ADSK - Autodesk: A Compounder Bargain

2023-05-17 17:19:47 ET

Summary

- Autodesk, Inc. continues to maintain market leadership in its software offerings.

- Ongoing initiatives maintain a long trajectory for growth.

- The valuation looks to be in a good spot, and free cash flow continues to compound higher. With Q1 earnings expected next week, Autodesk stock is a buy.

Looking at one of my favorite stock picks over the long term after its investor day, I was reminded of the many reasons why I originally purchased Autodesk, Inc. ( ADSK ). The company is committed to profitable growth and maintains a massive moat in its niche. The products are part of a virtuous cycle, with students learning and becoming proficient, leading to further penetration in the professional community.

Company Presentation

The company offers product licenses free to universities and some small startups in the hope of further marketplace adoption. This strategy has borne out with market-leading software products and a wide moat.

One of the other factors to consider is the difficulty in using these products. The software the company offers is nuanced, including 3D modeling for manufacturing, movies, architecture, etc. Getting proficient may take a matter of months, but mastery can take years of diligent practice. For professionals who have been trained on the software since college, transitioning to a different product and restarting the learning curve is not something most people would want to do.

Autodesk has also pushed for universal file formats. This allows their product to interface with other products in the marketplace, including competitors. This reduces the likelihood of lock-in to one ecosystem and improves the overall efficiency of the project. Although this could be a double-edged sword, Autodesk's offerings typically lead the market and this improves the overall marketplace, removing a reason for potential customers to be wary of a switch.

{kind=link}

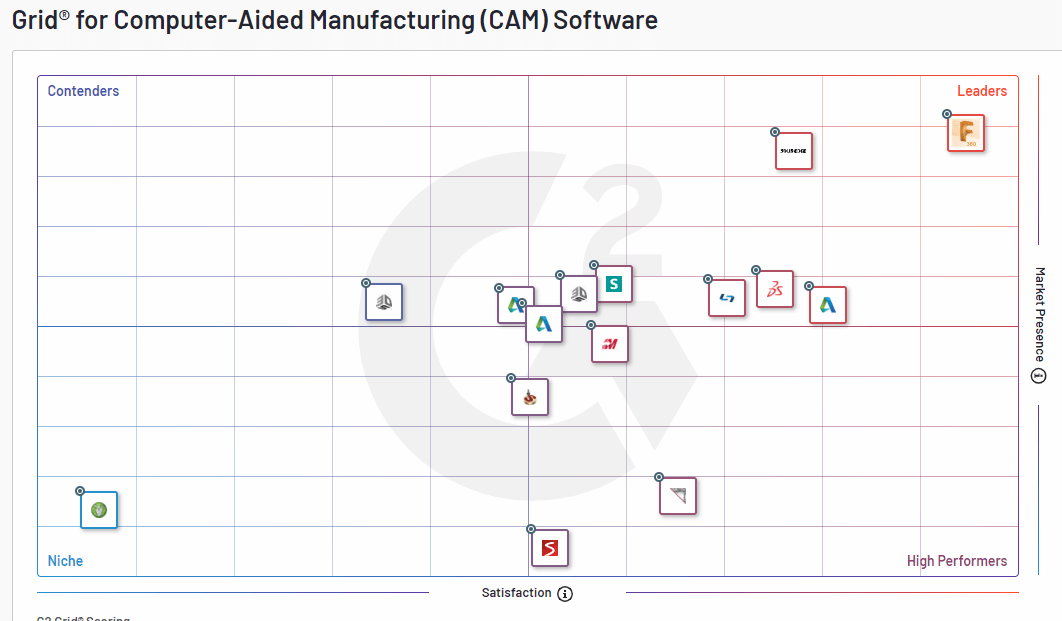

Looking at the G2 grid for Computer-Aided Manufacturing software, Autodesk's Fusion is well in the lead in performance and market presence, with few competitors close behind.

These grids are based on G2's algorithm and can be a useful tool for investors to look at software offerings that may not be used outside of some professional arenas.

