ADSK - Autodesk: Billing Changes Affect Free Cash Flow But It's Likely Temporary

2024-01-09 04:16:23 ET

Summary

- Autodesk has successfully transitioned from a licensing model to a subscription-based model, resulting in accelerated revenue growth and increased operating profits.

- The shift from multi-year contracts to annual subscriptions has impacted upfront payments and reduced free cash flow, but a recovery is expected in FY24.

- Despite challenges in cash flow, Autodesk maintains solid topline growth and a strong outlook, with a 9% revenue growth floor for the next fiscal year.

Autodesk ( ADSK ) is a leading player providing software and cloud subscriptions for the Architecture, Engineering, and Construction ((AEC)) end-market. Like some other software players, they initiated their transition from a licensing model to SaaS a few years ago. They have achieved double-digit revenue growth with decent operating profit growth. However, the current shift in billing from multi-year contracts to annual subscriptions is expected to result in lower upfront payments from customers, thereby reducing their free cash flow generation. I believe their free cash flow hit its lowest point in FY23 and should begin recovering in FY24. I am initiating coverage with a 'Buy' recommendation and a fair value of $250 per share.

Business Transition from License to SaaS

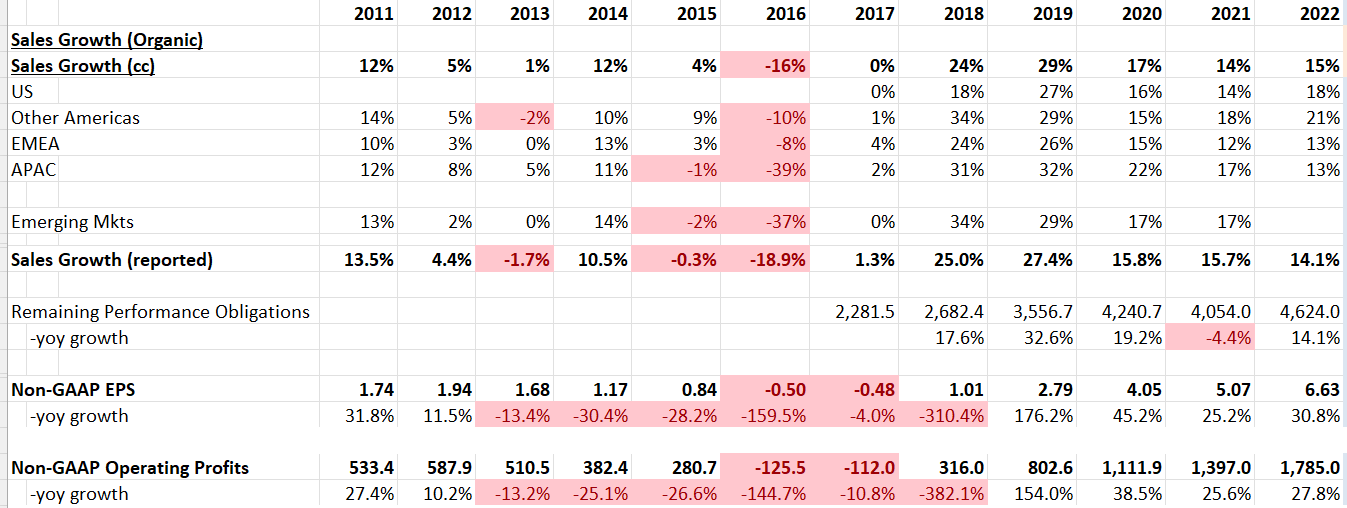

It is indeed reasonable for software companies to transition to a subscription-based model, as it enables them to generate more recurring revenue and provides increased visibility. Additionally, this model eliminates the need for customers to make a substantial upfront payment for license purchases, opting instead for manageable monthly subscription fees. Since implementing this business transition, Autodesk has experienced accelerated double-digit growth in topline revenue, as illustrated in the table below. Furthermore, the shift has positively impacted their adjusted operating profits, leading to notable growth over the past few years. It's important to note that in this article, FY22 refers to FY23 in Autodesk's earnings release, as their fiscal year ends on January 31.

