CPT - AvalonBay Communities: Better Way To Own Real Estate

2024-01-12 08:10:00 ET

Summary

- Buying rental properties for investment returns may not be as profitable as investing in well-managed REITs like AvalonBay Communities.

- AVB is one of the largest multifamily REITs with a strong presence in supply-constrained regions, leading to higher barriers to entry and less competition.

- AVB has demonstrated encouraging growth, a solid balance sheet, and a reliable dividend history, making it an attractive long-term investment opportunity.

Buying rental properties a common way to invest in real estate, and one way that many mom and pop investors use to measure investment returns from real property is to take the annual rental amount divided by the purchase price.

While this ratio may be higher than the dividend yield of some REITs, it's worth considering that this is before all costs such as property taxes, maintenance, insurance, and mortgage interest is deducted. Moreover, with a traditional mortgage, principal payments must be made on the mortgage, which further eats into real cash flow.

On the other hand, it's worth noting that REITs often don't payout out their entire funds from operations, so the FFO yield that an investor gets from buying a REIT is actually higher than the dividend yield, and the FFO yield is after operating, property tax, and interest expenses have already been paid.

Moreover, not paying out the entire FFO means that the REIT can use retained funds to grow its footprint organically. Also, REITs are able obtain unsecured loans that give them financial flexibility and make interest-only payments on terms that a most individual borrowers cannot get.

That's why it may make sense for hands-off investors to buy well-managed REITs such as AvalonBay Communities ( AVB ), which I last covered here back in September of last year with a 'Buy' rating, noting its solid positioning in a tight housing market and balance sheet strength.

AVB has since fallen and recovered from its lows hit in October, as fears around a higher for longer interest rate environment have subsided, with the price sitting just 0.9% higher since my last piece. In this article, I revisit the stock and discuss why now remains a good buying opportunity for income investors, so let's get started!

Why AVB?

AvalonBay Communities is one of the largest multifamily REITs on the market today, with 296 apartment communities primarily located in or around major metropolitan areas of the U.S. This includes the NYC and New Jersey, Mid-Atlantic, Pacific Northwest, and California.

