AVNS - Avanos Medical: Cost Restructuring Could Unlock Substantial Value

2023-04-21 05:16:06 ET

Summary

- Avanos has embarked on a cost restructuring to drive EBIT margin and grow free cash flow into FY'25.

- This could unlock tremendous value for shareholders in my informed opinion.

- Here I run through the salient points forming my refined investment thesis.

- Net-net, rate buy at a fair valuation of 48x forward earnings.

Investment Summary

The equity of Avanos Medical, Inc. ( AVNS ) remains a buy in my informed opinion and in this report I'm discuss the factors informing my guidance.

After a sustained growth period from FY'18-'22 the firm is now leaning up its cost structure and looks for $55mm in gross cost savings by FY'25 with $10mm set to come this year. As a result of the cost restructuring, AVNS will likely see a 4-5% decline in turnover in FY'23 and print ~$780-$800mm in top-line revenues by estimation. Despite this, the firm could still generate ~$38mm in adj. earnings this year and be a $100mm FCF company by FY'25 in my estimation, meaning I can increase my med-tech exposure via AVNS on a 54x fair forward P/E (my numbers) and pay 23x at the time of writing, collecting a delicious 104% premium in valuation upside if my thesis is vindicated. Wall Street also loves a good cost reduction exercise, and will likely reward AVNS if gains are realized below the operating line this year, in my firm estimation.

Net-net, I am reaffirming AVNS as a buy.

Stranded costs to be carved out

AVNS made no excuses when it revealed the planned cost restructuring over the coming 3-years. It hopes to achieve $55mm in annualized savings by then. These efforts are certainly warranted, in my opinion.

The main benefits will be seen below the operating line and could see the firm generate ~$160 in adj. NOPAT by FY'25 [h ere, I've adjusted OpEx for R&D investment, capitalising it as an intangible investment with a 7-year straight line amortization]. Hence, there is a major tilt in the risk/reward calculus if AVNS' pull through. The question is, how could it materialise.

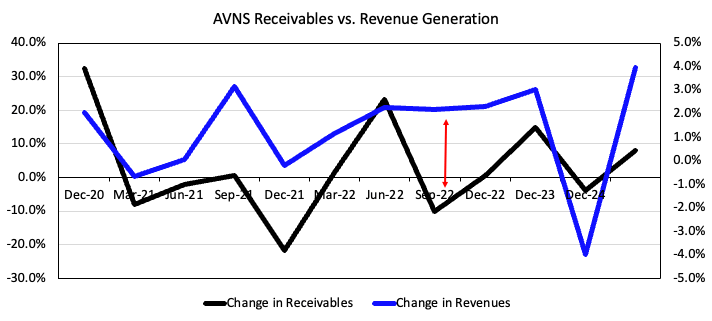

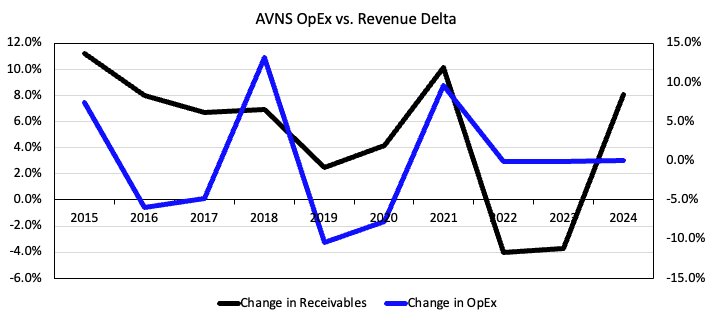

One, the previous cost structure was unsustainable to growing profits. Over a rolling T12M period from Q4 FY'20, the change in receivables outpaced revenue growth [Figure 1] for the most part, reducing putting a strain on cash conversion - particularly in FY'22. At the same time, operating expenditures had stretched well up off FY'19 lows and the change was becoming unreasonable. A big factor in the OpEx makeup were stranded costs AVNS couldn't reclaim, so it was forced to be more focal on more mission-critical capital allocation to drive up profitability. Consequently, management have made the right choice in addressing this in my opinion.

