AZO - AutoZone: One Of The Best Long-Term Investments

2023-03-06 10:51:54 ET

Summary

- AutoZone, Inc. is a company that retails and distributes various automotive parts and accessories.

- The company has performed consistently well, with uninterrupted growth since 2002. AutoZone's share price is up over 500% in the last decade, reflecting management's impressive decision-making.

- We believe AutoZone, Inc. will navigate the current economic slowdown well, with demand remaining resilient.

- The EV revolution is unlikely to impact the business materially in the coming decade, due to the size of their operations and brand value.

- AutoZone's financial performance has been incredibly impressive and is able to achieve >10% free cash flow conversion. Our valuation suggesting an upside of 9%.

Company description

AutoZone, Inc. ( AZO ) is a company that retails and distributes various automotive replacement parts and accessories. AutoZone offers products for cars, SUVs, vans, and light trucks, including new and refurbished automotive parts, maintenance items, accessories, and non-automotive products. AutoZone also offers commercial credit and delivery services through its sales program.

As of August 2022 , it operated 6,168 stores in the United States; 703 stores in Mexico; and 72 stores in Brazil.

Investment thesis

AutoZone, Inc. is a well-established business providing an important service to consumers and businesses. As one of the few dominant players in the U.S., it has the potential to generate robust profits and steady growth in line with population growth/inflation. This is especially valuable in the current economic climate, where investors are seeking defensive businesses which can navigate the next 12 months without being materially impacted.

The objective of this paper is to evaluate whether AZO can be that company. Our analysis will involve an assessment of the company's financial performance and consider how current economic conditions will impact its performance in the coming 12 months. Furthermore, the automotive industry is undergoing a once-in-a-lifetime transformation with the shift towards electric vehicles ("EVs"), and so we will also consider how this will affect the business.

Share price performance

AZO's share price reflects an impressive decade for the business, with an impressive bottom-line performance. This stresses the importance of valuation, as investors today will be paying close to the company's all-time high share price.

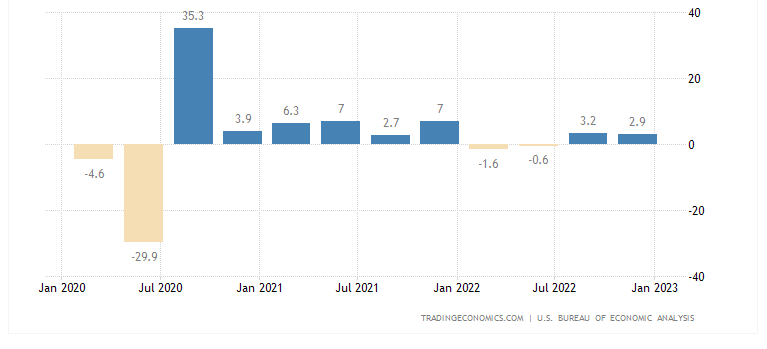

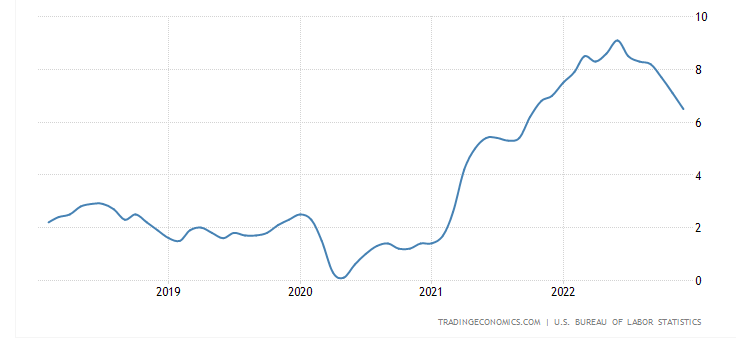

Economic conditions

The current economic conditions can be categorized by softening demand, driven by heightened inflation which has remained persistent. The cause of said inflation is a decade of aggressive monetary policy, energy price disruptions, wage inflation following COVID-19, and persistent supply chain problems.

