AZO - AutoZone: Running On All Cylinders

2023-07-30 05:57:22 ET

Summary

- AutoZone is a US-based company in the automotive replacement parts and accessories sector, with nearly 7,000 company-owned stores throughout the Americas.

- The company's private label brands may represent almost 50% of total sales, and it has achieved above-market revenue growth by expanding its store count.

- AutoZone's historical financial performance has been strong, with outstanding return on invested capital and a conservative capital structure. However, there are risks related to increasing complexity in automobile systems and the impact of electric vehicles.

- At the current price the stock appears to be fairly valued but on any market pullback the stock should be accumulated.

Company Description

AutoZone Inc (AZO) is a US based company which operates in the automotive replacement parts and accessories sector. It sells both directly to consumers through a chain of nearly 7,000 company owned stores throughout the Americas (including Mexico and Brazil) and it also distributes parts to the automotive industry trade (repair garages, car dealers, service stations, etc).

AutoZone retails products sourced from the leading industry branded suppliers and markets its own branded products (private label) sourced directly from low-cost Asian suppliers. Industry commentators estimate that AutoZone’s private label brands may represent almost 50% of total sales.

The company does not provide any break-down of its revenues by market segment or by region.

AutoZone is a sector consolidation story. I estimate that its revenues are predominantly from North America (about 90%). The market is mature, but AutoZone (and its major competitors) has been able to achieve above market revenue growth by expanding its store count and taking share from the very small companies in the highly fragmented tail of the market.

