ATRI - Atrion: Inventory Backups Capital Productivity Reduce Scope For Upside (Rating Downgrade)

2023-08-15 10:51:35 ET

Summary

- Healthcare equities are becoming attractive again after a selloff, with the sector converging to the upside.

- Atrion Corporation has missed the bid in July/August, challenged by unfavorable economic characteristics in my view.

- ATRI faces potential challenges in redeploying capital and overcoming supply and inventory issues.

- Net-net, revise to hold.

Investment briefing

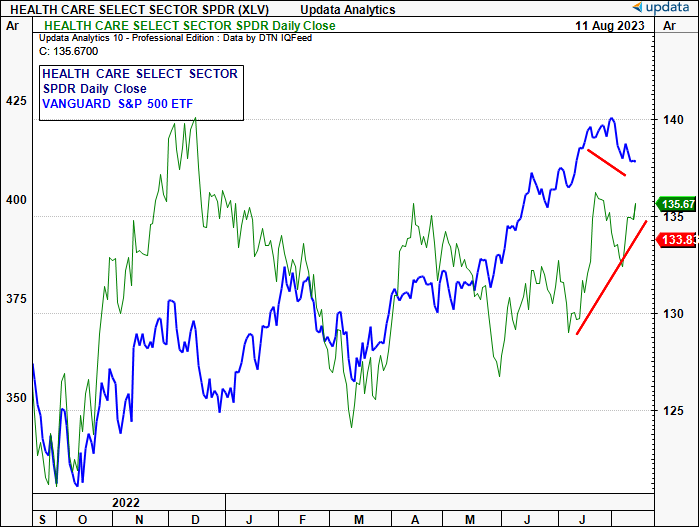

After a brief but sharp selloff rolling into H2 FY'23, listed healthcare equities are again catching a bid. The sector had diverged from the U.S. equity benchmark during Q2 with a fierce consolidation, but started its reversal in a stair-like pattern over these past 2 months [Figure 1]. With the SPY rolling over, healthcare companies are once again attractive in my view, presently converging to the upside.

Figure 1.

