AVTR - Avantor: Leaner Cost Capital Structure Ready To Throw Off Cash Earnings

2023-04-13 07:58:05 ET

Summary

- Avantor has attractive economics that sees it throw off large amounts of cash to drive valuation upside.

- The firm is projected to create value in the next 3-years with a leaner cost and capital structure.

- Valuations are attractive and shares trade at a substantial discount to my 27x forward P/E number.

- Net-net, reiterate AVTR as a buy.

Investment Summary

After a choppy YTD on the chart I still see long-term value in Avantor, Inc. ( AVTR ) equity. The stock trades at a deliciously cheap 15x forward consensus earnings [non-GAAP], and 2.8x book value, and my projected 19.7% FY'23 return on equity makes this is worthwhile.

The company has also simplified its capital structure. It restructured ~$6Bn of its long-term debt and hedged interest volatility with swaps that denominate interest payments into euro-specific rates. Further, none of the firm's customers generate >5% of top-line revenues and this, combined with its deep customer networks, mean its top-line is hedged from the reduction in Covid-19 revenues and macroeconomic sands that are shifting beneath our feet this very moment. I've talked about this as a central point in my investment thesis over the last 6 publications on AVTR, dating back to 2020.

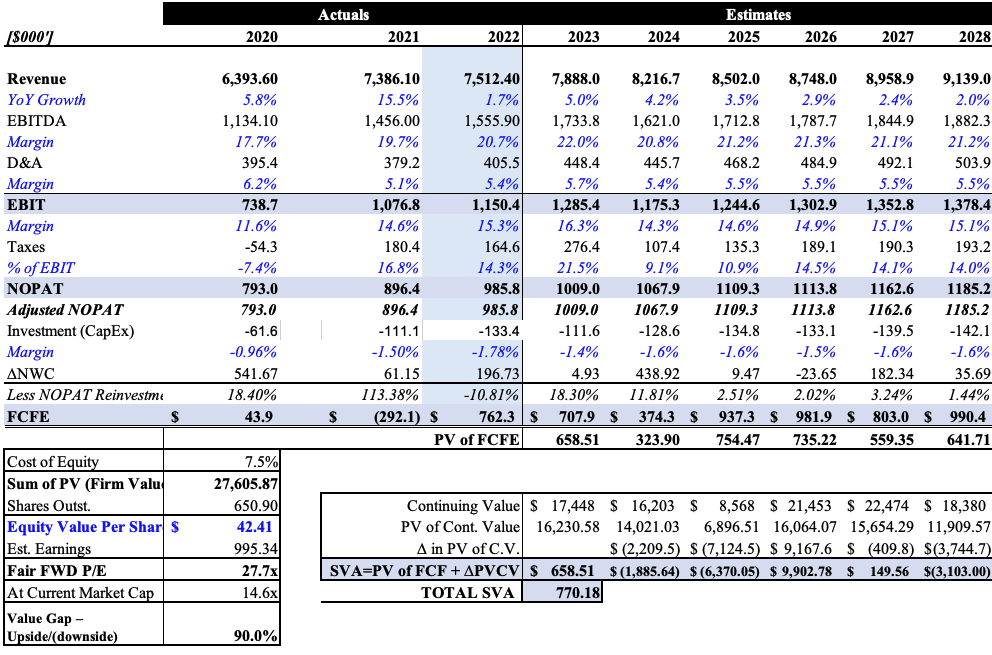

Collectively, AVTR is a long-term cash compounder, and I am aligned with management's FCF forecast of $700mm and call for $995mm in post-tax earnings in FY'23, calling for $1.53 in core EPS. After an estimated $184mm reinvestment for new growth capital, I project the firm generate ~$708mm in free cash distributable for shareholders this year, a 71% conversion rate from reported earnings. Looking out to FY'28, my estimates point to strong earnings power from AVTR, creating value for shareholders over this time.

Net-net, based on these growth assumptions, AVTR looks fairly valued at ~27x forward earnings or $30-$42 per share based on a 7.5%-9.5% discount rate. This is an attractive value proposition, and I am therefore still very constructive on this name for the long-term. Here I present the bullish case underpinning my thesis.

Fig. 1

Note: Earnings Power is the conversion of owner earnings from reported net income. Owner earnings is the net operating profit after tax less investments for CapEx, changes in net working capital, and investments to additional growth capital. In other words, the profit left over after reinvesting capital to maintain existing operations, and grow. (Data: Author)

Fig. 2 AVTR price performance

{kind=link}

Key Facts Underpinning Thesis

Here's the key points for consideration in the AVTR investment debate.

