AVACF - Avance Gas: Offering A 14% Yield Thanks To Strong VLGC Charter Rates

2023-12-06 10:30:00 ET

Summary

- Avance Gas reported a strong quarter with high charter rates and increased cash flow.

- The company's net income for the first nine months of the year was $102.1M, resulting in an EPS of $1.33.

- Avance Gas expects even better performance in the final quarter with higher spot rates and time charter coverage.

Introduction

I have been bullish on Avance Gas ( AVACF ) for as long as I can remember. Back in October 2022, I argued the 13% yield was very appealing but the company’s performance continued to improve on the back of higher charter rates which lasted for much longer than I had anticipated. Since that article, which was published less than six months ago , the share price increased by in excess of 60% (in US Dollar), so it is definitely time to have another look at this VLGC operator.

A strong quarter for Avance Gas - but the best is yet to come

The charter rates remained very strong for Avance Gas during the third quarter, and the company reported a total time charter equivalent rate of $55,300 per day based on a discharge-to-discharge basis. The average TCE rate was most definitely boosted by the contribution from spot voyages which were priced at in excess of $75,000/day and accounted for 64% of the available days. The remaining 36% of the days were fixed based on time charter coverage at an average charter price of just under $42,000 per day.

With a total operating expense of just over $8,000/day, Q3 2023 was once again an excellent quarter for Avance Gas which just continued to print cash.

That’s obviously clearly visible in the company’s quarterly financial results. Avance Gas reported a total revenue of $79.5M and this resulted in a total operating profit of $46.1M, which is approximately 66% higher than in the same quarter last year. And as the depreciation expenses remain relatively stable (there haven’t been any substantial changes in the fleet profile), the reported operating profit was $35.2M, which is more than twice the operating profit generated in the same quarter last year.

{kind=link}

Of course, Avance Gas doesn’t really escape the increasing interest rates, and while its existing hedges cover the majority of the risk (the hedging ratio is approximately 90%), there still is a small increase in the net finance expenses.

That’s really nothing to be too concerned about, and the company reported a total net income of $30.1M or $0.39 per share. This also means the net income generated in the first nine months of the year was approximately $102.1M for an EPS of $1.33. A very strong result, indeed.

Avance Gas announced a dividend of $0.50 per share which would indeed mean the dividend is not covered by the reported net income but Avance Gas also has a forward-looking view when it decides on its dividend. As you can see below, the strong cash position and robust expectations for the final quarter of this year are the main factors why Avance’s board approved a quarterly dividend of $0.50/share.

{kind=link}

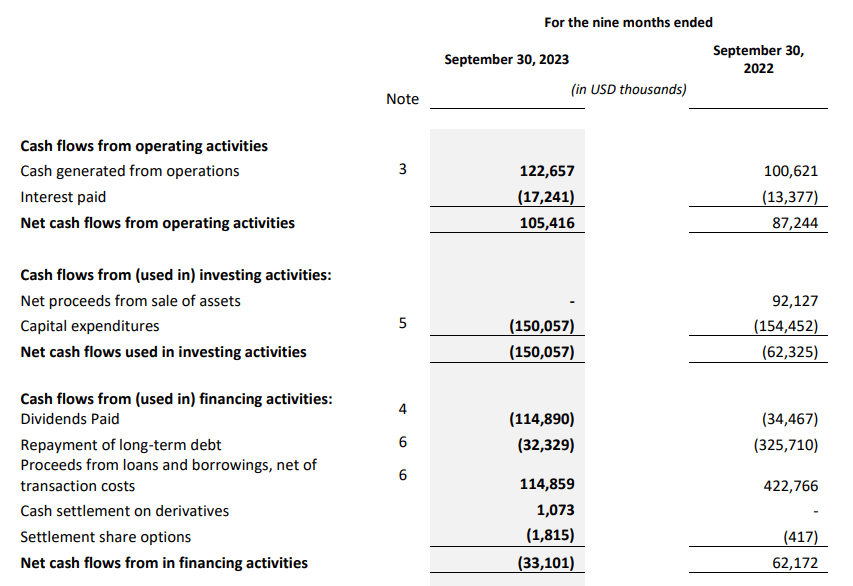

And while the company is spending quite a bit of cash on new vessels, the balance sheet remains in good shape. As you can see below, Avance Gas generated a total operating cash flow of $105.4M in the first nine months of the year, but this includes a total net working capital investment of approximately $32.5M which means the underlying operating cash flow was actually $138M.

{kind=link}

Thee total capex bill of around $150M mainly consists of the newbuild program and Avance Gas took delivery of two new VLGC vessels in the first half of the year. But the company’s expansion plans aren’t completed yet as back in June, it announced a new contract with a Chinese shipyard to build two mid-sized LPG/ammonia gas carriers and exercised an option to get an additional two vessels built. As Avance Gas obviously wants to protect its excellent financial position, it also sold a 15 year old VLGC vessel, the Iris Glory. This vessel will be delivered to its new owners in January 2024 and is currently classified as an ‘asset held for sale’ on the balance sheet with a book value of $38M. This means the company will generate a gain of $22M on this sale, as it sales agreement stipulates a sales price of $60M for the vessel.

At the end of the third quarter, Avance Gas had about $146M in cash while it had a total debt position of approximately $535M for a net debt level of approximately $389M. And including the Iris Glory sales proceeds, the net debt will decrease to $329M. Considering the total book value of the vessels plus the value of the newbuilds is approximately $880M, the debt ratio (in this case net debt versus vessel value) is just 37%. And that makes it perfectly reasonable for Avance Gas to spend the majority of its incoming cash flows on dividends.

{kind=link}

And considering Avance Gas has already arranged all required funding for the newbuild program, I am not expecting any balance sheet related issues.

{kind=link}

Investment thesis

While the third quarter was already pretty good, the company expects the final quarter of the year to be even better. Avance Gas expects spot rates to average $90-100,000/day while the time charter coverage will average around $50,000/day. This means Avance Gas will likely realize an average daily charter rate of $70,000-75,000/day and that is almost 40% higher than its average realized charter rate in the third quarter of this year.

That definitely helps to explain why the company’s board is so keen to keep the quarterly dividend unchanged at $0.50 per share, although the reported EPS was quite a bit lower.

I currently have no position in Avance Gas, and it looks like I sold my position too soon. Based on the current performance of the company, it would still be a ‘buy’, but I am not chasing the stock here and am patiently waiting for another opportunity to initiate a long position.

For further details see:

Avance Gas: Offering A 14% Yield Thanks To Strong VLGC Charter Rates