ATRI - Atrion: Trading Below Value Volatility Presents Mispricings

2023-05-19 08:01:28 ET

Summary

- Atrion Corporation has traded within a wide range over the past 6 months with little-to-no major catalysts.

- There appear to be market-generated reasons for this, rather than fundamental changes.

- The company's economic model is sound, and it throws off plenty of cash to shareholders, relative to turnover.

- Net-net, the volatility is a concern, but the empirical and fundamental data supports ATRI as a long-term buy in my estimation.

Investment Summary

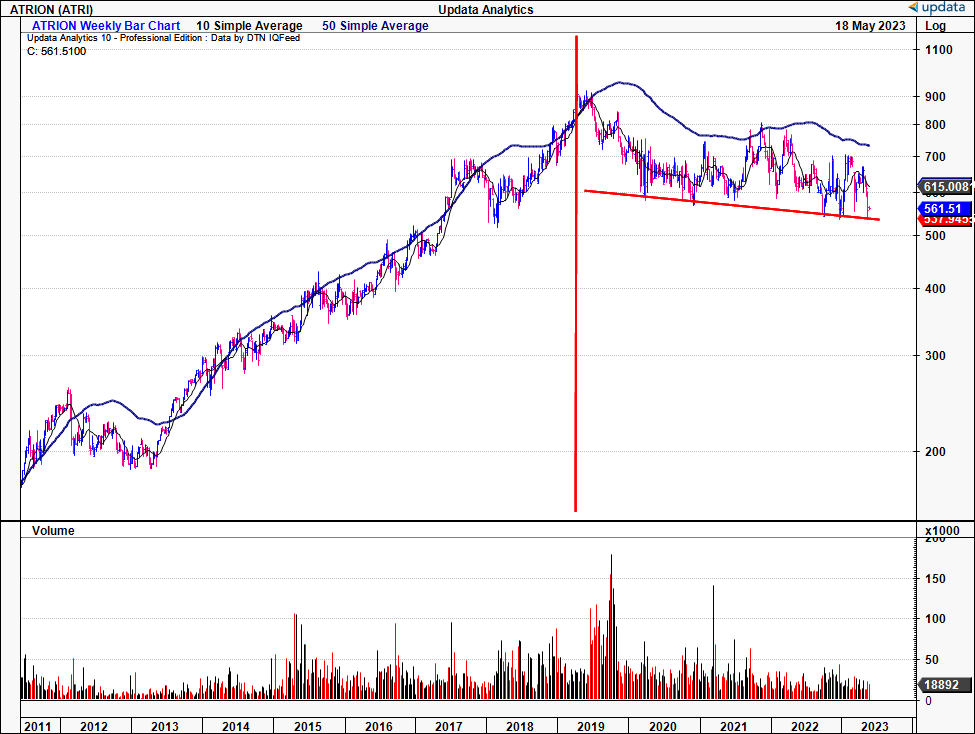

The October FY'22 rally in broad equities has rewarded high-beta names. This is great for popular tickers that attract lofty market premiums, at often psychotic valuations. Looking back over the past decade, owning stock of Atrion Corporation ( ATRI ) was an absolute fairy tale, up until April 2019 back in the Stone Age when it ran from $214 in 2013 to an all-time high of $909.

The pandemic era was unkind to ATRI's market valuation, driving gut-wrenching volatility in +/- $100 per share swings in mere weeks. These trends have continued to the present day, with the stock unable to catch a reasonable bid to extend price action in any directional bias.

Figure 1

{kind=link}

I had the privilege to own ATRI throughout some of this upside from 2015-'19, period but haven't enjoyed the ride the past 2-3 years. Check my last two publications on the name here:

- F air and reasonably priced for resiliency premium

- Exposure to defensive healthcare

You've got the $8.60 per share dividend that's increased for the past 18 years, plus the buyback program that's been in place since 2015. But the absolute pandemonium in its market value has been concerning, and potentially damaging for those keeping tight stops on their positions. Despite this, I believe ATRI is one for the long-term and if it can wade through the current market sludge I believe there's scope for the stock to trade back to the $660-$670 range. Net-net, reiterate buy.