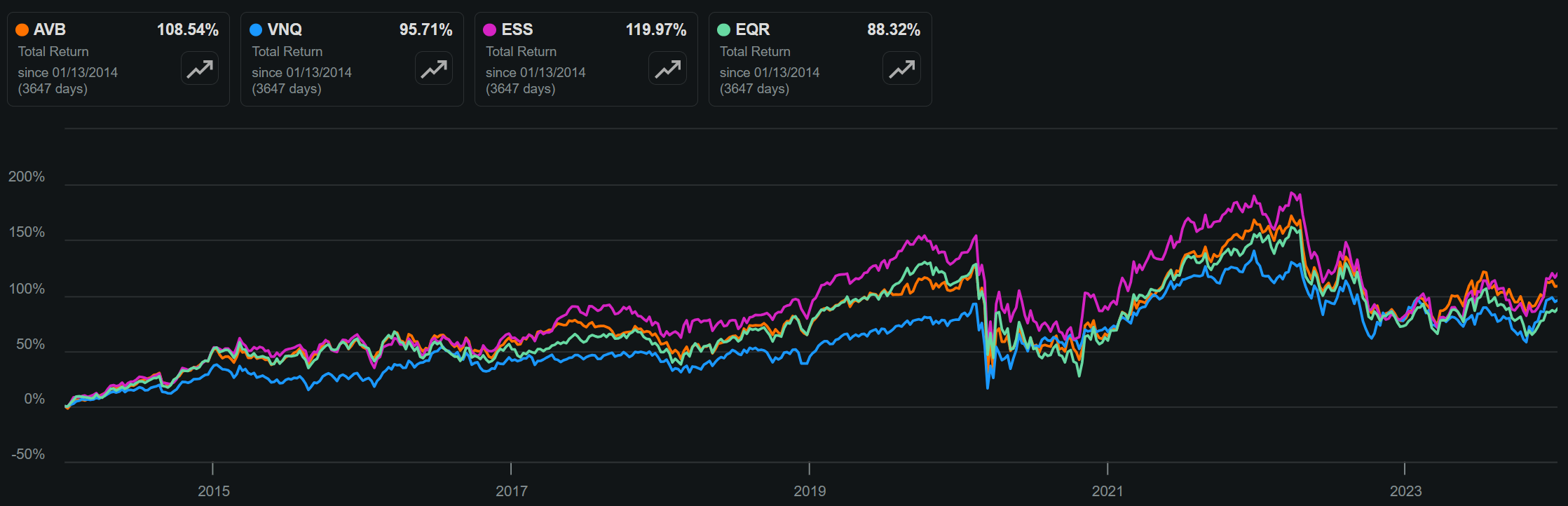

Notably, AVB has generated a respectable 109% total return over the past 10 years, surpassing that of the Vanguard Real Estate ETF ( VNQ ) and peer Equity Residential ( EQR ), while sitting behind West Coast-focused peer, Essex Property Trust ( ESS ). While this isn't a game changing return, investors have gotten paid a growing dividend along the way all while seeing around a 10% annual return that sits on the high end of the historical 6% to 11% annual return of commercial real estate.