As a reminder, AVTR generates ~85% of turnover as recurring revenues, and revenue streams are well diversified, with no customer making up >5% of sales. In addition, the deep customer network is a major value-add as ~40% of sales come from customers of ?15 years. Further, with respect to the company's four product segments:

- Materials and consumables

- Equipment and instrumentation

- Services and specialty procurement

- Proprietary materials and consumables

Each segment has high barriers to entry and high switching costs, adding to the competitive advantage. Additional evidence is that 52% of customers are bio-pharma related. The product contribution to top-line revenues in FY'22 is observed in Figure 3.

Fig. 3

Data: AVTR 10-K

In FY'22, thin YoY sales growth of 1.7% pulled in $7.5Bn in revenues and pulled to $2.6Bn in gross profit on a core EBITDA margin of 21%. OpEx has been well contained at ~19% of sales, leading to 680bps YoY growth in operating income on a 15% operating margin. AVTR generated $686mm in earnings and this pulled through to $760mm in shareholder earnings after factoring in all investments towards growth capital. This equates to 111% conversion from reported earnings, hence a major benefit for equity holders.

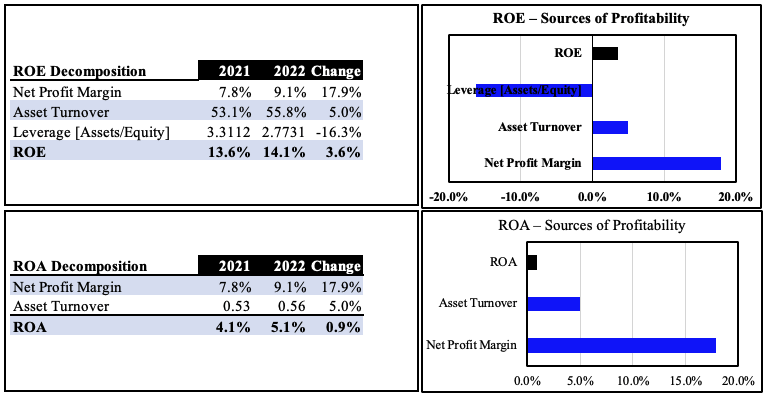

Despite a small $129mm gain in revenue, combined with the 1.3% percentage point gain in net margin, the latter was a major benefactor to generate 14% ROE in FY'22, especially pleasing given the 16% deleveraging from the year prior [Figure 4]. This suggests equity holders profited from growth in core operations rather than from leverage.

Fig. 4

{kind=link}

Equally as important is the contribution from its two most recent acquisitions:

- MasterFlex, made in November FY'21 on a $2.87Bn cash acquisition

- Ritter GmbH, completed in June FY'21 on a $1.08Bn valuation

MF clipped revenues of $227mm last year, or 3% of total sales. Ritter came in at 2% of sales with $151mm, leading to operating income of $23mm for the year [Figure 5]. As such, the return on investment for MF and Ritter last year was 1.21% and 2.13%, respectively, well below the cost of capital. It needs to do better on this front. Can't blame AVTR though - it generated a 45% incremental return on invested capital ("ROIC") in FY'20, so it was keen to deploy capital and deepen its network.

As such, these two strategic growth investments haven't begun to bear fruit just yet. The market has punished AVTR these past 12-18 months, and I believe this could be one major reason why. All in all, ~$4Bn in cash was spent on acquisitions in FY'21, capital that could certainly have gone to shareholders as buybacks or even a special dividend - this would have been $6.70 per share at 590mm shares outstanding, $6.14 if paid last year.

Moreover, the outlook for Ritter is mixed given "...reduced customer demand for medical fluid handling tips due to a decrease in COVID-19 testing" , per the 10-K. If it can't replace these revenues, it "...may be required to impair Ritter's long-lived assets". So market may have been sellers of AVTR for these reasons.

Fig. 5

{kind=link}

I'd also like to point out that Covid-19 related sales are diminishing rapidly, such that AVTR won't even be booking them as a segment this year. Looking at its latest numbers, widespread declined in Covid-related revenues are touted as the cause. Management have and will continue de-stocking relevant inventories and this already occurred last year within its merchandise inventory purchases [Figure 6]. Still, inventories increased in FY'22 but I'd be expecting a pullback given management's intentions this year.

Consider this as well - despite the fact Covid-19 revenues produced widespread YoY revenue declines across the majority of segments, this also had an adjacent benefit to gross margin from the more profitable product mix. Gross margin lifted 70bps YoY to 34.6% and my numbers look to 36.2% revenue as revenue mix shifts toward more profitable segments.

Fig. 6

Data: Author, AVTR 10-K

Growth contribution a standout

Getting down to the nuts and bolts of AVTR's valuation drivers is where the value can be extracted in my estimation. AVTR is a company where capital mostly produces its profits. It has more than 200 global facilities that cover manufacturing, distribution, service, research & technology and sales. It will therefore need ongoing capital investment to maintain existing operations, and continue its growth route.