Business Overview

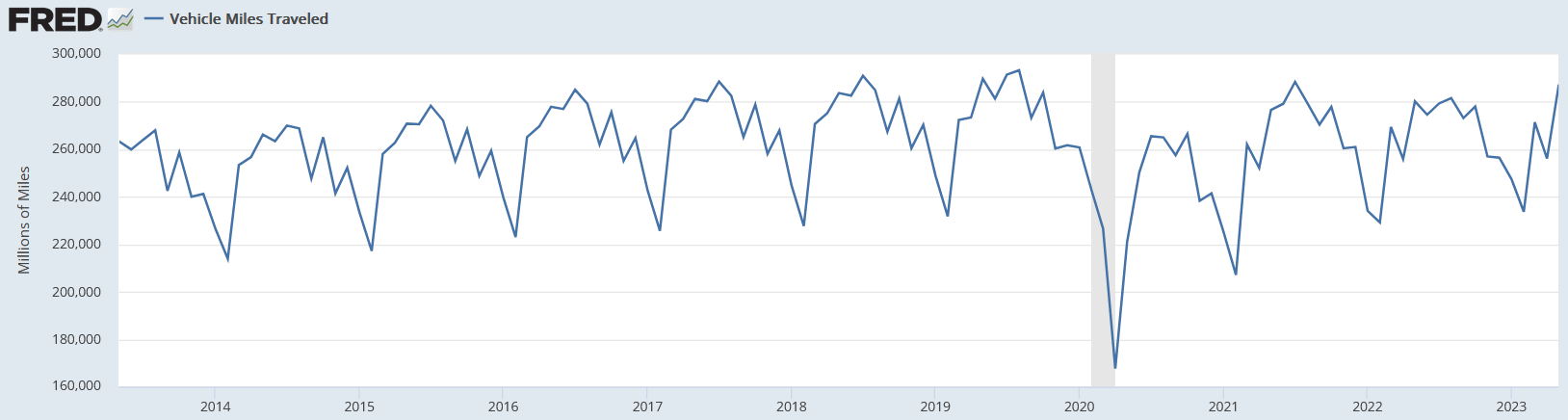

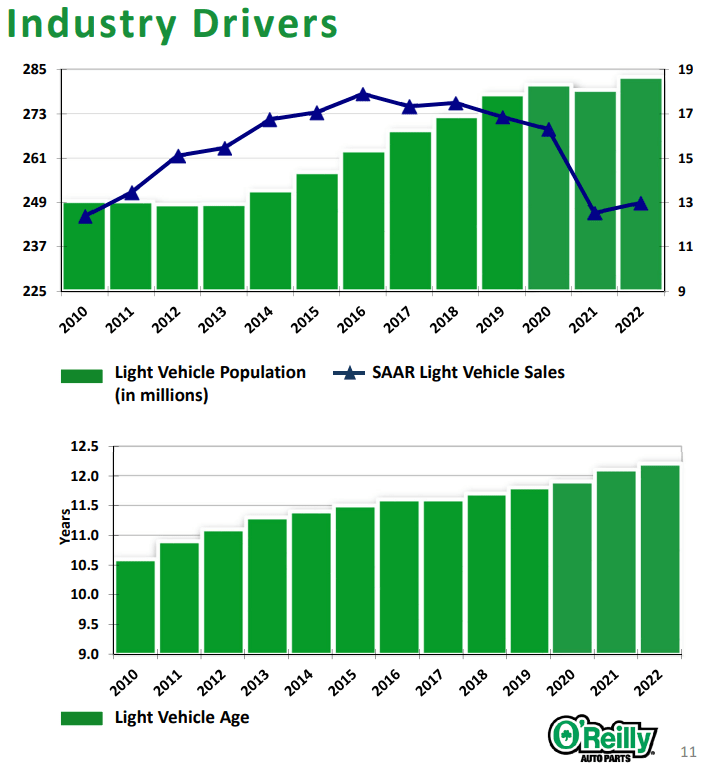

The industry participants believe that demand is influenced by the total number of vehicle miles driven and the average age of the car fleet. Both indicators have had favorable tailwinds (excepting for the short-term impact of COVID-19) as shown in the following charts:

{kind=link}

Pre-COVID the number of vehicle miles was growing at around 1.5% per year. The saw tooth pattern is caused by seasonality with more driving taking place during summer than winter.

{kind=link}

The average age of the light vehicle fleet is increasing at the rate of 1% per year and this trend is not expected to change over the medium term.

According to the industry body, Auto Care, the US automotive aftermarket size at the end of 2022 was about $329 billion in size:

ACA Factbook 2023.

The consensus estimates for future market growth over the next 5 years is between 4% to 5% per year.

It should be noted that AutoZone does not compete in all aspects of this market (collision repair, etc) therefore it’s addressable market may be only 50% of the total market.

The Auto Aftermarket can be segmented into two main elements:

- Do It Yourself (DIY)

This segment is dominated by the retailers who sell primarily to individuals. The on-line component of this segment is significant but reasonably contained due to its complex customer service requirements (a combination of price, availability and technical support is often required by customers).

- Commercial (Do It For Me)

The segment comprises the commercial repair shops, car dealers, etc. The customer requirements for this segment are less price sensitive and more sharply focused on the range, availability, and quality of the products.

Over the last few years, the Commercial market has become the strategic competitive battleground as it has provided the greatest opportunity for the major companies (including AutoZone) to grow their market share.

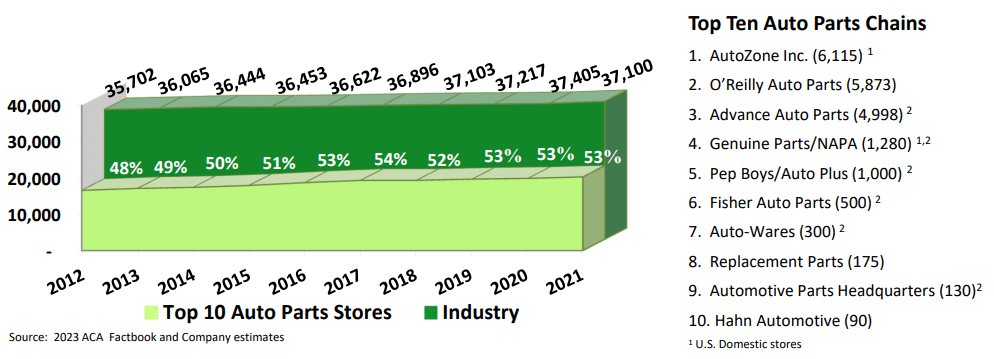

Both of these segments are highly fragmented and competition takes place at the local level. This is highlighted by the following slide which shows the number of retail locations and the major retailers in the segment:

{kind=link}

The market fragmentation ensures that no one company has a dominant market share. The major companies in this market include: AutoZone, Genuine Parts Company (GPC), Advanced Auto Parts (AAP) and O’Reilly Automotive (ORLY).

