ADSK - Autodesk: Double Earnings Beat And A SaaS Moat

Summary

- Autodesk is a leading software company in the engineering design, product manufacturing and animation industry.

- The company reported strong financial results for the fourth quarter of 2022, as it beat both revenue and earnings expectations.

- I believe Autodesk has a "moat" which includes gold standard technology and its products being the "industry standard" which is backed by the high retention numbers.

Autodesk ( ADSK ) is a legacy software company that creates "best in class" or industry-standard software for designers, engineers, and even animators. The business offers high margins, steady growth, and a sustainable competitive advantage or moat. In the fourth quarter of FY23, the company continued to execute well by beating both top and bottom-line growth estimates. The company also bought back a substantial 1.1 million shares for $210 million, at an average price of $193 per share, which was a positive sign. In this post, I'm going to break down its fourth quarter financial results, before outlining its "moat" (from my experience as a user in the engineering industry) and then reveal my valuation model and forecasts for the stock. Let's dive in.

Fiery Fourth Quarter

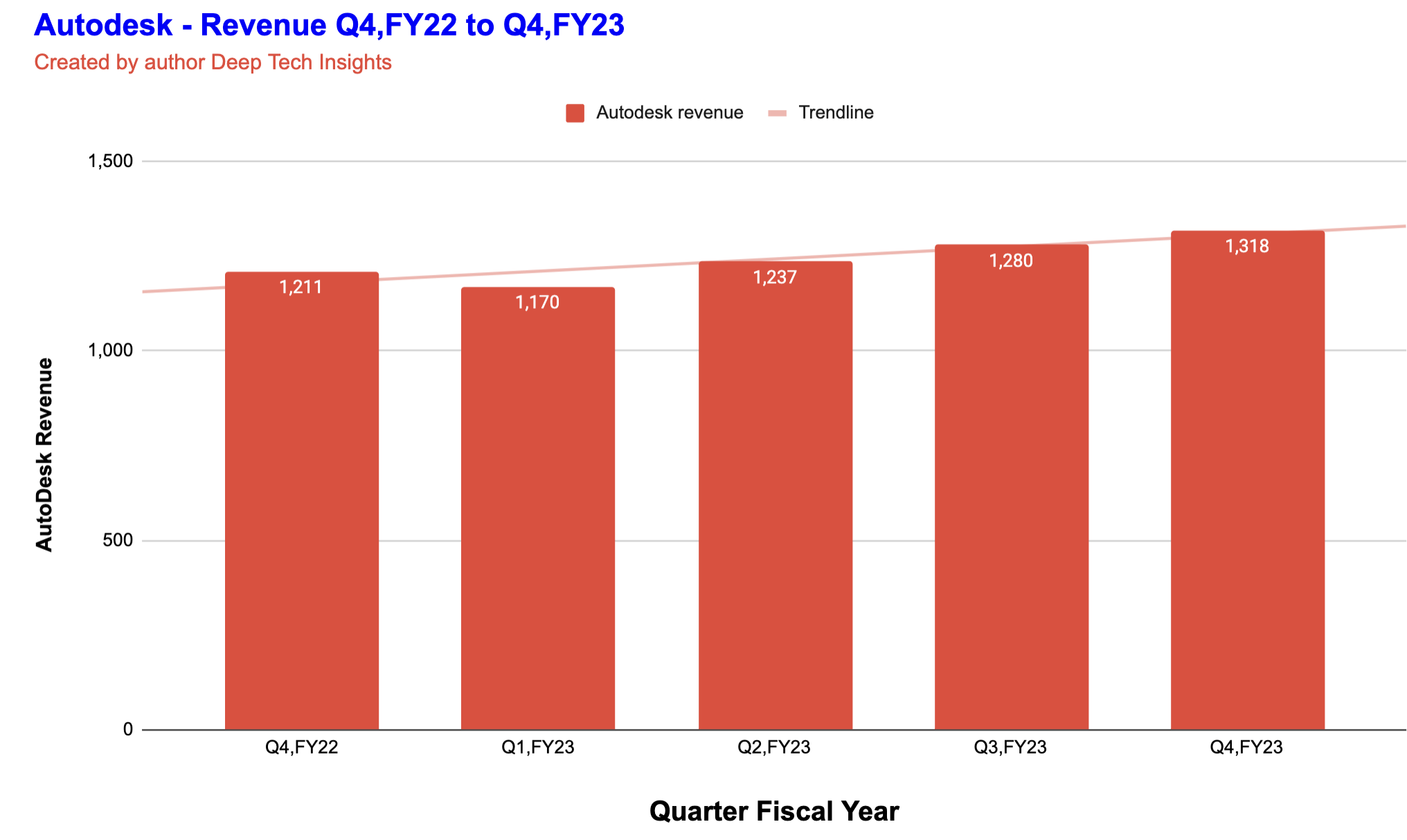

Autodesk reported strong financial results for the fourth quarter of the fiscal year 2023. Revenue was $1.32 billion, which increased by 9% year over year or 12% on a constant currency basis. I have plotted the revenue for the past few quarters on the chart below. You can see the trendline is mostly upward despite a dip in Q1 FY23. When I analyzed the prior growth rate metrics for the company, I discovered the trend is slowing currently. For example, in Q3 FY23, the year-over-year growth rate was 13.68%. In Q2 FY23, the YoY growth rate was 16.7% and in Q1 FY23 the YoY growth rate was 18.3%. Initially, this slowing growth rate would worry many investors. However, this is a common trend I have seen across multiple companies I have analyzed over the past few months (see my other posts). Therefore, I believe this is more of a macroeconomic issue than company specific. The U.S. dollar also started to rise substantially versus other currencies, such as the euro, from early 2022; thus, this will likely impact growth rates.

{kind=link}

Autodesk is also in a much stronger position than most other companies to survive and even thrive during a tough economic environment. This is because ~98% of its revenue is recurring which has been consistent over the past few quarters, with only a 1% dip since Q4 21 (calendar year) which suggests high customer retention and a high-quality business. In fact, the company reported a retention rate of between 100% and 110%, which indicates customers are staying with the company's products and even spending more through upsells.