US GDP growth (Trading Economics) US inflation (Trading Economics)

{kind=link}

{kind=link}

Businesses have been hit hard with margins tightening due to increased production costs, as well as pay hikes demanded by employees. Consumers have not been faring any better, with diminishing incomes and a decrease in discretionary spending.

The central bank's response has been to raise interest rates in an attempt to pull back demand. However, this approach has not been as effective as expected due to the persistent supply-side issues which are less sensitive to interest rates.

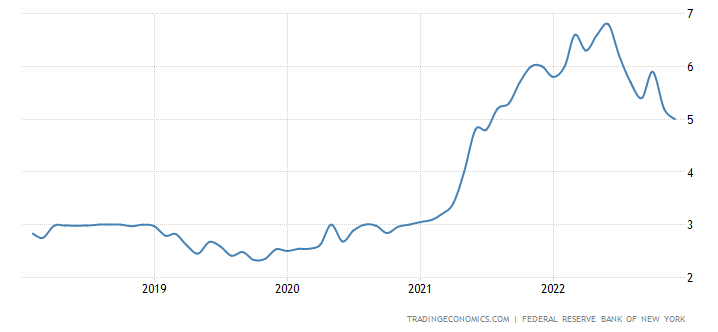

Looking ahead to 2023, our view is that demand will step down further as interest rates remain elevated. Current 12-month inflation expectations remain above 5%, which means further rate hikes are possible.

Inflation expectations (Trading Economics)

{kind=link}

The high cost of living, alongside low consumer sentiment and persistent geopolitical tensions between the U.S. and other nations, is further contributing to the uncertain economic outlook.

The potential impact on AZO is interesting. On one hand, the company should perform relatively well compared to retailers because people cannot avoid spending on necessary maintenance without causing bigger future problems. Additionally, during an economic downturn, people may choose to repair their vehicles instead of replacing them, seeing this as a cheaper option. However, consumers and businesses may also choose to postpone spending or look for more cost-effective options to save money. Using past economic downturns as an indicator, AZO should remain resilient. Between FY07-FY10, the company grew by at least 3.7%, and in FY20, it saw growth of 6.5%, indicating the ability to withstand weak market conditions.

Automotive industry

The retail industry for automotive parts and accessories is known for its intense competition due to traditional retailers and specialists competing together. It is a highly fragmented market, with numerous producers selling directly to local garages. According to Seeking Alpha, there are only 2 specialist players with a market cap in excess of $10BN. This is in an industry that supports the $2.9 trillion behemoth that is the U.S. automotive industry.

Top Automotive retailers (Seeking Alpha)

AutoZone has been able to differentiate itself from its competitors through its broad product offerings, expertise in the automotive industry, and commitment to providing exceptional customer service.

The automotive repair industry is becoming increasingly competitive, with the entry of new players such as discount retailers and online marketplaces. AutoZone has responded by focusing on providing an exceptional customer experience through knowledgeable employees and high-quality parts. This is a concern, as consumers in theory could purchase items from Amazon and take them to a local garage / conduct the work themselves. Realistically, however, most consumers are not sophisticated enough regarding cars or do not have the time to attempt this.

Reportlinker predicts the industry will grow at a rate of 3.84% in the next five years. Although this is lower than AZO's 10-year growth rate of 6.6%, this should not be interpreted as underperformance but rather highlights AZO's potential to outperform its peers by leveraging its well-established brand image.

Fuel prices

Fuel prices have increased substantially in the last year due to sanctions imposed on Russia after its invasion of Ukraine. OPEC and other oil-producing nations have shown no urgency in increasing supply, which will likely contribute to an extended period of time with oil prices above $70.

