XLV - Avadel Pharmaceuticals: Lumryz Approved Launch Expected June 2023 And We Remain Bullish

2023-05-17 02:56:26 ET

Summary

- Key update: as we predicted, FDA approval for LUMRYZ, a unique once-at-bedtime narcolepsy treatment. Orphan Drug Exclusivity is granted until May 1, 2030, offering attractive patent protection.

- Launch expected in June 2023, with a fast sales ramp anticipated considering concentrated (~5,000) prescriber base.

- The label looks fairly clean, boding well for the successful launch.

- Reiterating the buy rating despite potential first-launcher risks, we expect the stock to trend higher with earnings beat, given modest market expectations and valuation.

Update: LUMRYZ approved as expected

As highlighted in our previous article last month , Avadel Pharmaceuticals' ( AVDL ) LUMRYZ has received FDA approval for treating cataplexy or excessive daytime sleepiness in adults with narcolepsy. We remind readers that LUMRYZ is the first and only FDA-approved oxybate medication for narcolepsy that can be taken once at bedtime, and it has been awarded Orphan Drug Exclusivity until May 1, 2030. We consider ODD as the most robust patent protection that the drug can have, de-risking IP-related concerns. The company has stated that the approval is based on the successful results of the Phase 3 REST-ON clinical trial, which demonstrated significant progress in all three primary endpoints. Based on these results, the FDA has deemed LUMRYZ to be clinically superior to existing twice-nightly oxybate products, granting it seven years of Orphan Drug Exclusivity.