{kind=link}

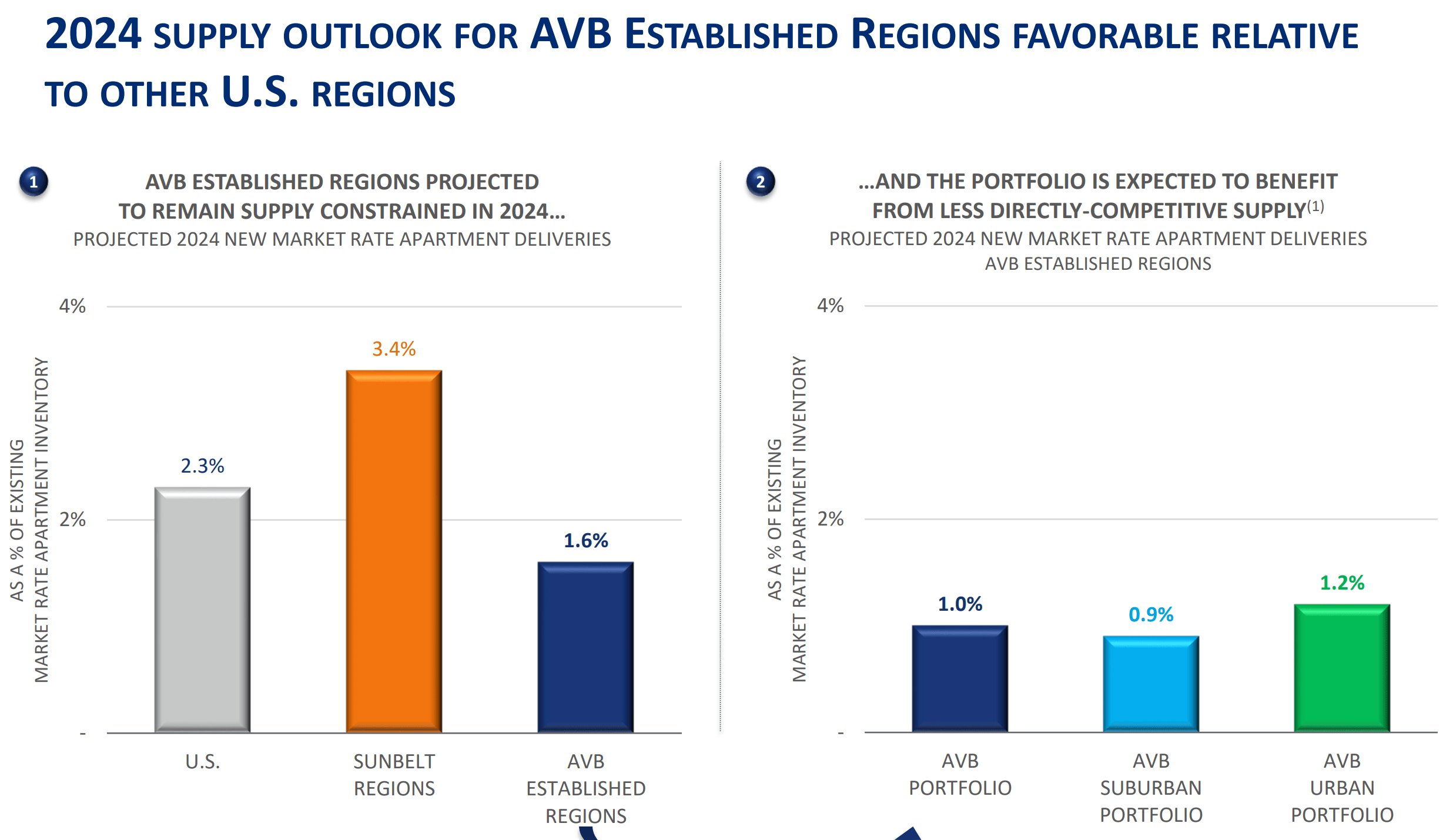

AVB's presence in supply-constrained regions means higher barriers to entry due to cost and less competition. This is supported by estimates that show low new expected supply in AVB's markets compared to the rest of the market. As shown below, new apartments are expected to represent just 1.6% of the total supply in AVB's markets, comparing favorably to the 2.3% average for the U.S. in aggregate.

{kind=link}

Meanwhile, AVB has demonstrated encouraging growth, with Core FFO per share growing by 6.4% YoY during the third quarter, and 9.7% for the first nine months of the year. This was driven by healthy top and bottom line growth at the property level as many regions saw a bounce back in demand. For example, San Francisco (where AVB has a presence) has led its peer cities in the number of workers returning to the office.

