ADSK - Autodesk: Niche SaaS With A Solid Moat

Summary

- Autodesk has evolved with the times to develop itself a nice moat, and the SaaS transition has been a good one for the company.

- The basics of the company are a pretty easy parallel to Photoshop and Adobe, which is another company I like a lot.

- Autodesk was part of the tech rout, but looks to continue compounding away as an industry leader with strong capital allocation and a fair valuation.

I've sat down to write this article several times over the past couple of years. Autodesk (ADSK) is a company I've been impressed with from a distance, and it is about time I actually dug into it. The company trading ~40% off of its highs was an added incentive to take a closer look.

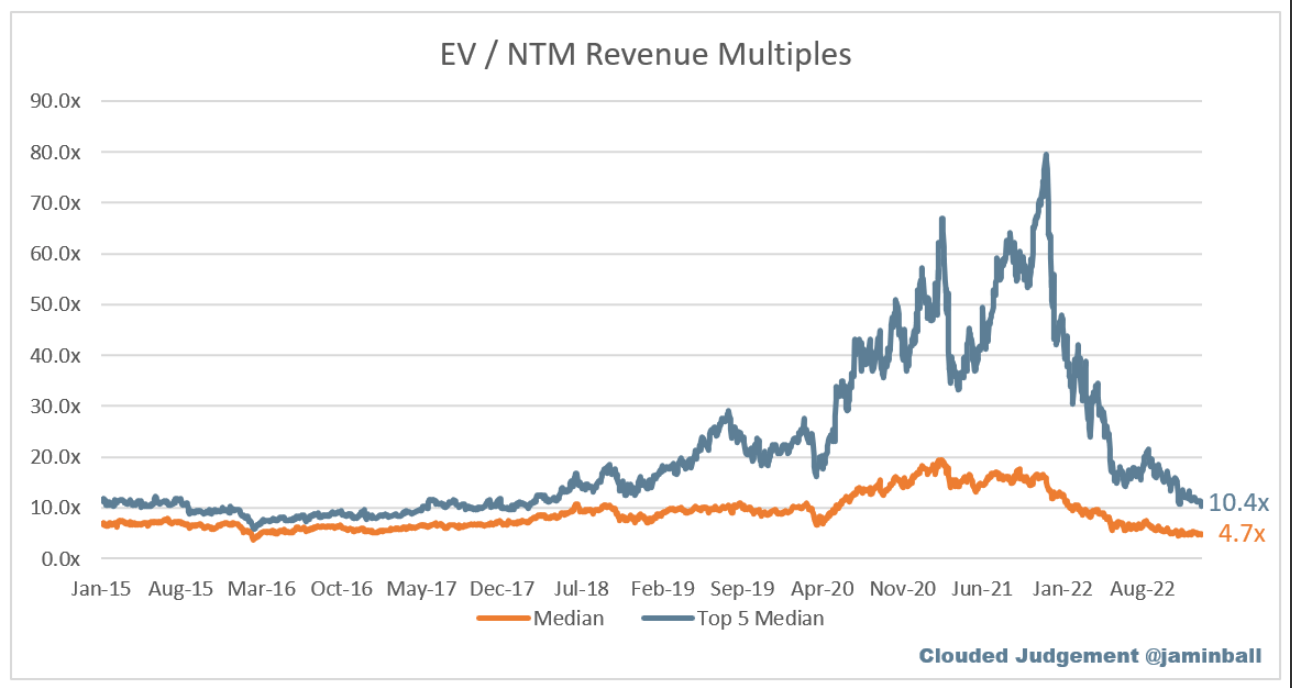

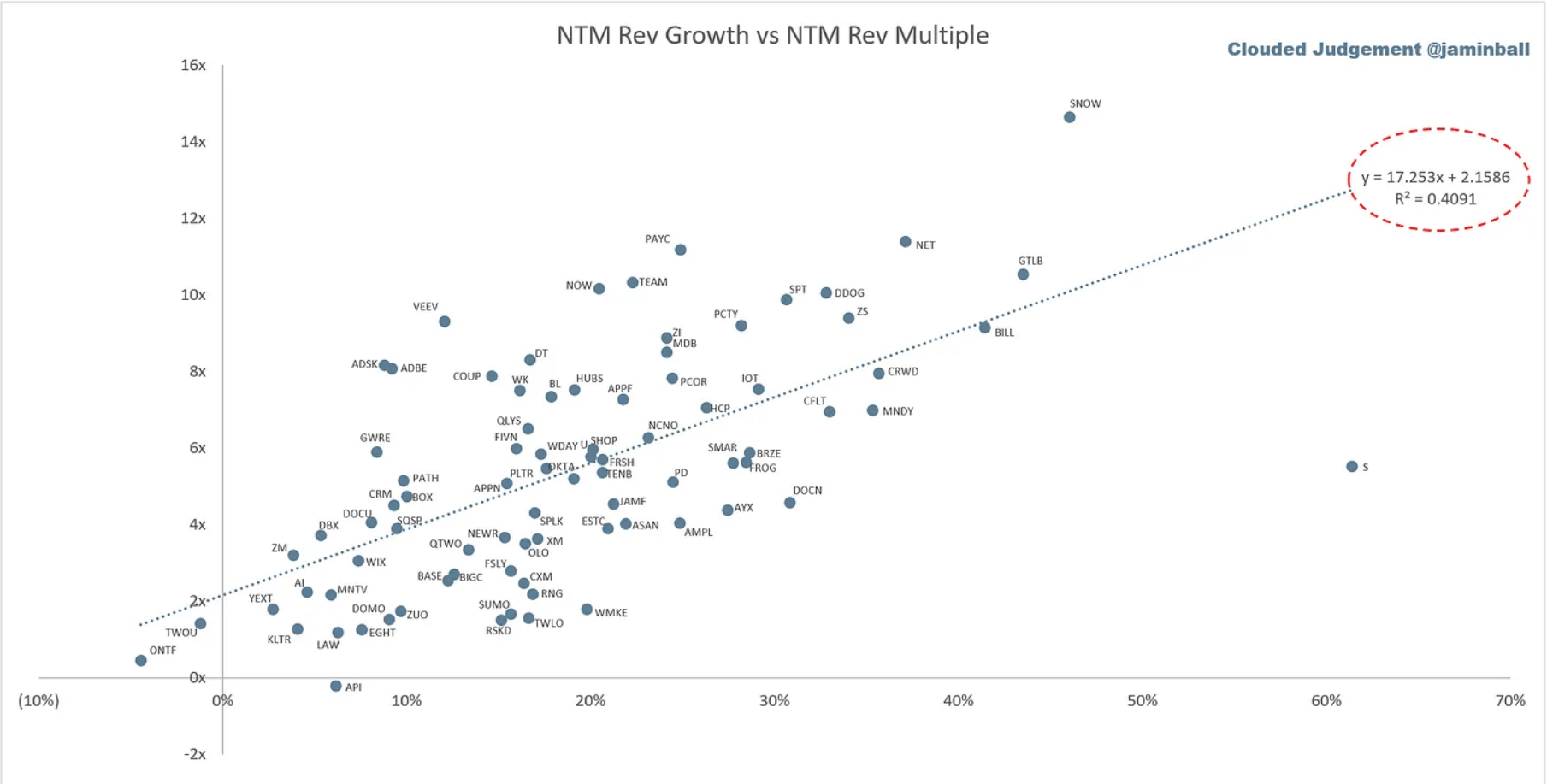

If you've been reading my recent articles, or really paying attention to tech at all, it will be no surprise that cloud stocks went crazy post-COVID and have subsequently collapsed. Looking below, the average cloud multiple took a pretty fun ride starting in March 2020 only to end up at the same place it sat at the end of 2017. It's typical that these sector-wide rotations will throw the baby out with the bathwater, and savvy investors should look for companies that will weather the storm.

{kind=link}

In my opinion, one of these is Autodesk. The company checks almost all of the boxes, with an industry-leading product, a flywheel effect for maintaining and growing subscription revenue, smart capital allocation, and sustained profitability. At current prices, ADSK is a solid addition to a growth portfolio with sustainable company metrics in mind.

