ADSK - Autodesk: Rapid Growth High Margins And A Strong Moat

Summary

- Autodesk creates industry-leading computer software used for engineering, construction and design.

- The business is high quality with many competitive advantages, from technology to network effects from industry courses.

- The company has generated strong earnings for the second quarter which beat both top and bottom line estimates.

Autodesk ( ADSK ) is a pioneer in CAD or Computer Aided Design. Basically, this company creates software that helps architects and engineers design buildings for real-world construction. The company is a dominant market leader with a series of competitive advantages. More recently Autodesk has beat revenue and earnings estimates for growth, while the stock price has pulled back by 39% from its all-time highs. In this post, I'm going to break down the company's unique business model, financials, and valuation. Let's dive in.

Business Model

Autodesk is the world's leading CAD software package which is used by architects, engineers, and designers across the world. As a former design engineer who has worked for a large consultancy, I have insight into the vast usage of the software package. The company benefits from a series of competitive advantages which include; technology, market-leading position, and network effects. its network effects are particularly interesting, as engineering students, consultants, and designers all have to learn the package in order to collaborate with each other on professional projects. This has led to a large community of resources, courses, and training programs that the majority (in my opinion) of design engineers have taken if they haven't learned on the job over many years. The package isn't easy to learn but again I believe that adds to its "Stickiness" as engineers will be reluctant to learn a new software package even if cheaper for the company, this gives Autodesk pricing power.

Autodesk Products (created by author Ben at Motivation 2 Invest)

{kind=link}

A look on the Gartner review website at alternatives to Autodesk shows, "SketchUp" which is great for creative CAD drawings and designs but does not touch Autodesk on advanced functionality. Then we have "TurboCAD" which is really just a low-cost training package for students. Next we have Siemens Solid edge, which according to reviews is easy to use but more for small assemblies.