{kind=link}

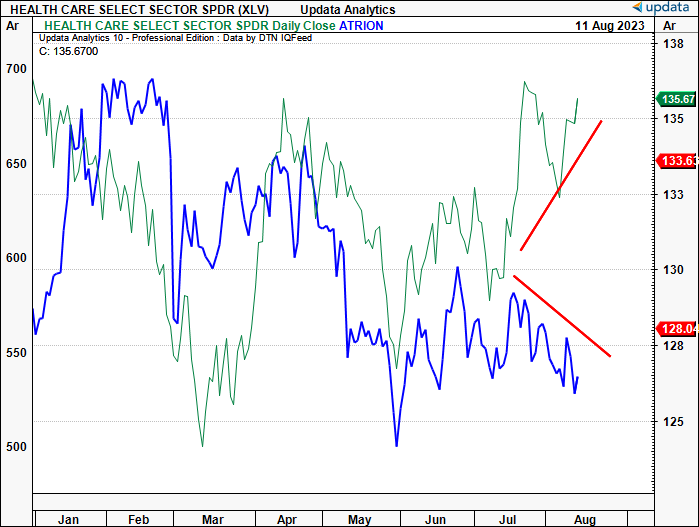

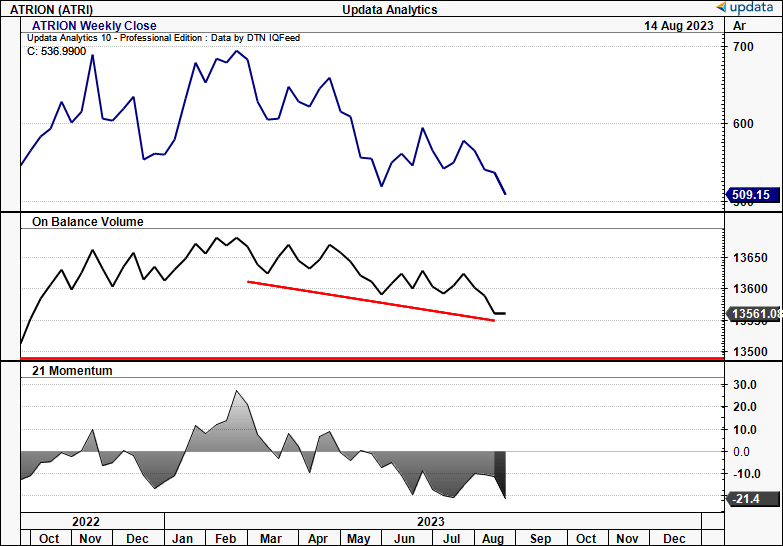

The same can't be said for Atrion Corporation ( ATRI ), having missed the bid during July/August [Figure 2]. My ATRI rating is now 12% out of the money since my September '22 publication , and flat from the May publication.

The ATRI investment debate is now balanced in my informed opinion, and in this report, I'll run through my reasoning behind the revised rating from buy to hold. ATRI is undoubtedly a company that has a propensity to adapt and evolve. However, just like the diner at the restaurant judging her chef's performance, we can only go by the dish we have in front of us—not what could be. ATRI's numbers are telling of a company that needs to 1) redeploy new capital commitments at higher rates of return, and 2) overcome supply and inventory challenges in its end-markets.

Net-net, I revise my rating on ATRI to a hold for the reasons outlined in this report.

Figure 2.

{kind=link}

Critical facts to revised thesis

The changes to the critical investment facts are driven by fundamental, economic, sentimental and value forces in my opinion. First in line are the company's latest numbers, and what this spells for ATRI's ability to create value for shareholders in the medium term. Second are the economic characteristics of the business and how these have changed over time, and finally, what this means for the perception of value in ATRI's stock.

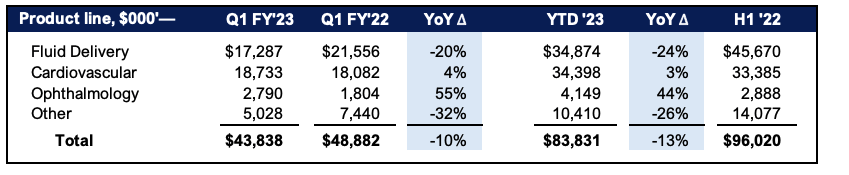

1. Q2 FY'23 insights

Starting with the Q2 earnings, revenues were down ~10% YoY to $43.8mm, led by a 20% wind-back in the fluid delivery segment. For the YTD, ATRI is ~24% behind where it was this time last year in fluid delivery sales. It did $18.7mm of business in its cardiovascular division, up 4% YoY and 3% this YTD. It pulled this to $7.4mm in operating income, down 32% YoY, on earnings of $3.73/share (vs. $5.21 last year).

Figure 3.

{kind=link}

Underperformance across the firm's core segments relates to its customer purchasing patterns. Recall in FY'22, the supply-chain issues that ensued as Covid-19 restrictions were wound back, amid other causes. In response, hospitals and healthcare providers overstocked on critical components to avoid facing any shortages.

The issue being that:

- The supply-chain woes were relatively short-lived for hospitals, and

- Customers are now heavily overstocked. To the point where many are even de-stocking, and more importantly to ATRI's case, slowing the pace of ordering, let alone order growth.

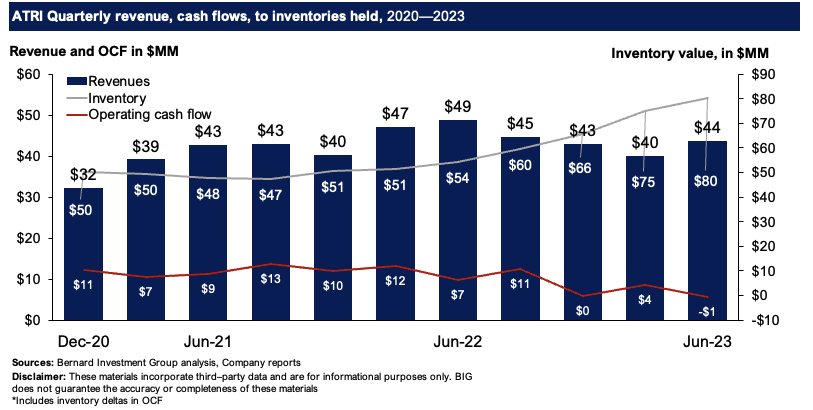

The quarterly divergence in inventories, revenues, and cash receipts from ATRI's customers is seen in Figure 4. Note the sharp divergence from Q3 FY'22, when most of the supply chain issues began to resolve, leaving ATRI holding ~$80mm on the balance sheet as of Q2 FY'23. As a result, the company only collected $4mm in OCF in Q1 this year and realized a cash outflow of $1mm in Q2. This, from peak quarterly revenues of $49mm in Q2 FY'22 (over the last 2.5 years).

