AZO - AutoZone: So Good It Drives Me Nuts

2023-10-15 00:55:30 ET

Summary

- Consumer sentiment has taken a significant hit due to inflation and recent events, putting pressure on spending.

- AutoZone Inc. has reported strong financial results, extending its success from previous years despite challenges in its commercial business.

- The company plans to accelerate its store expansion, opening 500 stores within five years, and remains committed to rewarding shareholders through buybacks.

Introduction

This market is very tricky. As I've discussed in countless articles, we're dealing with a vicious mix of sticky inflation, slowing economic growth, and a Federal Reserve trying to balance the fight against inflation and protecting economic stability.

This is doing a number on consumers.

The bottom 80% of households have run out of excess savings, meaning that the longer inflation remains elevated, the bigger the pressure on spending will be.

Bloomberg

Hence, it shouldn't be a surprise that consumer sentiment took a significant hit in early October, marking the most substantial decline in over a year.

Recent events, including the Israel-Gaza conflict, congressional budget disputes, the Speaker of the House's removal, and persistent labor strikes, have contributed to the souring of consumer sentiment - on top of the aforementioned inflation issues.

Wells Fargo

Even worse, inflation expectations are a significant concern from the latest consumer sentiment release.

Short-term expectations, influenced by immediate price fluctuations, have increased, likely due to rising prices for essentials like food and gas. Long-term expectations, critical for maintaining stable inflation, also rose slightly but remained within a recent range.

Wells Fargo

This doesn't bode well for spending.

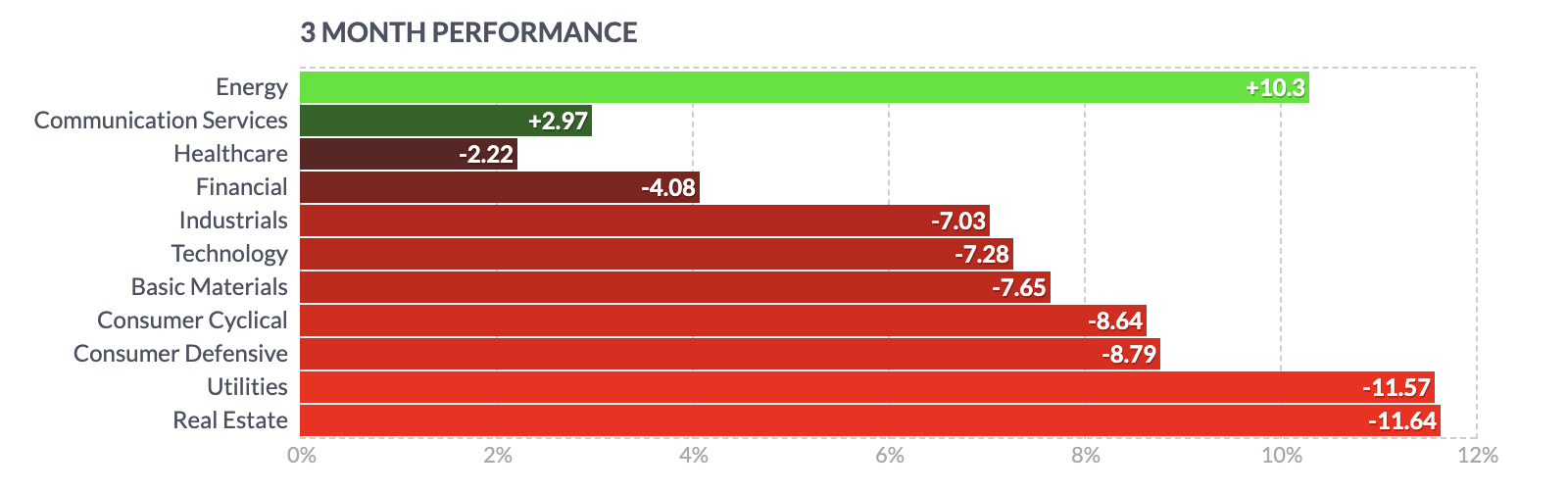

As a result, over the past three months, consumer cyclical and defensive stocks have performed poorly, falling close to 9%.