AutoZone’s Historical Financial Performance

AutoZone’s historical revenues and adjusted operating margins are shown in the chart below:

Author's compilation using data from AutoZone's 10-K filings.

The operating margins have been adjusted for the impact of:

- One-off extraordinary expenses in 2018.

- Operating leases (converting the lease payments to debt and depreciation).

The chart indicates that COVID was very positive for the company. It was able to grow revenues and margins throughout the pandemic. It is noted that over the most recent 3 quarters there has been some evidence that margins may have peaked and there has been a “give back” of around 50 basis points.

AutoZone has increased revenues by a little higher than 8% per year over the last 5 years. This has been driven by increasing store counts and by a growing focus on the commercial segment:

Author's compilation using data from AutoZone's 10-K filings.

The strength of a company’s competitive position is generally reflected in its return on invested capital ((ROIC)). My estimate of AutoZone’s historical ROIC is shown in the following chart:

Author's compilation using data from AutoZone's 10-K filings.

AutoZone’s ROIC is outstanding and is in the highest decile for the specialty retail sector.

The company’s value proposition (which includes a blend of brand, pricing, convenience, reliability, etc) is clearly resonating with its target market and appears to be very sustainable.

AutoZone’s Capital Structure

I do not have any significant concerns over AutoZone’s capital structure. The following chart shows the shift in the mix of its debt (including operating leases) and market value of equity over time:

Author's compilation using data from AutoZone's 10-K filings.

The chart indicates that AutoZone has been reasonably conservative in managing its debt levels and the increase in the market value of its equity has kept the company’s debt ratio well below the sector’s median of 37%.

The company has ample balance sheet capacity to withstand most near-term macroeconomic situations.

AutoZone’s Cash Flows

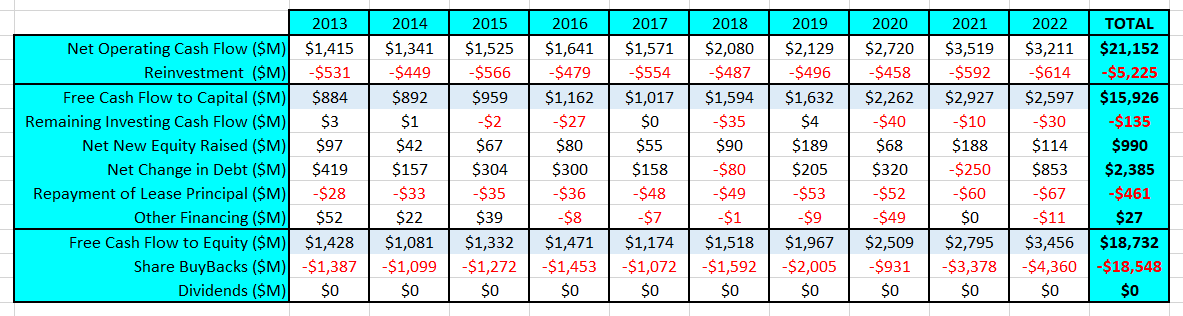

The following table summarizes AutoZone’s cash flows over the last 10 years:

Author's compilation using data from AutoZone's 10-K filings.

{kind=link}

The AutoZone business is not very demanding on reinvestment. It only requires 4 cents in every sales dollar. Over the last 10 years AutoZone has generated 14% free cash flow to capital from sales (this is significantly higher than companies like Home Depot).

AutoZone does not pay a dividend and returns cash to shareholders only through share buybacks. The share buybacks are partially funded by additional debt (about 13% of the debt is used for buybacks). The level of recent buybacks have been significantly above the 10 year average but at this stage appears to be sustainable provided there is no deterioration in business conditions.

In summary, AutoZone is an excellent converter of revenues to free cash flow with relatively modest reinvestment requirements.