Key facts in ATRI investment debate

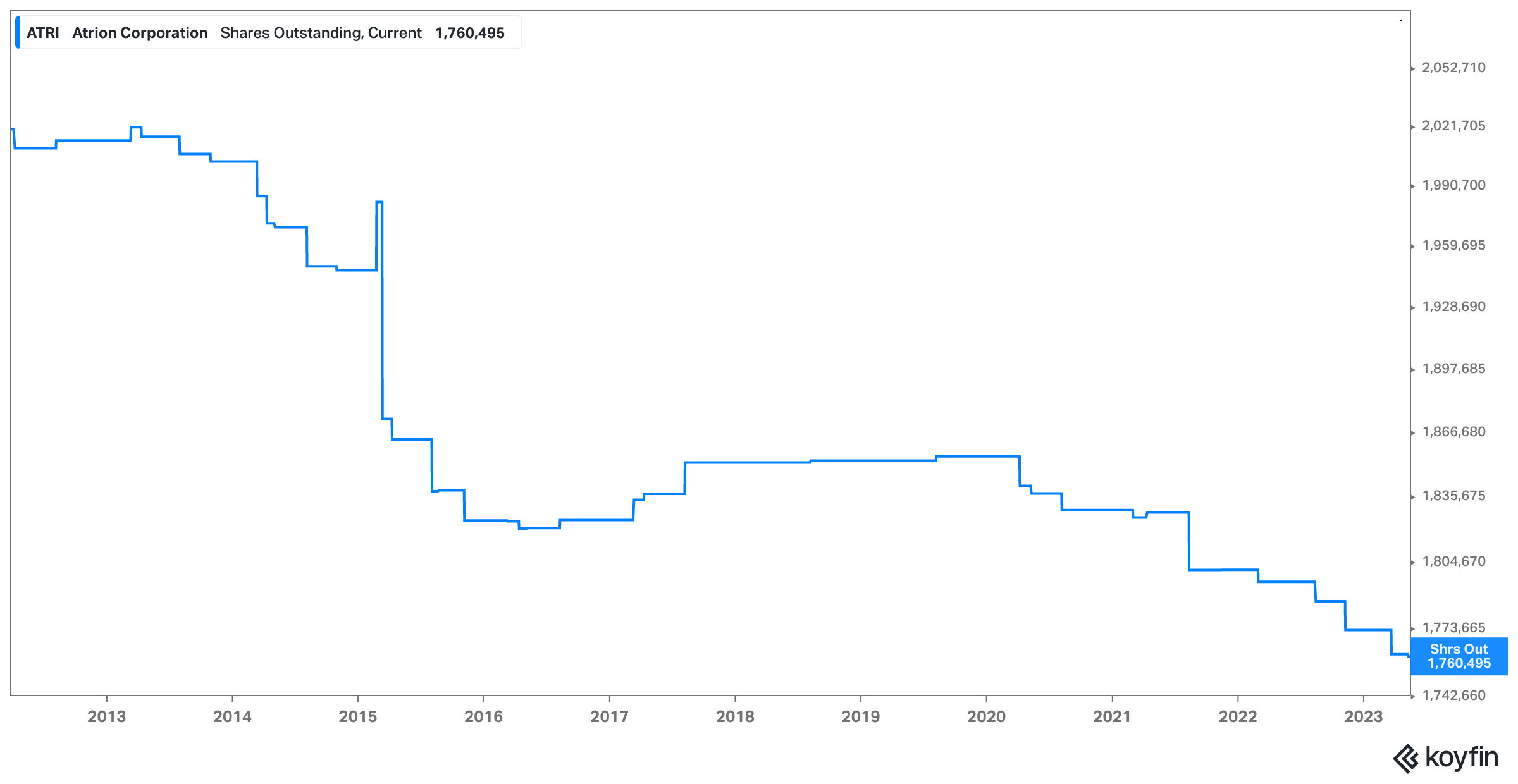

Eyes are immediately drawn to the psychotic volatility in ATRI's share price over the past 6-12 months. Nothing much has changed fundamentally, plus it's difficult to obtain granularity from the history of the order book. What is clear, is the 12.7% reduction in the company's share float, to just 1.76mm shares outstanding. Obviously, this creates liquidity dilemmas and muddies up price visibility due to the reduced strength of the order book. That in mind, it is unlikely that:

a). Orders (buys, sells) will get filled efficiently at various points along the price ladder. Instead, investors will have to accept the best offer either way; or

b). Market valuation will track intrinsic valuation/fundamentals. Although, this could also potentially aid in price discovery.

The Figure's 2 and 3 below track ATRI's share count and on-balance volume over the past decade and 15-months, respectively. Looking below, you can note the pace of repurchases increased from 2020-2023 after a flat period from 2016. Since 2020, the float has been reduced by another 93mm shares. Naturally, demand and supply mechanics come to mind, and my estimation is market activity on the punitive 1.76mm shares outstanding has something to do with the price swings we've observed of lately. Large, or cumulative buy orders can result in tremendous upside thanks to these market mechanics, by estimation.

