BSJT - Attractive Income Opportunities For Uncertain Markets

2023-11-30 23:30:00 ET

Summary

- Interest-rate hikes in the United States are on pause but may remain higher for longer with lagged effects likely to manifest in early 2024.

- There is renewed investor interest in fixed income as the asset class offers the potential for income and total return.

- Equities have remained resilient but restrictive monetary policy may impact corporate revenues going forward.

- Our asset mix favors fixed income and within this asset class we prefer investment-grade corporates. Within equities, we prefer high-quality dividend stocks.

By Edward D. Perks, CFA, Chief Investment Officer, Franklin Income Investors

In a turnaround from last year, there is renewed interest in the fixed income asset class as yields have risen. Ed Perks, CIO of Franklin Income Investors, shares his analysis of recent macro developments and where he sees opportunities for income.

A pause in US rate hikes

Looking back, the US Federal Reserve (Fed) was behind the curve in starting to tackle inflation. However, once it did, it raised rates quite substantially from 0.25% in March 2022 to 5.50% in July 2023. Despite the significant rise in rates over the past year, we believe there are valid reasons for the current pause in hikes.

In March 2023, there was some concern that hearkened back to the global financial crisis as higher rates caused banking stresses, hitting US regional banks particularly hard.

Concerns of contagion to the rest of the industry and the economy more broadly turned out to be unwarranted. The crisis was more idiosyncratic and affected regional banks with poor risk controls.

At the time, the Fed expanded their balance sheet, while it tried to understand the ramifications of the few regional banks that collapsed.

With the US Treasury also injecting liquidity into the markets, the effect of the tightening was delayed. By summer, the Fed moved back into quantitative tightening in a meaningful way and into more restrictive territory.

Although inflation remains high, monetary policy tends to have a lagged and variable effect. In our view, we could start seeing the lagged effect of the Fed’s tightening efforts in a more material way in the first quarter of 2024.

With the broader tightening of financial conditions, regional banks are back in the spotlight as they are beginning to feel the strain of higher funding costs. They have gotten a little bit of a reprieve due to economic resilience, but there are now underlying signs of some deterioration in credit conditions.

This will mostly affect small- and medium-sized businesses who depend on these regional banks and are important to the US economy as an important contributor to the overall level of employment.

Additionally, while bond yields have declined from recent highs in October, they remain well above the average levels from earlier in the year. In our opinion, yields may remain high through year-end and thus are doing part of the work of the Fed going forward.

Some economists estimate that the increase in longer-term yields we’ve experienced is equivalent to a couple of Fed rate hikes.