Fig. 1

Note: Rolling last 12-month ("TTM") periods are shown each quarter from Q4 FY'20. The chart plots percentage change of Total Receivables versus the percentage change in revenues each quarterly period on the T12M basis. (Data: Author, AVNS 10-K's)

{kind=link}

Fig. 2

Note: Annual periods are shown. (Data: Author, AVNS 10-K's)

{kind=link}

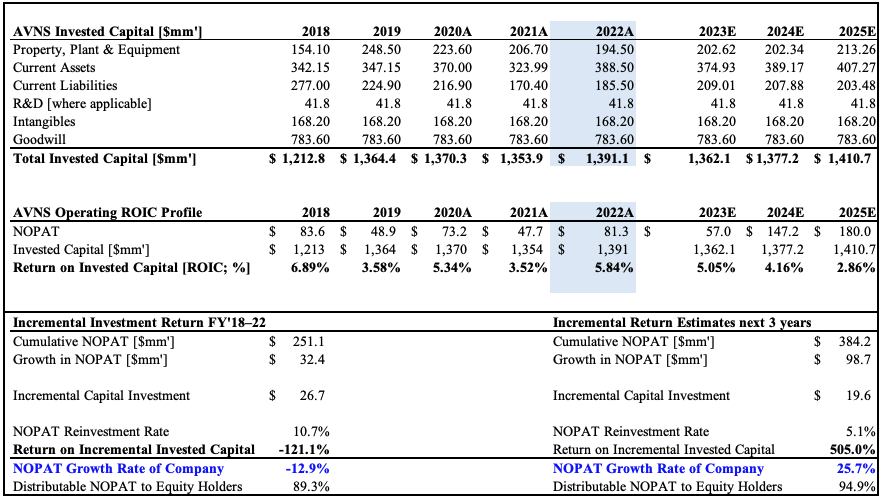

Two, AVNS' ability to harness capital productivity and profitability at the (adjusted) NOPAT level has been commendable. Since FY'18, capital intensity has narrowed substantially, such that invested capital turnover now rests at 1x versus 0.7x back then [Figure 3]. My numbers have this trend to continue and with the planned reduction in capital density and OpEx, to see capital turnover hit 1.2x this year and 1.5x by FY'25. This is very attractive in the era of tight money, high inflation, macro-volatility, etc. Less capital intensity means less reinvestment required to grow, and higher ROIC, meaning more cash can be pulled by shareholders at the end of the year.

Fig. 3

Data: Author, AVNS 10-K's

Three, any ratchet up in capital productivity could have tremendous pull-through to profitability by estimation. My numbers show that AVNS could generate $180mm in NOPAT by FY'24, on a $1.4Bn capital base (including capitalized R&D). That's $98mm growth in NOPAT on $19mm additional capital investment, which throws off a 500% return on incremental capital over this time [Figure 4]. For investors, the benefits are:

- These kind of returns on capital are what's required to grow owner earnings/cash flows substantially without jeopardizing growth.

- AVNS can grow without hurting owner free cash flows. It won't need to reinvest large sums of capital from owner earnings, meaning it can throw off that cash to shareholders.

- The mathematics suggest AVNS' could compound its operating growth at 25% with these kind of incremental returns.

My numbers suggest that of the $384mm I estimate AVNS to generate, ~95% of this could be distributed to shareholders as residual cash flows. In terms of business economics, these are the kind of numbers I search for. Second to that, this is a major contrast to the previous 5-years to date, where capital intensity was reducing, but profits weren't expanding.

Fig. 4

Note: Net Operating Profit After Tax is from adjusted operating profit, where GAAP operating income has been reconciled to remove R&D investment as an operating expense. Instead, it is capitalized on the balance sheet as an intangible asset, with a 7-year amortization over a straight-line. The amortization expense is then recorded on the income statement under adjusted operating expenditures. (Data: Author, AVNS 10-K's)

{kind=link}

Four, on the prospect of economic profitability, the cost-savings could also lead to tremendous value creation for shareholders. Taking WACC values for the firm over the past 5-years to FY'22, it was clear there's been a negative spread between AVNS' returns on incremental capital and the cost of capital, meaning the firm's growth initiatives haven't created shareholder value. In fact, it has been destructive to value, as seen on the price chart - shares are down >35% in the past 5-years.

However, investors are beginning to see the light ahead, because the stock has caught a strong bid in 6-months to re-rate 46% higher at the time of writing. My information suggests that short interest has dropped to just 2%, call option demand for April expiry at the $30 strike point has soared and AVNS is now back at a January FY'22 market cap once again. This tells me the firm's cost exercise is likely to generate economic profits for shareholders above the cost of capital, corroborated by the market's trading of the name. This requires AVNS' capital (including human capital) productivity is sufficient to ensure cash is distributable t shareholders without jeopardizing growth. Any growth therefore would create further value for shareholders. I'd be looking to the next 12 months as key to setting up the coming 3-5 year period for AVNS.