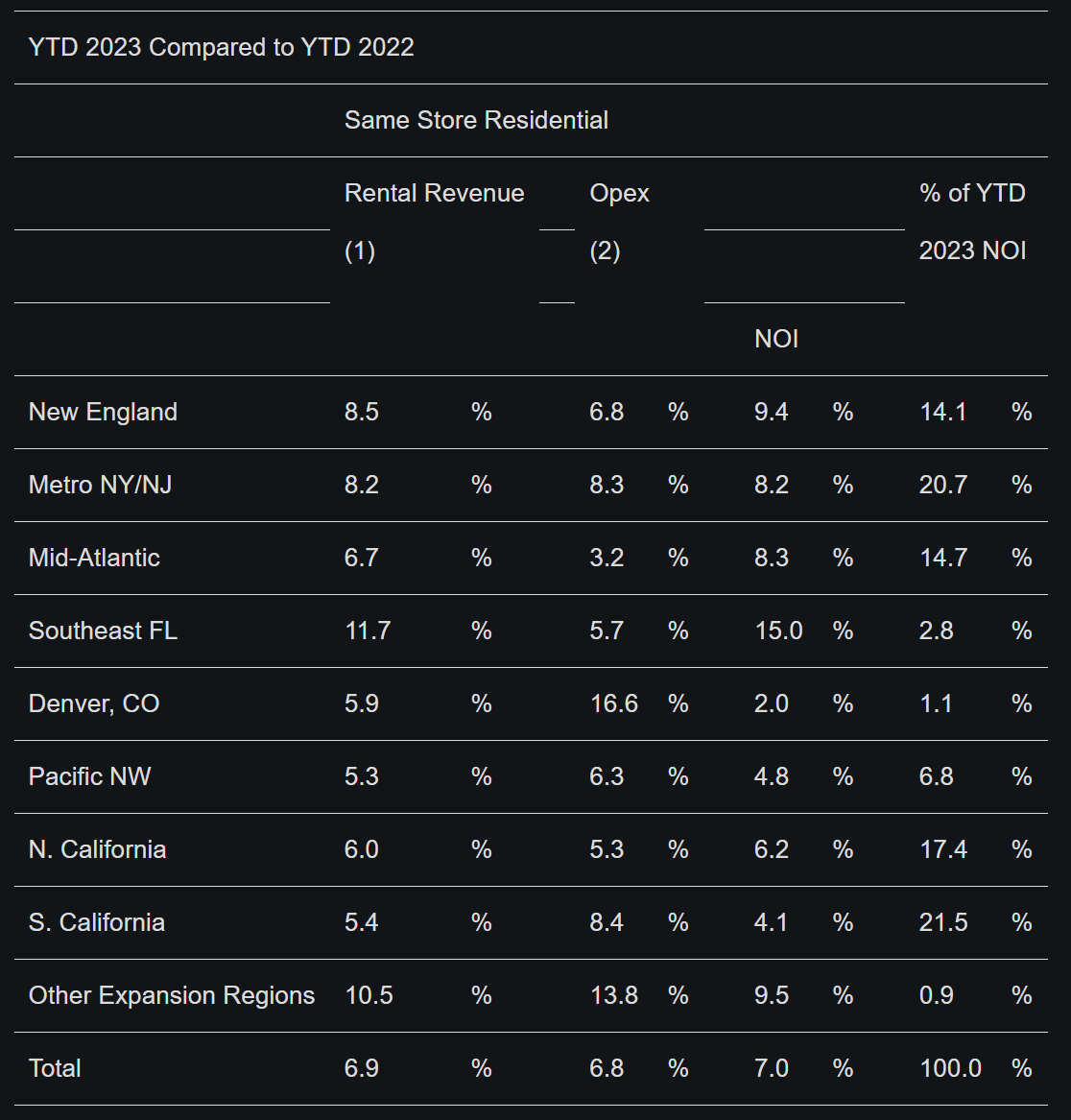

As shown below, early pandemic-era losers like New England, Metro NY/NJ and Northern and Southern California saw strong NOI growth ranging from 14% to 21% during the first nine months of last year, as many workers have moved back to those regions.

{kind=link}

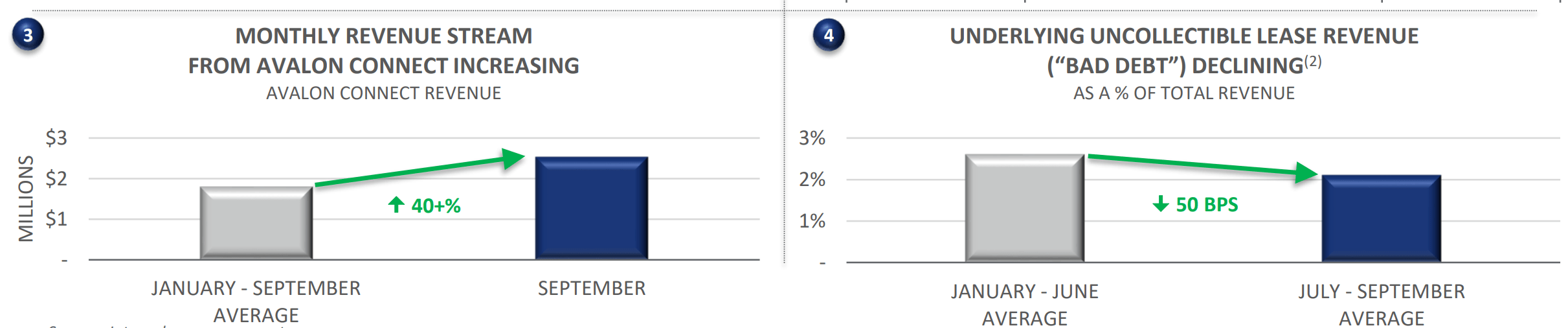

Looking ahead, AVB remains solidly positioned that support its same-store revenue growth in 2024. This is reflected by bad debt expense trending lower on the back of a strong labor market with low unemployment rates , as well as the innovative AvalonConnect offering, which bills residents who opt-in $75 a month for streamlined WiFi, Package Delivery, and Payment Services. As shown below, this service as demonstrated impressive growth in monthly recurring revenue.

