ATOGF - AUTO1 Has Been Beaten Down I Think It Is A Buy Now

2023-04-17 23:52:15 ET

Summary

- AUTO1 is a European online used car dealer with a merchant and retail business.

- Shares have continuously been beaten down since the IPO in February 2021.

- AUTO1 forecast to reach profitability (on an adjusted EBITDA basis) in Q4 2023. If the company manages to do this, there is a significant upside for the share price.

- Risk comes primarily from the development of the used car market.

(Note: all amounts in the article are in EUR. At the current exchange rate 1 EUR is 1.1 USD.)

Investment Thesis

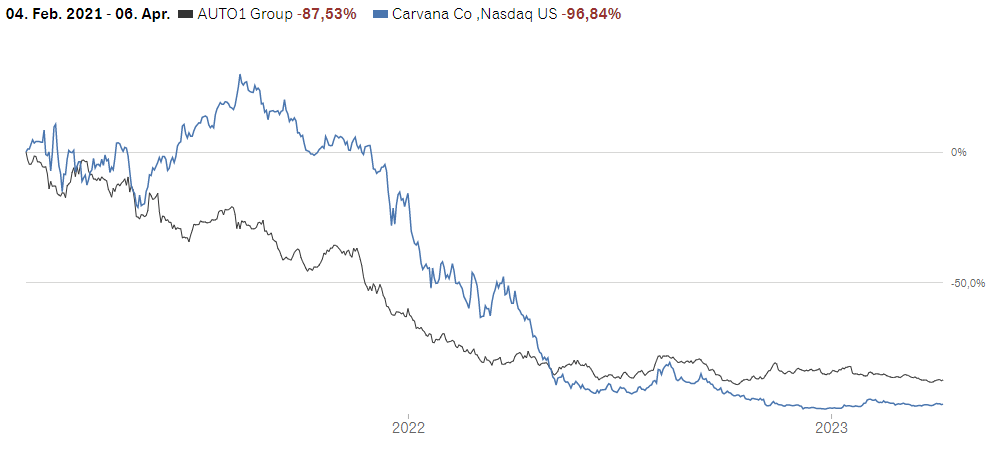

AUTO1 Group ( OTCPK:ATOGF , OTCPK:ATOGY ) certainly is an under covered stock on Seeking Alpha. The stock has only about 80 followers and just one article has been written on AUTO1 since the IPO in February 2021. The title of that article could be an explanation, Auto1 Group: The European Carvana Has A Compelling Narrative. The author obviously got something right, but not in the way he meant it. Like Carvana (NYSE: CVNA ), AUTO1 shares are down significantly, minus 74% since the publication of the article in November 2021 and minus 87.5% since the IPO:

AUTO1, Carvana stock price (Source: Handelsblatt)

{kind=link}

Despite the catchy title, the author pointed out risks and challenges with AUTO1, and he gave only a Hold recommendation.

I think it is time to look at AUTO1 again, as the company might be one of the rare cases where an investment can multiply within just one or two years. I expect that this will depend to a large degree on whether AUTO1 can manage to be reach profitability (on an adjusted EBITDA basis) in Q4 2023, as the company is predicting.

That said, AUTO1 is certainly a high-risk investment. Execution by the AUTO1 management has proven to be quite strong – at least in my view. But the development of the European used car market regarding pricing and unit sales is the big unknown here.

Why AUTO1 is probably not the European Carvana

AUTO1 and Carvana do have a very similar business model. While Carvana could be marching towards bankruptcy though, I think that AUTO1 has a good chance to reach its profitability goal this year.

The online used car dealer managed to increase gross profit every single year except the pandemic year 2020, which I think can be overlooked as an exception.

AUTO1 has not engaged in any acquisitions and has been building up the business from the ground up. The company has a solid balance sheet, enabled by the IPO, and no corporate debt. The only financial liabilities are held through two asset-backed securitization programs. At the end of 2022 debt securities in the amount of 455mn had been issued through this ABS facility. They are secured by the used car inventory and do not allow any further recourse to the AUTO1 Group.

There have been no scandals, significant customer complaints or accusations of illegal practices. On the contrary, the retail brand Autohero has 4.5+ ratings on Trustpilot across Europe:

Autohero Trustpilot ratings (Source: Trustpilot)

{kind=link}

All of this is quite unlike Carvana. The key question of course is whether the company has a business model that will lead to profitability, and when. I am very confident on the principal profitability question. AUTO1 has forecasted EBITDA profitability in Q4 2023 at the time of the IPO and they have been upholding this prediction since then. The key risk is the condition of the used car market over the year.

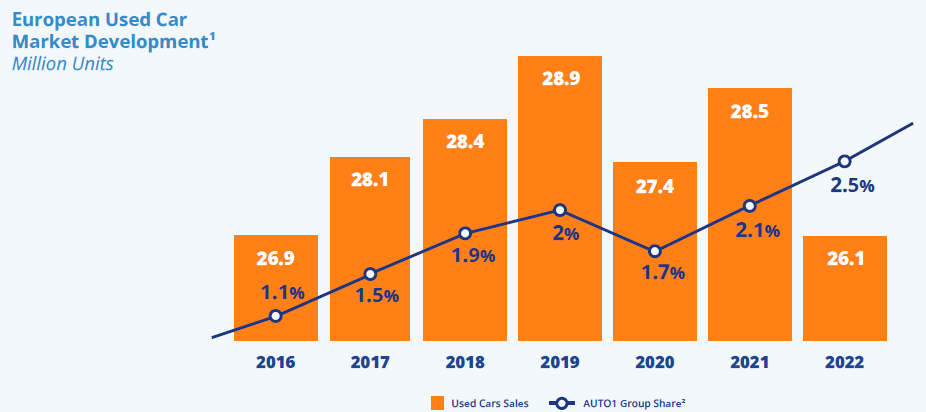

AUTO1 grew in 2022 more than the market, but below expectations

The European Used Car market declined in 2022 with only 26.1mn units sold. In 2021 28.5mn used cars were sold, so -8.4% YoY. As you can see in the graph below, the pre-pandemic high was in 2019 with 28.9mn used cars sold across Europe.