{kind=link}

This brings me to the star of this article, AutoZone Inc. ( AZO ). As I'm currently hunting for attractive investments, I had (and still have) a close eye on this auto parts retail store.

Unfortunately for me, the stock keeps firing on all cylinders. Over the past three months, the stock has been unchanged, ignoring widespread weakness in consumer sectors.

Since I wrote an article titled The Power Of Buybacks: AutoZone's Dividend-Free Advantage in June, AZO has risen by 5%.

The good thing is that this is fully backed by strong fundamentals. As we'll discuss in this article, the company is firing on all cylinders, offsetting consumer weakness and planning on a more aggressive expansion.

As much as I like that AZO is doing well, it's driving me nuts, as I don't seem to get a good entry. After all, I'm just not willing to buy stocks that are not on sale in this economic environment.

An Unstoppable Force(?)

A few weeks ago, AZO reported its 4Q23 and FY23 financial results. For the fiscal year, total sales grew by 7.4%, and earnings per share increased by 12.9%, building on the success achieved during the pandemic years of 2020 to 2022.

The domestic average weekly sales per store increased by 33% from 2019, driving significant growth in operating profit.

In other words, instead of suffering from tough comparisons, AZO is just extending the success of the past few years.

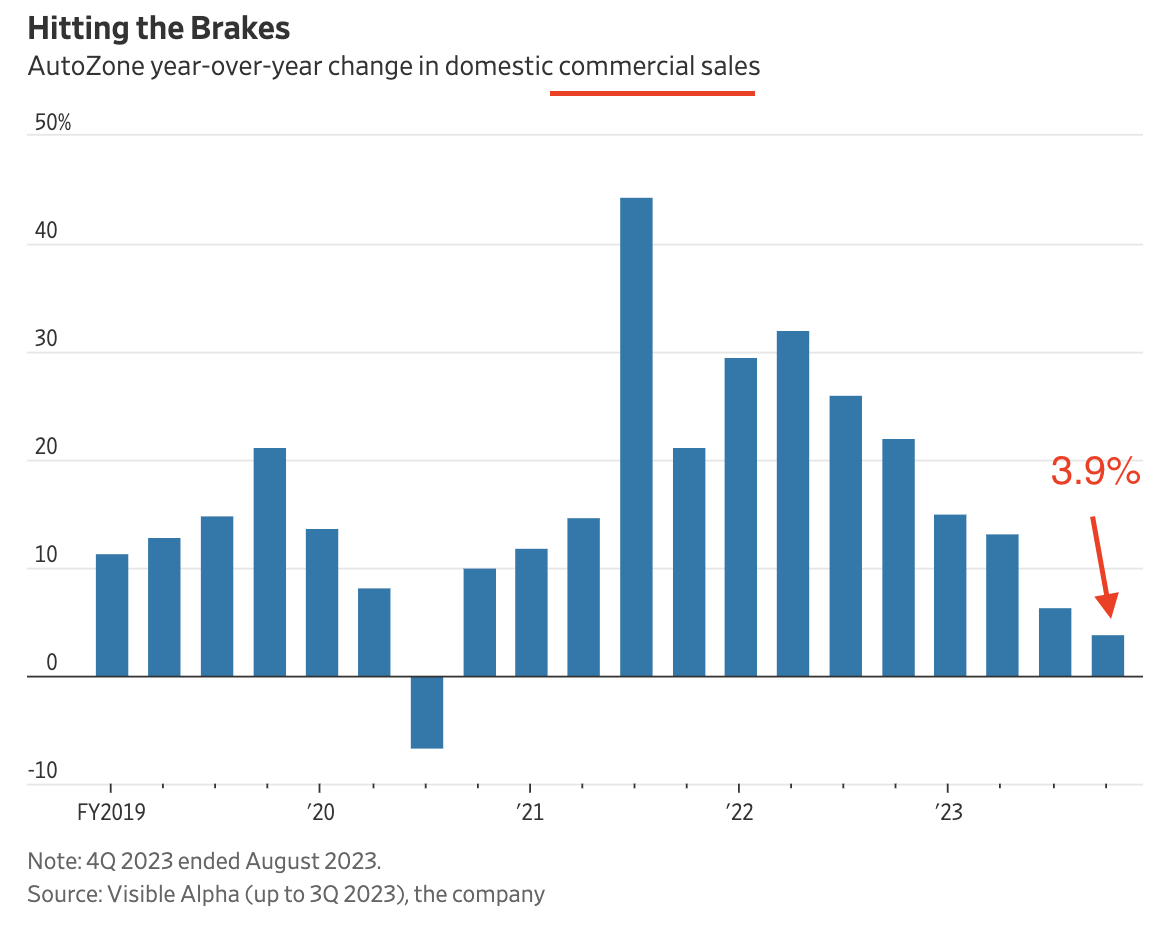

AutoZone's domestic same-store sales growth for the quarter was 1.7%, and the domestic commercial sales grew by 3.9%.