This has led to a significant increase in gasoline prices in the U.S., reaching levels not seen since 2014. This has both short-term and long-term negative impacts on the traditional internal combustion engine vehicle industry. In the short term, consumers may opt for alternative transportation options such as trains, buses, and walking due to high fuel costs. This, combined with inflation and increased borrowing costs, is putting pressure on consumers' income. As a result, there will be less vehicle use and thus reduced demand for maintenance and parts. In the long-term, this could encourage consumers to shift towards electric vehicles, which is a negative impact that will be discussed further. According to the EIA, crude oil is expected to average $83 per barrel in 2023 and decrease only slightly to $78 in 2024. This indicates a prolonged period of elevated fuel prices, which will only act to exacerbate the aforementioned factors.

EV revolution

The shift towards electric and autonomous vehicles is expected to have a significant impact on the automotive repair industry. It is not a matter of "if" but "when" the transition from gasoline-powered vehicles to EVs/AVs will occur. Electric vehicles have fewer moving parts, which reduces the likelihood of breakdowns and repairs. Further, they require more complex parts, many of which are OEM only and are far more complicated to repair. This creates a complex transition for the parts market as it is not as simple as beginning to stock EV parts.

AutoZone has the opportunity to invest in the required staff training and changes to the infrastructure required but realistically, the business needs support from the EV producers. The company could partner with electric vehicle manufacturers to offer specialized services and products. Given the company's geographical footprint, it offers enough value to an automotive major for this to be a realistic option.

However, it should be noted that the growth of electric vehicles is a double-edged sword for AutoZone. While EVs present new opportunities as the industry grows at a rate in excess of ICE-powered vehicles, it also poses a threat to the traditional parts business. Thus, expanding into this industry will involve the cannibalization of its current business.

We acknowledge the possibility of AZO becoming redundant, although we consider the risk to be minimal. The shift towards electric vehicles has been slow in the U.S., and the government's target is to only have 50% of vehicles sold be EVs by 2030, compared to Europe where the transition is more advanced. Hence, AZO has ample time to prepare and develop a strategy before gasoline-powered vehicles are significantly replaced by EVs.

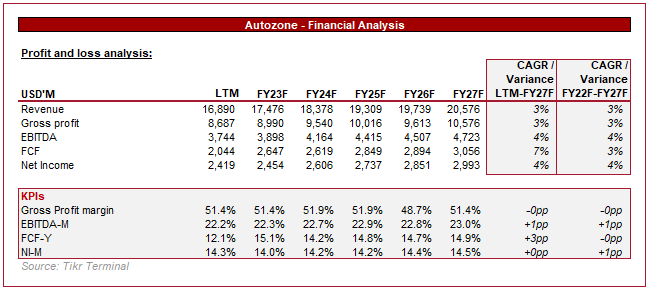

Financials

AutoZone Financials (TIkr Terminal)

{kind=link}

Profit and loss

Analyzing AZO's financials has been a pleasure. The financials are exceptionally clean and operationally superior, without any significant red flags.

Revenue has consistently increased at a 7% CAGR with minimal fluctuations. The business is highly efficient, and this stability can be attributed to the factors discussed previously, which suggest demand is fairly inelastic.

Gross profit margin have consistently remained within a 300bps range for over 10 years. Although it has slightly decreased by less than 100bps in the latest period due to inflationary pressures, this is insignificant compared to the declines that many mature retail and production businesses experience from inflation.

Additionally, cost savings have been realized in the S&A expenses, which have grown at a slower rate than revenue, leading to an increase in bottom-line profitability.

The business's profitability is remarkable, with a net income margin of 15% and a free cash flow yield of 12%, which is considered market-leading in the retail industry regardless of segment. This consistency is especially noteworthy, as the retail industry is often known for its cyclical nature.

Balance sheet

AZO's balance sheet is equally as impressive. Many retailers are currently struggling with poor inventory management, resulting in inflated balance sheets which will likely be unwound by discounting the products and thus reducing their margins. This is not the case for AutoZone, which has actually seen inventory turnover increase. Further, they have managed to further improve cash conversion, which is now over a month. This is a testament to management's drive for efficiencies.