{kind=link}

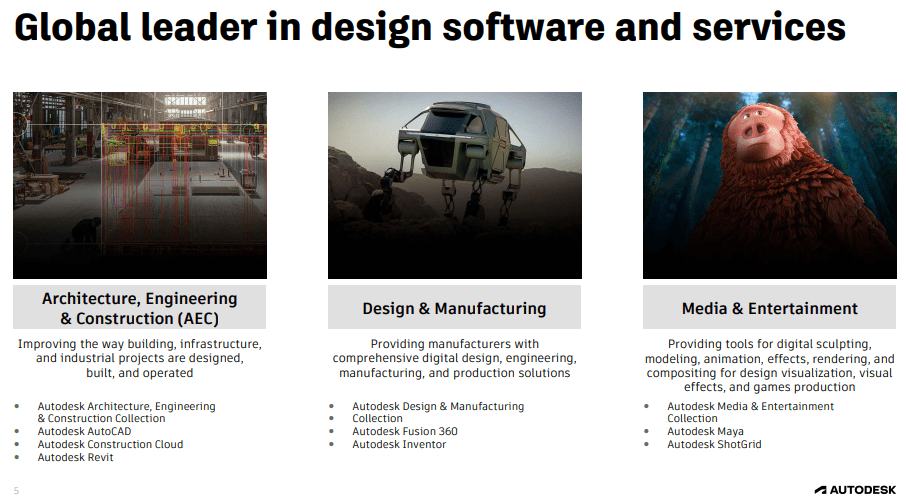

ADSK's flagship product is AutoCAD, and what they are best known for. The software is the industry standard for use in architecture, engineering, and construction, and the company continues to make strides to keep it that way. ADSK is a member of a global organization called Building SMART, which advocates for setting industry standard file types, such that any designs can be transferred seamlessly, reducing rework. This allows customers to come to their products more easily, while also allowing them to fold in portions of previous designs or better work with other firms when starting a project. The segment accounts for 73% of revenue in FY21 overall, so it is a good overall proxy for the company.

However, that shouldn't minimize the success the company has achieved across its other business lines. Fusion 360 is a leading provider for the growing additive manufacturing space, and I see it as a nice way to add some exposure to 3D printing without the risk inherent in many of those companies. Additionally, Media and Entertainment doesn't account for a huge slice of revenue, but the product (Maya and 3DS Max) has been used in the last 20 Academy Award winning movies.

I mentioned the company's flywheel above. That word is thrown around a lot now, but I think it's a good way of looking at a business like this. Much like Adobe's Photoshop, the popularity of the software feeds itself. Education systems train on it, because it is what industry uses, and industry uses it because it is what people are most comfortable with. Once that is set in motion, it is difficult to disrupt. Switching costs would be significant for many firms due to the time required to train its people on another software, especially in design.

Company 1990 Annual Report

One thing you get with ADSK is an extensive operating history. I attached the revenue breakdown from the 1990 annual report. I've often found these older AR's interesting for companies I follow, and there aren't many continually successful tech firms from 30+ years ago still plugging along. Through that time, ADSK has continually reinvented itself, and smartly acquired additional technology to stay relevant.

{kind=link}

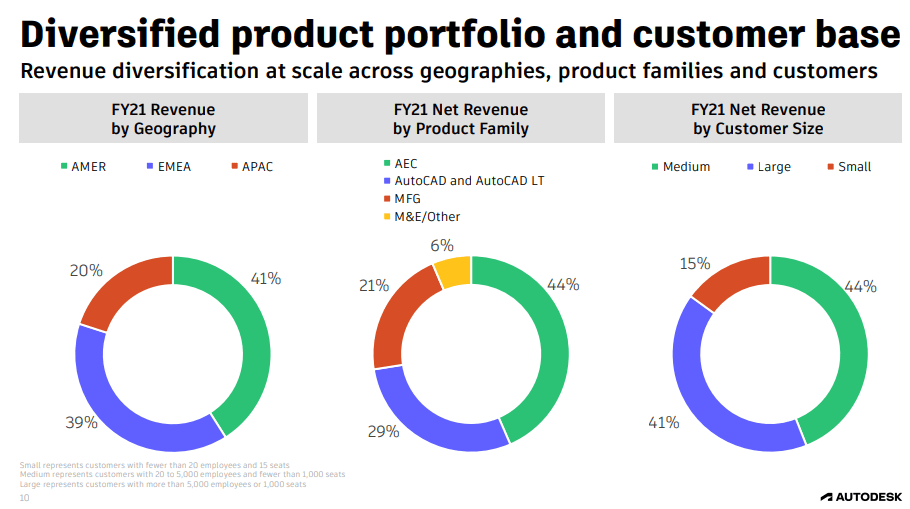

Looking above, ADSK is global, across all firm sizes, and in that regard is well diversified. Of note, due to the high exposure to new construction, the company is likely more sensitive to economic pressures than other technology companies. A good way of thinking about technology companies, in general, is though they may trade with other tech companies, they get their revenues from widely disparate areas of the economy.

