AVTR - Avantor: Customers Destocking Order Volumes Down Challenges To Rating (Rating Downgrade)

2023-09-07 23:35:24 ET

Summary

- Avantor, Inc. faces significant challenges to growth, with reduced orders and sales slowdowns in semiconductor-related sales.

- The company's Q2 numbers reveal a decline in revenue and earnings, with multiple headwinds including inventory destocking and constrained end-markets.

- Negative sentiment is reflected in reductions to AVTR's revenue and earnings estimates, as well as the stock trading below key levels.

- Net-net, revise to hold.

Investment updates

Since the April publication on Avantor, Inc. (AVTR) there have been multiple updates to the investment debate that need discussion. Chiefly, its Q2 numbers reveal significant challenges to growth in its end markets. This is not unique to AVTR - many healthcare and materials providers are witnessing order volumes pare right back as customers destock inventories brought online during the 2022 supply chain fiasco. The net effect is that many of AVTR's customers have reduced orders in vast numbers. Semiconductor-related sales were down 80% YoY, for example.

This report will unpack some of the challenges AVTR faces moving forward and illustrate why I've pared back the rating to a hold. Net-net, revise to hold, looking at ~$20 as the trading range going forward.

Figure 1.

{kind=link}

Critical changes to investment thesis - Sales slowdowns, sentiment changes

1. Q2 FY'23 insights + guidance

AVTR put up its Q2 numbers in late July. Critical info is gleaned from the takeouts. It clipped Q2 sales of $1.74Bn , down 6.5% in its core business, on adj. EBITDA of $343mm. Multiple headwinds were observed during the quarter - slowdown in core markets, constrained spending (due to the rates/inflation axis), and continued inventory destocking from its major customers, particularly in its biopharma and advanced technologies ("AT") and applied materials ("AM") markets.

This isn't an issue AVTR is facing alone, nor is it unique to healthcare/biopharma et al. Many industries overstocked inventories during the supply-chain fiasco exhibited last year. Fast forward to FY'23, and we've got a situation with 1) overstocked end markets, 2) delinquent inventories, 3) reduced order volumes and demand-pull as a result. Most corporates believe the issues will resolve by FY'24, but the impact to respective equities cannot be ignored in my view.

Given the setbacks this YTD management revised its yearend forecasts and expects a decline of 7-9% in revenue, calling for $6.89Bn-$7.04Bn at the top. It is eyeing FCF of $600mm-$675mm on this.

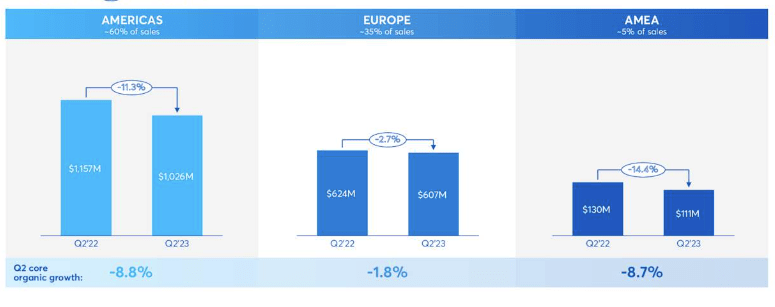

As to the regional highlights, observed in Figure 2:

- Its Americas market was down 8.8% YoY, again due to weaker customer demand in biopharma and AT and AM mentioned earlier. In particular, the biopharma business was severely impacted by sequential declines in both research and bioproduction. But the biggest flag for mine was that semiconductor-related sales plummeted by >80% YoY due to these inventory destocking trends. I must say I've seen this trend in anything related to semis in Q2/Q3 this year and there could be a continuation given the rapid advancements in these products. I'm not sure, but the fact is these factors led to a ~220bps headwind for AVTR's top line in Q2.

- Its EMEA business slipped 8.7% to the downside due to a drop of ~70% in formulated solutions for its semiconductor customers. The fact overall demand in research settings across all end markets was sluggish didn't help either.

- Europe was also down ~180bps for similar reasons. Management said "the recession in Germany also put pressure on equipment and instrument sales", but in reality, it was the same thematic in Europe as well (destocking, reduced order volume, cost containment, etc.).

Figure 2.

Source: AVTR Q2 Investor Presentation

{kind=link}

Moving down the P&L, gross margins compressed by ~80bps YoY to 33.8%, a result of the lower overall volumes and adverse mix effects from its bioprocessing and semiconductor headwinds. Also - and I hate to say it - the conclusion of its margin-rich COVID-19 revenues played an impact here. But AVTR can't continue using this as a reason behind sluggish margins going forward. We are nearing the end of 2023, and (fingers crossed) the pandemic is well behind us. I will no longer be accepting this kind of reasoning behind any sluggish performance going forward, and haven't been for the most of '23.

