AUPH - Aurinia Pharmaceuticals: Lupkynis Patent Settlement Removes Overhang

Summary

- Aurinia Pharmaceuticals recently announced they have reached a settlement with Sun Pharmaceuticals concerning the patent challenge for Lupkynis. Both companies will dismiss their claims and counterclaims against each other.

- Following the settlement announcement, AUPH shares jumped up over 30%, and have since climbed to around $6.75 per share. This settlement removes a significant overhang for the company and AUPH.

- The stock is still down roughly 70% over the past twelve months. I believe AUPH offers a great opportunity for a potential trade or investment at these prices.

- AUPH was once a rumored acquisition target. The Sun Pharmaceuticals settlement might reignite M&A chatter once again.

- I have decided to put AUPH on my watch list for Compounding Healthcare. It appears to be a prime candidate for my “Bio Boom” Speculative Portfolio.

Aurinia Pharmaceuticals ( AUPH ) recently announced they have reached a settlement with Sun Pharmaceuticals (SMPQY) to dismiss their claims and counterclaims against each other. Now, Aurinia does not have to worry about Sun’s patent challenge for Lupkynis, which was a major overhang for the company and the stock. Following the patent settlement announcement, AUPH shares jumped up over 30%, and have since climbed to around $6.75 per share. However, the stock is still down roughly 70% over the past twelve months. Now that Lupkynis has an improved long-term outlook, I believe AUPH offers a great opportunity for a potential trade or investment at these prices, especially considering we could see renewed buyout chatter. As a result, I have decided to put AUPH on my watch list for Compounding Healthcare and could be a prime candidate for my “Bio Boom” Speculative Portfolio.

I intend to provide a brief background on Aurinia and the Sun Pharmaceuticals agreement. In addition, I discuss how this development changes the company’s and AUPH’s outlook. Then, I provide some downside risks that investors should consider. Finally, I deliberate on adding AUPH to my watch list.

Background on Aurinia

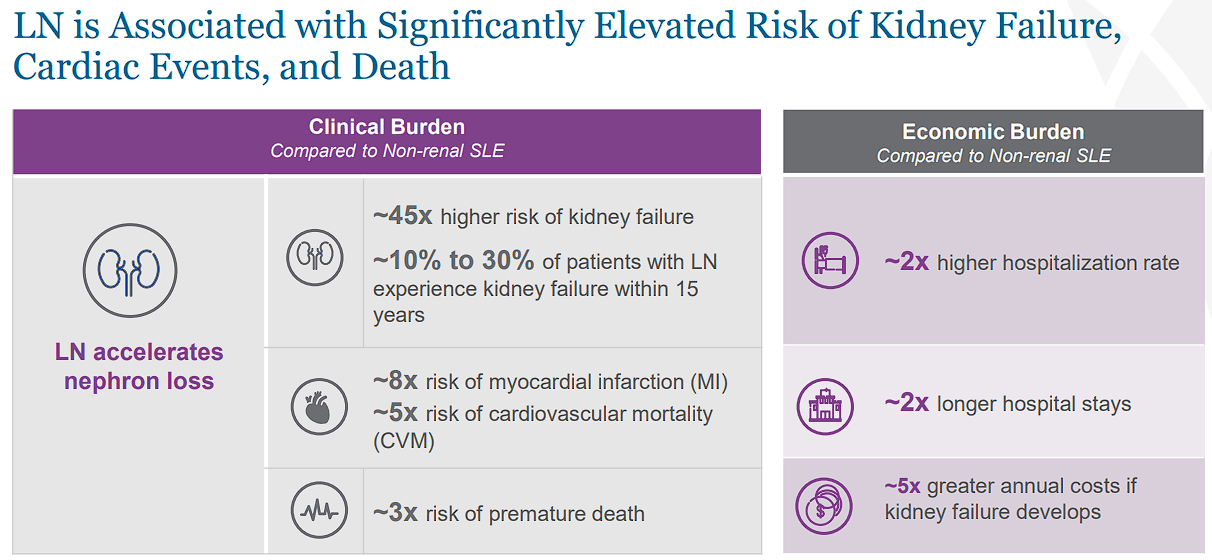

Aurinia Pharmaceuticals is a commercial-stage biopharma that focuses on developing and commercializing therapies for serious diseases with high unmet medical needs in the United States and internationally through its partner. The company’s flagship product, Lupkynis, is the first FDA-approved oral therapy for adults with active lupus nephritis “LN”. LN is one of the most serious complications of systemic lupus erythematosus “SLE”, a chronic and complex autoimmune disease. LN can cause permanent kidney damage and failure, as well as cardiac issues, and even death. It is estimated that roughly 200K-300K people live with SLE in the US with about 1/3 being diagnosed with LN at the time of their diagnosis and around 50% of all SLE patients might progress to have LN.