Fig. 5

Note: Economic profit is measured as the annualized average quarterly WACC for AVNS from FY'18. The spread of ROIC over(under) this figure is the economic profit(loss). The Economic Profitability of a firm is a non-negotiable characteristic to ascertain if its growth is accretive to value. If the firm produces an economic loss, value creation is agnostic to growth. If it is an economic profit, capital productivity ensured that cash is distributable to shareholders without jeopardising growth, and vice-versa. (Data: Author, AVNS 10-K's)

Valuation and conclusion

AVNS is an absolute peach at 1x book value in my opinion, and makes the 3% ROE I've forecast for FY'23 more palatable. Even the market has AVNS priced at 0.04x PEG suggesting the earnings growth is set to pull through from the cost profile of AVNS this year. The question is, what does this mean for value to shareholders.

My conclusions on the valuation debate include the following:

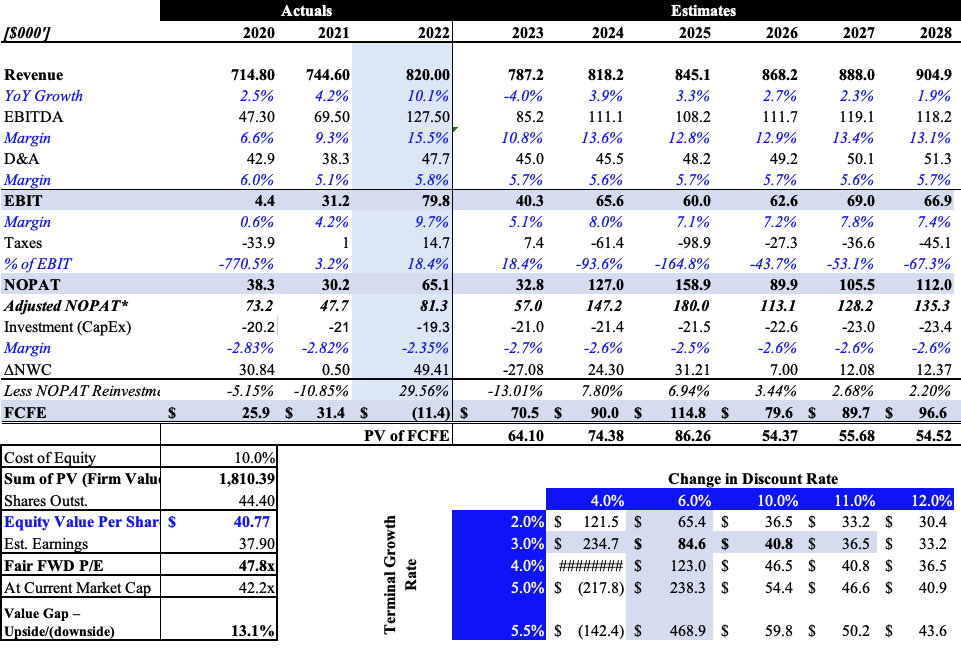

- If all goes according to plan, AVNS could be generating $100mm in FCF by FY'25. Reinvestment rates would therefore be lower, throwing off higher piles of cash to shareholders.

- Discounting the projected stream of cash to shareholders (shown as "FCFE" in Figure 6) at 10% (opportunity cost of equity) into FY'28 to reduce forecasting risk, AVNS could be valued at $1.8Bn in market cap.

- For my FY'23 adjusted earnings estimates, this derives a 48x forward P/E, well above the market's 23x forward P/E.

- This represents >100% upside potential in multiple upside if vindicated.

- Further, I'd look for AVNS to reprice to $40, if its opportunity cost of equity was to revert to ~6%, $84 is a reasonable target.

Subsequently there is tremendously attractive value on show here that would be accretive to share price in my best estimation. This certainly supports a bullish thesis.

Fig. 6

{kind=link}

Using a valuation concept by Alfred Rappaport, cited in Mauboussin (2022), called shareholder value added ("SVA"), I've estimated the operating profits AVNS could capture above its funding costs/costs of capital, using my growth assumptions.

Fig. 7

Data: Author Estimates

These could be valuable if the ROIC is above the market's rate of return. I'll wait a little longer before confidently prescribing these kind of upside targets, however, it is very insightful to know

In summary, it's best to think in first principles. In doing so, the AVNS investment debate can be best surmised in the following way:

- AVNS is embarking on a significant cost-restructuring regime to recapture stranded costs, reduce capital intensity and lean up the OpEx requirement.

- This could pull through to the operating line with higher capital productivity, greater returns on incremental capital, meaning the firm can compound owner earnings without jeopardizing growth.

- With a higher cost of capital, the growth in profits could be beneficial in generating economic profits for shareholders.

- Meaning it can throw off more cash to shareholders, resulting in valuation upside.

- With these points, I consider AVNS to be fairly valued at 48x forward earnings, and am happy to pay 23x as its marked today.

Net-net, I reaffirm that AVNS is a buy.

For further details see:

Avanos Medical: Cost Restructuring Could Unlock Substantial Value