The customer de-stocking was well recognized by management:

We continued to experience disappointing results with declines of 10% in revenues and 33% in operating income as customers continued to reduce their inventories...[w]e are proactively undertaking a number of initiatives to improve our performance" —David Battat, Atrion Corp. CEO

In my opinion, this could play out for the remainder of FY'23 and presents a critical risk to the company's intrinsic value rating higher. Looking past FY'23, I'm sure ATRI will balance out the net effects, but allocating today comes at the opportunity cost of higher conviction names in my coverage universe.

Figure 4.

{kind=link}

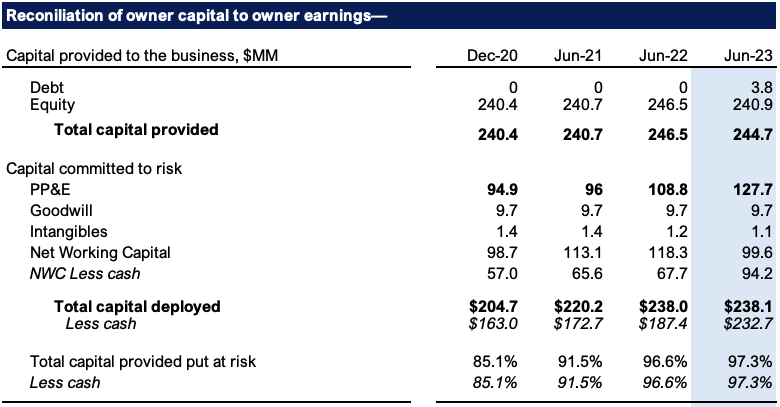

2. Capital deployment into growth operations

The economic characteristics of ATRI's business operations show a diminishing intrinsic value for the discernible future in my opinion.

It has committed an additional $23mm as growth capital into the business since June FY'21. Of the investor capital provided to the business (basically all equity), it has deployed ~97% at risk to operations, with the remainder recycled back as dividends to shareholders. It had $238mm at risk that was needed to run the business in Q2, of which ~$99mm is tied up in NWC—predominantly inventory—and $127mm in its manufacturing facilities, including its facility expansion in Florida.

One point is that just 1.76mm of common equity shares makes up the capitalization of $944mm as I write. Hence, per-share metrics are positive—$15.40 in trailing EPS, $136 in book value per share.

Figure 5.

{kind=link}

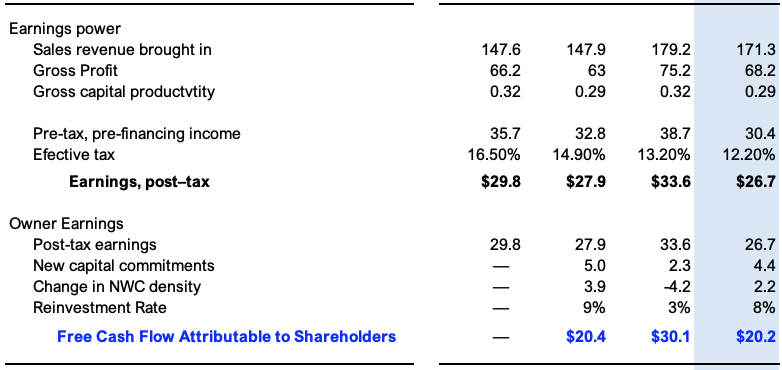

But these are poor metrics to value ATRI by in my view. The company books revenues and profits from the sale of its products to hospitals etc.; thus, it's a function of the unit economics ratcheting higher. It's the post-tax margins and cash flow ATRI can spin off to its shareholders that matter most to me.