{kind=link}

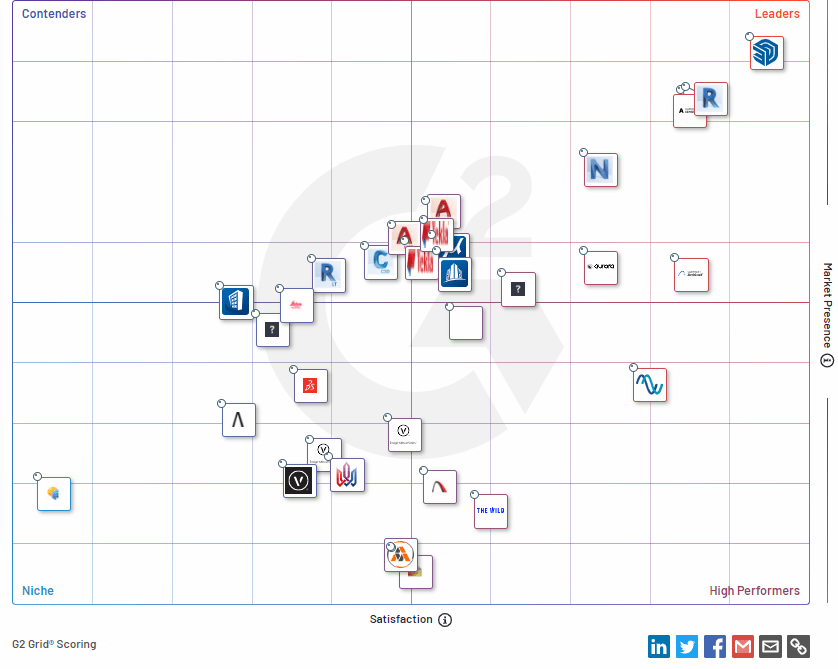

Looking at the areas Autodesk competes in, the company's offerings are well-regarded. Revit and AutoCAD are slightly behind SketchUp here, but it is basically just the three of them on top of the mountain.

{kind=link}

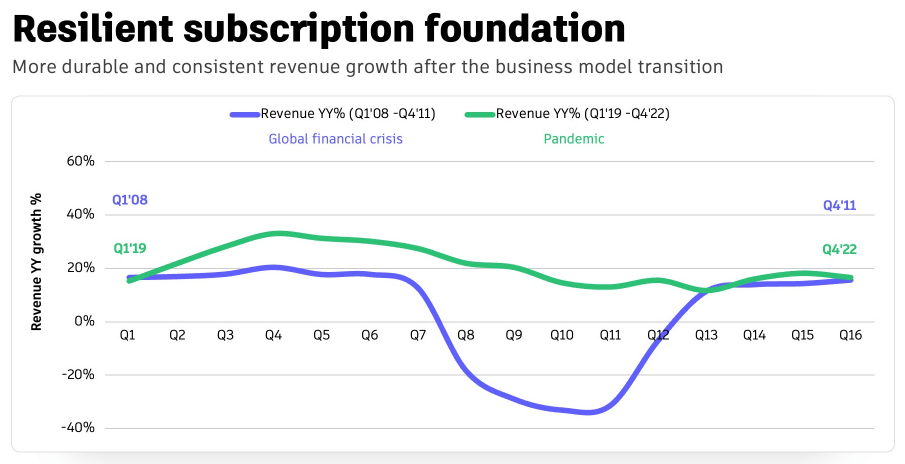

Autodesk transitioned to a recurring subscription model a few years ago, a move most software companies undertook to provide resilience in revenues, forecasting, and above all some resistance to the boom-bust of the economic cycle. The great financial crisis wasn't great for Autodesk, who is materially affected by the construction and manufacturing industries. However, this is somewhat mitigated with annually recurring software subscriptions the larger companies and governments are unlikely to cancel despite economic conditions.

The company is now transitioning its multi-year contracts to annual terms in order to provide more opportunities for upsell. There are two sides to the coin, since annual subscriptions could raise churn, but the company's calculus is the opportunity to load up more offerings once a year is worth any additional cancellations. This will negatively impact free cash flow ("FCF") in 2024, as it affects the timing on when billings are booked, which should rebound back to normal in 2025.