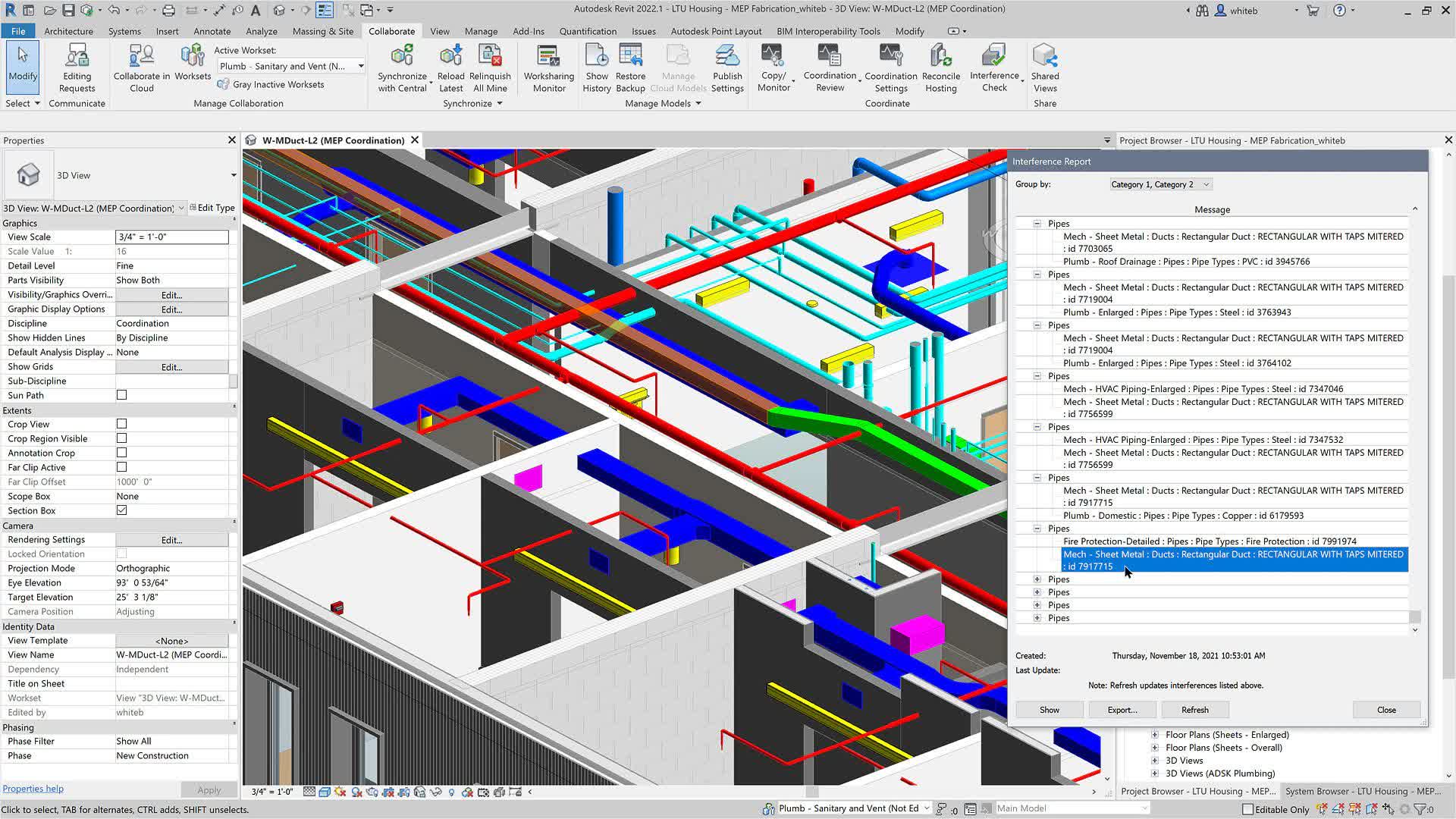

To give you an idea of the scale of Autodesk and its advanced functionality, an entire new building model can be rendered inside Autodesk, with accurate dimensions and measurements throughout. The beauty of the platform is it allows cross-collaboration between teams. So let's say you have the Electrical design team (which I was on), we would be designing cable tray runs across a Hotel ceiling as an example. But we also want to make sure we are not bumping into any plumbing pipework or mechanical air conditioning equipment. With Autodesk, both teams can work on a common model, so when a change gets made by one team, it shows up for the other team. This is something only advanced technology can do.

{kind=link}

It's no surprise that Autodesk has a high Net Revenue Retention rate in the 100 to 110% range which means customers are finding the product "sticky" and spending more. This makes complete sense due to the aforementioned reasons, a large architecture firm or construction company is unlikely to end its subscription just because business is slow for one month. The platform is the tool of the trade.

Growing Financials

Autodesk generated strong financial results for the second quarter of 2022. Revenue was $1.24 billion, up a rapid 17% year over year and beating analyst estimates by $12.23 million. The beauty of Autodesk is the majority (98% of its revenue) is recurring and thus offers more predictability than many companies.

its top-line revenue growth was driven by $1.064 billion in Design Revenue, which was up 15% year over year and 6% Q/Q. In addition to $113 million in Make Revenue, which was up 26% YoY and 27% on a constant currency basis.