{kind=link}

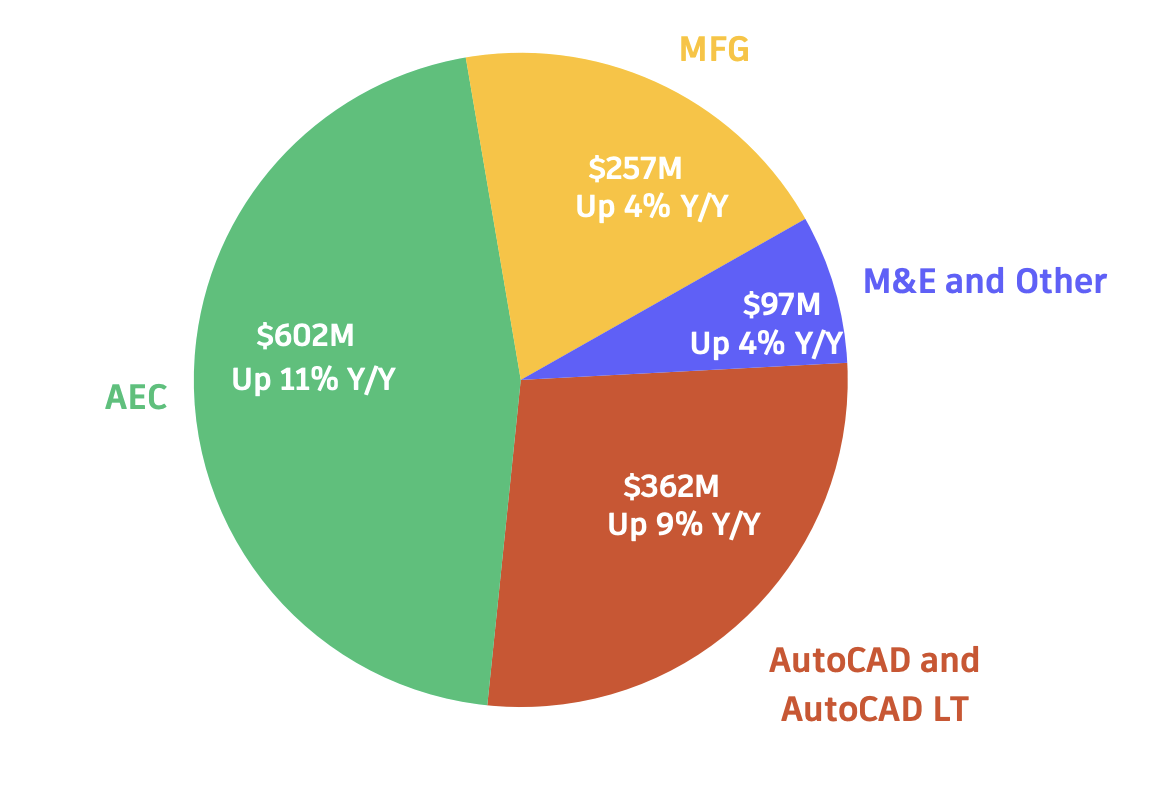

Breaking down revenue by product type, its AutoCAD and AutoCAD LT revenue increased by 9% year over year to $362 million, while its AEC (Architecture Engineering & Construction) revenue increased by 11% year over year to $602 million. It is positive to see growth in these segments especially given the macroeconomic climate (I will dive into the reasons for this in the "Moat" section next). Rounding off product revenue, the business manufacturing revenue increased by a steady 4% year over year to $257 million. This is of course excluding foreign exchange rate changes and adjusted for upfront revenue. Its M&E (Media & Entertainment) revenue was technically down 10% year over year. However, a positive is this was mainly driven by upfront revenue achieved after the segment recorded its largest-ever enterprise business agreement in Q4 FY22. Thus, if we adjust for this, M&E revenue actually increased by a steady 4% year over year. This segment is particularly interesting as it includes the software used by animators and visual effects artists such as 3ds Max and Maya. The metaverse industry is forecast to grow at a rapid 42.7% compounded annual growth rate [CAGR], and reach a value of ~$427 billion by 2029. Therefore, I believe Autodesk will benefit massively from this trend as visual effects and animation is effectively a key part of the metaverse. In fact, large technology companies such as Nvidia (NVDA) have announced deep integrations with Autodesk Maya for its "Omniverse" platform.

{kind=link}

The Moat

The aforementioned diverse number of revenue drivers brings me neatly onto the "moat" of Autodesk. As a former design engineer at a large consultancy, I have first-hand experience of using Autodesk products which were abundant across the industry and the "standard". Now you may say can't a company just switch to a "better, faster, cheaper" product? Well, it's not that simple.

Firstly, to develop a "better" product, a competitor would require intense R&D efforts and huge investment in order to even have a chance of competing. This is because Autodesk has a first-mover advantage in terms of decades (founded in 1982). the physics and principles of construction haven't changed much (apart from more regulation, data, and environmental concerns). Therefore, Autodesk has many years of identifying and solving issues at a granular level for its customers. Its major competitors I can find online include TurboCAD (which is really a simplified version), SketchUp (which is also simple in terms of features) and Siemens, which does offer a good product manufacturing suite but not so much on the AutoCAD collaboration side.