{kind=link}

In a SaaS business transition, similar to what Adobe ( ADBE ) underwent many years ago, the transitioning company typically experiences initial deceleration in both revenue growth and free cash flow. However, as time progresses, these metrics tend to accelerate in the later years. Autodesk's growth pattern aligns quite closely with this trajectory. I believe their management made the right decision in transitioning their products to the cloud and adopting a subscription model.

Notably, Autodesk's offerings such as BIM 360, Autodesk Build, Fusion 360, ShotGrid, and the AutoCAD web app provide comprehensive cloud solutions for their customers. This strategic move not only reflects the industry trend but also positions Autodesk to cater to evolving customer needs in a rapidly changing technological landscape.

From Multi-year Contract to Annual Subscription

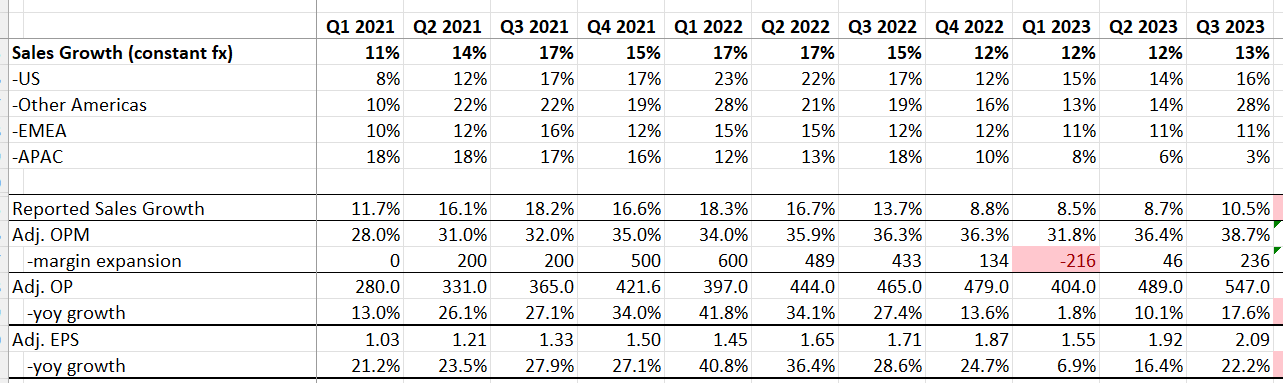

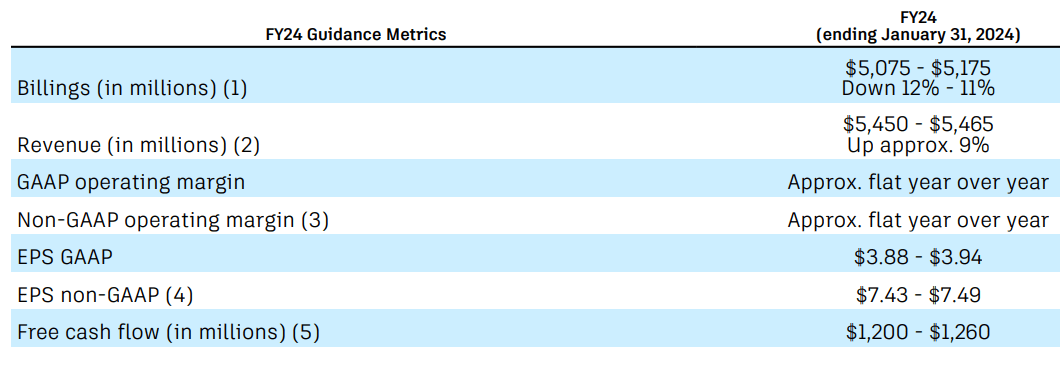

In Q3 FY23 , Autodesk experienced billing changes, transitioning from upfront to annual billings for multiyear contracts, resulting in an 11% year-over-year decline in billings. This shift poses growth headwinds for their free cash flow, as the company now receives fewer upfront payments from customers. The guidance for free cash flow this fiscal year is in the range of $1.2-1.26 billion, significantly lower than the $2 billion reported in the last fiscal year.

