AUPH - Aurinia Pharmaceuticals: Updating My Revenue And Valuation Model

- LUPKYNIS revenues and company net losses are tracking better than my valuation model predicts -- and new European revenues are on the horizon.

- However, expenses continue to rise, which is contrary to my modelling.

- Overshadowing all of this are severe patent risks.

This article is a follow-up to my previous coverage of Aurinia Pharmaceuticals ( AUPH ) and as such may run a little shorter than earlier ones. In particular, today, I'd like to update my revenue and valuation model to include the latest two quarters of data. I'll then turn to the biggest risk for the company, one which has recently taken the stock price down even further. But before turning to these, let's begin with a review of LUPKYNIS, as the company has issued some new ways of looking at the drug's use and value proposition.

LUPKYNIS

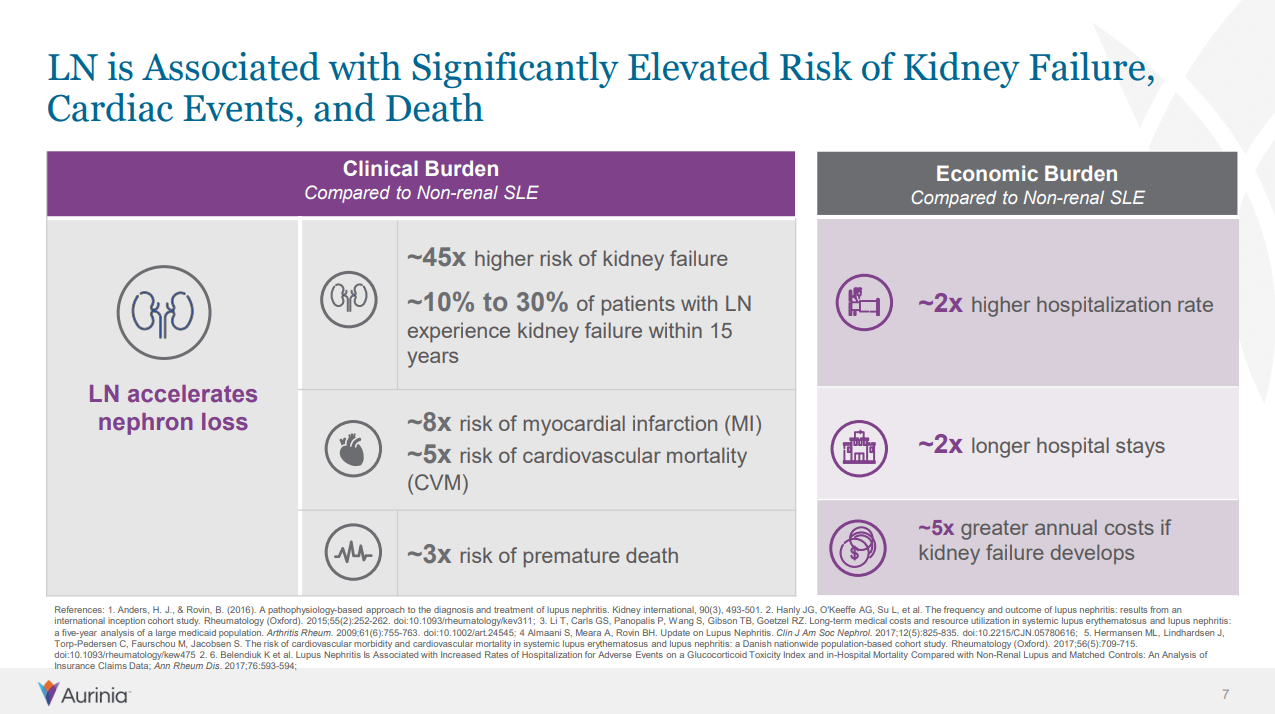

First, consider the need and value for LUPKYNIS in active lupus nephritis ((LN)) patients. When untreated, LN increases the risk of kidney failure by 45X in comparison to patients with non-renal systemic lupus erythematosus (SLE). It also greatly increases the risk of cardiovascular events and premature, all cause, deaths. Each of these risks have a commensurate cost incurred by patients and the healthcare system as a whole.