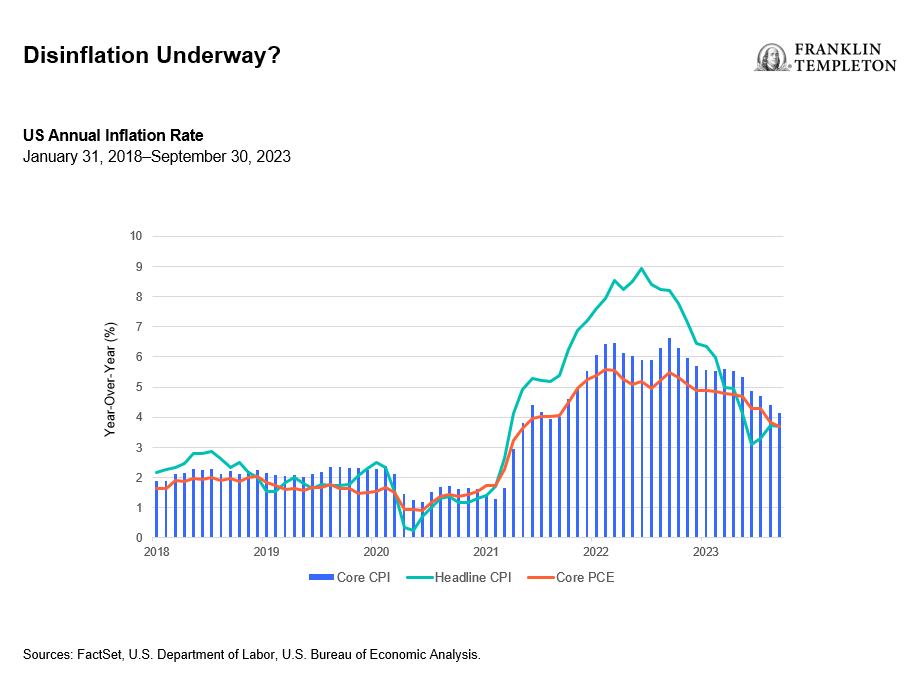

Lastly, the markets generally expect the US economy to slow, although maybe not the recession that market participants were fearing earlier this year. The trajectory for the Consumer Price Index heading into 2024 appears to be a continued downward movement, albeit slowly.

While inflation has likely peaked, the rest of the way toward the Fed’s 2% target could prove to be more challenging. We believe rates could stay on hold and be higher for longer.

{kind=link}

Reasons for the renewed focus in fixed income

The last time the Bloomberg US Aggregate Bond Index, which broadly tracks the performance of the US investment-grade bond market, had a positive total return was in 2020.

It was mildly negative in 2021, and 2022 was historically one of the most difficult years for fixed income investors, which also coincided with a downturn in equities. 1

However, the landscape has changed dramatically more recently, and we believe the longer end of the yield curve and taking on some duration now look attractive.

Although we believe cash continues to offer solid yields, if there is a change in the rate policy regime, we think cash investors would be left in the dust sitting on too much short duration.

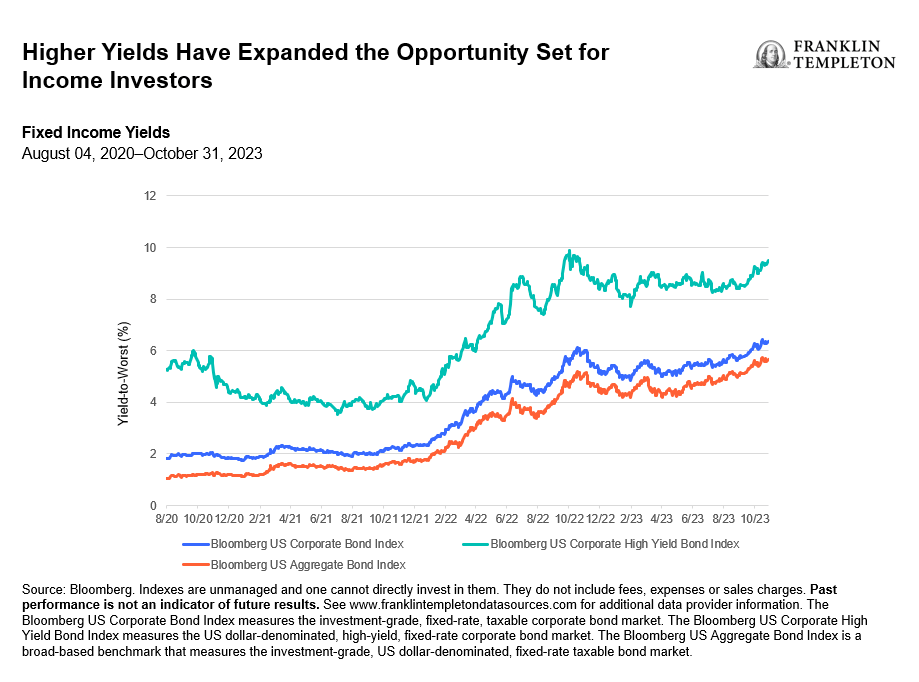

For instance, yields have risen across the board within fixed income. As of October 31, 2023, the broader Bloomberg US Aggregate Bond Index offered yields at 5.6%, investment-grade corporates (as measured by the Bloomberg US Corporate Index) offered 6.4% and high yield (as measured by the Bloomberg US Corporate High Yield Index) offered 9.5%. 2 So we are now seeing high-yield bonds associated with higher yields once again.

{kind=link}

A deeper dive into equities

It is worth discussing the relative attractiveness of bond yields versus equity yields given the amount of monetary tightening this past year and the slower growth trajectory of the US economy going forward.