Figure 2

{kind=link}

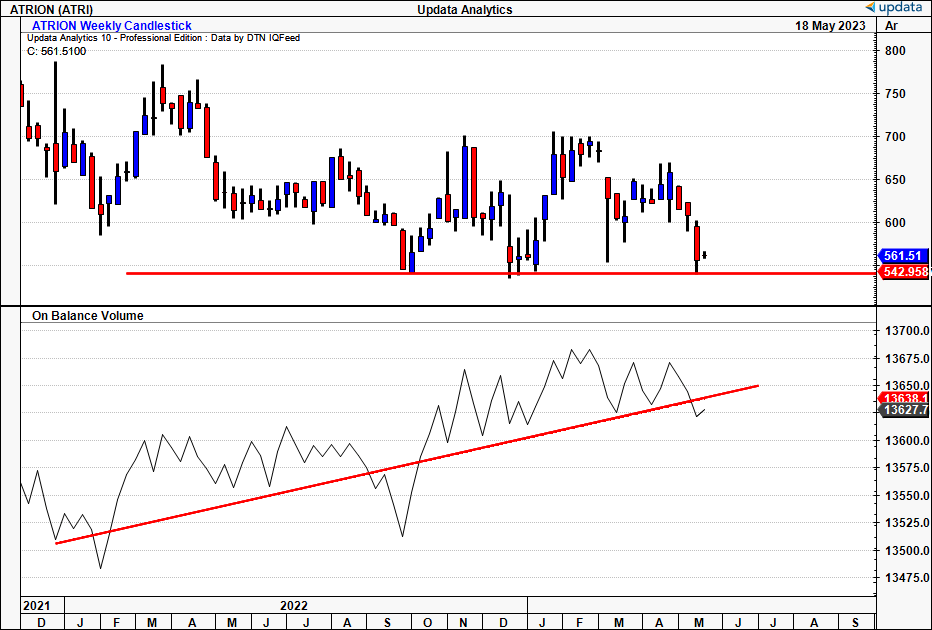

Zooming in on the last 12-15 months, whilst ATRI's stock has backed and filled into congestion, trading in a c.$250/share range, long-term demand has accelerated. You can see in Figure 3 this very trend in action. The on-balance volume, that measures buying/selling volume trends over a longer time frame, is wedging towards the price line. This gives insight into the behaviour of more committed investors.

This convergence should not be ignored. Tied with the price sensitivity to large or cumulative buying patterns, if investors are indeed building up longer-term positions in ATRI, this could potentially be an idiosyncratic factor that isn't yet priced into the stock price. I'd be watching the OBV indicator closely to observe further convergence.

Figure 3

{kind=link}

Aside from these isolated factors, there are fundamental drivers that I believe warrant serious consideration. You don't survive as a going concern since 1944, as ATRI has, without some form of competitive edge, quantified via the economic characteristics of the business. Fundamental equity managers looking for long-term capital appreciators might be first interested in ATRI. Plus, it is important to understand there's actually a strong set of investment criteria on show here. These could potentially see ATRI rate back to all-time highs if all goes unscathed. Here is my case:

- One, even after 79 years of existence, gross capital productivity is a substantial driver of value for ATRI's shareholders. As shareholders, owners of the business' operating capital, you'd be pleased to know the company's investments produces $0.25-$0.30 in gross margin for the capital that's been put to work. Here, the gross profitability is taken as the TTM gross profit scaled by total assets each quarter, to demonstrate the gross return ATRI produces on each $1 in assets. You can see this figure curling higher from 2021-date, with total assets now scaled back to 2020 range. This is a more capital light business that is still generating 25-30% gross profit from its productive assets, freeing up cash to distribute to shareholders.

Figure 4

Data: Author, ATRI 10-K's

- Two, ATRI clipped $40mm in quarterly revenues and pulled this down to $4.5mm in operating income and diluted earnings of $1.98 per share in Q1. Each of these are down YoY, spurred on by customer actions throughout the last 2 quarters. According to ATRi, "[s]everal customers unexpectedly pushed out deliveries of products citing concerns that a global economic slowdown is impacting the speed at which their inventories will be brought to appropriate levels" . Hence, these look to be one-time items, but rattled top-bottom line growth nonetheless. Thankfully, the impact hasn't flowed through to infect the profitability of the business. Looking back to Q3 2020, the after-tax operating earnings booked by ATRI on a rolling TTM basis outpaced the capital required to produce them. This is observed in Figure 5, where trailing NOPAT is taken as a function of the operating capital ATRI has put at risk (invested capital) to show the return on existing capital. As shown, it has remained in the double-digits over the past 2-years.

- The economic earnings produced on ATRI's investments has also maintained a positive spread above the 12% required rate of return the market seems to command before rewarding a firm with a higher valuation. Given the economic profitability, all of ATRI's growth is accretive to its valuation in my opinion, regardless of the daily marks on its market quote.