{kind=link}

Looking at growth prospects, there are a few worth noting. The upcoming FedRAMP approval opens the door to multiple Autodesk offerings tailored specifically to the government. The company has relationships with departments of transportation around the country, and the government relationship should be a lucrative and sticky one for long-term contract value.

The company is also pushing more towards self-service. I was somewhat surprised this wasn't already an initiative, but this could significantly lower the company's S&M expense over time as companies can handle more of the onboarding themselves.

{kind=link}

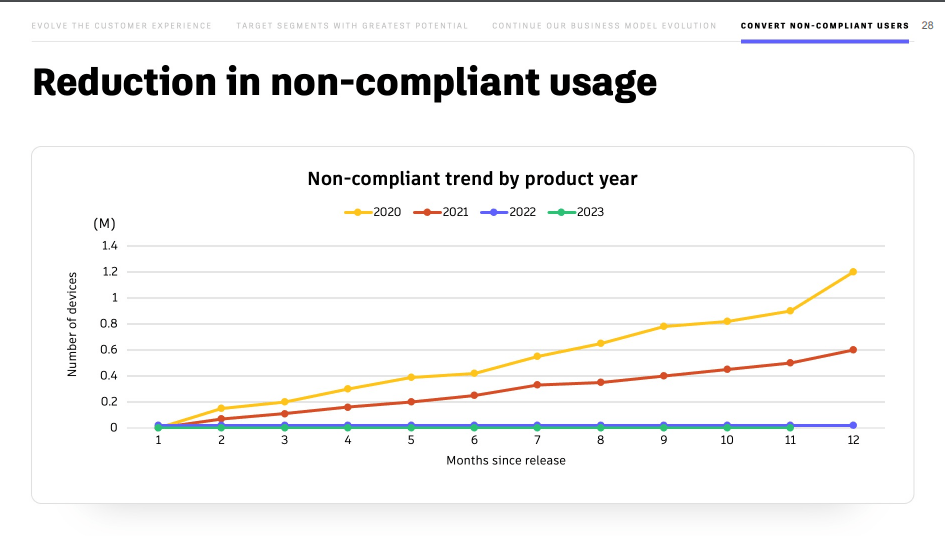

Separately, the company still faces an uphill battle with non-compliant users utilizing the software without a license. Estimates have around 12M non-compliant users against the company's total paying user base of 8M. Initiatives thus far have fallen somewhat flat, including in-app messaging. In my opinion, the in-app messages are more of a nuisance, and ultimately users aren't likely to even read them, especially if it's repetitive every time an application is opened. However, the company has also removed offline activation and instituted concurrent user limits for its licenses. If management is able to gain traction on converting non-compliant users to even a low-tier offering, it could be a boon.

The most recent Q4 results (ADSK is expected to report Q1 results on Thursday, May 25 post-market) were solid for the company, which rarely sets the world on fire but continues to compound away hitting targets. Revenues grew 12% constant currency (Autodesk generates around 58% of its revenue from outside the U.S.), billings grew 28% on the back of multi-year discount removals, and operating margins were up around 1% on the quarter and 4% on the FY to 36% non-GAAP. The company's gross margin of 92% is incredible and should be the goal for every long-term established software company.

Management guidance for FY24 came in at 13% revenue growth and $1.15-1.25B in free cash flow. Longer-term targets of 10-15% revenue growth, a rule of 40 of 45%, and lowering stock-based compensation to 10% of revenues or lower are laudable.

Free cash flow hit an inflection point with the transition to SaaS and has been growing strongly since. Long-term debt remains very manageable.

Weighing the company's metrics against peers in the same growth cohort, Autodesk measures out well. At 7.8X next twelve months' revenue and 30X free cash flow, the company isn't cheap on an absolute basis. However, the company's 20% GAAP operating margin and 90% GAAP gross margin are among the best-in-class. This is accomplished by 13% stock-based compensation, 11% G&A, 24% R&D, and 35% S&M against revenues. All of these figures are where you want to see them for the best cloud companies. With a rule of 40 of 50% on 40% free cash flow margin, these metrics help the fact next twelve months' revenue growth is lower than some of the high-flyers.