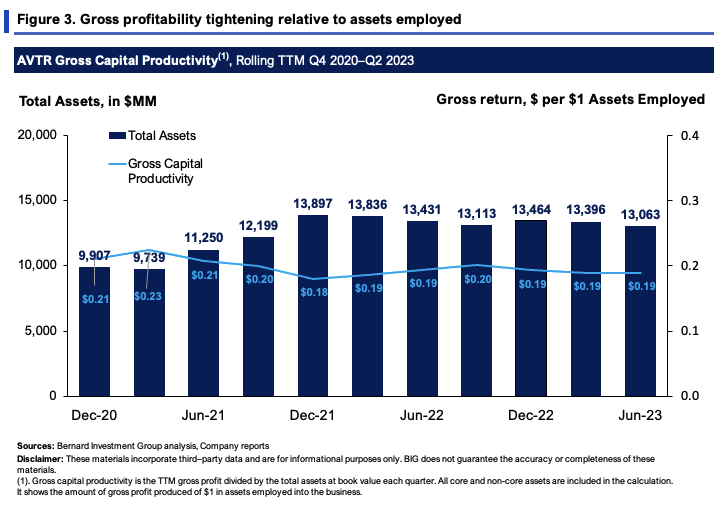

Moreover you'd expect the growth in assets employed to be recycling back more in gross as time rolls on. But this isn't the case. Figure 3 shows the gross capital productivity of the firm from 2020-date on a rolling TTM basis. Instead, numbers are down from $0.21 in gross per $1 in assets employed, to $0.19 last quarter.

Hence - a more asset-heavy business, but less income to show for it.

{kind=link}

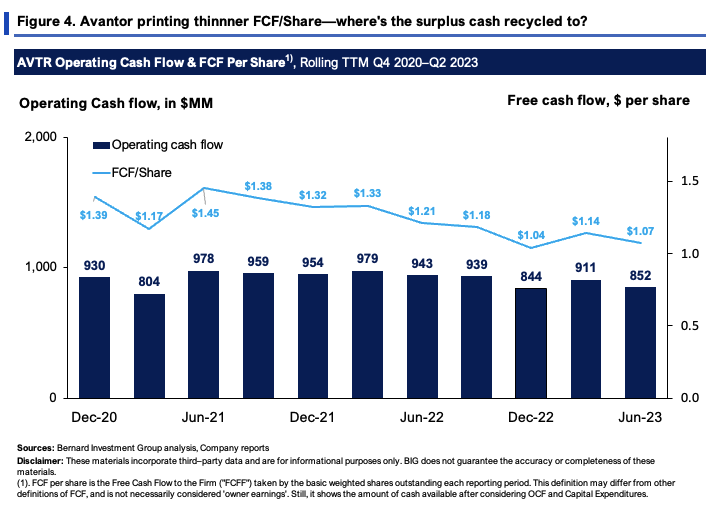

Finally, AVTR clipped $138.1mm in quarterly FCF during the quarter, converting 85% from the bottom line. This came from working capital changes - which are the link between earnings and cash flows. But the FCF numbers aren't incrementally adding value here. Figure 4 shows AVTR's operating cash flows an FCF/share on a rolling TTM basis since 2020. It has produced a series of sequential declines in FCF/share since 2021. Whereas OCFs are down ~$100mm off highs.

I'm not so concerned about the OCF numbers, but I would have expected to AVTR to have recycled the capital into more profitable business lines or to see it reinvesting surplus cash back into the business. Acquisitions made across the last 2 years have yet to accrete earnings or FCF's, and this has me questioning their benefit at the moment. The downsides in its equity stock may very well reflect this sentiment as well. Not to mention, it ended the quarter at 3.9x debt/adj. EBITDA, and had to increase its revolver capacity 515mm to $975mm during the quarter (for a FY'28 maturity).

{kind=link}

2. Changes in sentiment

One can't look past the negative sentiment in AVTR's equity stock. Sentiment is one of the 3 or 4 critical factors needed to drive a company's market value higher. We see the negative sentiment in two ways.

One, there's been no less than seventeen - yes, 17, one-seven - reductions to AVTR's revenue and earnings estimates from Wall Street analysts in the last 3 months. Not one source has raised their targets going forward. What's more, the declines extend out to 2027. Like it or not, The Street's estimates are used by swaths of investors in decision-making, in part at the very least. So the windback in estimates represents the sentiment of a large substrata of the market populous. This certainly supports a neutral posture in my opinion.