The management acknowledged that FY23 would mark the trough for free cash flow. I anticipate a gradual recovery beginning in FY24, with acceleration in FY25. Despite the challenges in cash flow, their topline growth remains notable, boasting a 13% increase in Q3 FY23. Additionally, adjusted operating profits grew by 17.6% year over year, as illustrated in the table below. It's important to note that the billing changes primarily impact accounting and cash flow, not the Profit and Loss statement. The underlying health of their business appears robust, with solid growth trends.

{kind=link}

Secondly, Autodesk continues to enter into multi-year contracts as part of their standard operating model, indicating no significant changes in their business approach. While acknowledging that the free cash flow pattern will experience adjustments in FY23 and FY24, particularly due to billing changes, it's important to note that over the long term, the total cash flow is expected to remain consistent.

Finally, despite potential impacts from the current macro environment on renewal rates, Autodesk maintains a solid 9% revenue growth floor for the next fiscal year. Notably, they have emphasized in recent conference meetings that this figure represents a floor, not just guidance. This stance reflects the management's optimism about sustained revenue growth. It is anticipated that the topline and profit growth will counterbalance the challenges posed by the billing changes, providing a positive outlook for the company.

Financial Results and Outlook

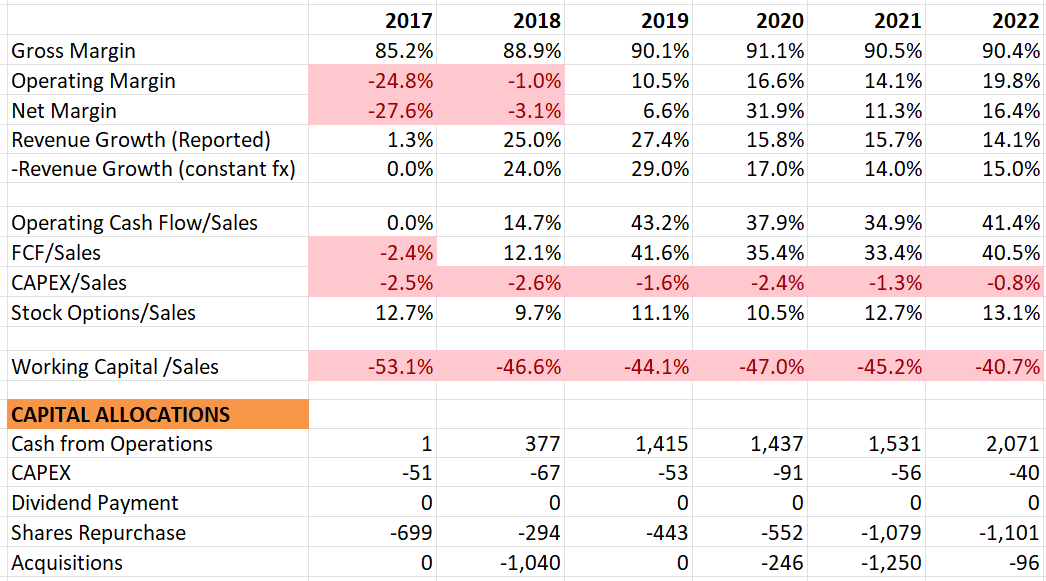

Historically, Autodesk has maintained a robust gross margin, and their operating margin has trended towards surpassing 20%. The company has strategically utilized its cash flow for share repurchases and acquisitions. Operating with an asset-light business model, Autodesk typically allocates only around 2% of group sales to capital expenditures on average. The company's balance sheet is notably strong, characterized by a minimal net debt position.

{kind=link}

In 2021, Autodesk acquired Innovyze for $1 billion. Innovyze, a global leader in water infrastructure software, is expected to enhance Autodesk’s design and analysis solutions, including products like Autodesk Civil 3D. This strategic acquisition makes sense in broadening Autodesk’s software offerings.

In 2021, Autodesk acquired UpChain , a cloud-based product lifecycle management platform. I believe UpChain’s solutions could seamlessly integrate into Autodesk’s centralized data management and process management platforms. These acquisitions are tuck-in in nature.

