ATHM - Autohome: Leading Chinese Automotive Platform Operator

Summary

- ATHM is currently the biggest auto platform operator in China, but it is facing stiff competition from rivals as evidenced by recent industry data.

- On the flip side, the positives for Autohome include the presence of new growth opportunities and the company's meaningful share repurchases.

- I rate Autohome's shares as a Hold; I am worried about potential market share loss driven by tougher competition, but I have a positive view of ATHM's new growth drivers.

Elevator Pitch

I award a Hold investment rating to Autohome Inc.'s ( ATHM ) [2518:HK] stock. On the positive side of things, ATHM is actively looking at new growth opportunities, and it continues to return excess capital to shareholders via buybacks. On the negative side of things, industry metrics imply that competitors are giving Autohome a run for their money. Therefore, I have a mixed view of ATHM's shares which explains why I have chosen a Hold rating for Autohome.

Company Description

In its fiscal 2021 20-F filing , Autohome describes itself as the biggest "automotive service platform" operator in China based on the number of "daily active users" for 2021 according to data sourced from QuestMobile .

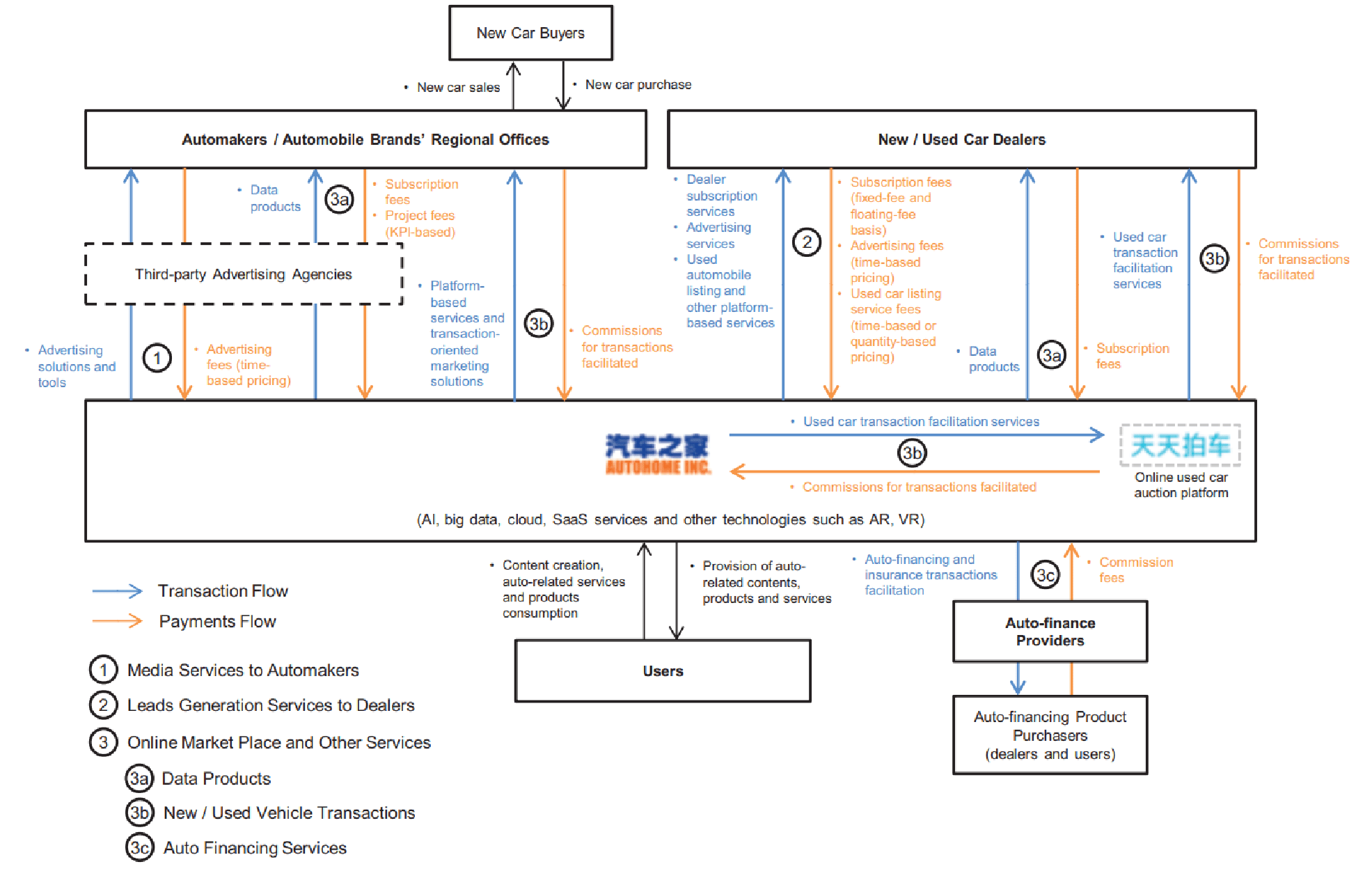

An Overview Of ATHM's Business Operations

{kind=link}

Autohome's IPO Prospectus

As per the chart presented above, Autohome's key revenue streams are lead generation services, online marketplace products & services, and media services which accounted for 41%, 31%, and 28% of its FY 2021 top line, respectively.