Aurinia Pharmaceutical LN Clinical and Economic Buren (Aurinia Pharmaceutical)

{kind=link}

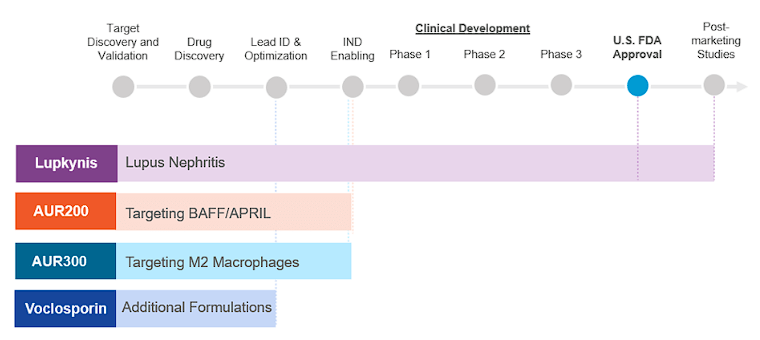

Aurinia has a collaboration and license agreement with Otsuka Holdings (OTSKY) for oral voclosporin for LN in the EU, Japan, as well as the UK, Russia, Switzerland, Norway, Belarus, Iceland, Liechtenstein, and Ukraine. In return, Aurinia received an upfront cash payment and has the potential to receive milestone payments, as well as tiered royalties.

In addition to voclosporin “Lupkynis”, the company has two other pipeline assets that they have acquired. AUR200 is the company’s recombinant Fc fusion protein intended to explicitly block B-cell Activating Factor “BAFF”, and A Proliferation-Inducing Ligand “APRIL”, which are involved in the pathogenesis of some autoimmune diseases and nephrology conditions. The company is currently working on pre-clinical work for AUR200, but expects to submit for an IND at some point in 2023.

The company also has AUR300 , a novel peptide that moderates M2 macrophages which can facilitate fibrosis when dysregulated. AUR300 is taking on autoimmune and fibrotic diseases by attempting to regulate M2 macrophages and reduce inflammatory cytokines that are associated with these diseases. Aurinia expects to submit an IND for AUR300 in 2023.

{kind=link}

In terms of performance, Aurinia has reported significant growth due to their commercial launch of Lupkynis. In fact, the company’s Q3 earnings were better-than-expected financials, with revenue more than tripled year-over-year to $55.8M as a result of a $30M regulatory milestone payment from Otsuka for Lupkynis European approval. In addition, the company noted that the number of patients on Lupkynis increased ~6%, and product revenue rose ~74% year-over-year to $25.5M.

However, they lowered their full-year guidance from $115M-$135M to $100M-$105M. The company alluded to weak demand for Lupkynis attributable to “reduced lupus nephritis diagnoses and patient visits in the quarter.” Aurinia also provided preliminary guidance for 2023, indicating $120M-$140M in net revenue from Lupkynis sales, and $229.2M in revenue.

Aurinia reported a net loss of $9M for Q3 and a net loss of $82.1M for the first three quarters of 2022. Aurinia finished Q3 with $376.6M in cash, cash equivalents, and restricted cash and investments, which was down from $466.1M at the end of 2021. However, this did not include the cash receipt of the $30M milestone payment from Otsuka related to EC approval received this payment on October 31 st . So, the company’s cash, cash equivalents, and restricted cash and investments were around $400M .

Sun Settlement

As I mentioned above, Aurinia recently announced a settlement agreement with Sun Pharmaceuticals, where both companies will file a joint motion to terminate the ongoing battle over Aurinia’s patent for Lupkynis, as well as the patent infringement litigation over Sun’s CEQUA. Both companies are to dismiss their claims and counterclaims and cease future action against the other.