{kind=link}

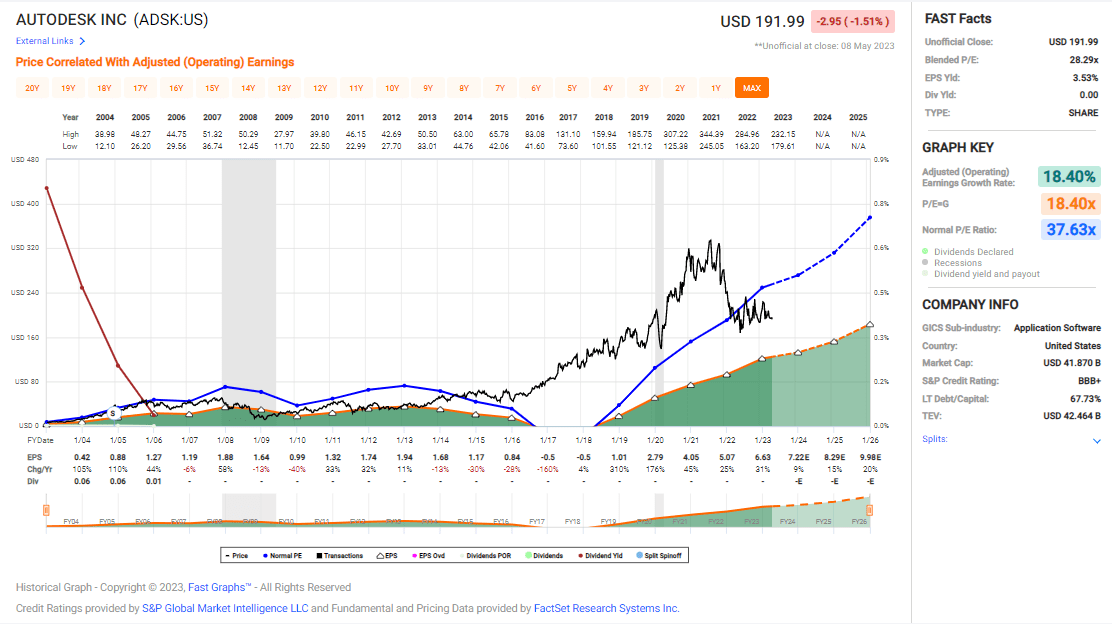

Looking at the company's valuation against earnings, it's pretty obvious when the company transitioned to the subscription model. The company wasn't immune to the crazy tech run-up, but the valuation is back to its nominal post-2017 trajectory, and high 20s multiples seem fair.