Intensifying Competition Is The Key Concern

I highlighted in the preceding section that Autohome was the market leader in the Chinese auto service platform space in 2021. But industry data suggests that Autohome's key competitors could be potentially growing their respective market shares at the expense of the company.

According to a November 4, 2022 research report (not publicly available) issued by Guotai Junan Securities titled "V-Shaped Rebound" citing data from Chinese automotive research firm MoonFox , the gap between ATHM and its closest rivals is narrowing.

In the third quarter of 2021, the number of daily active users for Autohome was +32% higher than that for Dongchedi. A year later in the third quarter of 2022, Dongchedi's daily active users were a mere +8% lower than the number of daily active users that ATHM had in that quarter. Furthermore, Dongchedi had 32% of its monthly active users which interacted with the company's platform on a daily basis for Q3 2022 as compared to Autohome's relatively lower daily active users-to-monthly active users metric of 27% in the same quarter.

Another one of ATHM's key rivals, Bitauto, had been much more aggressive in expanding its user base in the prior year. Autohome added a reasonably good 26.8 million new users in the first nine months of 2022. But this was inferior to Bitauto's 31.4 million new user additions for the 9M 2022 period.

As a comparison, ATHM boasted a 29.9% revenue share of the Chinese auto advertising and leads generation segments in 2019, as per Chinese market research firm iResearch's findings. In contrast, the second and third largest players had much lower market shares of 16.8% and 3.9%, respectively in the same year. Although iResearch didn't disclose the names of the second and third biggest automotive platform operators in its research, they are likely to be Bitauto and Dongchedi, respectively in my opinion. It is reasonable to come to the conclusion that the market share differential between Autohome and its peers might have shrunk in the past three years.

In summary, Autohome is probably still the leading automotive platform operator in China, but the company's rivals are catching up fairly quickly.

New Growth Opportunities And Shareholder Capital Return Are Key Positives

It is a concern that ATHM's competitors are gaining ground, but there are also bright spots for the company relating to new growth drivers and its share buyback program.

Autohome can possibly deliver better than expected revenue expansion in the future despite competitive pressures, if the company is able to capitalize on new growth opportunities.

At the company's most recent Q3 2022 earnings briefing in November last year, ATHM revealed that sales derived from NEVs surged by +141% YoY in the third quarter of the prior year. Moving forward, Autohome's strategy is to open new physical stores focused on NEVs called "Autohome New Energy" as a means of increasing its future revenue contribution from this segment. ATHM's first physical store opened its doors to consumers in Shanghai in September 2022, and the company has plans in place to establish more of such stores to showcase new NEVs in the near future.

Separately, Autohome disclosed at Jefferies' ( JEF ) 2023 Asia Internet Corporate Access Conference in early-January that the company has the intention to establish an "one-stop transaction platform" for "used cars", according to a January 5, 2023 Jefferies report (not publicly available). This might be a new growth driver for ATHM. Earlier in October 2020, ATHM had made an announcement highlighting that it had invested in an "auction platform for used cars" called TTP Car. It is likely that ATHM can leverage on its stake in TTP Car to support its ambitions of building a new integrated user car platform.

It is also encouraging to note that ATHM has been buying back its shares in a meaningful way. Autohome spent $106.3 million on share repurchases between the beginning of August 2022 and the end of October 2022, and it still has $93.7 million (approximately 2.1% of ATHM's market capitalization) remaining from its current share buyback authorization which lasts till mid-November 2023.

As per S&P Capital IQ's valuation data, Autohome used to consistently trade at consensus forward next twelve months' P/E multiples in the high teens to low twenties range between mid-2017 and early-2021. ATHM is currently valued by the market at a relatively lower 15.4 times consensus forward next twelve months' P/E, which might be attributable to investors' concerns about competition. As such, ATHM's buybacks aren't just a means of returning excess capital, as these share repurchases also send the message that the company sees its shares as undervalued.

Concluding Thoughts

Autohome's shares are deserving of a Hold rating. It is good to see that ATHM is exploring new growth opportunities in the area of NEVs and used cars, but the company is also facing stiffer competition from its closest rivals. Considering both the risks and rewards associated with a potential investment in ATHM, I think that a Hold rating is fair.

For further details see:

Autohome: Leading Chinese Automotive Platform Operator