{kind=link}

Inflation resulted in low single-digit price increases, with ticket averages up around 2%. The industry historically increases pricing to maintain margins as costs rise, and AutoZone expects this trend to continue.

While this performance in retail was respectable (using the company's words), the commercial sales performance in the second half of the fiscal year declined. Regional disparities were observed, with the Northeast and Midwest markets underperforming due to a lack of winter weather.

Our performance in retail was respectable and generally in line with our expectations. But as was well documented last quarter, our commercial sales performance in the second half of our fiscal year declined meaningfully and to us unacceptably. We ended with 3.9% growth in domestic commercial sales. - AZO 4Q23 Earnings Call

{kind=link}

As a result, the company has made improvements in execution and completed a strategic review of its commercial business.

{kind=link}

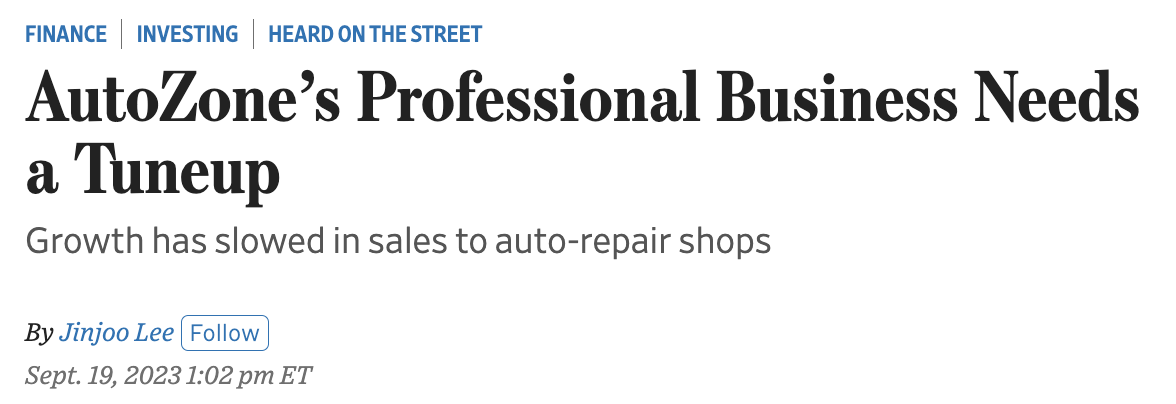

As reported by the Wall Street Journal, which quickly covered an unusual problem at one of the nation's best-run retailers, AutoZone acknowledged challenges in maintaining sales growth within the professional segment compared to competitors like O'Reilly Auto Parts ( ORLY ), which posted an 18% growth in the latest quarter.

The company identified employee turnover and reduced staff experience due to the pandemic as contributing factors, along with the need for improved inventory management and faster delivery times.