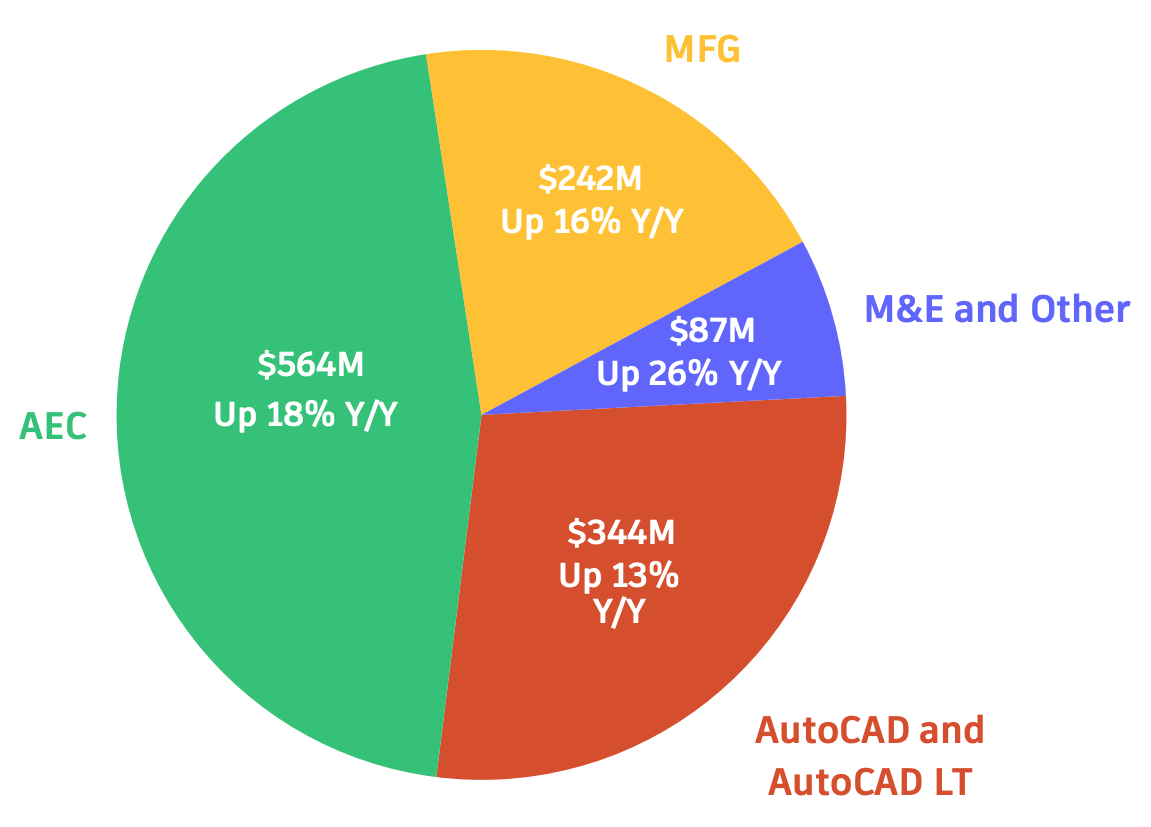

By product, [AEC] Architecture, Engineering & Construction software makes up ~45% of Autodesk's revenue ($564 million) and was up a rapid 18% year over year. This is followed by the second largest segment AutoCAD and AutoCAD LT which makes up $344 million or 28% of revenue and was up 13% year over year. its other product segments such as MFG and M&E are also growing strong by 16% and 26% respectively. This product diversification is a positive sign and should lead to stable revenues moving forward.

{kind=link}

"Billings" is an interesting metric commonly used for subscription companies. This is the amount customers are invoiced and gives an accurate gauge of future revenues. For example, if a customer signed a $30,000 3-year contract with Autodesk, the company would invoice the customer $10,000 per year. Thus in this case its total billings increased 17% year over year to $1.191 million which shows solid demand overall.

Remaining Performance Obligations [RPO] is the sum of Deferred Revenue and Backlog. Where Deferred Revenue is the contractual obligation to deliver the product for the period invoiced. In addition, Backlog is the future contract obligation.

In this case, Total Remaining Performance Obligations [RPO] was $4.7 billion and the current RPO was $3.1 billion which grew by 13% and 10% respectively. This reflects strong growth in billings and the volume of multiyear contracts. In addition, it was great to see a slight increase in long-term deferred as a percentage of total deferred revenue which reflects the growth in multi-year contracts, which locks in predictable revenue.

its GAAP operating income was $242 million, up a blistering 63% year over year from the $148 million generated in the second quarter. This was driven by a 6% increase in GAAP operating margin, which reached a healthy 20%, which was higher than historic levels.