{kind=link}

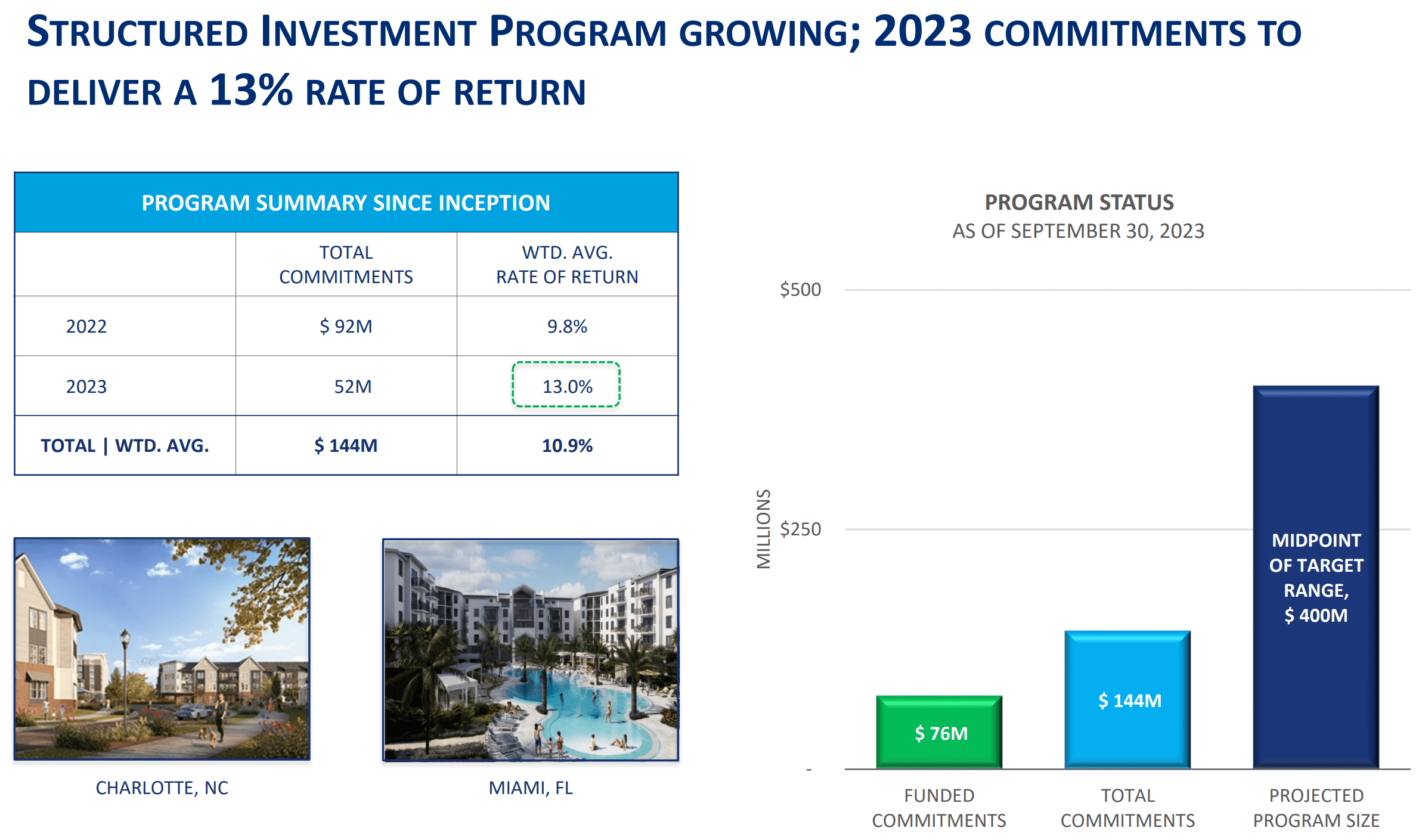

AVB is also positioned to see solid external growth as it's expected to see 4,200 cumulative apartment unit deliveries by the end of this year, at an attractive weighted average stabilized yield of 7.4% , sitting higher than the original 6.5% projection. It should also continue to see elevated returns in its structured finance program, in which it provides mezzanine loans to 3rd party apartment developers. Higher interest rates have driven higher returns on this program to 13% last year (up from 9.8% in 2022). As shown below, this program is expected to grow from $144 million in total commitments to $400 million.

{kind=link}

AVB is also supported by one of the strongest balance sheets among REITs, with a net debt-to-core EBITDAre ratio of just 4.1x, sitting well below AVB's 5.0x to 6.0x target range. It also has a very high interest coverage ratio of 7.5 and 95% of its developments are match-funded with debt, helping to ensure that the timing of interest payments are balanced with stabilization of rent on those properties. After funding open development commitments, AVB is expected to still have $1.6 billion in remaining liquidity.