Despite these challenges, the broader industry dynamics remain favorable, given the increasing average age of vehicles on the road and a rising share of cars in the age range with high auto parts demand.

The average car in the U.S. is now 12.2 years old.

Wall Street Journal

I believe that this trend will remain up for a number of reasons:

- The energy transition is causing auto producers to switch to electric vehicles. While these vehicles have fewer moving parts and less need for maintenance, they increase the average vehicle prices, causing many people to stick to their old cars.

- Cars have gotten really good (on average). It's attractive for most people to just stick to an old car that works well. I know a few very wealthy people who drive around in > 10-year-old cars.

- Due to economic developments, buying a new car is not feasible for many people.

While S&P Global agrees that this trend continues, it expects this trend to level out next year. However, it needs to be said that this call is on

S&P expects the average age of cars on the road to level out in 2024 as supply chains return to normal, but don't expect prices for new cars to fall. The average new car costs over $48,000 according to Kelly Blue Book. And Toyota expects that number to cross the $50,000 barrier at some point this year.

During the AZO earnings call, the company expressed confidence in its growth prospects for FY24. Despite the underwhelming results in the commercial business, the company's DIY business has remained resilient, and its international business has been growing at a fast pace. In addition, the company's domestic commercial business has been gaining market share and is strong.

The company also emphasized a commitment to long-term shareholder value through strategic investments, earnings growth, and prudent capital allocation. This includes a footprint expansion to achieve the aforementioned market share gains.

Over the last five years, the company has been opening an average of 190 new stores annually in the Americas.

However, they now plan to accelerate this pace and aim to open as many as 500 stores five years from now, with a split of 300 in the U.S. and 200 internationally.

This is what the company said with regard to this somewhat unusual shift in expansion pace (emphasis added):

You may be asking why this change of strategy and why now? The answer is our profitability per store is materially higher since the beginning of the pandemic . We continue to find new trade areas even in our more mature U.S. markets . Our growth in commercial has materially changed the economics on a per-store basis. We believe this is just the beginning on commercial, and our ROIC, one of the most important metrics we track is over 50% . - AZO 4Q23 Earnings Call

This brings me to the next part of this article.