{kind=link}

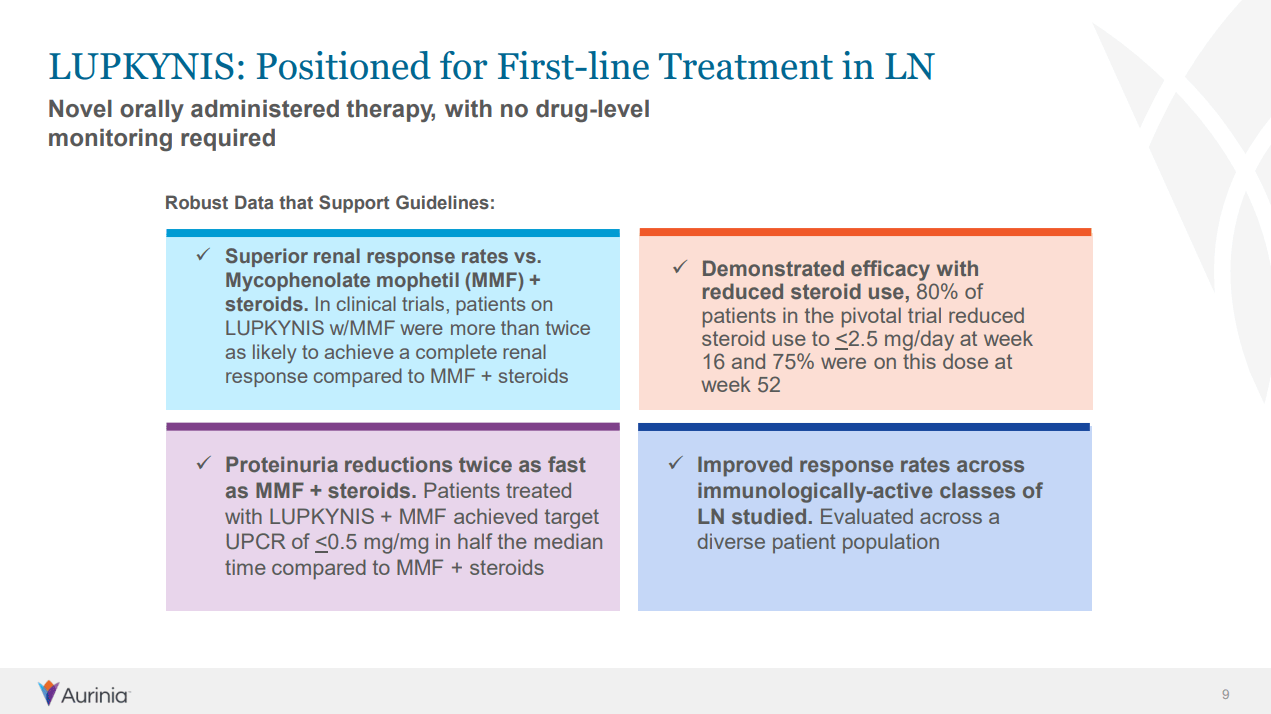

LUPKYNIS acts to reduce these risks by reducing proteinuria to reduce and even reverse kidney damage. Moreover, the time it takes for patients to benefit from the drug is on order of half the time associated with other leading drugs. This slide summarizes some of these benefits.