In our analysis, there will likely be a bit more compression in equity market multiples as the Fed tries to engineer a soft landing to restore price stability. We believe there are two primary contributors to the broad equity market resilience of 2023.

First is the resilience of the broader economy, with US consumers continuing to spend their pool of excess savings built up during the pandemic.

Second is the bifurcation in the equity markets as the so-called Magnificent Seven (Alphabet ( GOOG ) ( GOOGL ), Amazon ( AMZN ), Apple ( AAPL ), Meta ( META ), Microsoft ( MSFT ), Nvidia ( NVDA ) and Tesla ( TSLA )) have provided most of the positive total return for the US equity market year-to-date.

The S&P 500 equal-weighted index - without the effect of market capitalization of these seven companies - shows a more difficult backdrop for the rest of the components of the index. 3

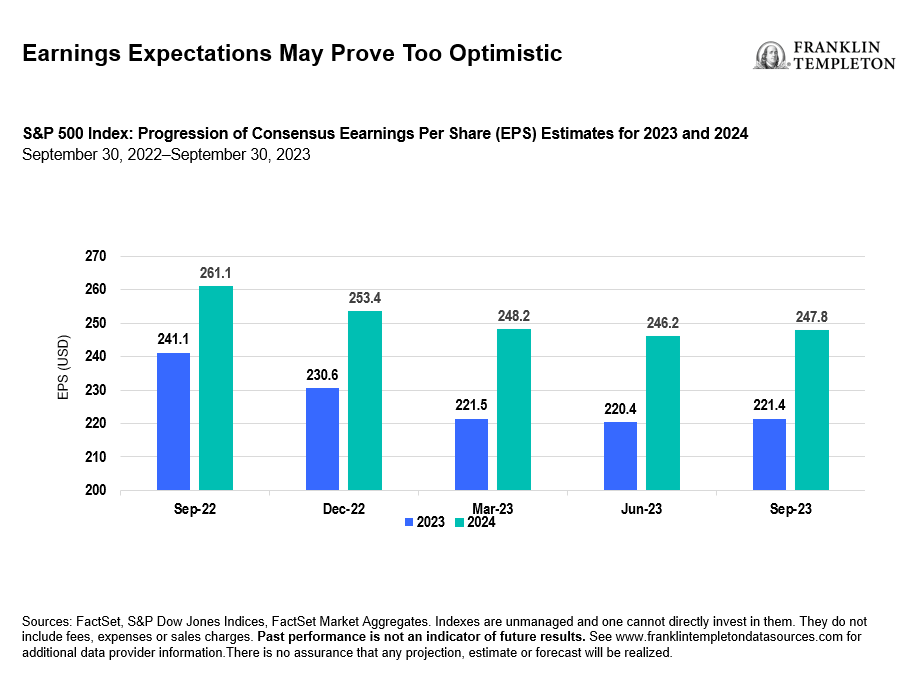

Additionally, while this past earnings season has shown that companies have remained resilient, their reliance on pushing through price increases to their customers may be waning.

With the higher-for-longer and lagged effect of monetary policy, we expect revenues and earnings growth to be far more challenged in the coming quarters.

{kind=link}

Asset-mix strategy

From an asset allocation standpoint, we continue to prefer high-quality fixed income due to what we consider attractive yields and longer-term total return potential.

We have modestly pulled back on high-yield bonds, as higher rates may put greater strain on many non-investment-grade balance sheets. We continue to maintain a diversified exposure to equity sectors that we think can generate income and participate in a broad-based equity market advance.

Within equities, we prefer high-quality dividend stocks where valuations have become a bit more palatable, in our opinion.

What are the risks?

All investments involve risks, including possible loss of principal. Equity securities are subject to price fluctuation and possible loss of principal. Dividends may fluctuate and are not guaranteed, and a company may reduce or eliminate its dividend at any time. Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

1. Source: Bloomberg. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator of future results.

See www.franklintempletondatasources.com for additional data provider information.

2. Source: Bloomberg. As of October 31, 2023. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator of future results.

See www.franklintempletondatasources.com for additional data provider information.

3. Source: Bloomberg. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator of future results.

See www.franklintempletondatasources.com for additional data provider information.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Attractive Income Opportunities For Uncertain Markets