To that effect, we've had negligible movement in earnings and the free cash attributable to shareholders these past 2 years (TTM values). The owner earnings of the business—those left over after taxes and allowance for reinvestment—are flat at $20mm from Q2 FY'21—'23 (in the TTM). Similarly, it has only reinvested ~5% of earnings on average during this time, despite expanding capacity in Florida, and beefing up inventory values. The company is basically debt-free (~100% equity financed), hence this is a good number to measure ATRI's changes in value.

Figure 6.

{kind=link}

Explanations for the flat earnings growth (and lack of value-add) are as follows:

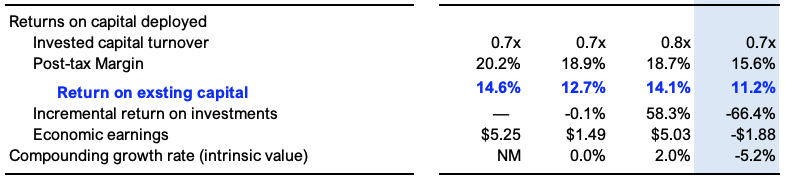

- Post-tax margins have tightened ~300bps YoY and ~500bps from 2021 to 15.6% (TTM values), thereby crimping the profits generated off ATRI's invested capital [inventory included].

- ATRI doesn't enjoy capital turnover benefits thus, all capacity enhancements have only broadened the capital requirements of the business without adding additional profits [not yet, anyway].

- The returns produced on capital ATRI has deployed into the business from its equity holders have shaved ~300bps off its ~14% average last quarter.

Here's where the business economics run into some trouble. Benchmarking the company's investment returns vs. the long-term market return on capital (c.12% here), the erosion of value is clear to see in the scenario below,

Presuming no future earnings growth , in June FY'22, it printed $33.6mm in TTM earnings after tax from $238mm employed in the business (14.1% return on capital). This is 200bps above the hurdle rate of 12%, thus a return above the capital charge ($33.6/0.12 = ~$280mm > $238mm). This created shareholder value, producing economic earnings—those earnings above the cost of capital—of $5.03mm ( [0.141–0.12] x 238 = $5.03).

Contrast this to last quarter:

- Still $238mm deployed at risk in operations, producing $26.7mm in profit after tax

- 11.2% return on capital employed (TTM figures once again)

- This is below the hurdle rate (11.2% — 12% = -0.8%).

- Hence, this missed the capital charge required to produce these profits, eroding shareholder value ($26.7/0.12 = $222mm < $238mm).

- Note: This is called the $1 test, and it can be employed as an efficient measure of a company's earnings power.

If an investment doesn't produce what it costs to make in the first place, simple logic tells us there's no value created. Case in point here. The 12% hurdle rate is relevant here because investors can reasonably expect this as a long-term return by simply riding the benchmark. Hence, if I'm going to give even 1 cent to any company in market value, I want it compounding capital at obscene rates of return, at multiples above c.12%.

Figure 7.

{kind=link}

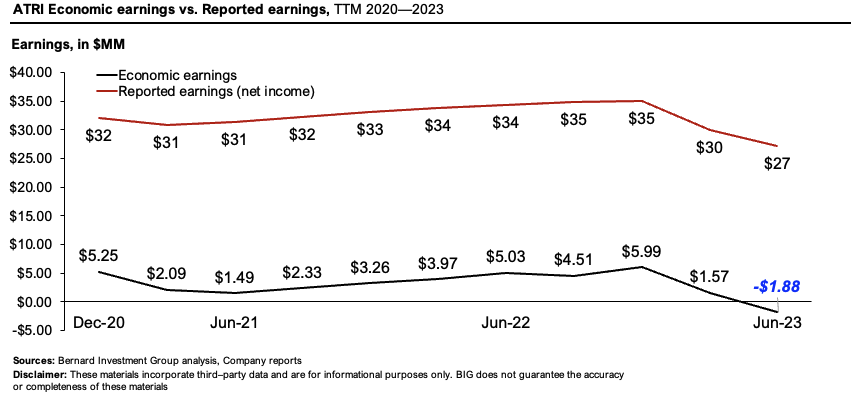

The net effect is observed below, presenting the economic earnings for each period on a rolling TTM basis. Note the spread in reported earnings vs. economic profits, with ATRI generating an economic loss last quarter of $1.88mm. Thus, no value-add, and the market recognized this in my opinion. Economic earnings, including the spread of ROIC to cost of capital, are well accepted by the market as a key driver of value in mature companies.