{kind=link}

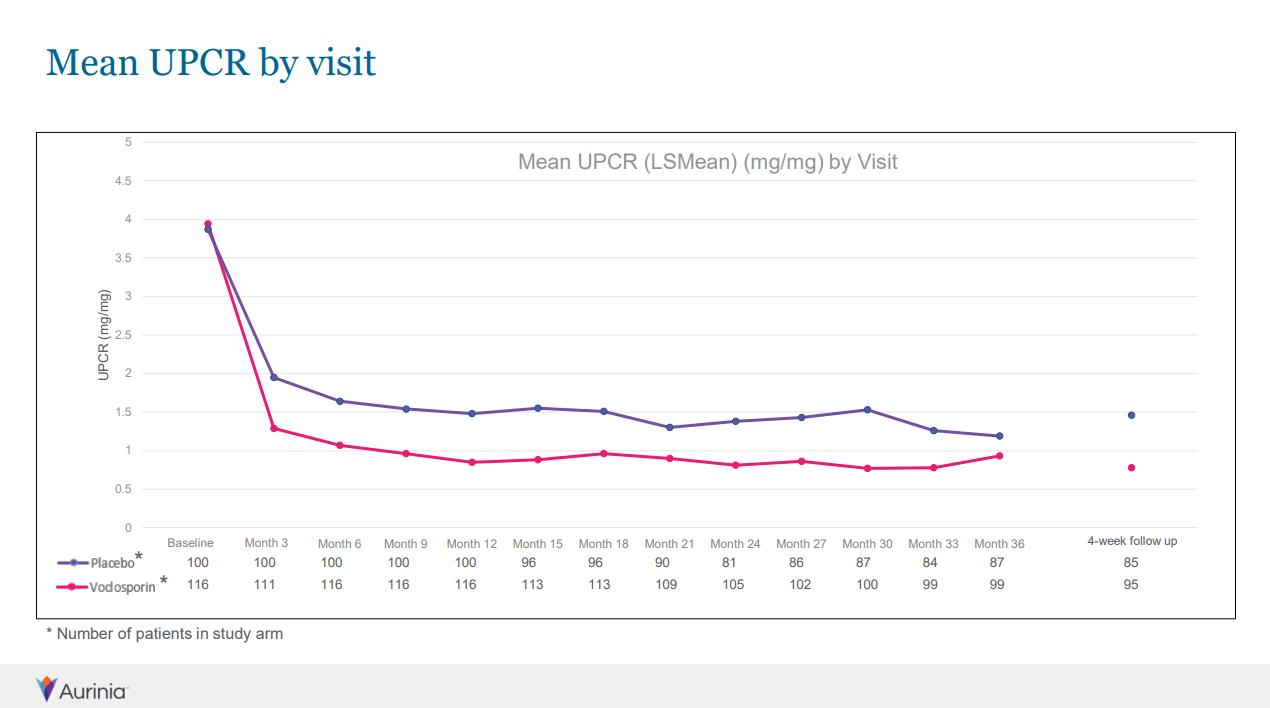

Recently, AUPH obtained follow-on data that shows that the benefits of staying on LUPKYNIS can extend to three years. This is relevant as it makes it more likely patients will stay on medication rather than discontinuing in a year or less. Moreover, the long-term study showed fewer adverse events in the treatment arm than in the placebo arm which is very comforting to patients, doctors and regulators.

{kind=link}

LUPKYNIS UPTAKE

Before updating my revenue and valuation model, it's worth pointing out some of the comments, both positive and negative, the company made in this regard during the most recent earnings call (with my emphasis).

During the first quarter of this year, we saw many encouraging trends supporting the commercial performance of LUPKYNIS. The majority of which persisted into the second quarter with a number of them actually improving quarter-over-quarter. Here are some positive trends we saw in Q2. Total patients on therapy grew to 1,274, up 19% from 1,071 at the end of Q1. We saw notable improvements in refill rates and shipped the highest number of wallets in a quarter since the launch of the product. Persistency trends in our business also remain encouraging. Consistent with the last quarter, approximately 70% of commercial patients remain on treatment at six months, and at nine months approximately 60% of patients remain on treatment.

As previously discussed, we will continue to update these figures as we progress further into the launch. Conversion rates and patient access remain robust, whether it's 30, 60 or 90 day conversion rates all continue to improve and are currently at peak level since the launch. Efforts to increase healthcare provider adoption of LUPKYNIS and regular practice remain consistent and positive. Each month, we're adding new prescribers with 190 new prescribers in quarter two alone. Prescribing rates remain balanced between both rheumatologists and nephrologists.

[...]

So while we're pleased with those positive trends, we're less pleased with our performance on PSFs for the quarter. In Q2, we added a total of 409 PSFs, bringing our year-to-date total to 867 PSFs as of June 30th. The updated number of prescription start forms year-to-date through Friday, July 29th is 981 .