For example, Autodesk has recently improved its BIM (Building Information Modeling) software for civil engineering to include a variety of collaboration features. I believe this is especially important given the rise of remote working and team coordination, as it has always been a big issue to solve for engineering products. For instance, when I was a design engineer, we used Autodesk Electrical to design cable routes for buildings. Now a software copy of this could be made easily (on a static building model). However, this software enables coordination and collaboration with other engineers and teams such as the plumbing or HVAC (Heating, Ventilation, and Air Conditioning) engineers. Thus, this would prevent the issue of a ventilation duct being designed in the middle of a cable run and vice versa. This is vital for accurate building services design and requires immensely valuable software. These days "collaboration" tools such as Monday.com or Google Sheets have become the norm, as many team members can make changes in the cloud. But these software tools are extremely lightweight and don't include billions of data points, files, and designs for an entire building. Therefore, it would be unlikely another company could compete and if they could, switching would go against the industry standard.

Third, when new engineers are onboarded at many large design consultancies (including where I used to work), they usually need to undergo an Autodesk training course, as mastering the software can take many years. Therefore as more professionals invest time, money and energy into learning how to use the complex product, "stickiness" is effectively guaranteed. Thus, the fact it can be challenging to use and master is actually a positive long-term.

My fourth and final point is Autodesk's software is fairly cost-effective (in the world of construction) and many packages lock users into 3-year deals.

{kind=link}

Given most construction projects are long-term endeavors, even during tough economic times, design and building work continues. In Autodesk's numbers, we can already see signs of this with billings of $2.1 billion, up 28% year over year, and total deferred revenue of $4.6 billion, up 21% YoY.

Economic uncertainty will only likely impact the number of "new builds" and upsells/cross-sells for Autodesk. However, if we look at regulatory tailwinds such as the bipartisan Infrastructure spending bills, this aims to spur the investment of ~$2 billion into bridges and over $1 billion into other infrastructure projects. Speaking of Government, Autodesk is getting closer to FedRAMP Authorization soon which will enable the business to sell directly to government agencies more easily, as its security standards will be met.

