AMT - Attention REIT Shoppers: A Blue Light Special In The Cell Tower Sector

2023-10-23 07:00:00 ET

Summary

- Crown Castle and American Tower, two cell tower REITs, are undervalued and offer attractive yields.

- Crown Castle is trading at its cheapest level in a long time, with a yield of 7.29% and a coverage ratio below 90%.

- American Tower has solid fundamentals and growth estimates, with an upside potential of 20-21% annualized return on investment.

This article was coproduced with Wolf Report.

When we last wrote about the two cell tower REITs – American Tower ( AMT ) and Crown Castle ( CCI ) specifically, we said that Crown Castle was valued for essentially 0% growth.

Not only is this still the case today, but the valuation is also even more compelling.

{kind=link}

We seem to be seeing a repeat of the fall 2022 trends but for different reasons.

While based on macro and overall interest rate risks there might exist justification for the market to be dropping as we're seeing today, it's also important to emphasize the degree of undervaluation and bargains available today.

It's always tricky investing in companies that have very few growth prospects. In today's interest rate environment, substantial asset and portfolio safety is required to offset the lack of growth risk.

We also shouldn't be buying non-growing companies at anything approaching premium valuations.

We haven't completely avoided the former problem.

Some of the options contracts that we've been selling have actually gone ITM at significantly lower price levels than we expected. This sort of outcome means a miscalculation on our part and requires us to adjust our way of thinking where necessary.

When it comes to Crown Castle and American Tower though, this is somewhat different.

iREIT®

2 Cell Tower Bargains

We own quite a few businesses that help people communicate:

- Deutsche Telekom ( OTCQX:DTEGY )

- Telenor ( OTCPK:TELNY )

- Telia ( OTCPK:TLSNF )

- Tele2 ( OTCPK:TLTZF )

- Orange ( ORAN )

- AT&T ( T )

- Verizon ( VZ )

These companies provide high dividends with high, relative margins of safety while not providing us with that much overall growth. That's the reason we have a high interest in the Cell Tower REITs.

People often ask us how we think about income versus growth investments - how we think about our portfolio in terms of expected returns.

The answer is that we tend to use a 60/40 approach - where 60% of our portfolio is weighted more toward income-focused companies.

This is where you'll find REITs, Telcos, finance companies, and other businesses with an above-average yield but solid fundamentals where our focus is on the attractive dividend.

CCI is still the largest provider of communications infrastructure in the USA and one of the largest in the world.

It owns over 40,000 towers, 120,000+ small cell towers as well as over 85,000 route miles of Fiber infrastructure - and absolutely nothing of this is going anywhere in the near term future.