European used car market in 2016-2022 (Source: AUTO1)

{kind=link}

AUTO1 increased its market share to 2.5%, which does not look like much, but was enough to make the online used car dealer the leader in this fragmented market. AUTO1 operates across Europe, but not in the UK. Based on customer location, Germany, France and Italy make up around 50% of revenue .

AUTO1 key metrics in 2022 (Source: AUTO1)

{kind=link}

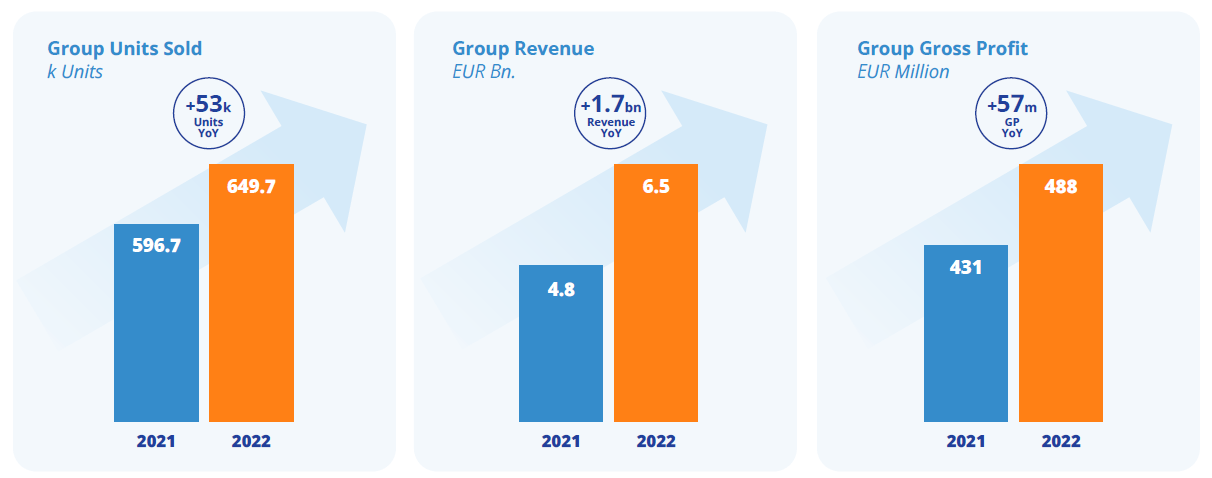

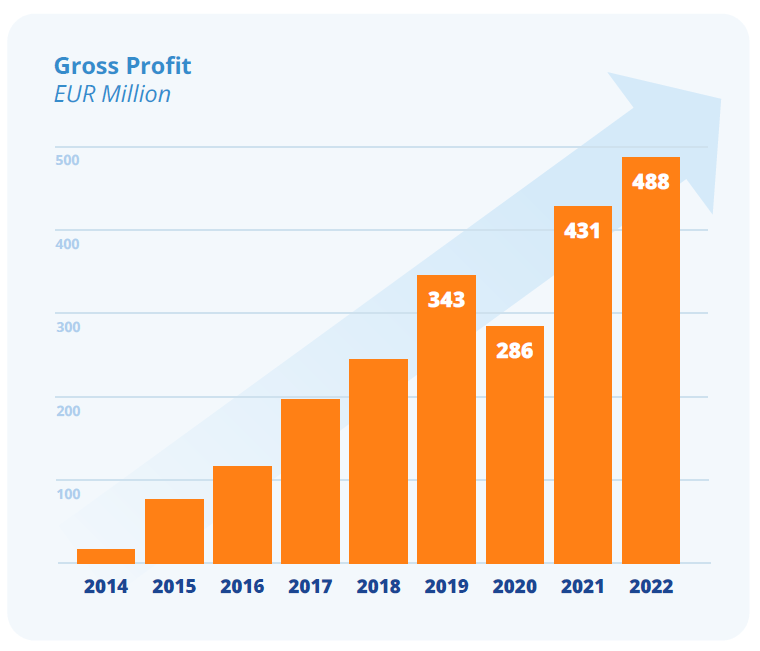

Despite the decline in the size of the total used car market after 2019, AUTO1 has continuously increased gross profit - the pandemic year 2020 beginning the one exceptional year where gross profit has not increased.

AUTO1 gross profit 2014-2022 (Source: AUTO1)

{kind=link}

Merchant bu s iness

AUTO1 has two business segments, Merchant and Retail. In the Merchant segment used cars are sold to commercial car dealers through the AUTO1.com brand. Dealers can also sell used cars through the platform. AUTO1 claims that more than 60,000 partners in over 30 European countries are using AUTO1.com.

An interesting thing here is that AUTO1 uses algorithmic pricing and they recently started publishing the AUTO1 Group Price Index , which shows the monthly evolution of wholesale used car sale prices across Europe since 2015, based on around 3.6 million used car transactions. There is supposedly a stock of more than 30,000 inspected used cars on the platform, with 3000+ cars being added on a daily basis. Dealers, manufacturers, leasing, and rental car companies can sell cars within 24 hours online and across European borders to the connected dealer network.