This latter observation is one of the big risks with AUPH. Throughout the rest of the earnings call, the company was confident that it would re-accelerate the number of patient start forms ((PSF)) in future quarters, but if they can't, then the company will never be profitable. It's one of the most important metrics to watch going forward.

With that said, let's look at where the company is on revenues versus the valuation model I presented in this earlier article .

Updated Revenue and Valuation Model

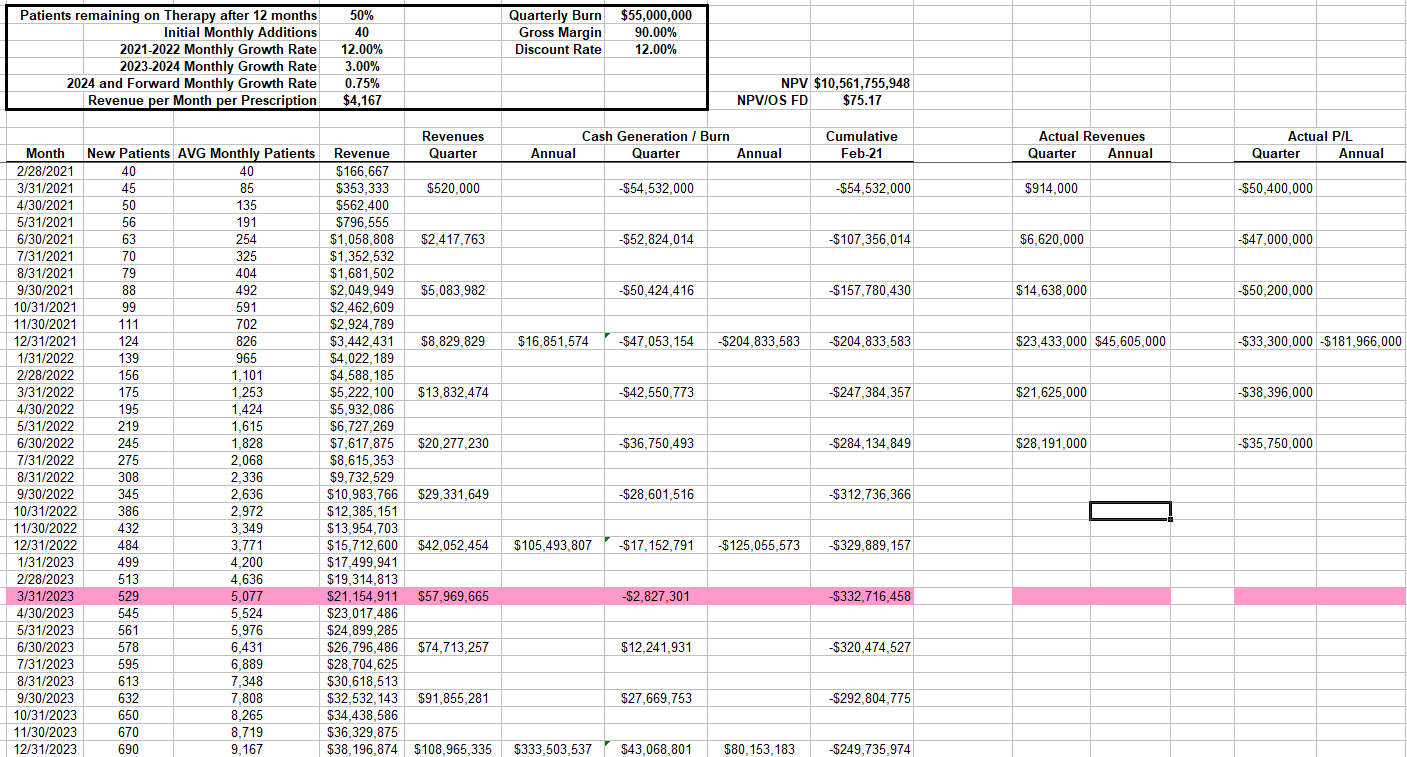

The figure below has entries for my estimated revenues and cash burn, alongside the actual revenues and P/L for the company through the 2Q 2022. Actual revenues are still outpacing my estimated revenues, and even the profit/loss is better than my anticipated cash burn for recent quarters. However, I'm a little worried that expenses keep trending up, which wasn't something I modeled (see graph below the spreadsheet).