The resolution of this matter is huge for the company and should continue to translate into the stock. Obviously, not having full patent protection on a recently approved branded drug will crush the drug’s peak sales and impact the company’s long-term outlook. This is especially true for drugs that are pushed by small and mid-cap companies that just trying to establish their presence on the market. Aurinia does not have a large-scale sales organization that big pharma has, so it can take additional time to get a new drug to peak sales. So, the prospective loss of IP was viewed as a potentially fatal result for the company. Moreover, the patent litigation stopped the buyout chatter around Aurinia, which was partially responsible for the stock's previous premium valuation.

Now, the company appears to be in clear with Lupkynis, which should allow them the time to see the drug hit peak sales. In addition, the removal of the litigation should reignite the buyout chatter around ticker… especially at these current valuations.

Downside Risks

AUPH has multiple downside risks that investors need to consider when managing their position. First, Aurinia is still recording losses and reported a net loss of $82.1M for the first three quarters of 2022. Indeed, the company has a strong cash position at this point in time, but the company is going to need Lupkynis to start gaining some traction in the coming quarters if they want to avoid dilutive financing in the future. Unfortunately, the company saw a small decline in new patient start forms in Q2, and also publicized a ~9% year-over-year decline in Q3. Remember, the company lowered their full-year guidance from $115M-$135M to $100M-$105M, which is concerning considering the drug was just launched. Keep in mind, the company needs Lupkynis to be a commercial success, because their next pipeline program is several years away from a potential approval.

Indeed, these circumstances could be addressed in the coming quarters as the company refines their commercial strategy and accelerate growth. Still, investors need to accept that there is some risk in AUPH, therefore, I am assigning AUPH a conviction level of 2 out of 5 at this time.

On My Watch List

I have been on the lookout for healthcare tickers that have been punished during this prolonged market-wide sell-off. Typically, I am looking for tickers that have experienced unjustified selling pressure and are now trading at a discount. Prior to the settlement announcement, I wouldn’t put AUPH in that category due to the unknowns and downside risks. Now that the patent issue has been resolved, I would classify AUPH as an oversold ticker that is trading at a discount for its potential growth prospects.

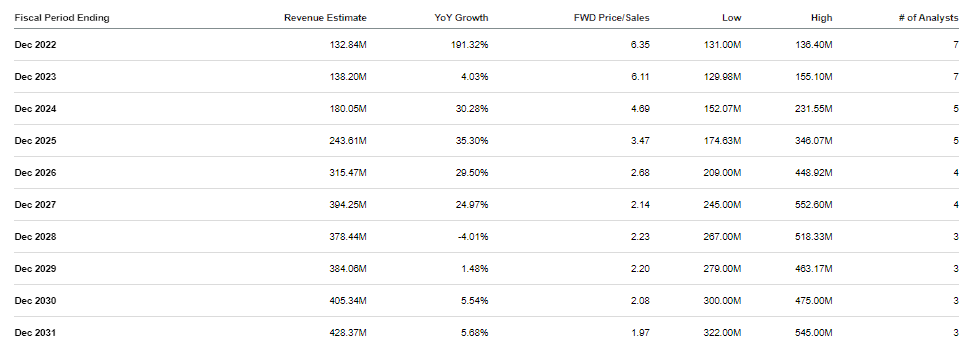

Looking at the Street’s revenue estimates, we can see that analysts expect Aurinia to report strong double-digit revenue growth for the next several years and hit around $394M in 2027, which would be a forward price-to-sales of roughly 2x.

{kind=link}

Considering the industry’s price-to-sales is around 4x-5x, we can say that AUPH is trading at discount for its projected future sales. If the company was to be valued in line with its peers, it would be trading around $11-$14 per share. Indeed, we don’t know if the company will hit these revenue estimates, but they do illustrate the company's potential growth in the coming years.