Cars are purchased either from private individuals (which is the majority and AUTO1 labels this as C2B) or from commercial fleet operators and dealers (which AUTO1 labels as Remarketing). AUTO1 runs localized websites like wirkaufendeinauto.de or vendezvotrevoiture.fr (in English: we buy your car) to source cars from private individuals.

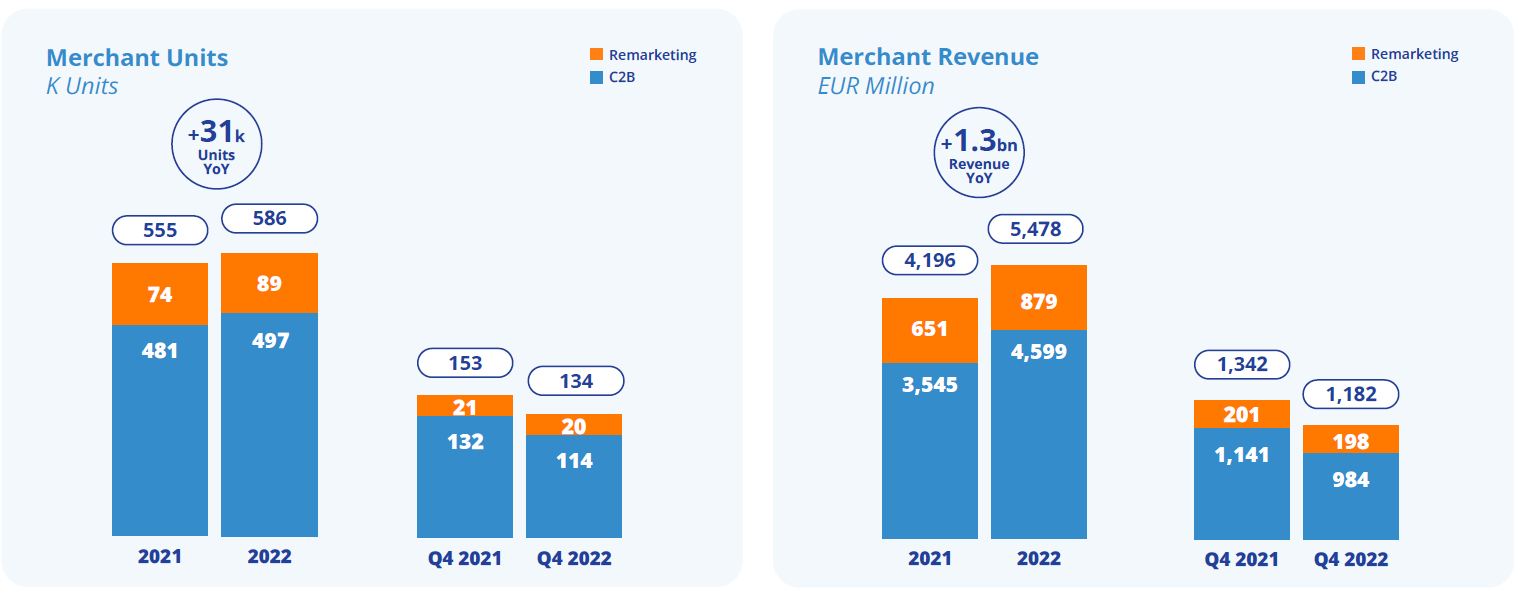

While both units and revenue grew YoY over the full fiscal year 2022, Q4 saw a deterioration.