As of now however, I'm maintaining my model and hope that the company can become cash flow neutral sometime in Q2 2023.

Author's model

{kind=link}

Were it not for the risks, I'd be buying more AUPH at today's prices, since the model still is very positive for AUPH's valuation, should it be able to maintain its growth trend through 2037. Moreover, there's been very favorable movement in the approval process in the EU, such that milestone and licensing revenues should begin to accrue from here on out. From the latest 10Q (with my emphasis):

In July 2022, Aurinia announced that the Committee for Medicinal Products for Human Use ((CHMP)) of the European Medicines Agency ((EMA)) adopted a positive opinion recommending voclosporin (brand name, LUPKYNIS) for marketing authorization to treat adults with active LN. Upon approval by the EMA, we would be eligible for up to an additional $30 million as an approval related milestone, in addition to low double-digit royalties on net sales and revenues for the supply of product to Otsuka under a cost-plus arrangement .

Risks

Let's now consider the risks of investing in AUPH, the first of which has grown in seriousness and likely explains why the stock has continued to fall despite decent revenue growth.

Patent Risk

LUPKYNIS is currently protected by two key patents. The first is a composition of matter patent good through October 2022 (but with the company having filed for a routine extension through October 2027). The second is a patent which AUPH obtained for a proprietary method of dosing LUPKYNIS based on personalized pharmacodynamic eGFR data, good through December 2037. LUPKYNIS is intended to be administered using this personalized method dosing, because it both improves efficacy and helps ensure the safety profile of the drug.

However, it's this latter patent that's now under dispute, and should the company not prevail, then any model of revenues will be moot past October 2027 at best. (If one examines my model, one will see that the big values accrue after this 2027 date.)

Here's what the company said on the subject during the most recent earnings call (including important color on why the dosing is important, shown with my emphasis):

As announced last week, the U.S. Patent and Trade Office’s Patent Trial and Appeal Board notified us of its decision to institute trial on the Inter Partes review or IPR filed by Sun Pharmaceuticals. The patent subject to the IPR is related to LUPKYNIS dosing protocol and extends patent protection to 2037. A determination on patentability in relative to this IPR is expected on or prior to July 26, 2023.

Regardless of the final outcomes of the IPR, we have filed a standard patent term extension for our existing composition of matter, which if granted, when extend – could extend the terms for that patent by five years through October of 2027. We also have other patent applications underway, which if granted could offer additional intellectual property protection for LUPKYNIS.

In addition, our lawsuit against Sun Pharmaceuticals, where we allege their infringement on our patent on voclosporin in an ophthalmic solution remains ongoing. In all cases, we have and are intending to continue to take action to protect our intellectual property rights for LUPKYNIS.

[...]

Well, the first that’s already been issued is the one that’s in question relative to the IPR challenge, which is our 036 patent that you all know, was the patent that was issued a couple of years ago by the USPTO based upon the observation we saw in both the AURA [ph] and AURORA where when dose adjusting downwards based on eGFR response. We actually saw improvement in terms of patient response in terms of their lowering of proteinuria. So that patent goes all the way to 2037. In addition to that patent, we have additional filings on file with the USPTO that we’ll talk more about as we get closer and as these patents issue. But I would think of these more as ring fencing strategies around the patents that we currently have.

Should AUPH lose this challenge, there's probably not much value to the company, a fact that the market is beginning to discount.

There's also a second risk:

Execution Risk

I highlighted this above, but if the company can't re-accelerate patient start forms as well as reducing overall expenses, then it will never become profitable regardless of the status of its patents. This risk is real, but secondary to the patent risk.

My Position

Considering all of this, I still think LUPKYNIS is a very valuable drug and should sell well. However, I have no way to handicap the patent lawsuit(s), and so I'm maintaining my existing position but not adding shares at today's stock price.

For further details see:

Aurinia Pharmaceuticals: Updating My Revenue And Valuation Model