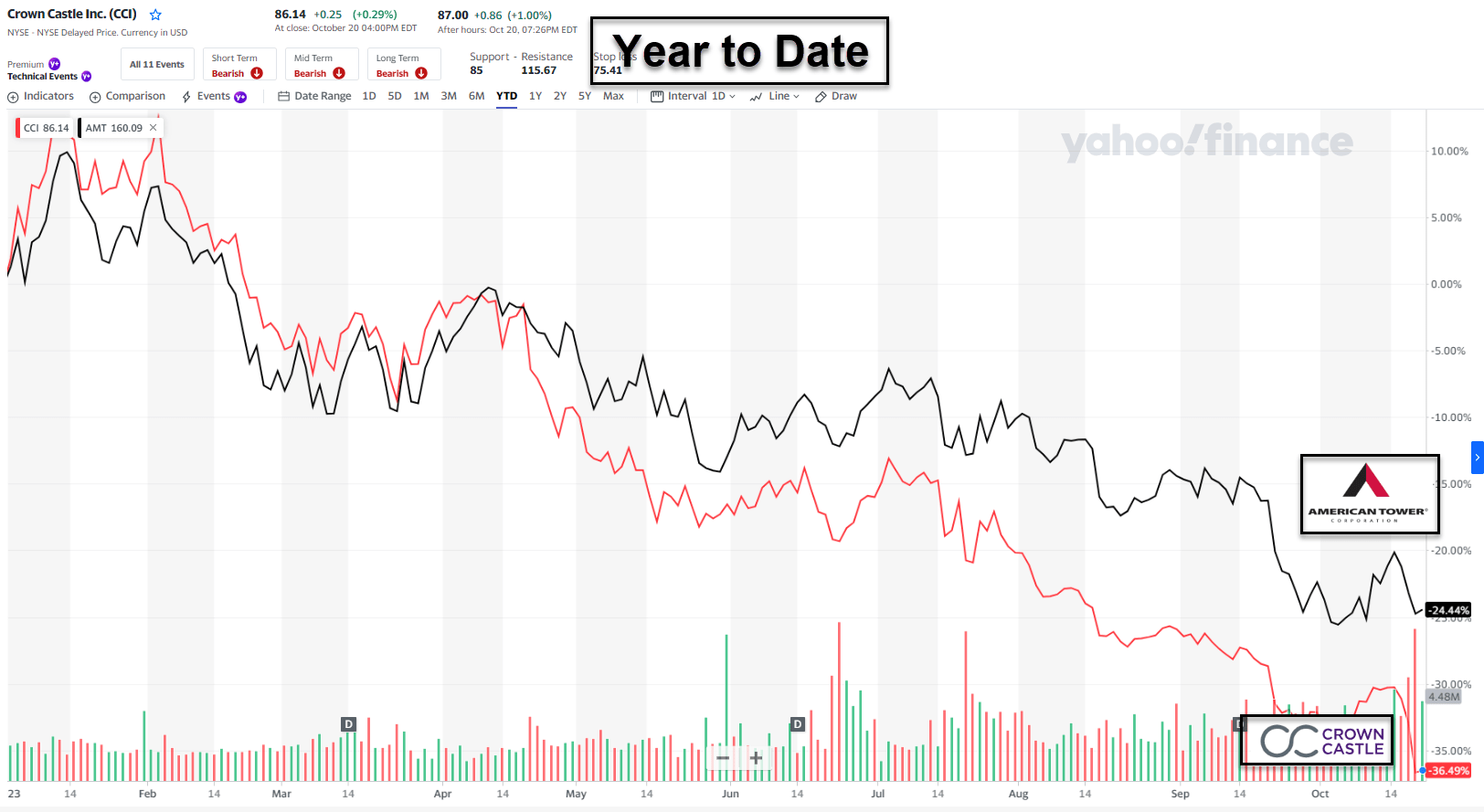

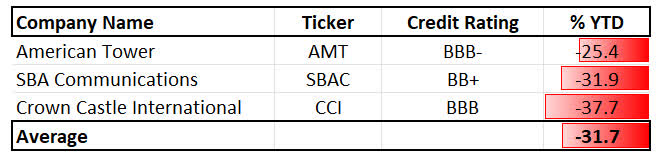

The current levels of valuation mean that we're getting a 7.29% yield for a BBB-rated cell tower REIT.

That is the cheapest the company has been in a very long time, even as long as the company has been around. It currently trades at 11.4x to FFO, despite a coverage ratio even if we forecast a 2-4% annual decline in FFO, of below 90%.

CCI has a near-unbroken record of FFO growth of 7-9% up until this year, in 2024 fiscal, when the trend is expected to go negative.

This FFO is based on a fundamentally sound set of infrastructure assets - even if investors argue the merits and demerits of the various technologies here.

CCI IR

In the most recent communication, CCI went ahead and further adjusted its expectations for the 2024 period, while clearly stating its ambition and likelihood of meeting its 2023E goals.

In fact, despite what you may see in the share price, results were actually mostly in line with overall expectations, which is also why the company is fully on track to meet 2023E, which includes 5% organic revenue growth and 10k small cell node.

And top-line organic growth is not the problem for CCI.

2024E results are, equally and in line, expected to see 4.5% organic revenue growth, and even more adds of small cell nodes, as well as organic growth in fiber.

CCI fully expects a low point in FFO - and for the time being, this is expected to be troughing in 1H24, with growth resuming in 2024E.

Even if we say that growth resuming may go at a later point than this, it's hard to argue anything except the company being very cheap at this point, despite it being in a slight decline.

But that is the way the market currently is. Even if your business promises high amounts of dividend income, and even if that dividend income is safe, this is not enough for many investors anymore - your REIT or your company is, despite this, being "devalued" here.

CCI IR

These are the results based upon which we're currently seeing a significant decline in valuation.

Is this in any way justified?

Maybe - but not to the degree that we’re seeing here.

AMT, or American Tower, has similar trends, though and is not estimated to actually fall, but grow.

That's why some prefer AMT to CCI, even though CCI has a better credit rating and better yield.

AMT yields around 4% here, trading at a 16.3x P/FFO - it's held up better, but it's still down significantly.

But both companies are extremely forecastable , meaning a 90%+ accuracy ratio in terms of hitting forecast targets, even with only a 10% margin of error.

While AMT has not yet reported its 3Q23 at the time that we’re writing this article, we do not expect the company to drop as violently as CCI has YTD.

As we’ve said before - we do not mind investing in companies that are seeing earnings, FFO or net income decline, as long as you can justify that we’re getting a bargain and we see a turnaround.

Usually, if we go statistically by our investments over the past 10 years, such cases turn out fine or more than fine.

Only a small handful of cases have turnarounds that we’ve invested in turned sour - and none of those have been infrastructure companies with this sort of market cap that we're seeing for CCI or AMT.

CCI has a combination of balance sheet strength and portfolio appeal.

The balance sheet is because CCI was one of the few companies to issue longer-dated debt at interest rates that at the time seemed high, but now seem low.