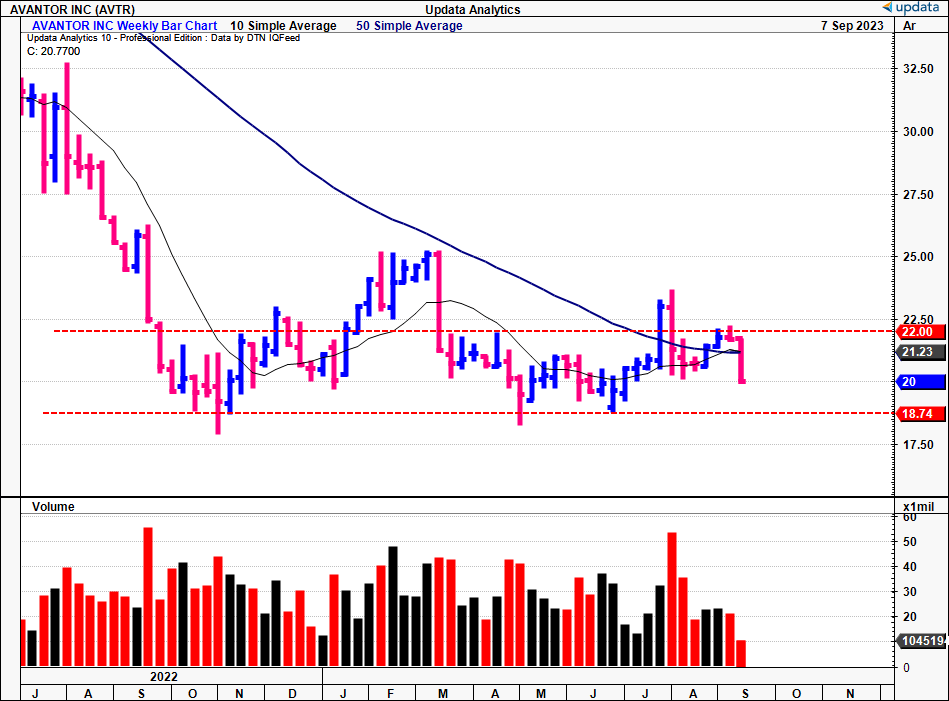

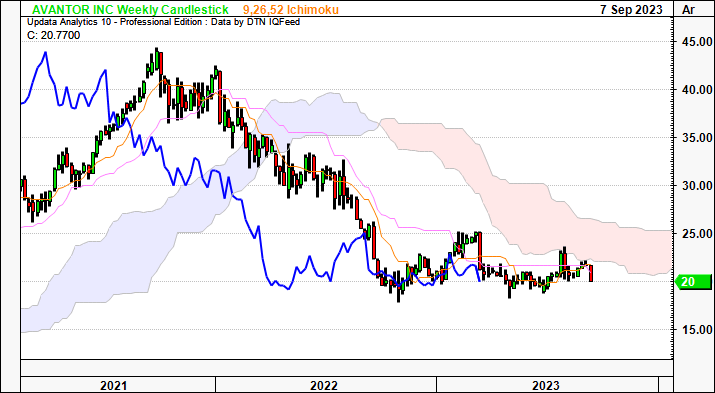

Two, market generated data indicates a lack of bullish positioning as well. The stock is trading below key levels, as shown in the cloud chart on Figure 5. Both price and lagging lines are below the cloud, having pushed into congestion for the bulk of '23. You'd need a break above the cloud, around the $25.00/share market to call a bullish reversal here. The point and figure studies in Figure 6 support this view. The latest target thrown off by the P&F study is to $18.25, thrown off in July. These charts show objective moves in trend, and are fantastic in sideways markets to get a directional view. These are both neutral points in my view.

Figure 5.

{kind=link}

Figure 6.

Data: Updata

Valuation and conclusion

Despite its economic woes, AVTR still sells at 19.6x forward earnings (33x GAAP EPS) and 16x forward EBIT. The company has only created $2.60 in market value for every $1 in net asset value. You're getting a 5.5% forward cash flow yield on this, when cash is paying 4-5% starting yields as I write. This tells me two things:

- Slack earnings growth on high market prices (19.6x forward is ~1.5% premium to the sector, and the forward PEG ratio on this is >2x).

- The market values its net assets at a small premium (~2.5x).

At a $19.85Bn EV as I write (adding in $5.88Bn of debt to the $14.2Bn market cap), I find it difficult to see AVTR trading into a higher multiple than 19x whilst offering just 5.5% yield on cash flow. At 19x forward, using consensus earnings estimates of $1.07/share, this gets you to $20.90/share as a forward target, in-line with the current market value. This supports a neutral view. Notably, these posture is supported by findings from the quant system, that uses an objective composite to aggregate key factors into a rating. These ratings are excellent in obtaining an objective viewpoint.

Figure 7.

{kind=link}

In short, there are multiple challenges AVTR has to contend with leading into the back end of FY'23. The major slowdown in its core markets is being felt throughout the P&L and balance sheet, despite reasonably strong FCF conversion. The problem in my view is, none of these cash flows are accretive to shareholder value. Or they haven't been in FY'23 either. With further downsides forecast for FY'23 and FY'24, I am reducing my rating on AVTR to hold in search of more selective opportunities. Revise to hold.

For further details see:

Avantor: Customers Destocking, Order Volumes Down, Challenges To Rating (Rating Downgrade)