.

For further details see:

Atrion Corporation: Too Pricey For Such Limited Growth