The business is cash rich and has utilized it to finance substantial share buybacks in recent years. The company's investment in capex and store openings has remained consistent relative to revenue, leading us to believe that this is an appropriate use of capital.

The company has bought back so many shares that there are only 18.77 million outstanding, for a business with a market capitalization of $47 billion. With the stock price at a high of $2.5k, a stock split may be worth considering. In the future, it may be unlikely for the business to repurchase shares at the current rate, but it is important for investors to understand that the generated cash is being utilized to directly benefit shareholders.

Based on our credit analysis, investors may be concerned about the company's rising debt, which has partially been used for share buybacks. Despite this, the business maintains a debt-to-EBITDA ratio of less than 2.5x, so we do not view the balance sheet as being heavily leveraged. Management is again maximizing operational efficiency by growing leverage in proportion to the growth of the business.

Outlook

We have a positive outlook for AutoZone in the coming years, with the business able to leverage its strong market position and superior economics to grow at a sustainable level going forward. There do not appear to be any problems that can derail this in the next few years, but the key is how they manage the EV transition when it comes to thinking about 10+ years.

As the following shows, management is continuing to grow its number of stores, with the most recent quarter still showing like-for-like sales growth.

Store openings (Q1 FY23 investor pack)

Analyst consensus financials (Tikr Terminal)

{kind=link}

Analysts' consensus numbers indicate that revenue growth will decline compared to prior periods, but margins will continue to improve. We concur with this view as management has shown a track record of incremental improvements, though we believe the sales growth forecast for the period between FY25F to FY27F is conservative.

Valuation and relative performance

Relative performance

Automaker peers (Tikr Terminal)

The automotive parts industry in the U.S. is dominated by AutoZone and O'Reilly Automotive, Inc. ( ORLY ), who have substantially more market share compared to their peers. This scale advantage clearly translates to profitability, with both AutoZone and ORLY above any other business in the industry. Further, forecast growth is fairly uniform across the businesses. With such dominance over their nearest competitor and the industry as a whole, AutoZone/ORLY will maintain their monopolistic control over the industry and new entrants are unlikely to cause an impact.

Valuation

Automaker Valuation (Tikr Terminal)

The superior performance of AutoZone and ORLY is reflected in their valuation relative to Advance Auto Parts, Inc. ( AAP ). Given the difference in performance and size, it is difficult to assess the fair value of AZ on a comparative basis. Our view is that a fair value for AutoZone would be 15-17.5x EBITDA, based primarily on their consistent free cash flow ("FCF") yield of over 10% and the lack of significant threats in the next decade. A higher valuation of 20x+ EBITDA would be reserved for companies with higher growth prospects.

In order to cross-check this assumption, we have also conducted a discounted cash flow ("DCF") valuation of the business.

Our key assumptions are:

- Revenue growth between 4-5% in the coming 5 years, which is slightly above analyst forecasts but below the levels previously experienced.

- An FCF conversion of 11.5%, which is well below the 5 year average of 16.2%. Our belief is that normalization could occur, driving this down.

- An exit multiple of 15x, reflecting that sticky margins will mean investors will be able to yield at least 10% FCF long-term.

- A perpetual growth rate of 2.75%.

Based on this, we derive an upside of 9%.

Conclusion

AutoZone, Inc. is a mature business that is excellently managed and able to make incremental gains through operational efficiencies. Its growth has been robust, with only 2 years in the past decade showing growth below 4%.

While there may be potential opportunities and challenges, including those not mentioned in this paper such as international expansion, we believe that the management team's track record implies there is no reason to be concerned.

Determining the business's value relative to the market is difficult, so we have relied on a DCF analysis to guide our assessment. This analysis indicates an upside of a 9% and importantly values the perpetual growth in line with an exit multiple of 15x (current trading levels). Some may argue that 9% upside is not enough to justify an investment at this time, but AutoZone, Inc. stock has a history of consistently appreciating and is unlikely to go "on-sale." Attempting to time the market is folly.

For further details see:

AutoZone: One Of The Best Long-Term Investments