As the global leader, ADSK has expanded use cases for its software, and works with many of the largest companies in the world. I've included an interesting anecdote from the most recent quarterly earnings call below:

Heineken is on a mission to become the best connected brewer as part of its evergreen strategy and is undergoing a digital transformation to ensure is prepared for the unforeseen challenges in an ever-changing world. To help, Autodesk has been supporting Heineken's 3D printing initiative with an expanded adoption of Fusion 360 across a number of breweries. By designing and manufacturing their own equipment parts in-house, Heineken has been able to see a reduction in the replacement times of a number of parts from over 6 weeks to just 4 hours, significantly reducing downtime and lessening the carbon impact of shipping new parts when necessary.

YCharts

Ever since ADSK shifted its model to subscription-based, all of the metrics have pointed in the right direction. Revenue obviously became more consistent, and has been growing strongly. Go back and look at any chart of Adobe when it shifted, it was a huge opportunity.

YCharts

Free cash flow is positive, and also pointed in the right direction. Management anticipates $1.9-1.98B this year.

YCharts

The long-term debt is almost entirely serviceable by a year of free cash flow, no concerns here.

Here's where I blow your minds. Share count has actually fallen. This is a mature business, transitioning into SaaS, that actually repurchases shares with profits. The company is a net acquirer of shares, repurchasing 4.4M at an average price of $200 last year, and has a new $5B authorization coming next year. This is normally my #1 complaint of cloud companies, and ADSK bucks the trend.

{kind=link}

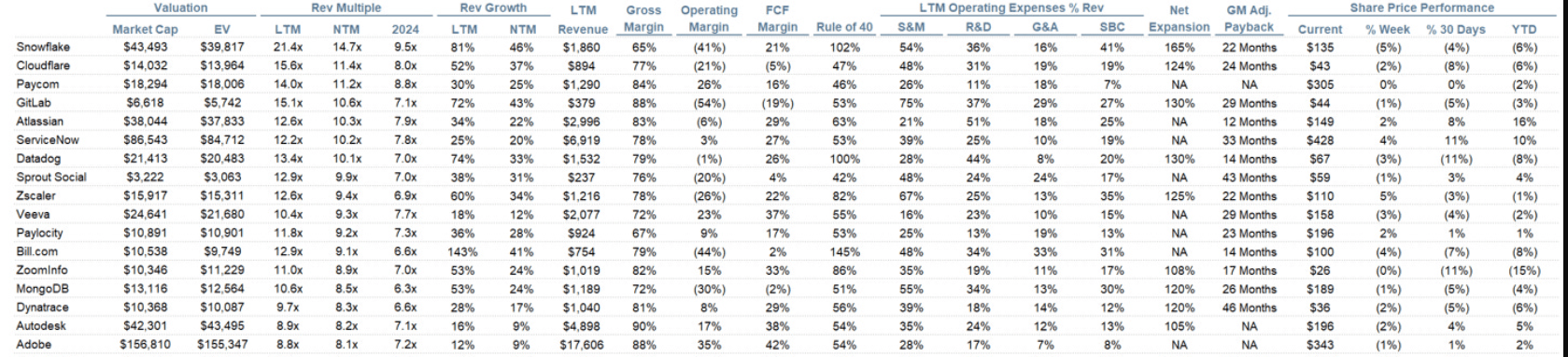

Some key metrics from the table above to keep in mind. ADSK is trading around 7X revenues on low double digit sales growth rates. Net revenue retention is relatively low between 100-110%. This isn't a feather in the cap for the company, it just shows either higher churn or a slower land-and-expand than some other companies. ADSK derives business across the landscape, from individual designers to major corporations, so I'd anticipate some churn from its smaller businesses. Gross margins are rock solid at 90%, operating margins are pointed upwards and non-GAAP is in the 36% range, which is great and shows good expense management. Lastly, the company ticks the Rule of 40 box at 54%. Can't find anything not to like here, outside of this company not breaking the meter on growth rates.