Management's ongoing cost discipline, combined with high operating leverage due to low fixed costs has caused this healthy boost in margins.

Earnings Per Share [EPS] [GAAP] was $0.85, which beat analyst estimates by $0.07.

Cash flow from operations was $257 million, up $55 million with Free Cash Flow of $246 million, up $60 million year over year.

Management showed confidence and repurchased $1.4 million shares for $257 million, this was at an average price of ~$182 per share. Autodesk has a solid balance sheet with $1.5 billion in cash, cash equivalents and short-term investments. However, the company does have a fairly high total debt of ~$3 billion the good news is only $350 million is due in the short term.

Stable Guidance

We have seen many companies slash guidance on a fearful outlook in the latter half of 2022 and into 2023. But in Autodesk's case management states the business conditions are "broadly unchanged" from their perspective. This is a testament to the company's product moat and high stickiness which I discussed in the business model section.

The company is expected to experience some slight FX headwinds from a strong US dollar. However, its guidance is "unchanged" at the midpoint "across all metrics". Autodesk's "underlying momentum" is expected to offset any FX headwinds, which is a positive sign.

Advanced Valuation of Autodesk

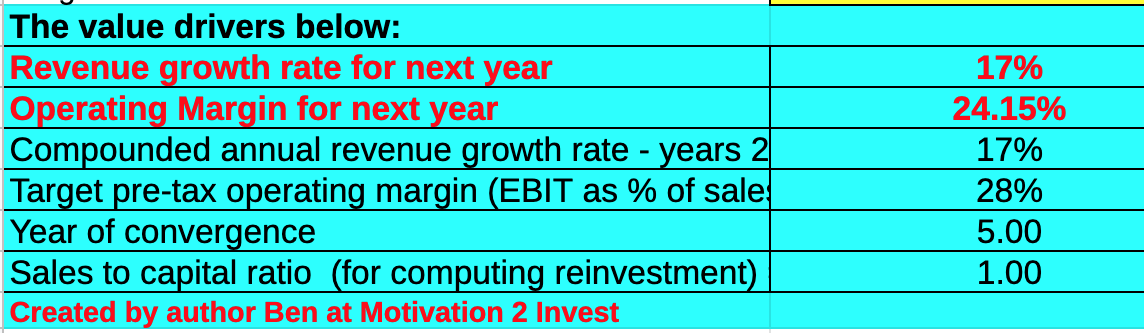

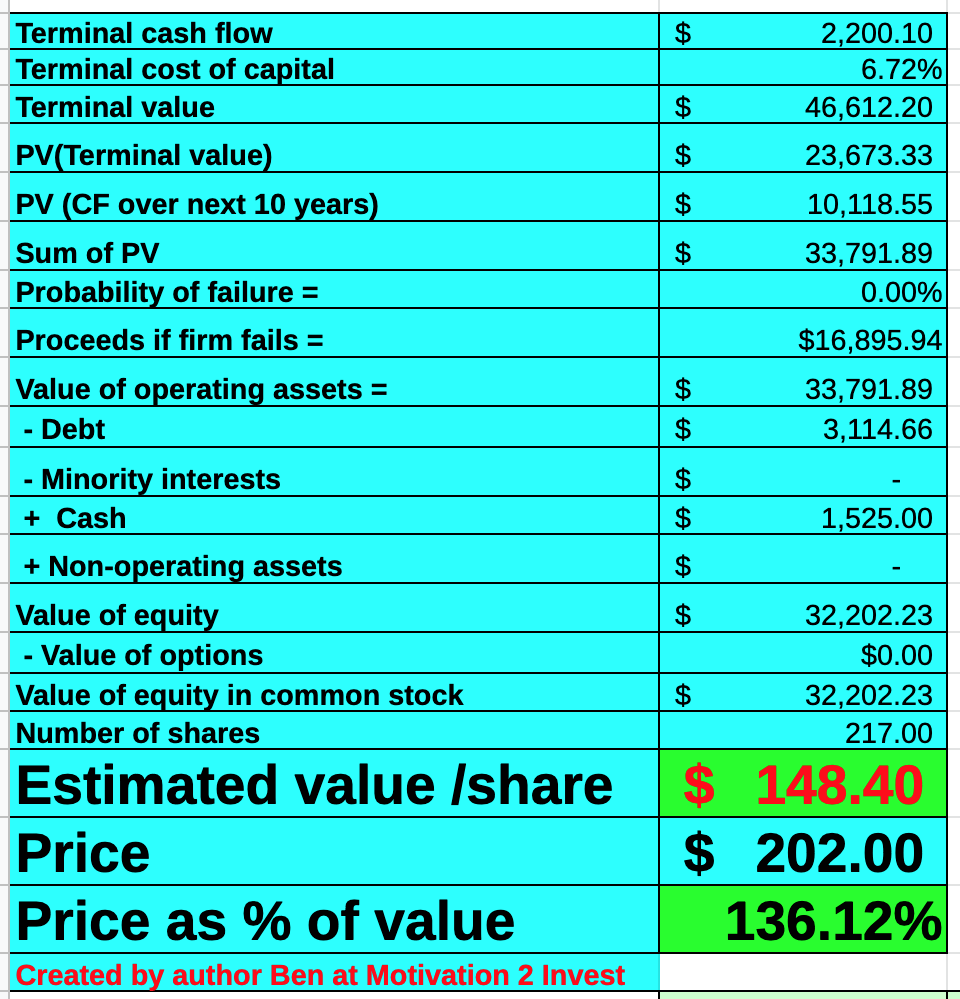

In order to value Autodesk, I have plugged the latest financials into my advanced valuation model which uses the discounted cash flow method of valuation. I have forecasted 17% revenue growth per year over the next 5 years with is in line with historic levels.

Autodesk stock valuation 1 (created by author Ben at Motivation 2 Invest)

{kind=link}

I have also forecasted the company's operating margins to continue to increase to 28% over the next 5 years, on cross-selling opportunities.

Autodesk Valuation 1 (created by author Ben at Motivation 2 Invest)

{kind=link}