{kind=link}

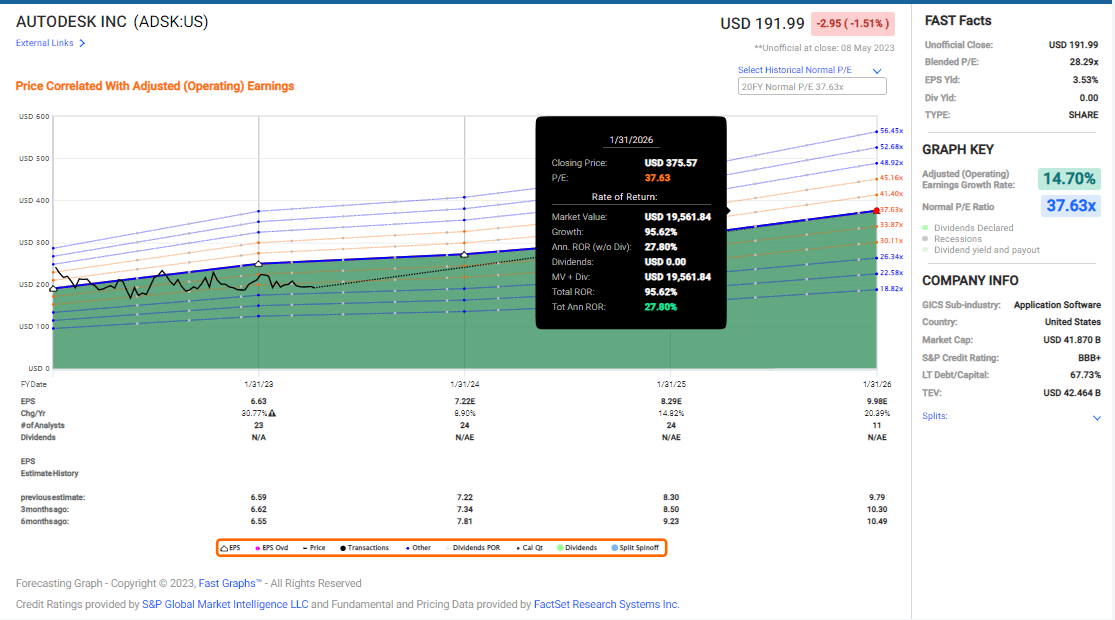

Based on analyst estimates for earnings growth and a return to around 37X earnings, an investment today could yield around 27% annualized. However, I like the valuation today and continue to scoop up shares. Regardless, the company is projected for double-digit earnings growth in excess of revenues in 2025 and 2026.

{kind=link}

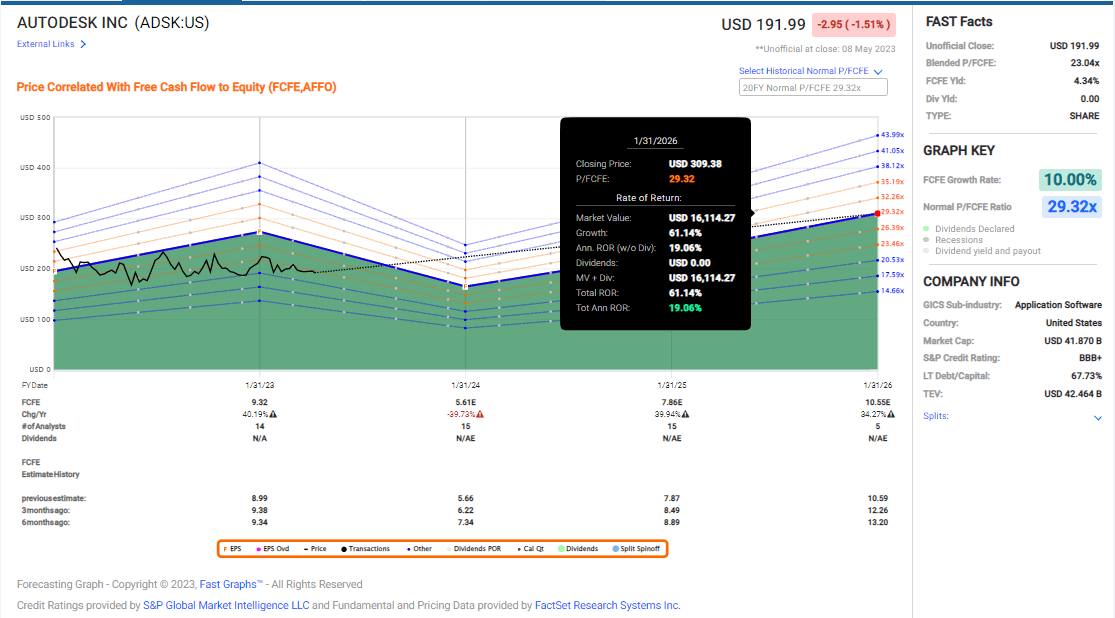

Looking at free cash flow projections and a return to around 30X, an investment today could yield around 19%. This is more in line with earnings growth and accounts for the free cash flow hit the company will take due to the shift away from multi-year contracts next year. This is based on the timing of its billings and is not related to the actual fundamentals of the business.

Autodesk continues to churn away, innovating its products and generating cash. The valuation is fair today, the company's growth prospects look solid, and management has maintained strong operating metrics. It may not be the flashiest, but I consider it a cornerstone of my portfolio, and it's a buy today.

For further details see:

Autodesk: A Compounder Bargain