Looking across the cloud landscape, ADSK trades almost exactly with ADBE in terms of valuation. It's high compared to the company's growth, but you are paying for consistency, profits, and intelligent capital allocation (can't say enough about that in this space). If you buy it today, the odds you are negative on your investment in a decade are significantly lower than for some of the companies on the graph below.

{kind=link}

{kind=link}

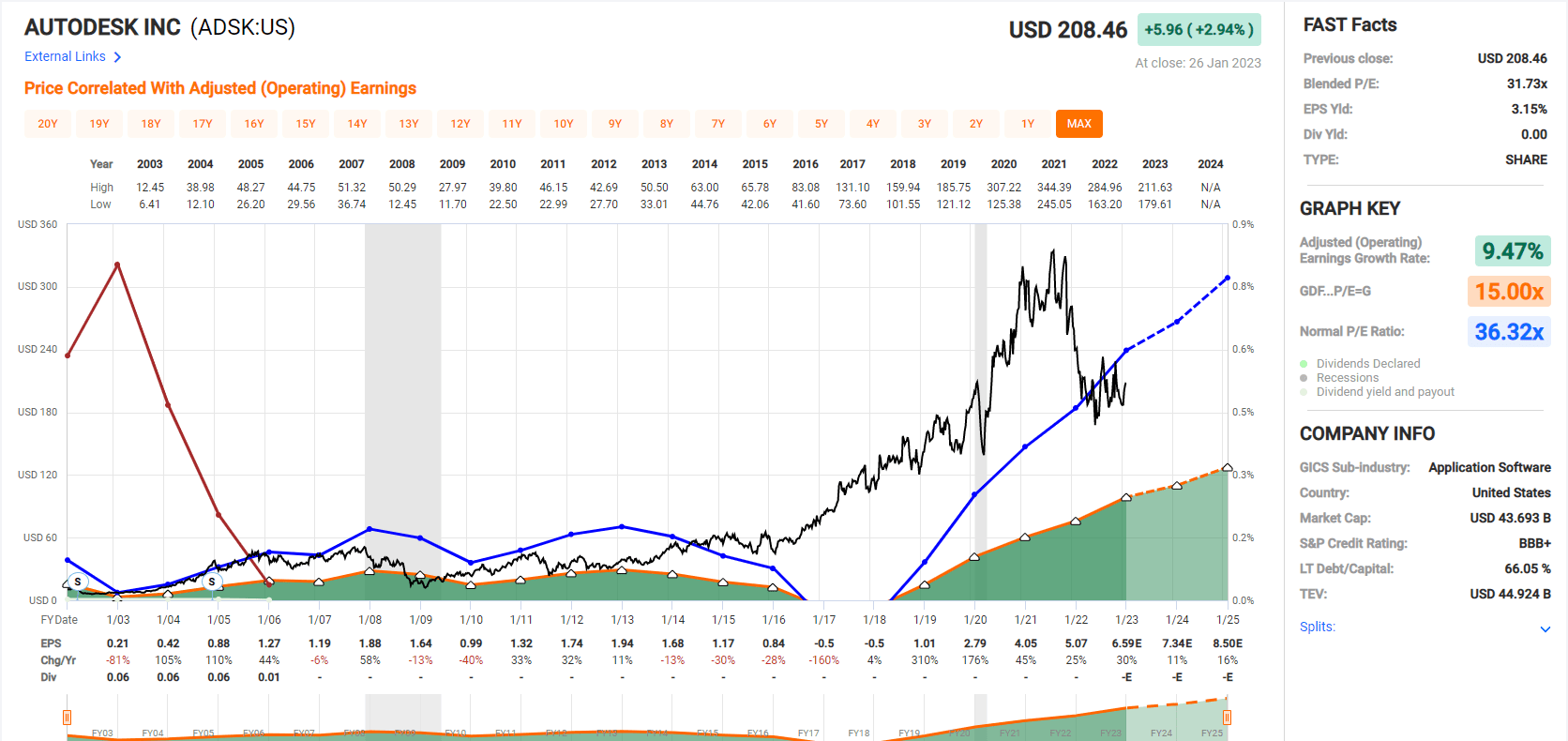

Looking at the long-term, notice an inflection point? The company sacrificed short term earnings for a subscription model, and the company has benefited incredibly. 2016-2018 were rough, but earnings have bounced back in a big way and are pointed in the right direction.