Buybacks & Valuation

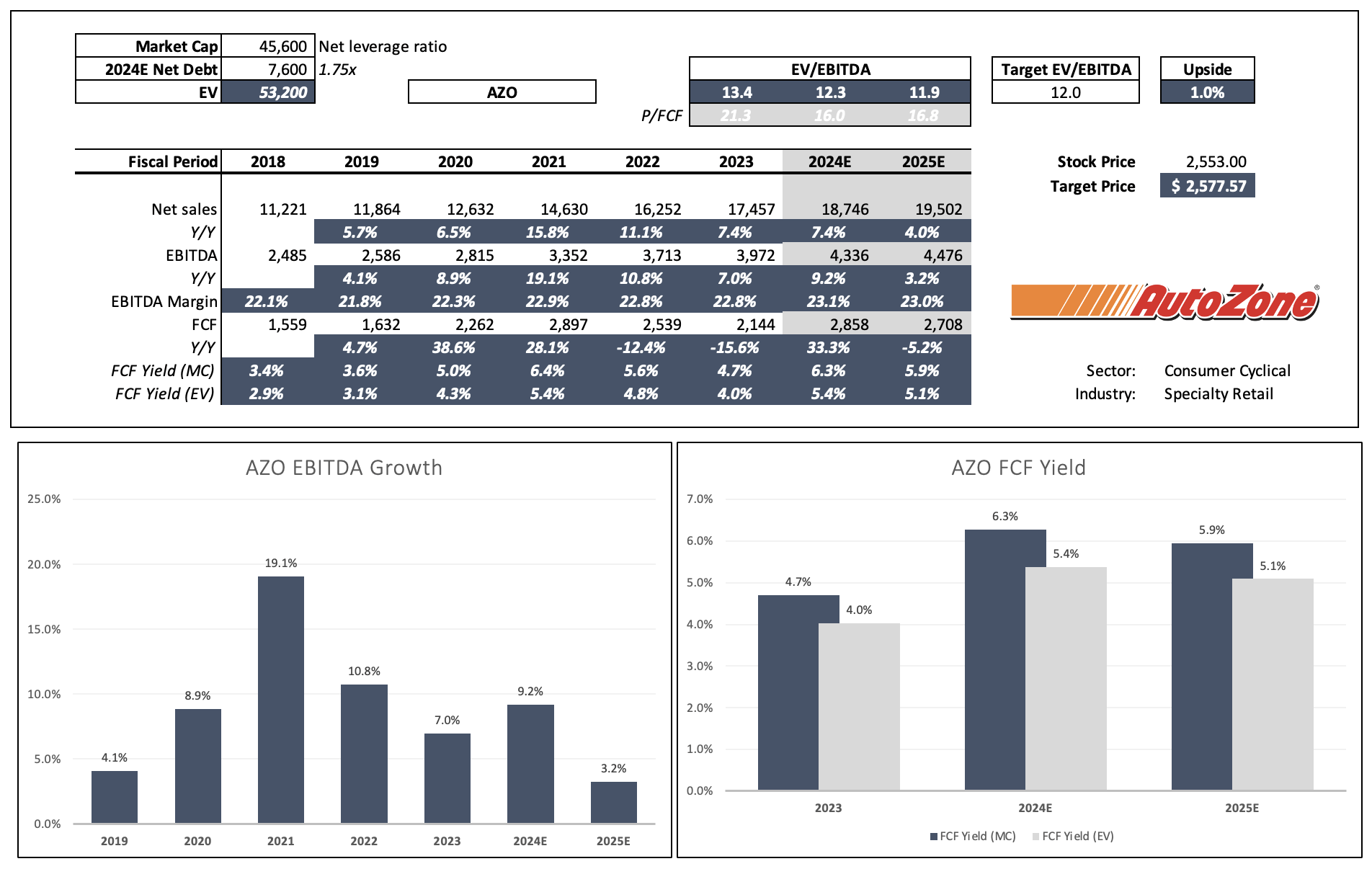

Using FY2024 net debt expectations of $7.6 billion, the company has a very healthy balance sheet with a net leverage ratio of 1.75x. It has a BBB credit rating.

This allows the company to focus on shareholder distributions despite operating in an environment of elevated interest rates.

As a result, AZO keeps doing what it does best: reward shareholders through buybacks.

The strong earnings, balance sheet and powerful free cash we generated this year has allowed us to buy back 8% of the shares outstanding since the beginning of the fiscal year.

[...] We remain committed to this disciplined capital allocation approach that will enable us to invest in the business and return meaningful amounts to cash to shareholders. We finished Q4 2.3 times EBITDAR, which is below our historical objective of 2.5 times EBITDAR. However, we remain committed to our leverage objectives, and we expect to return to the 2.5 times target in FY24.

- AZO 4Q23 Earnings Call

Over the past ten years, AZO has bought back 48% of its shares.

Some people make the case that AZO should start to pay a dividend. As much as I love dividends (I'm a dividend growth investor), I disagree with that.

AZO investors want buybacks. That's why they bought it in the first place. Barely anyone holds AZO shares to bet on a future dividend.