Margins and Balance sheet

Moving onto the company's profitability, Autodesk reported operating income of $277 million in Q4 FY22 which increased by a staggering 93% year over year. In addition, its operating margin rose by 9% year over year to 21%. Now before you get too excited, it's worth remembering the company was hit with a large $100 million charge related to leases in Q4 FY22; therefore, we are now seeing a favorable comparison for Q4 FY23. The positive is on a non-GAAP basis, its operating margin was up 1% YoY and came in at a super high 36%.

In terms of the company's balance sheet, the business reported ~$2 billion in cash and short-term investments. The company does have fairly high debt of $2.66 billion, but only $2.28 billion of this is long-term debt and thus manageable.

Valuation and Forecasts

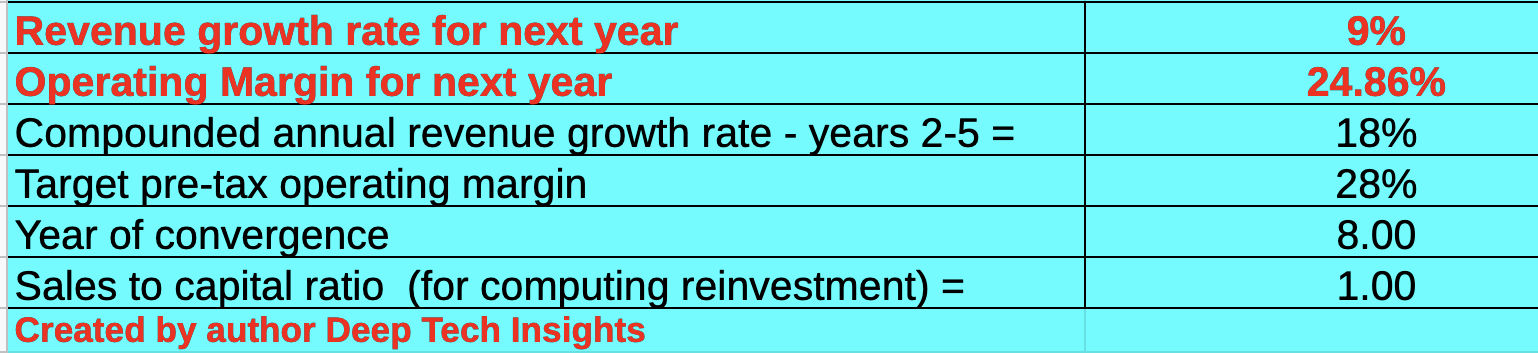

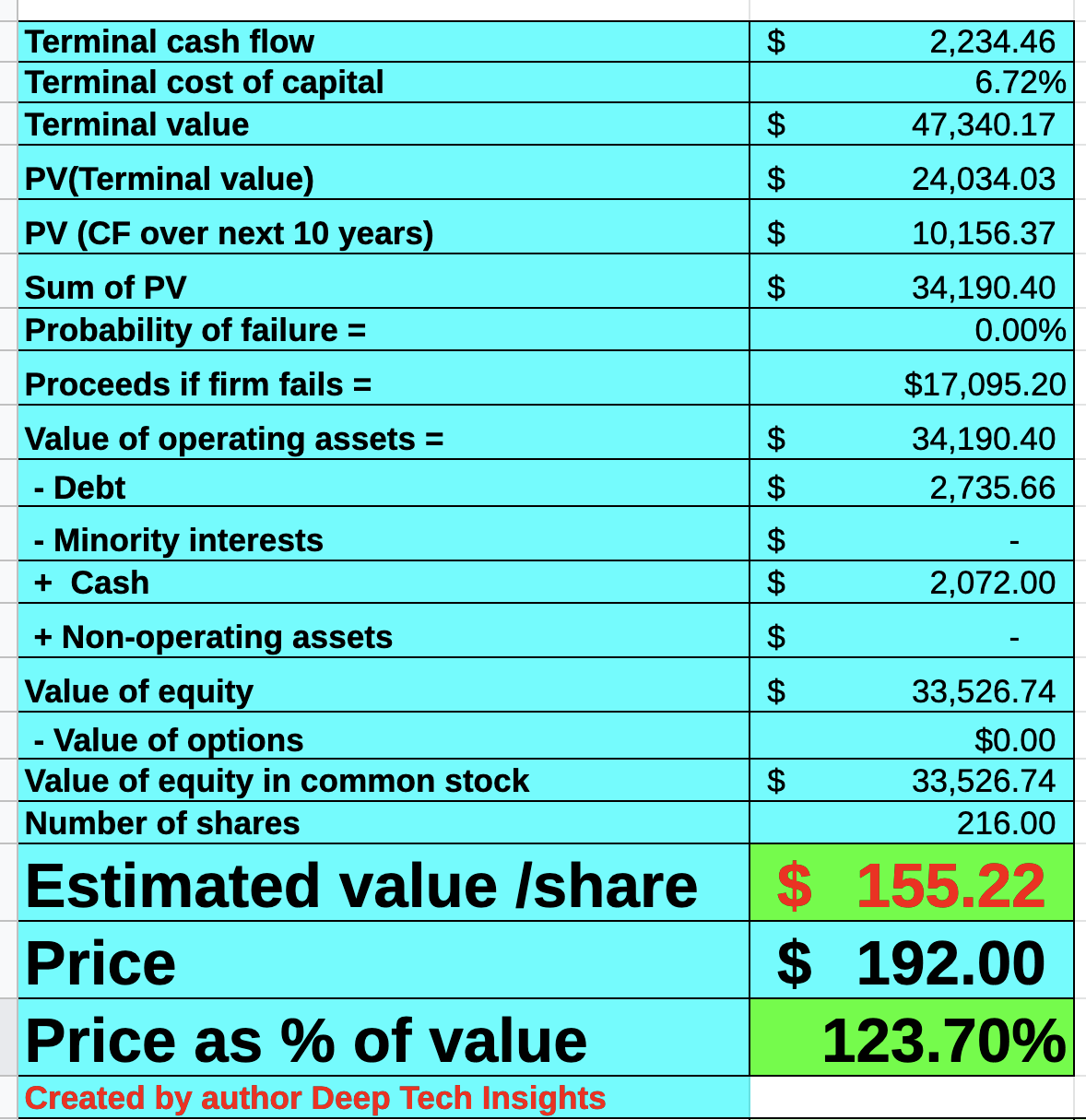

In order to value Autodesk, I have plugged its latest financial data into my discounted cash flow valuation model. I have forecast 8% revenue growth for "next year" or the fiscal year of 2024 in my model. This is based upon the midpoint of management guidance of between $5.36 billion and $5.46 billion.

This follows the prior trend of "slowing" revenue growth but this level is only 1% less than the Q4 FY23 YoY growth rate, which reflects a tepid macroeconomic environment. In years 2 to 5, I have forecast a faster 18% revenue growth rate which reflects a return to the prior YoY growth rate generated in Q1 22 (calendar year). I forecast this to be driven by improving economic conditions which will likely bolster product upsells and multi-product purchases.

Autodesk stock valuation 2 (Created by author Deep Tech Insights)

{kind=link}