In their current year guidance, they anticipate a 9% increase in revenue, with billings expected to drop by 11-12% due to the transitions in multi-year contracts. As discussed earlier, I anticipate a recovery in their free cash flow in the next fiscal year, gaining full growth momentum in the subsequent year.

{kind=link}

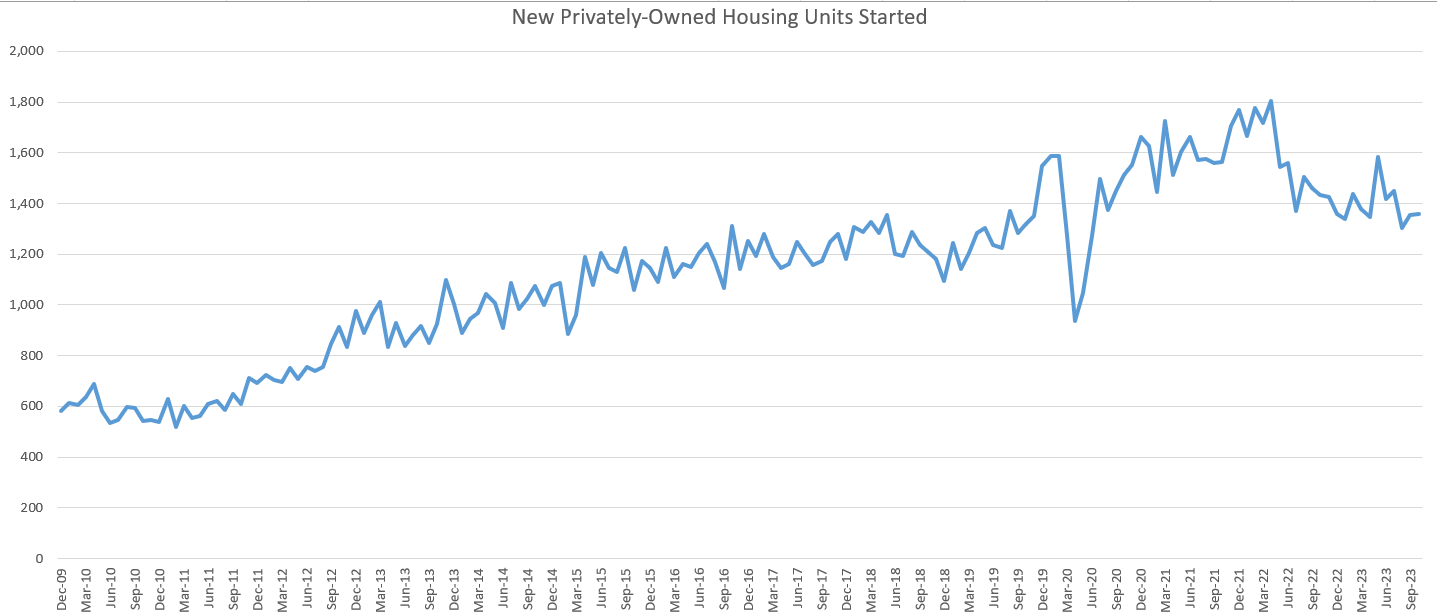

To some extent, Autodesk’s business is linked to construction activities, encompassing residential, commercial, and infrastructure projects. While housing starts have declined from the peak during the pandemic period, they remain at a reasonable level. In my view, there is no immediate concern for a housing crisis.