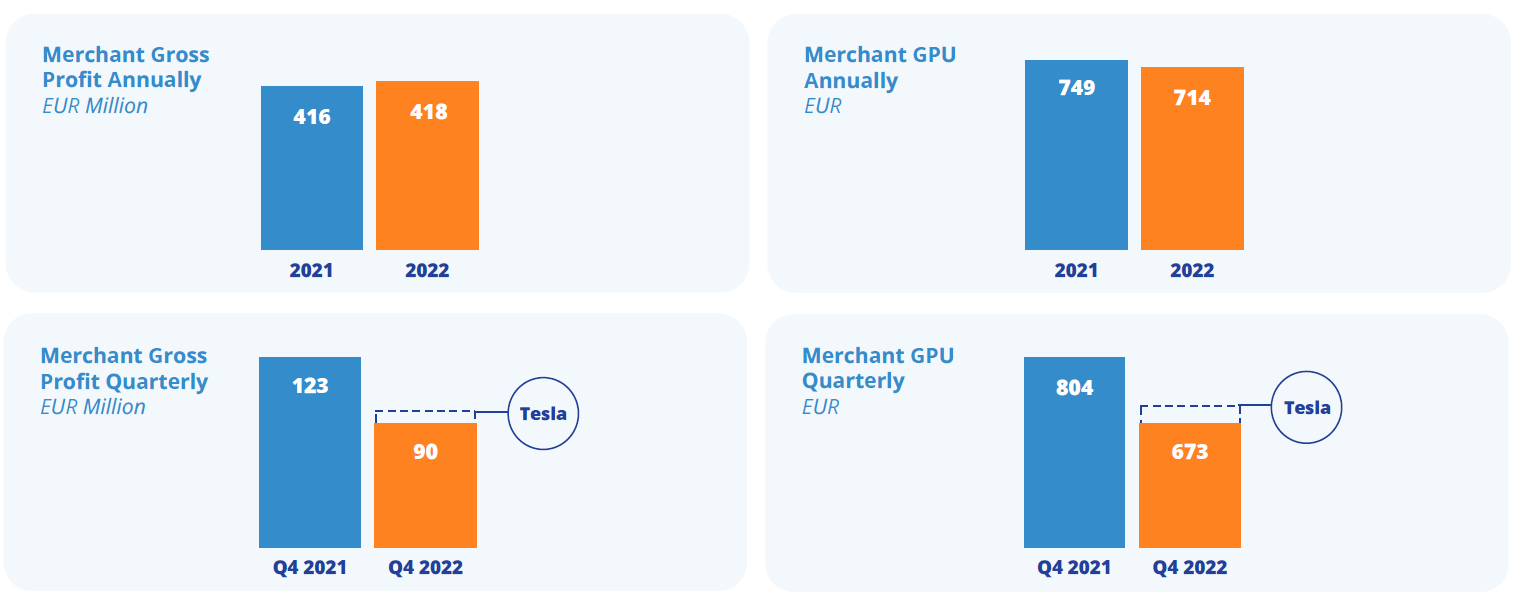

AUTO1 Merchant Units sold, Revenue 2022 (Source: AUTO1) AUTO1 Merchant Gross Profit, Gross Profit per Unit 2022 (Source: AUTO1)

{kind=link}

{kind=link}

You probably have noticed the Tesla (NASDAQ: TSLA ) circle in the profitability graph. AUTO1 explained this on the Q4 earnings call as inventory write downs due to Tesla price reductions. I am mentioning this because there seems to be significant sensitivity in the business to used car prices and short-term changes to those.

Retail business

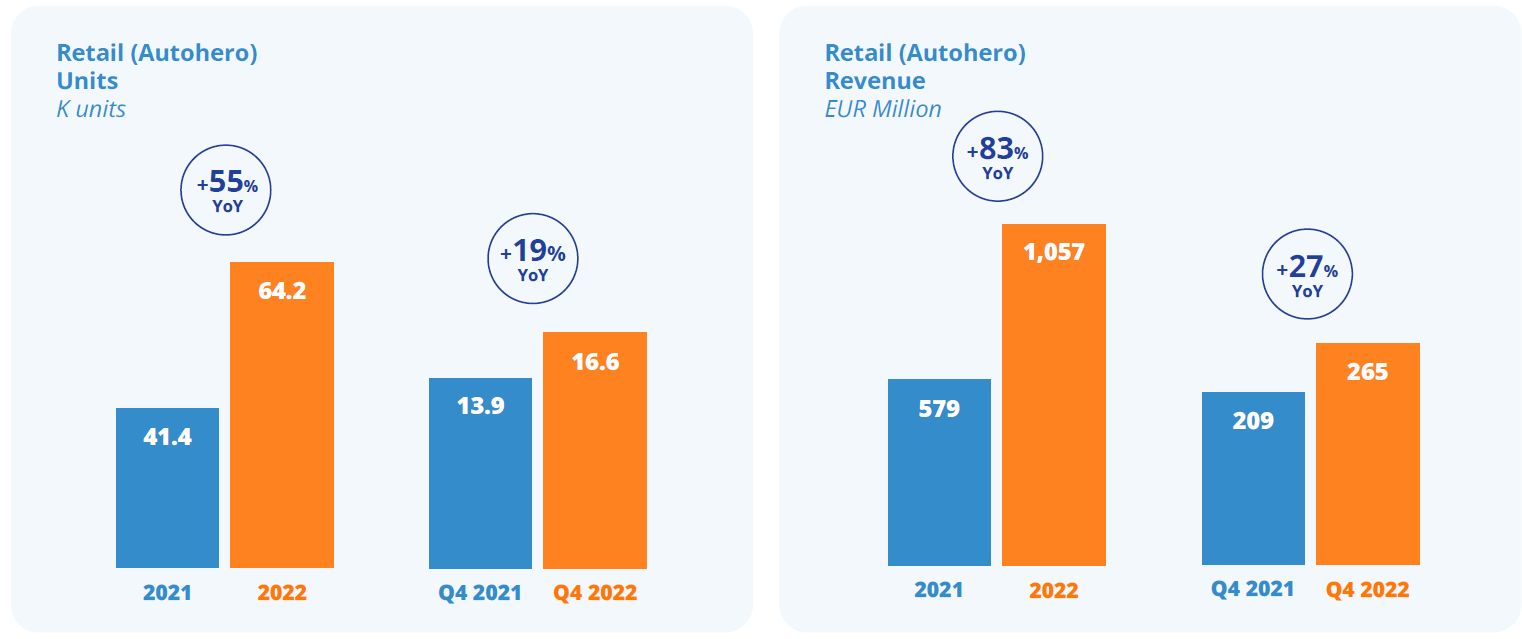

The Retail business, albeit smaller than the Merchant business, has shown a strong and continuous growth in 2022, including Q4.