{kind=link}

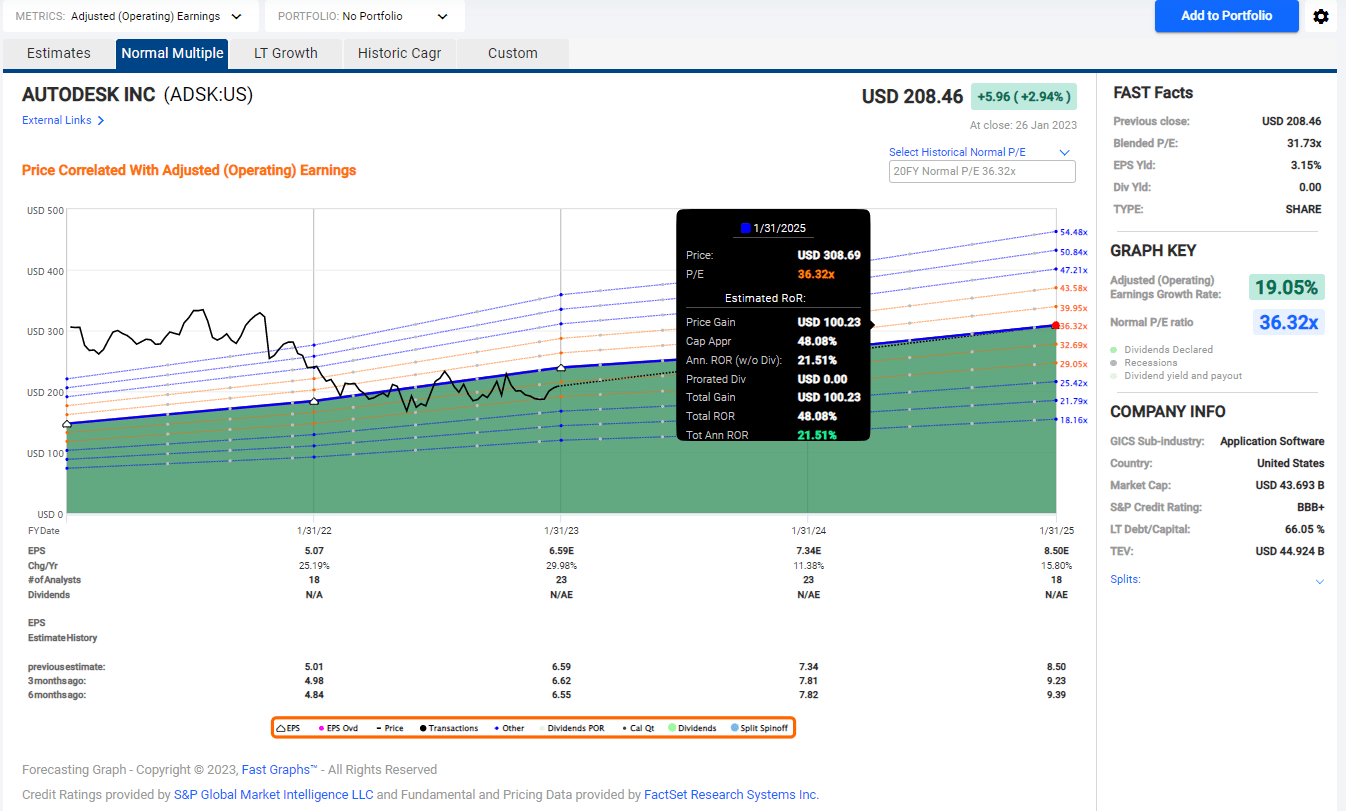

Looking at some analyst estimates and a return to the company's long term average valuation, an investment today could net somewhere in the ballpark of 20% annual returns. Obviously, that is a back-of-the-napkin type conjecture, but the company leads its space, has solid fundamentals, strong capital allocation, and has multiple growth vectors. I'm looking at ADSK as a strong buy from here.

For further details see:

Autodesk: Niche SaaS With A Solid Moat