Given these factors I get a fair value of $148 per share, the stock is trading at $202 per share and thus is 36% overvalued, at the time of writing. This overvaluation is not a surprise given the company's exceptional market positive, with high retention rates, predictable revenue, and many competitive advantages. To put things in perspective during the 2020 stock market crash, Autodesk dipped to a low of $140 per share and has a 52-week low of $164 per share. Therefore this is the type of stock I expect to always be "overvalued" to some extent unless under extreme circumstances.

The good news is Autodesk's valuation multiples have compressed substantially with a Price to Earnings Ratio [FWD] = 31 , on a Non GAAP basis which is 57% cheaper than its 5 year average of over 70. In addition, its Price to Sales [PS] Ratio = 8.9 which is 27% cheaper than its 5 year average.

Risks

High Valuation

Autodesk has been one of my favorite companies for a long time and I have bought and sold the stock multiple times. The company is "Overvalued" the majority of the time due to the business quality and strong market position. its valuation multiples have compressed but given the number of "cheap" stocks in the market, it is still a little spicy.

Recession/Construction Industry

As per my own industry knowledge and management's own outlook, I don't imagine Autodesk's existing revenue will be affected too much by a recession. However, it is good to keep in mind that this is still a software package used primarily for construction and thus a slowdown in that industry could lead to a temporary slowdown in new product purchases.

Final Thoughts

Autodesk is a wonderful company with a series of competitive advantages. It has generated steady growth and has been increasing its margins over the past few years. However, the high valuation means this stock price is still a little spicy and I expect that continue unless under extreme circumstances. The key would be to write down the buy points I mentioned prior and if the stock drops to these, then loading up the truck wouldn't be a bad idea.

For further details see:

Autodesk: Rapid Growth, High Margins And A Strong Moat