Key Risks Facing AutoZone

The 2 key threats to AutoZone’s business are both driven by technology – will the increasing complexity in automobile systems threaten the level of DIY maintenance and what will be the impact of electric vehicles (EV)?

Cars are becoming increasingly more complex which makes it more difficult for DIY repairs other than very basic tasks. AutoZone is aware of this threat to the DIY segment hence the strategic focus to build up the commercial channel. Although not officially reported by the company, with some manipulation of the financial data the level of commercial sales can be estimated. I believe that commercial sales appear to represent almost 30% of the North American revenues and having been growing at 15% per year for the last 5 years.

Another significant threat is the increasing popularity of electric vehicles (EV). EV’s currently have a low level of market penetration (around 5%) but this is expected to increase over time. EV vehicles will continue to require many of the parts that AutoZone supplies but obviously those parts associated with the internal combustion system will not be required. EV’s will be a negative for AutoZone, but I also think that this will be a problem in 10 to 20 years’ time and not in the short to medium term.

Finally, AutoZone sources a large portion of their private label parts from Asia (predominantly China). If the relationship between China and the US were to significantly deteriorate this would have a material impact on gross margins and the profitability of the business.

My Investment Thesis for AutoZone

My scenario for AutoZone continues to be reasonably buoyant and optimistic:

Growth Story

The sector is reasonably mature and the consensus estimates are for growth of around 4% to 5% over the next 5 years. AutoZone will continue to participate in the consolidation which is taking place amongst the “tail” of the sector (with particular focus on the commercial segment in the US). The consolidation will take place via competitive actions and not by acquisition. This should enable AutoZone to achieve revenue growth of 8% per year for the next 5 years.

Margin Story

The COVID pandemic enabled margins to be expanded but this is now reversing, and margins will settle back at the pre-COVID levels. Competition (particularly with O’Reilly) appears to be reasonably “orderly” therefore I don’t expect any further significant margin pressure as a result of competition as AutoZone (and the other major players) slowly increase market share.

Growth Efficiency

AutoZone’s current sales / net capital ratio is around the sector’s 70 th percentile. Over time I expect that AutoZone will be able to slow its reinvestment rate back to the sector’s median.

Risk Story

The sector has a relatively low cost of capital compared to the market average (I estimate that AutoZone’s current cost of capital is around the market's 25 th percentile) due to its relatively stable cash flows. I have assumed that the terminal cost of capital is between the current level and the market median (the increase reflects some of the longer-term risks to AutoZone’s business model).

Competitive Advantages

I have assumed that AutoZone’s competitive advantages remain and allow the company to earn above its cost of capital in perpetuity.

Key Assumptions in AutoZone’s Valuation

The following table summarizes the key inputs into the valuation:

Author's model inputs.