{kind=link}

Valuation

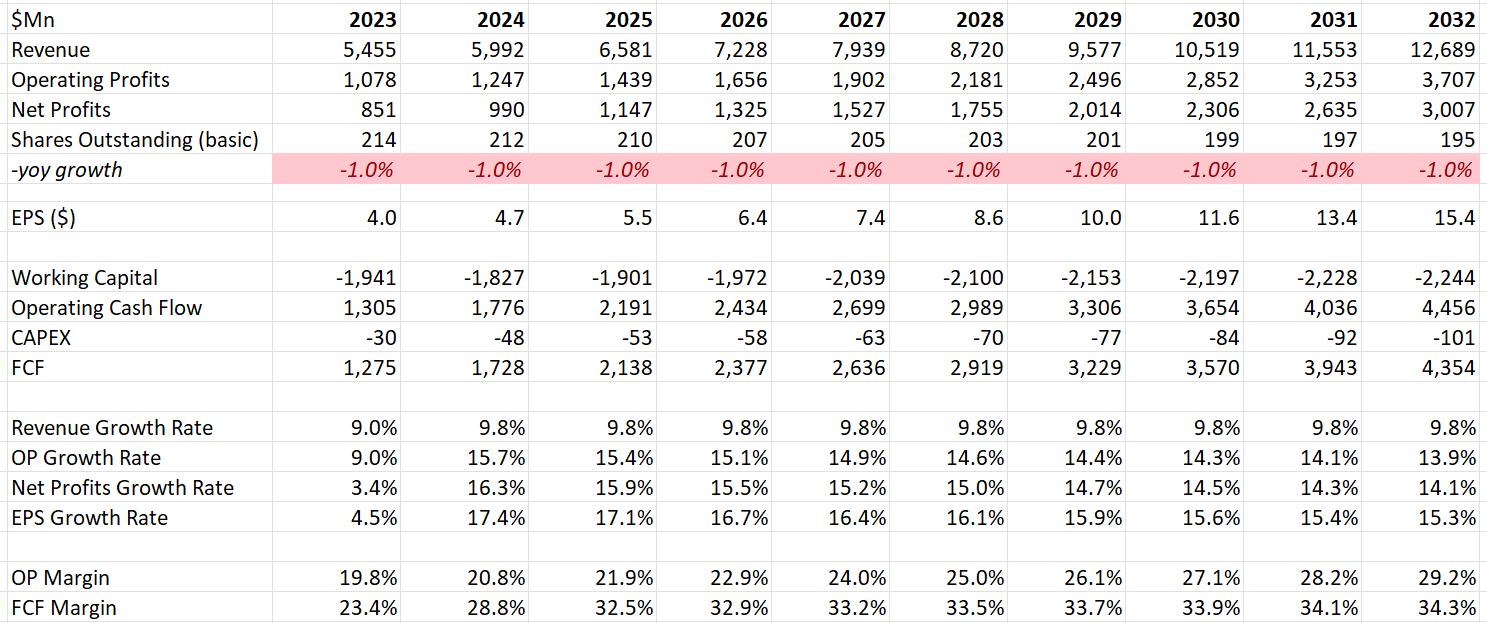

I anticipate a 9% organic revenue growth for both FY23 and FY24, in line with the company's guidance. For normalized revenue growth, my assumptions include 9% organic growth and an additional 0.8% from tuck-in type acquisitions. These projections are intentionally conservative when compared to their historical track records. Regarding margins, my forecast predicts continued expansion of the operating margin over time, driven by operating leverage and the maturation of their business transition from license to subscription. I find it reasonable to project a 30% operating margin by FY32 for a pure software company.

{kind=link}

The model utilizes a 10% discount rate, 4% terminal growth rate, and assumes an 18% tax rate. Based on these parameters, the fair value is calculated to be $250 per share.

Key Risk

High Stock Based Compensation : SBC represented 13.1% of total revenue in FY22, a relatively high level compared to other software companies. Autodesk's future margin expansion hinges on their effective management of SBC expenses. Should they maintain such a high percentage of SBC, achieving a 30% operating margin over time could prove challenging.

Empty Promises : Autodesk’s current management hasn't had a good track record of keeping promises. An illustrative example is their guidance of $2.4 billion in free cash flow for FY22 during the investor day in September 2021, yet they only delivered $2 billion. Personally, I favor companies that tend to under-promise and overdeliver.

Conclusion

I believe Autodesk's free cash flow hit its lowest point in FY23 and is poised to begin recovery in FY24. As a result, I am initiating coverage with a 'Buy' recommendation and a fair value of $250 per share.

For further details see:

Autodesk: Billing Changes Affect Free Cash Flow, But It's Likely Temporary