Figure 8.

{kind=link}

Valuation and conclusion

The convergence of on-balance volume to ATRI's market value was discussed at lengths in the last publication. This convergence appears to have rolled over and investors look to have been net sellers since April [Figure 9]. To me, this suggests demand is low. Not to mention, with just 1.76mm shares outstanding, liquidity in the order book may potentially be an issue.

Figure 9.

{kind=link}

ATRI is selling at 35x trailing earnings and 31x EBITDA, on ~$4 of net asset value for every $1 in market value. These are pricey in my view—especially given the economic factors outlined earlier.

So, you might think ATRI could be trading fair with the recent pullback in market value. But it would appear ATRI is not relatively 'cheap', even at these uncertain market prices, with investor demand (outlined earlier) further exemplifying this sentiment.

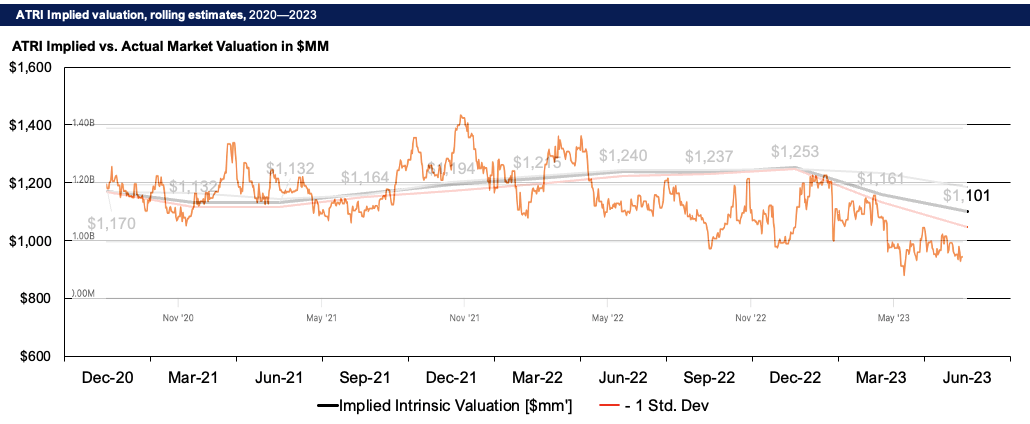

My readers will know I value the implied market value of a firm's equity stock as the rolling function of its ROIC and reinvestment rate. Both are tight in ATRI's case and have been narrow for some time. The $8.60/share forward dividend is indeed recognized here—but at just 1.6% forward yield, mind you. Not enough to offset other headwinds outlined.

Performing the calculus gets me to $1.1Bn in market value for ATRI, or $625/share, 16% upside potential as I write. This sits outside of a 20% margin of safety and thus doesn't qualify as a buy in my view. The market looks to have been a fairly good judge of the implied intrinsic value these 3 years as well. In my previous publication in May, the stock looked undervalued, but recent developments have confirmed the market's view, not my own. This supports a neutral view.

Figure 10.

Note: The orange market cap line is retrieved from Seeking Alpha. and superimposed over the implied valuation line. Hence the slightly faded image (Sources: BIG Insights, Seeking Alpha)

{kind=link}

In short, the investment debate is best summed up by the following data points in my opinion:

- ATRI faces inventory backlog and customer supply headwinds, given most of its customers are de-stocking inventories and slowing the pace of orders

- It has upped capacity at its facilities, but post-tax margins on existing sales are tightening, therefore tightening the profitability of its investment capital

- These issues have fronted a re-rating to the downside in both intrinsic value and market value from my estimations

- This is clamping the amount of cash it can spin off to its shareholders, dividends included

- These points aren't conducive to investors paying higher market values to buy the company in the medium-term.

Net-net, I revise my rating on ATRI to hold, noting the company trades ~1 standard deviation behind my estimates of fair value.

For further details see:

Atrion: Inventory Backups, Capital Productivity Reduce Scope For Upside (Rating Downgrade)