AUTO1 Retail Units sold, Revenue 2022 (Source: AUTO1)

{kind=link}

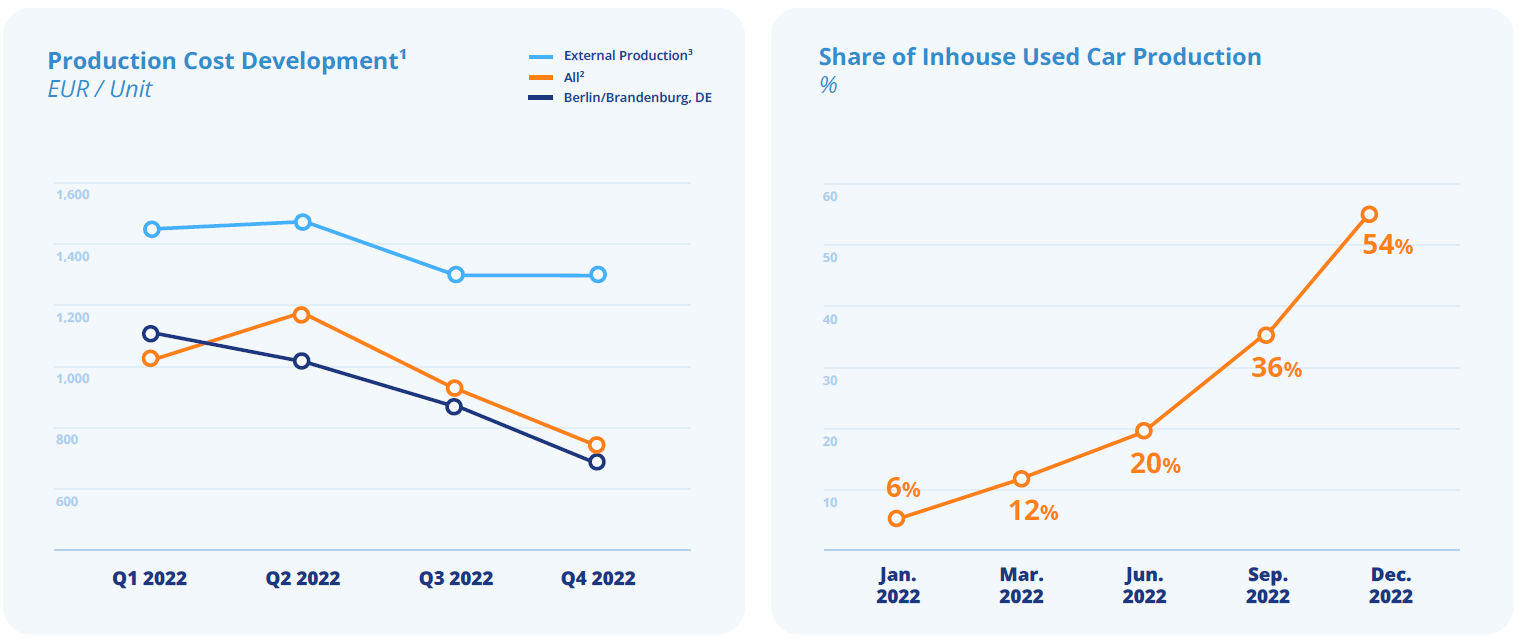

Cost reductions through in-housing of the used car production have been a major driver. As you can see in the chart below, in-house production is 50% cheaper than external production. The company now has 7 production centers across Europe in Germany (2), Spain (1), Italy (1), Belgium (1), the Netherlands (1) and Poland (1). The total annual capacity from in-house production is now 147,400 cars, and the share of cars refurbished internally grew from 6% in January to 54% in December.

AUTO1 in-house production (Source: AUTO1)

{kind=link}

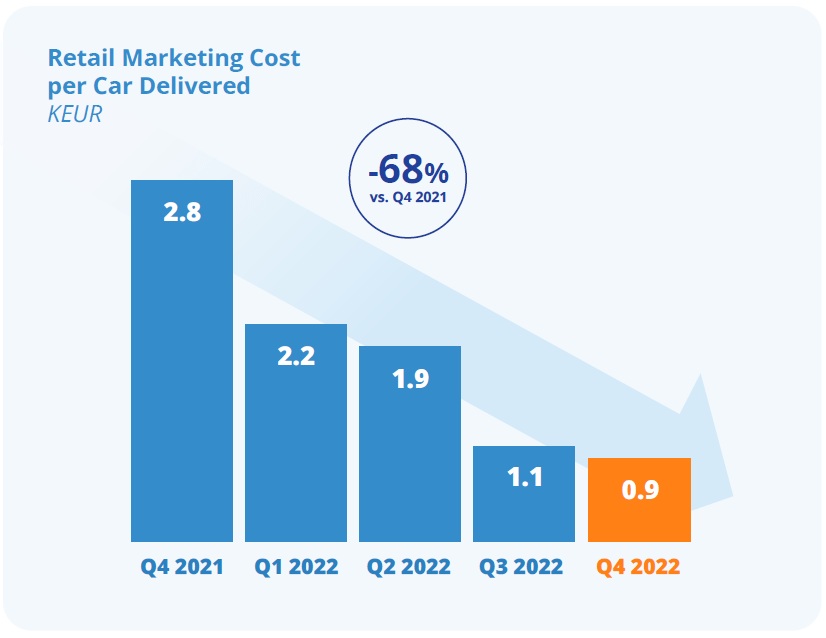

Another improvement on the cost side was a significant reduction in marketing cost. Marketing cost per car delivered went down to EUR 900 from EUR 2,800 a year ago:

AUTO1 Retail marketing cost per car delivered (Source: AUTO1)

{kind=link}

One more nice thing to see is that AUTO1 is quite aggressively expanding the consumer loans portfolio, which should help with increasing GPU going forward. Currently the company offers financing only in Germany and Austria. The financing portfolio in those two countries grew to 185mn in 2022, up 277% YoY.

Path to profitability

AUTO1 says that the company will be profitable on an adjusted EBITDA basis in Q4, so not for the full year. But this is in line with the forecast that was done during the IPO.

In 2022 GAAP EBITDA was -182.9mn and adjusted EBITDA was -165.5mn. About half of the difference came from stock-based compensation. AUTO1 does not give details for the other half, the annual report just says that it is other non-operating expenses. With 17mn, the difference is not huge though, and it was a similar amount in 2021. Stock based compensation increased though from around 5mn to 8mn in 2022. I am not too worried about it, as the numbers are relatively small.

