ADSK - Autodesk: Valuation Is At Attractive Levels Relative To Peers

2023-07-06 13:19:58 ET

Summary

- ADSK faces short-term headwinds due to macro cycles.

- The shift to an annual payment model may cause increased volatility and lower free cash flow in the short term, but offers potential future price-hike opportunities.

- Despite risks such as sustaining growth and capturing new users, ADSK's strong margin profile and discounted valuation relative to peers make it an interesting investment option.

Thesis update

I see Autodesk ( ADSK ) as a great business with a large TAM but faces short-term headwinds due to macro cycles – which has created an interesting investment opportunity as the market derates valuation to an attractive level vs peers. I give credit to the bear thesis that ADSK near-term outlook does not look extremely great due to ADSK exposure to cyclical -end markets, which are obviously hit by the economy cycle. As such, there is little reason or catalyst to drive the stock up in the near-term. However, I am recommending a buy rating as I am willing to support the other side of the equation by looking at the positives so far. Management is guided for 2H23 growth acceleration and ADSK is also seeing continued momentum with Fusion 360, traction with Flex consumption model, and improving renewal rates relative to 4Q22.

Near-term share price outlook

Shares of ADSK could experience increased volatility in the near future as the company shifts from a three-year upfront payment model to an annual payment model, which I expect free cash flow to drop this year. The long-term deferred revenue account will also decrease from its current level as a percentage of total deferred revenue. Financials would not be simple to dissect and analyze during this transitional period, which could confuse some investors and lead them to use more conservative assumptions in their models. Since the changeover began on March 28, its effects should start to become more apparent starting in the second quarter. A potential upside is that it provides ADSK with additional price-hike opportunities in the future.

Business outlook

Although management has noted a slight slowing in the growth of new ADSK subscribers, they have reported no signs of weakness in the growth of existing subscribers. Growth is also being seen in other qualitative metrics, such as Product usage and BuildingConnected. Although ADSK's business model is less cyclical than the commercial real estate market as a whole, I am aware that it is not completely protected from the industry's ups and downs. Given the current macroeconomic environment, it is clear from a close examination of the stock price movement that investors are placing an emphasis on short-term business performance. My suspect is investors are not willing to take the risk to underwrite ADSK recovery today due to the industries it is exposed to. I'm not going to argue that the investors are wrong, but I do see an intriguing opportunity to capitalize on the cheap valuation.

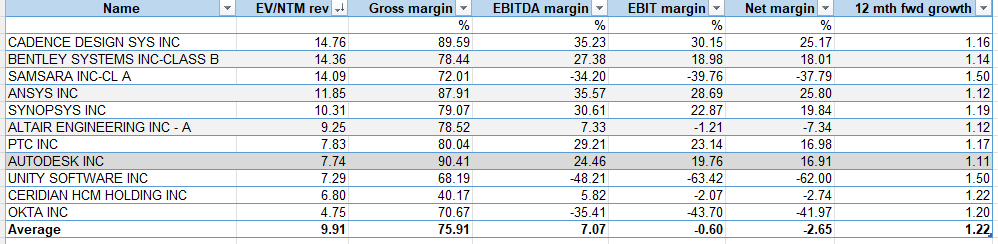

Valuation

ADSK is trading at attractive levels when compared to peers in similar industries, particularly Bentley Systems, Ansys, and Altair Engineering. Looking at the comp set below, while ADSK expected 1-year forward growth is the lowest amongst peers, it has one of the best margin profile – which should improve as it continues to raise prices and completes its transition to annual subscription model. At 7.7x forward revenue, ADSK is trading at as much as 50% discount to peers, which I see as unwarranted, and the stock should re-rate eventually.

{kind=link}

Bloomberg

Risks

The risk here is how long can ADSK continue to sustain growth at the mid-to-high end of its mid-term guidance range – 10 to 15%. The problem is a lot of growth is being driven by price increases and renewals, which I guess it is alright as ADSK serves a very critical function in the users workflow process. But, it is not winning enough users despite the TAM being extremely huge. The worry is ADSK is continuously depending on its legacy base of users that are stuck with them, and not capturing new wave of users as well as I expect.

Conclusion

Despite short-term headwinds due to macro cycles, the market has derated ADSK's valuation, creating an opportunity for investors. While near-term outlook may be impacted by cyclical end markets, positive factors include projected growth acceleration, traction with key products like Fusion 360, and improving renewal rates. The shift to an annual payment model may lead to increased volatility and lower free cash flow in the near future but offers potential price-hike opportunities. Although ADSK faces some risks, such as sustaining growth and capturing new users, its strong margin profile and discounted valuation relative to peers make it an attractive investment.

For further details see:

Autodesk: Valuation Is At Attractive Levels Relative To Peers