Notably, AVB pays a well-covered 3.6% dividend yield that's well-covered by a 62% payout ratio. AVB also has a dividend history that dates back 29 years with no interruptions or cuts, including the financial recession of 2008-2009 and the most recent recession in 2020.

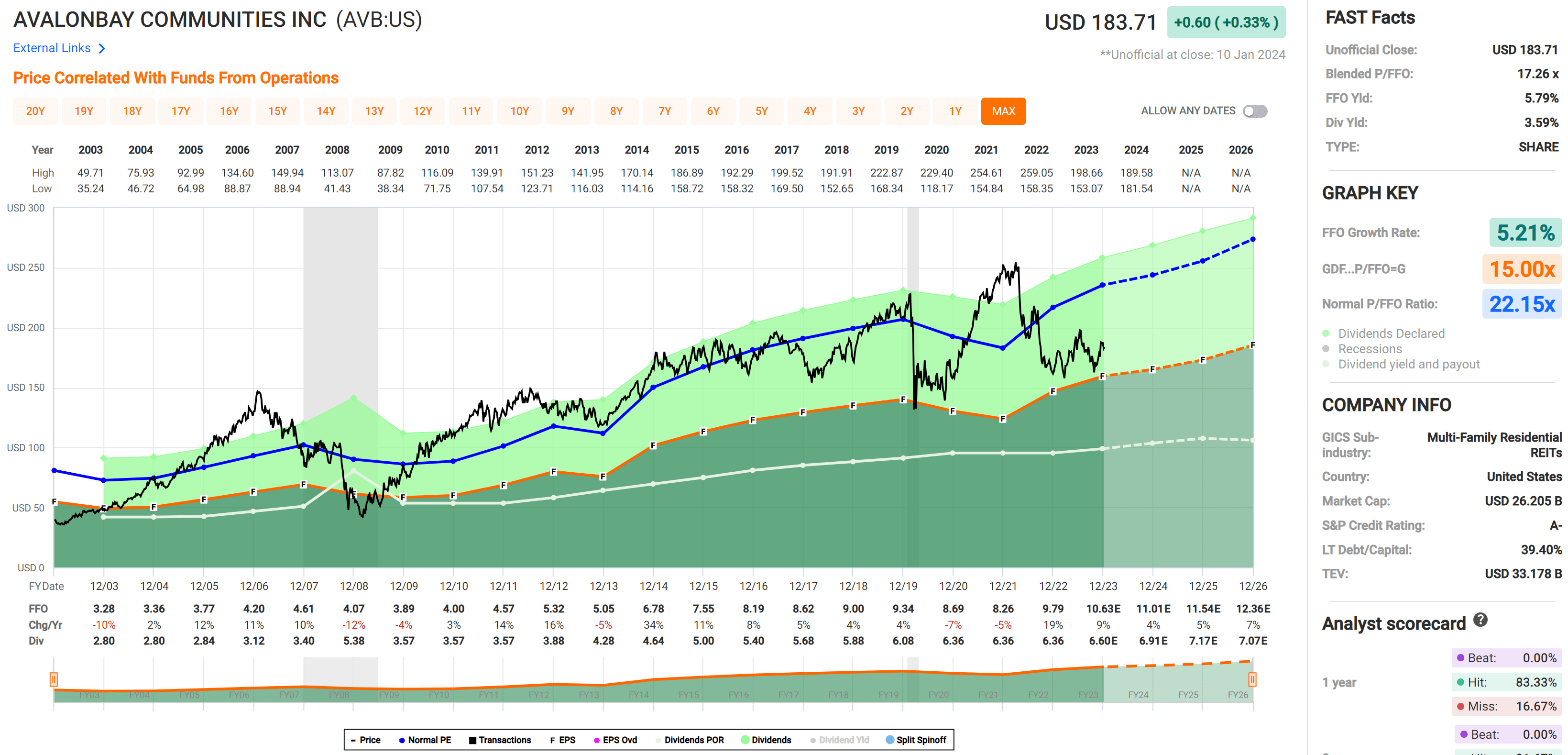

While the dividend yield isn't particularly high, it worth noting that AVB carries a 5.8% FFO yield, based on the current share price of $183.71 with a forward P/FFO o 17.3. This means that AVB could theoretically yield 5.8% if it paid out 100% of its FFO, which is what most private owners of real estate get from their rental properties. The only difference is that AVB is able to utilize its retained capital to fund future growth.