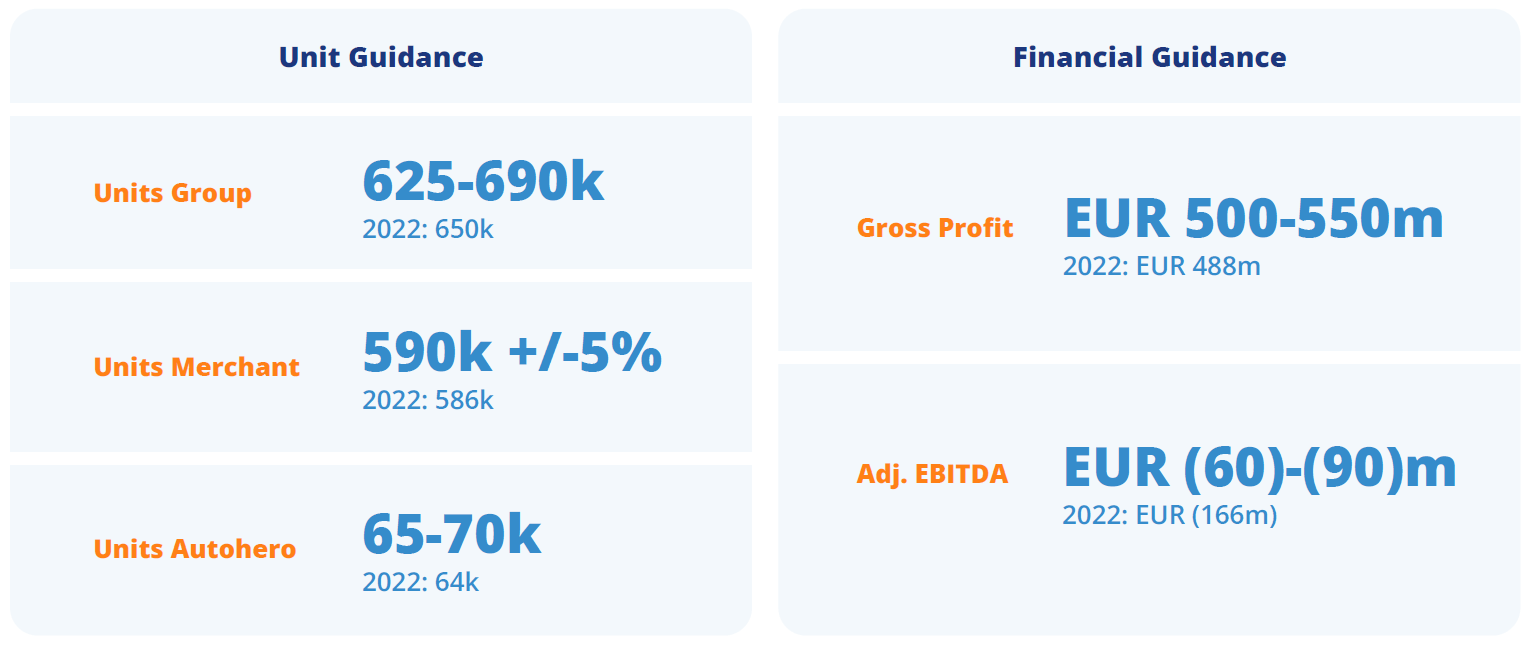

The management assumptions underpinning the path to profitability look reasonable to me. AUTO1 does not assume strong growth on the top line in 2023.

AUTO1 2023 guidance (Source: AUTO1)