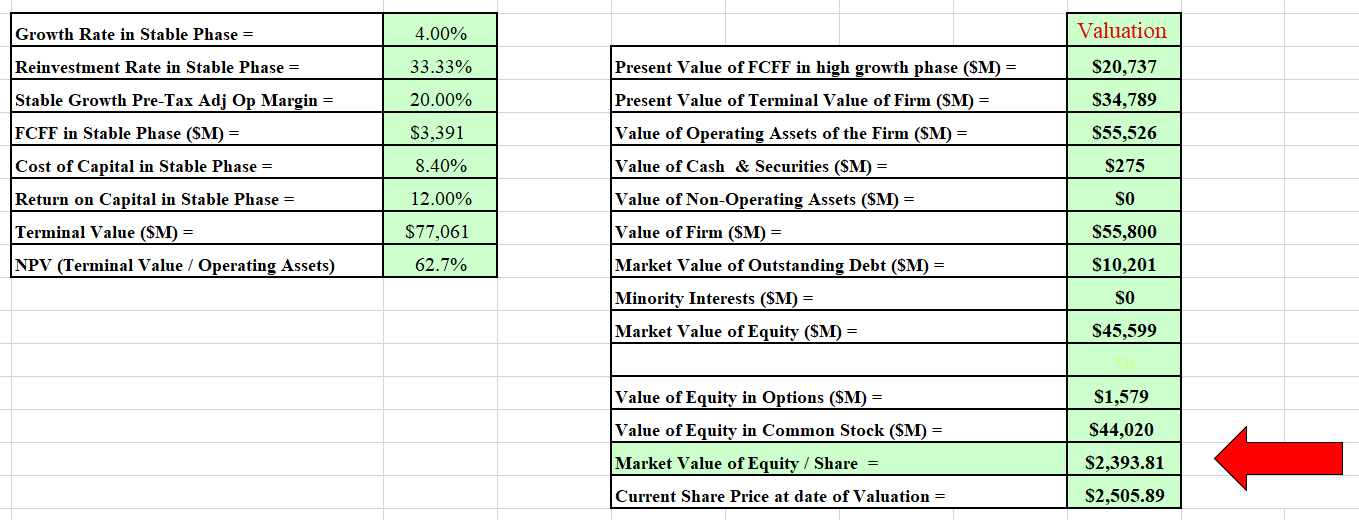

Discounted Cash Flow Valuation

The output from my DCF model is:

Author's model.

{kind=link}

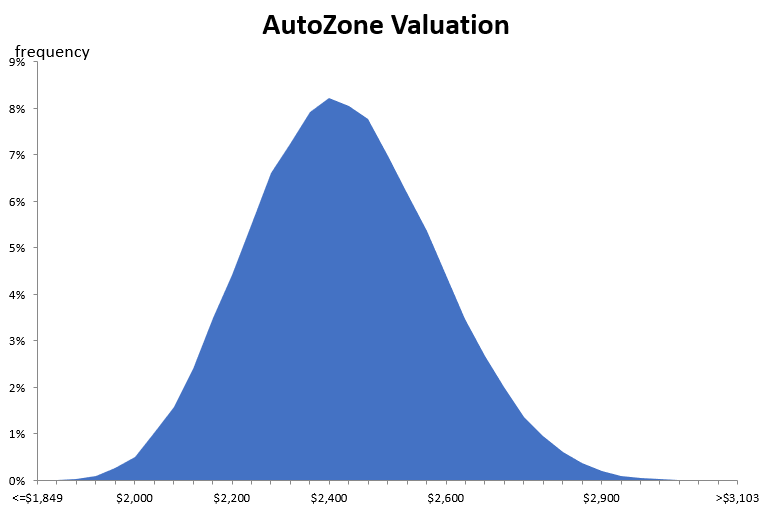

I also developed a Monte Carlo simulation for the valuation based on the range of inputs for the valuation. The output of the simulation was developed after 100,000 iterations.

{kind=link}

The Monte Carlo simulation not only indicates the extremes of the valuation, but it can be used to help understand the major sources of sensitivity:

- 53% of the variation comes from the revenue growth estimate.

- 28% of the variation comes from the operating margin estimate.

The simulation indicates that based on my future scenario AutoZone’s intrinsic value is between $1,849 and $3,103 per share with an expected value around $2,395.

Based on my scenario I conclude that AutoZone’s shares are currently fairly priced.

Final Recommendation

AutoZone is a leading US brand and because of its customer value proposition has been able to generate high returns on capital. From an investment perspective, long term shareholders have done extremely well and have earned returns well above the market.

The auto parts sector is relatively mature but highly fragmented and this has enabled AutoZone to grow much faster than the sector for a reasonably long period of time as it participated in the sector’s consolidation. There is still more sector consolidation to take place in the US and AutoZone will continue to participate for many years to come. At the same time AutoZone will continue to expand its footprint internationally where it can leverage its value proposition.

Like any investment, if this market thesis is correct, then it is imperative that investors do not over-pay for above trend growth that may not happen.

Is AutoZone today a buy, hold or sell?

I believe that AutoZone is a HOLD at today’s prices. My analysis suggests that the current market price is marginally on the high side of my valuation range.

Given the current macro uncertainty, holders of the stock should carefully consider their current portfolio allocation to AutoZone and ensure that it is within their target allocation.

I currently do not own the stock, but I would certainly buy it if the market presented a price in the lower half of my valuation range.

For further details see:

AutoZone: Running On All Cylinders