The company was able to pay down higher-expense debt with the proceeds of this, and it has resulted in a stellar debt/EBITDA rate. We would argue that the company, with only around 4.5x, is indeed as high as BBB+ or even A-rated.

That makes it one of the highest-rated Tower infrastructure companies around.

AMT has what we would consider an almost equal level of overall safety and upside. The company even estimated, in their last report, that revenues for the year are going higher than initially expected. This also included a raise in expected EBITDA for the company.

These companies come with solid investment profiles - both of them.

You can either go with CCI or AMT, or you can do as we do, and invest in both.

CCI is somewhat fundamentally stronger, as confirmed by a better credit rating, but is currently in more of a slump.

AMT has a lower yield, but isn't expected to go through a slump, but rather continue to grow.

This hasn't helped the company's valuation or the rate of decline though.

Valuation for AMT and CCI

Beginning with CCI, we share the analyst forecast that we're probably seeing a downturn in 2024E, but we wouldn't necessarily guarantee that 2025E is going to turn out as badly as analysts seem to expect it to turn out.

And given that we're already trading at severely discounted levels, the upside is only improving more and more.

Let’s begin by showing you the long-term trend.

FAST Graphs

What you see above is the reason why we were actually not interested in buying the company until now. This company, and these sorts of companies have traded at such extremes to their relative fundamentals for such a long time. It's easy to believe that they are now undervalued to an almost insane degree.

We would say that CCI is now at levels where we can not only buy, but we can seriously buy.

We say that because even if we assign a very conservative multiple to over $35B worth of market cap in a portfolio in fundamental infrastructure yielding over 7.2% your upside is now over 16.4% annually.

That's on a 15x P/FFO with an average of 22x over the past 5 years.

22x is unrealistic on a forward basis.

But 17-19x P/FFO is at the very least possible in the long term. So the upside we see for CCI for the long term is between 16.4% annually at this price, and up to above 25-26% p.a. if some sort of premium holds, here implied with a $130/share price.

FAST Graphs

AMT has similar upside levels, only in this case, we don't have a good upside to a conservative 15x P/FFO.

The upside for AMT to 15x P/FFO is closer to 7.5% per year, which isn't great, however, AMT based on its fundamentals and growth estimates deserves a minimum of 17.5x, and potentially all the way up to a 19-20x P/FFO - and when we estimate there, we find a 20-21% annualized RoR potential.

FAST Graphs

The simple fact is that both of these companies at the very least deserve a modicum of attention from you - at least in considering if they somehow meet your investment goals.

These companies are not A-rated, but the infrastructure portfolios they manage, and the companies they work with, are A-equivalent or comparable, based on their operations.

Both of them are coming out of extremely high-valued situations that for a long time have impacted what the market believes them to be worth.

That logic is, with the current interest rate environment, thrown out the window - and we need to re-evaluate what these companies are worth.

We believe that both of these companies offer good enough business models with extremely forecastable and secure cash flows to where paying their respective dividends is not going to be a problem.

We also believe that this marks perhaps the first opportunity in many, many years of buying them at a good price - similar to what we're seeing in other parts of the overall market.

We also see this as being a good case study for why the long term matters, and why you should never believe that just because a company has tended to a premium for 5-6 years, this should stick around - and why at times, you're better off selling and reinvesting into cheaper options.

FAST Graphs

Just look at these trends.

This has nothing to do with any assumption that AMT is a bad company because that is certainly not the case. It's just that every reason why AMT has been valued at such a premium has been disappearing, with perhaps the exception of FFO growth - but even that really only goes so far.

We believe it's the best time in almost 10 years to buy both of these businesses and here is our thesis for that.

{kind=link}

Thesis

- Crown Castle Inc. is among the market-leading cell tower/infrastructure REITs. It yields around 7.0% and while it won't grow much, its yield is covered (82% payout ratio). While leverage remains a concern though one that's being paid down, this is the only actual risk/Drawback, aside from the lack of growth seemingly inherent here.

- We would value CCI at 17-18x P/FFO for a "BUY". That means that as the valuation stands today, we can actually buy the company.

- There is an upside, and my PT is $125/share or below for CCI for the long term.

- American Tower is among the market-leading cell tower/infrastructure REITs. It yields over 3.5%, and it has operations across the world, which we view as an absolute must for investment in this type of company. While leverage remains a concern though one that's being paid down, this is the only actual risk/Drawback, aside from a single-digit AFFO growth rate, that I see for this REIT.

- We would value AMT at 17-21x P/FFO for a "BUY" for the long term, lowering the accepted premium for the company. That means that as the valuation stands today, we can actually buy the company.

- There is an upside, and my PT is $180/share or below.

{kind=link}

Remember, we’re all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, we harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, we buy more as time allows.

- We reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are our criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansions/reversion.

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

Attention REIT Shoppers: A Blue Light Special In The Cell Tower Sector