{kind=link}

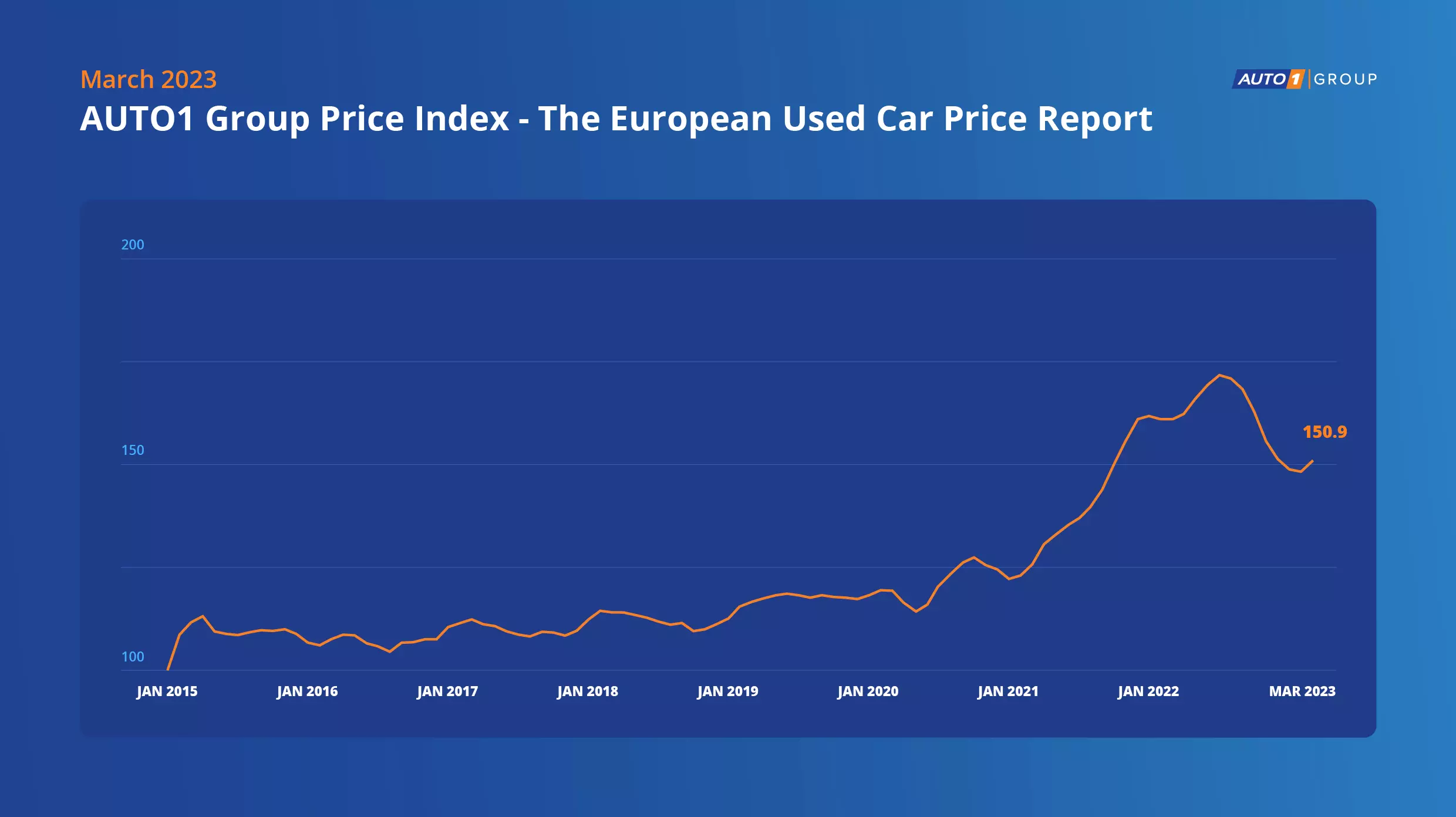

I prefer this to aggressive growth assumptions that depend on external factors, with a disappointment and excuses at the end. I do not think that the used car market in 2023 will be very strong. Beginning of April, AUTO1 said in a press release that used car prices have stabilised in Q1 2023, but they are still below their 2022 levels:

AUTO1 Group Price Index (Source: AUTO1)

{kind=link}

How to value AUTO1?

As AUTO1 is not profitable yet, it is quite hard to put a target value on the stock. I do not think it is very helpful to consider the IPO price of EUR 38 as a relevant number. The stock, which is now at EUR 7, could not see its IPO price again for years to come. I think the best way to look at the company is sales potential, gross profit per unit and the margin from that.

As we have seen, AUTO1 has managed to grow unit sales in 2022 even in an overall shrinking market. In the Merchant segment the market shrank by 8% while AUTO1 grew by 5%. This is an outperformance of 13%.

Averaging the last 5 years for the European used car market (and I do not see a reason why the total market itself should grow) gives us an addressable market of 27.9mn units.

I think it is reasonable to assume that AUTO1 can keep growing its market share. It has been doing this continuously except for the pandemic year 2020 and the trend towards online sales will continue to be a strong tailwind in my view. If we assume a 4% market share from the 2.5% where the company is now, we get to 835,000 units per year.

Next, looking at gross profit per unit – AUTO1 had a GPU of 746 euros in 2022. This is quite low compared to U.S. peers. CarMax (NYSE: KMX ) just recently announced results for Q4. Retail GPU was at USD 2.277 and wholesale GPU at USD 1.187.