Figure 5

Data: Author, ATRI 10-K's

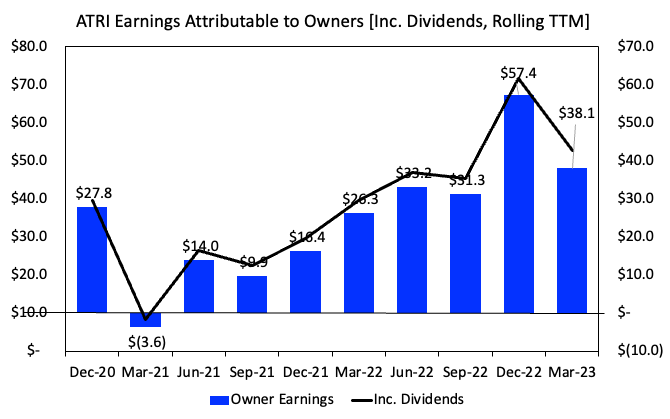

- Three, relative to the top-line, ATRI converts high percentages of free cash flow from revenue and spins this off to shareholders at an average 15% margin over the past 2-years (TTM basis). The earnings attributable to owners has grown from $28mm in Q3 FY'20 to $38mm last quarter, peaking at trailing $57mm in Q4 last year. Including dividends, ATRI spun off trailing $52mm to shareholders last quarter, 30% of TTM Q1 revenues. Combined, you're receiving $31.2 in owner earnings per share at a 5.5% earnings yield on these figures, really not bad numbers on a $565 share price in my opinion. However, it's the growth that's been most important - 174% growth in free cash to shareholders from Q2 FY'21 to Q1 FY'23. The cash ATRI's investors have received (ex-dividend) is calculated as the NOPAT less investments made each quarter, including changes in NWC, less reinvestment into future growth. Cumulatively, this is an additional $226mm in cash ATRI has thrown off to investors, $337mm including dividends ($226mm in FCF + $110mm in dividends = $337mm). Looking forward, my numbers have ATRI to do $40-$45mm in FY'23 NOPAT and this could throw off $55-$60mm in cash to shareholders, including dividends, if all goes well - $42/share and 31% YoY growth.

Figure 6

Note: Owner earnings (free cash to shareholders) is calculated as [NOPAT - investments - reinvestment] where investments is the periodic change in total capital invested, and reinvestment is the percentage of earnings reinvested back into the business for maintenance/future growth, as [Incremental Invested capital / TTM NOPAT] (Data: Author, ATRI SEC Filings)

{kind=link}

These factors outline the core tenets forming my long-term investment thesis on ATRI. These kind of business economics are attractive to me, and I believe the firm will continue growing the economic earnings to its owners into the coming years.

Valuation

On my FY'23 estimates of $45mm in NOPAT and $55-$60mm in earnings to shareholders I've got ATRI valued at a steady-state of $500mm, using a 12% discount rate ($60/0.12 = $500). Assuming no growth going forward, and using the $53mm in trailing owner earnings, we get to $441mm.

At the current market capitalization of $988mm, the market expects a present value $118mm for the company's future free cash flows at the 12% hurdle rate ($118/0.12 = $987.50). That tells me investors are putting a c.137% premium on the company's steady-state value, and expect an 18.5% CAGR in earnings over the coming 5-years. At 18.5% on the current trailing NOPAT, this gets you to $35mm in FY'23 earnings, behind my estimates. I'd highlight two things here:

- The disconnect in my estimates to the market's suggests there could potentially be a mispricing in expectations.

- At 18.5% growth per year on $60mm FY'23 est. FCF into 2028 (in-line with market implied expectations), I get to $1.17Bn NPV in market valuation discounting at the 12%, or 19.5x forward P/E.

In that vein, I continue to rate ATRI a buy, noting potential mispricings in the market's expectations currently folded into its share price.

In short

Admittedly it has been quite an unenjoyable ride holding ATRI over the past 6-12 months. Forget holding the stock with tight stops - you'd have been liquidated ages ago. However, there are potential market generated explanations underneath the violent price swings, not to mention the fundamental data as well.

Whilst ATRI is a slow-growing, mature name, it still throws off cash to shareholders and produces positive economic earnings on a rolling basis. It is reasonable to expect these trends to continue further. The market has it valued at $988mm market cap at the time of writing (fluctuating between $1.16Bn and $980mm the last 6 months) and expects $118mm in owner earnings over the coming 5-years in my opinion. This is reasonable, but my estimates have ATRI to do $140mm in FCF in FY'28 calling for $1.17Bn in NPV or $664 per share. Net-net, reiterate buy.

For further details see:

Atrion: Trading Below Value, Volatility Presents Mispricings