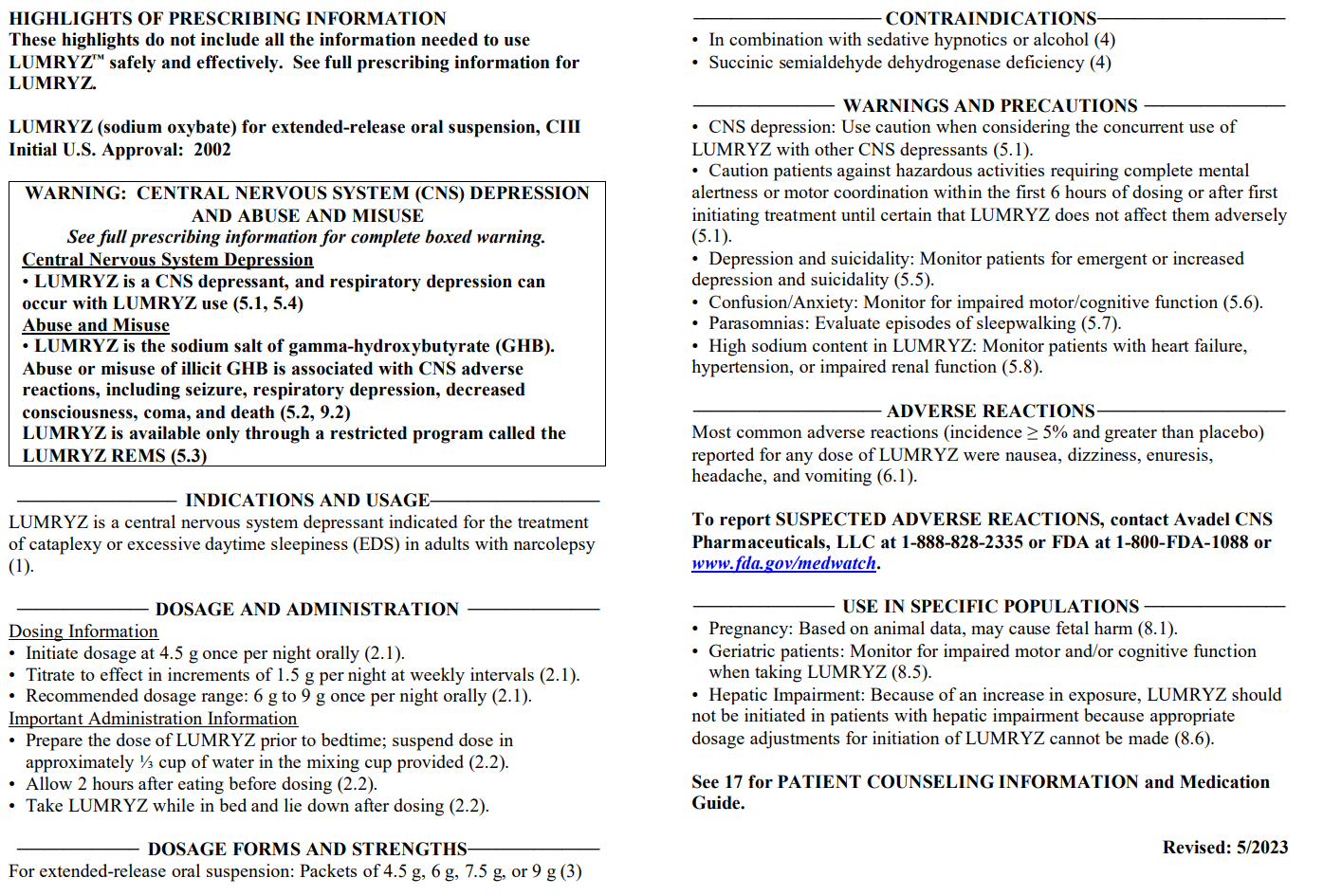

The label aligns with what we expected.

We highlight that the label seems fairly clean, even though there are boxed warnings (i.e., CNS depression, abuse, and misuse concerns). Still, we believe that should be expected, and we are not surprised, considering the drug's mechanism of action (sodium oxybate).

{kind=link}

FDA Monograph (FDA Monograph)

Launch expected in June 2023; fast ramp expected

The company reiterated that they expect LUMRYZ to launch in early June comfortably. That being said, the next key question is how fast the launch ramp would be; here are our reasons why we believe the sales ramp to be fast. Firstly, the market has a relatively small target prescriber base (~5,000 prescribers); secondly, the company's RWE studies would further expedite the market access/pricing negotiations, which we believe the company will disclose additional data in the next few months (faster than expected private and public payer reimbursement can be a big catalyst for the stock). Thirdly, we believe the company has placed efficient pre-launch efforts (built REMS programming and Patient Services Center, already trained sales team (~50 people), payer discussions ongoing, established network with KOLs and sleep specialists, etc.). Of note, the company plans to move forward with 50 personal sales teams and 12 field reimbursement managers, which we believe should be adequate. Furthermore, we appreciate the Orphan Drug Exclusivity that gives 7 years of exclusivity to the drug. The FDA's decision on the ODE was based on the FDA's view that the drug offers major value to patient care over SOC (twice-nightly) drugs.

We agree that the first-time launch presents a potential overhang, and we usually sell into the launch, but scPharmaceuticals Inc ( SCPH ), which we initiated early this year, rocketed 71% during the first few quarters of launch due to the drug's clear clinical benefit and launch preparedness even with a small sales force. Although we do not believe the market expectation around LUMRYZ is that high, the current valuation (~$1.13bn) is modest for the compelling drug that the company holds. Therefore, we maintain a buy rating and plan to hold into the first few quarters of the launch. Furthermore, we believe the RTW deal to be a strong vote of confidence in the drug's commercial success, as royalty investments usually take place after extensive due diligence and are more focused on downside protection.

More detail about the RTW deal can be summarized below:

Furthermore, we note that several recent developments have enhanced Avadel's preparedness for a potential Lumryz launch. These developments include an equity offering, an RTW royalty agreement, and a convertible notes exchange, which raised approximately $165 million in cash and delayed the maturity of AVDL's $96m convertible debt until 2027. Additionally, AVDL will gain access to $45 million upon achieving quarterly sales of at least $25 million by 2Q24. We see this net positive for the company as it can provide a robust cash runway for a couple of years and support Lumryz's launch, expected in June 2023.

Risks

- Underwhelming sales print during the first few quarters due to unforeseen hurdles around step-edits and prior authorization may take place hurting the physician prescribing momentum.

- Payer and reimbursement headwinds.

- If the company doesn't turn cashflow positive on time, it may need to raise more cash, leading to shareholder dilution. However, the recent royalty agreement with RTW will provide enough cash buffers for the next few years, even if the sale falters, and we are not too worried about it.

Conclusion

We reiterate a buy rating and plan to keep our position into the first few quarters of the launch. Avadel Pharmaceuticals' LUMRYZ has received FDA approval as a unique once-at-bedtime treatment for narcolepsy, with Orphan Drug Exclusivity until May 1, 2030. The approval is based on positive Phase 3 REST-ON clinical trial results, and the drug has been granted seven years of Orphan Drug Exclusivity for its clinical superiority. With a launch expected in June 2023, we anticipate a rapid sales ramp due to a focused prescriber base and the company's RWE studies supporting market access and pricing negotiations. Furthermore, we believe the current cash balance of $100m represents a robust cash runway considering ~$28m of quarterly cash burn (Q1 23), which will be further off-set by the revenue of LUMRYZ.

Despite potential launch risks, such as underwhelming sales or reimbursement challenges, we maintain a buy rating, considering the modest market expectations and current valuation.

For further details see:

Avadel Pharmaceuticals: Lumryz Approved, Launch Expected June 2023 And We Remain Bullish