Risks to the thesis include potential for an economic downturn should high interest rates pressure consumers, as that could result in lower rent growth. Also, lower interest rates could introduce new competition from increased supply in its key markets. Plus, AVB's foray into mezzanine lending carries risks, as this funds developments which may come to halt in a recession, thereby resulting in potential losses.

Considering all the above, I continue to see value in AVB at the current price with forward P/FFO of 17.3, sitting below its normal P/FFO of 22.2, as shown below. While AVB is far from being a get-rich-quick stock, I believe it's reasonably attractive considering its high quality portfolio, low leverage, and analyst expectations for 4% to 10% annual FFO/share growth between now and 2026.

{kind=link}

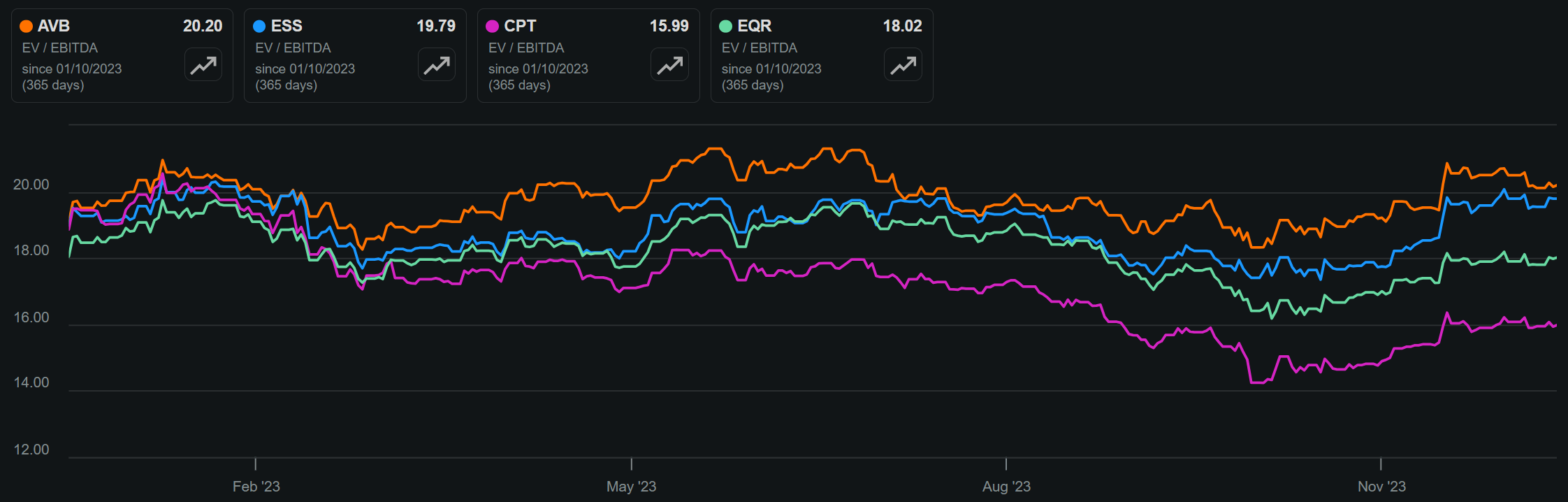

Those who would prefer alternatives may also want to consider Essex Property Trust, Camden Property Trust ( CPT ) and Equity Residential, all of which carry quality multifamily portfolios of their own in many Tier 1 markets. As shown below, AVB's peers all trade at a discount to AVB from an EV/EBITDA standpoint.

{kind=link}

Investor Takeaway

In conclusion, AVB's presence in supply-constrained regions and strong portfolio performance make it a solid investment choice for those looking to diversify their real estate holdings and portfolio. With encouraging growth potential, a strong balance sheet, and a reliable dividend history, AVB presents a compelling opportunity for long-term investors who want a hands-off vehicle for owning property. Lastly, with a valuation that remains appealing, I maintain a 'Buy' rating on AVB.

For further details see:

AvalonBay Communities: Better Way To Own Real Estate