To increase the accuracy of my valuation, I have capitalized R&D expenses which has lifted net income. I have forecast a target pre-tax operating margin of 28% over the next 8 years. I expect this to be driven by increased operating leverage improvements as its software business scales, in addition to a greater number of feature upsells and more government contracts (thanks to FedRAMP authorization).

Autodesk stock valuation 2 (Created by author Deep Tech Insights)

{kind=link}

Given these factors, I get a fair value of $155 per share. ADSK stock is trading at ~$192 per share at the time of writing, and thus it is ~24% overvalued.

This doesn't surprise me with Autodesk given the high quality of the company, high margins, and strong leadership position. A positive is the company trades at a price-to-sales ratio = 7.66, which is ~36% cheaper than its 5-year average.

Risks

Recession/Lower Cross-sells

As mentioned prior, Autodesk is one of the companies which is best protected against a recession , due to its highly "sticky" subscription business. However, it is not completely immune, as a prolonged recession could cause an immense slowdown in the construction industry and thus impact Autodesk's revenue growth rate even more so, as it is already slowing down.

Final Thoughts

Autodesk has continued to execute tremendously in the fourth quarter, despite a tough economic backdrop. The company has maintained (and even grown) its high margins, while still generating revenue growth and maintaining high customer recession. I believe this business has a sustainable competitive advantage and moat, which is a major positive. The real issue with Autodesk is its valuation is currently "overvalued", according to my intrinsic valuation model and forecasts. This has been a common occurrence for such a high quality company and thus this makes it an ideal candidate for an investor's "watch list" as I will label the stock a "hold" for now.

For further details see:

Autodesk: Double Earnings Beat And A SaaS Moat