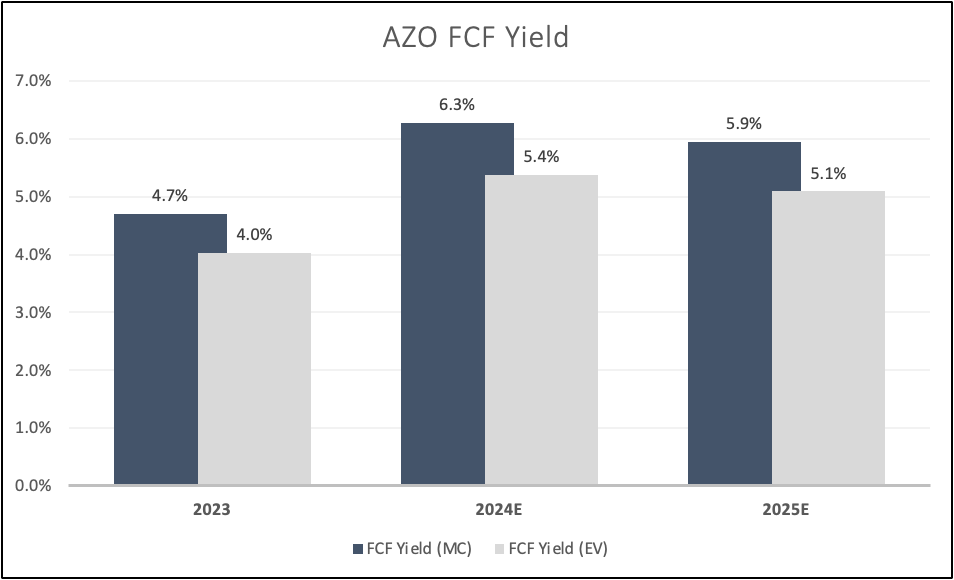

Looking at analyst estimates, the company is expected to maintain a free cash flow yield close to 6% in the next two years. If the company were to spend all of it on distributions, it would have to use roughly a third of that (2%) to pay a somewhat decent yield. That would significantly reduce its buyback power.

Leo Nelissen (Based on analyst estimates)

{kind=link}

A dividend payout wouldn't be catastrophic (and it may happen in the future), but I hope AZO prioritizes buybacks.

With regard to the valuation, I am going to stick with a Hold rating.

Historically speaking, AZO has traded close to the longer-term median of 12x EBITDA.

Using current analyst estimates, the company is trading at 11.9x 2025E EBITDA.

EBITDA growth is expected to remain very strong in 2024 (+9.2%( but fall to 3.2% in 2025, which is why I believe that a 12x valuation is fair.

Leo Nelissen (Based on analyst estimates)

{kind=link}

This implies that the stock is trading roughly at fair value.

I believe that the fair value would be much higher if economic growth were stronger. If the consumer were in a better spot, I have little doubt that the company could maintain consistent high-single-digit annual EBITDA growth (or better).

However, for now, I'm sticking with a 12x valuation and expectations that EBITDA growth is coming down.

Current consensus estimates are a bit more bullish. The average price target is $2840, which is 11% above the current price.

I have put AZO on my watchlist. It's one of the few stocks on there that doesn't pay a dividend.

However, I believe it would make a great addition to my portfolio, as I own just one cyclical consumer stock. Another stock I'm watching is the Tractor Supply Company ( TSCO ), which I discussed in this article .

I want to buy AZO during a 15% to 20% sell-off (I'm looking for $2,200). While this may come with the risks of not being able to buy AZO at all, it's a risk I'm willing to take.

Economic risks could pave the road for stock price weakness, and if I don't get the chance to buy, I'll buy alternatives.

Takeaway

In this turbulent economic landscape marked by inflation and uncertainty, AutoZone emerges as a resilient standout.

With a track record of strong sales and earnings growth, AZO remains unfazed by challenging market conditions. While consumer sentiment takes a hit and inflation concerns loom, AutoZone continues to thrive.

Despite some commercial sales setbacks attributed to employee turnover and supply chain disruptions, the broader industry outlook remains favorable, driven by the aging vehicle population and rising prices of new cars.

AutoZone's expansion plans, aiming to open 500 stores within five years, indicate confidence in its future prospects.

Furthermore, AZO's commitment to rewarding shareholders through buybacks aligns with investor preferences, keeping it on the radar of those seeking growth over income.

Given my view on economic growth and the stock's valuation, I'm on the lookout for an investment if the market offers an attractive opportunity in the next few months and quarters.

For further details see:

AutoZone: So Good, It Drives Me Nuts