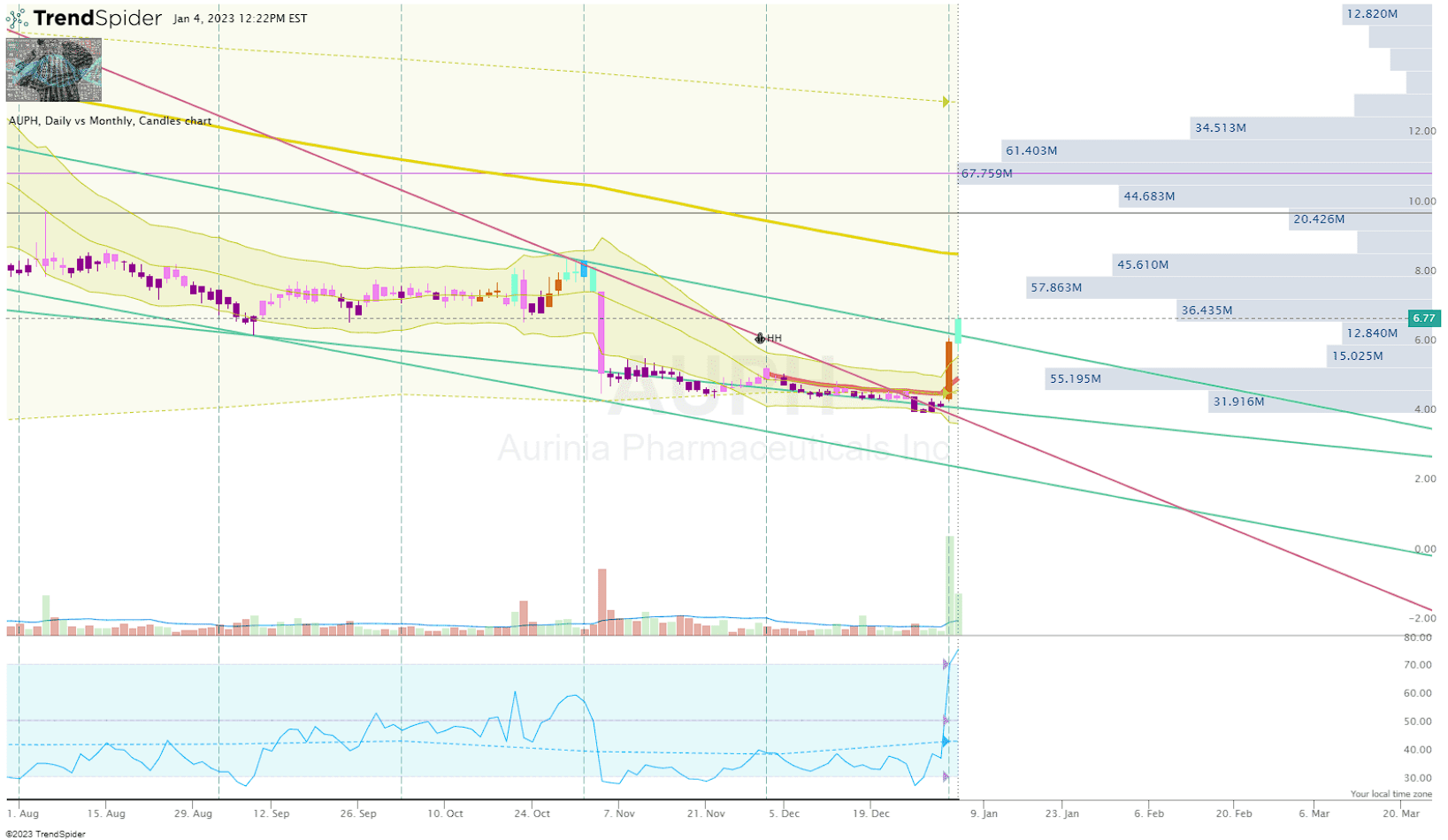

For me, I am going to set some alerts around the formation high around $5.75 per share to see if the prior resistance has become new support.

{kind=link}

AUPH Daily Chart Enhanced View ( Trendspider )

If I see a spike in volume and a solid bounce of these levels, I will attempt to find a clean entry point for a starter position. Admittedly, this position would be minuscule compared to some of my larger “Bio Boom” positions, but the company’s product and area of focus will help broaden the portfolio. I anticipate maintaining an AUPH position for at least five years in anticipation the company will make Lupkynis a commercial success and/or the company is acquired at an acceptable valuation.

For further details see:

Aurinia Pharmaceuticals: Lupkynis Patent Settlement Removes Overhang