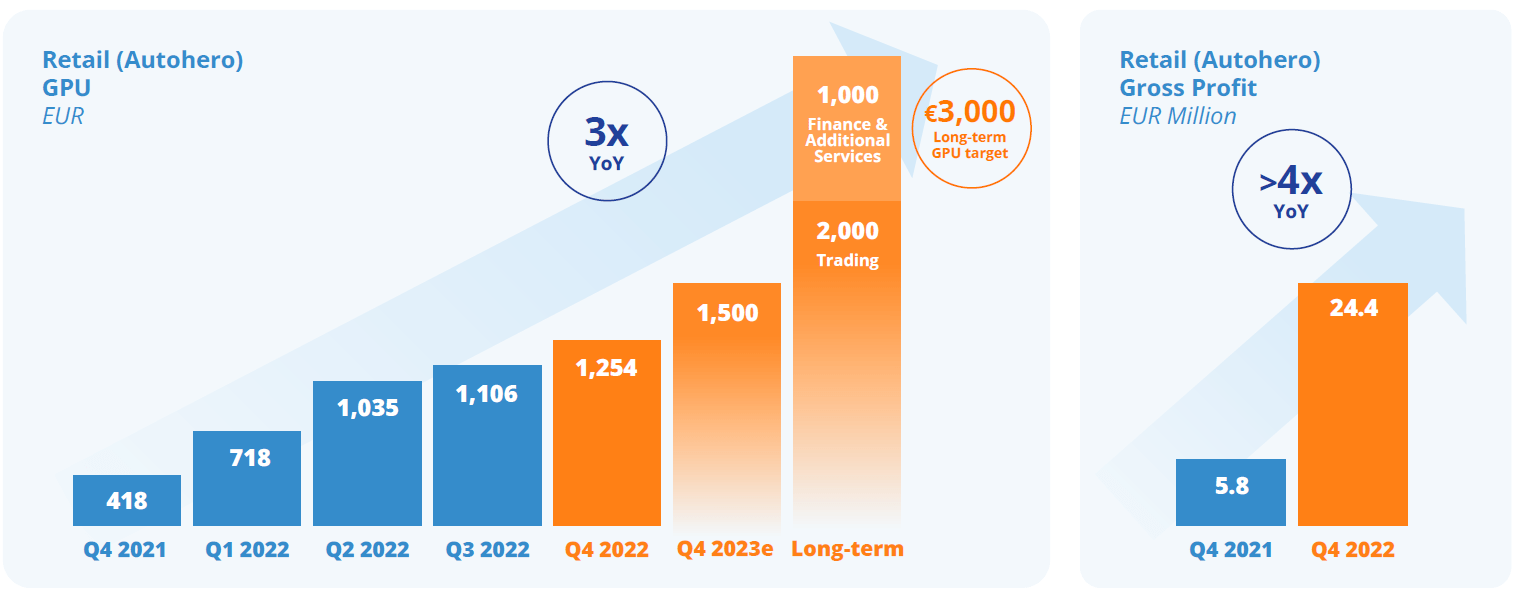

The lower GPU in the Merchant business is driving the AUTO1 number. On the Retail side, where AUTO1 intends to grow, GPU was 1,254 euros in Q4. This is still well below CarMax (not to speak of Carvana). AUTO1 predicts a significantly higher GPU in the Retail business going forward, although this is one case where I find their predictions quite aggressive.

AUTO1 Retail GPU (Source: AUTO1)

{kind=link}

I am more comfortable assuming an average GPU of 1,250 across the Retail and Merchant business (in line with the current Retail GPU), at least for the next years.

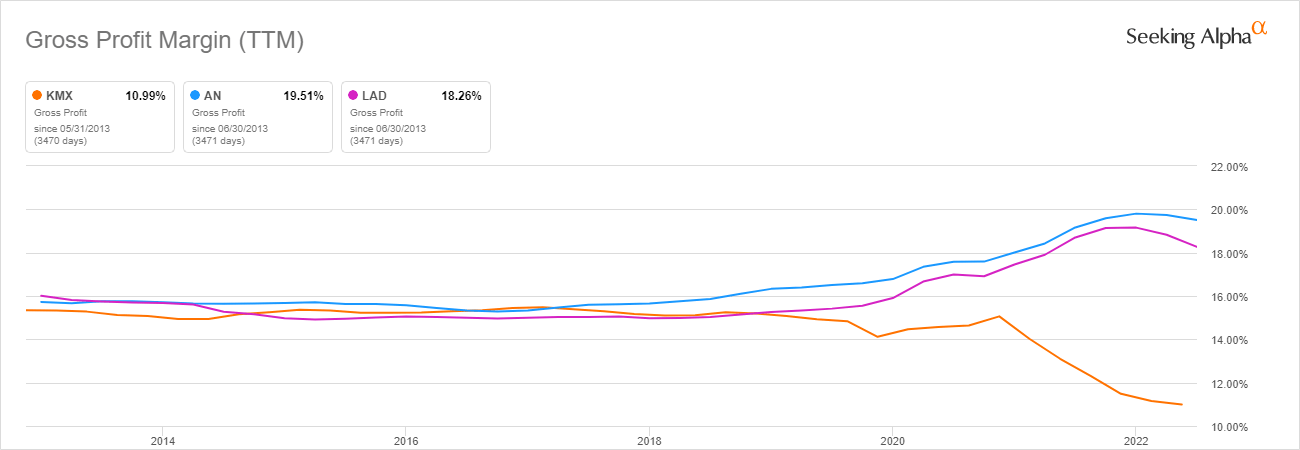

This leaves us with an assumption on the profit margin we think AUTO1 can achieve. There is a lack a peer companies in Europe, especially publicly traded ones with available financial numbers. So I looked at CarMax, AutoNation (NYSE: AN ), and Lithia Motors (NYSE: LAD ) in the U.S. I am aware that those companies operate in a different geography and that there are business model differences. Their historic gross profit margins have been at 15% and this is still the average, although AutoNation and Lithia Motors have been doing better recently and CarMax has been doing worse.

Gross profit margin CarMax, AutoNation, Lithia Motors (Source: Seeking Alpha)

{kind=link}

So I am going with the 15% profit margin as an assumption - which leads to annual earnings of more than 200mn (209mn exactly) and, even if we put only a multiple of 15 on it, a value of more than 2x the current market cap.

I think, if AUTO1 can keep growing its market share as I assumed above, quite significant platform and scaling effects will kick in, enabling even further growth. So a multiple of 15 would be in the low side in my view, but even this gives us a significant upside on the share price.

I am of course not making a prediction here, as there are a lot of uncertainties, but just showing the art of the possible with (what I think are) relatively moderate assumptions.

Conclusion

AUTO1 has been so beaten down that I think the risk/reward ratio is very good now. There is a further downside risk if the used car market deteriorates more (which is certainly possible), but I think this is probably a limited and temporary risk. On the other hand, if AUTO1 reaches profitability this year the stock price has significant upside potential.

A final remark for U.S. based investors: besides ATOGF shares (listed on the Frankfurt stock exchange) there are also ADRs, but I recommend buying ATOGF if you can do this through your broker. With the current market cap of 1.49bn, AUTO1 is small enough for a takeover. 25.3% of shares are held by founders and 18.2% by SoftBank ( OTCPK:SFTBY ), so a deal would be not too difficult to do. In the event of a takeover (and I have absolutely no indication of this) I would prefer holding the ATOGF shares.

For further details see:

AUTO1 Has Been Beaten Down, I Think It Is A Buy Now