In that vein, it is important to note the following points on the economic profitability and returns on capital for AVTR:

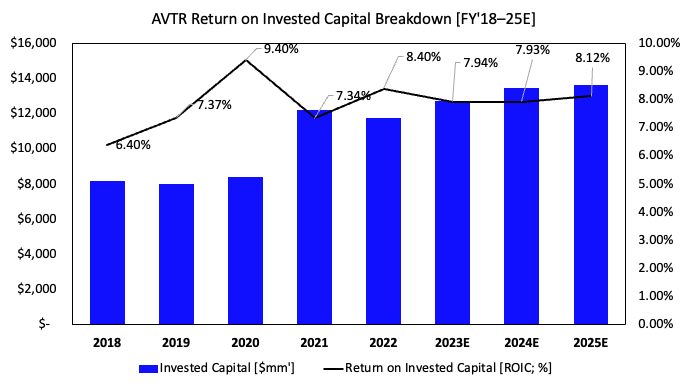

- The company has continuously generated 7-8% ROIC since FY'20. Excluding goodwill in the calculation, it's produced a tidy 14-16% ROIC. Looking ahead, my numbers call for a similar range [Figure. 7]

- Capital intensity has increased substantially since FY'20. However, last 2-years AVTR has grown with CapEx at just 1%-1.8% of revenues, and it required another $196.7mm in NWC last year to generate an additional $89mm in NOPAT.

- On the point of economic profits, the firm didn't generate a return that outpaced the cost of capital last year. ROIC was 8.4% on a 9% WACC hurdle, an effect caused by an increasing cost of capital. This is a problem, as it hurts shareholder value, and matches the market value of its stock price over that time.

- Two things on this, however. One, AVTR has restructured its credit profile and has locked in fixed euro rates to hedge rates volatility, as mentioned. This has reduced its cost of capital. Two, looking ahead, my numbers indicate that it may revert back to delivering economic profit to shareholders [Figure 8].

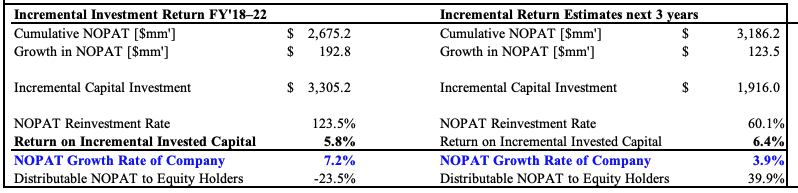

- Incrementally, it is projected to invest another $1.9Bn [60% of projected NOPAT] to generate an additional $123mm in NOPAT, a 6.8% incremental ROIC [see: Appendix 1]. Whereas growth came at a net cost loss to shareholders in FY'22, my numbers see AVTR throwing off high amounts of free cash flows and driving earnings to its shareholders over the coming 3-years. The deviation from Covid-related sales no doubt plays a factor here also.

These points are important for a number of reasons, but it's the growth in earnings to shareholders that is most critical. Its capital produces earnings and so therefore requires investment to maintain and grow. So the earnings we receive as shareholders are the reported post-tax earnings less the capital it needs to reinvest in order to grow. My outlook looks to AVTR clipping CapEx beneath $150mm per year into FY'26 and see's NWC capital requirements trending down as well. This will be beneficial to the capital charge it incurs and the cash flow through as earnings to shareholders.

As such, a higher rate of return above the cost of capital, on a more efficient capital base are two major bullish factors in my estimation.

Fig. 7

{kind=link}

Fig. 8

Data: Author, AVTR 10-K

Valuation

I'm calling for AVTR to grow revenues 5% YoY to $7.8Bn this year and generating $1Bn in NOPAT $995mm in earnings. I'd be looking for an additional c.$116mm in capital and NWC requirements to hit this mark, and for AVTR to reinvest 18% of its earnings into growth expenditures for FY'24.

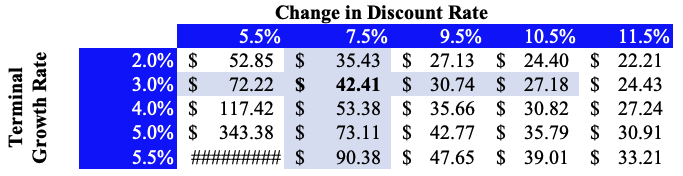

These assumptions call for $708mm in free cash to equity holders (owner earnings) after factoring in the reinvestment rate, 71% of the projected reported earnings. Looking to FY'28, my numbers have strong YoY growth in free cash to shareholders and discounting these at the 7.5% WACC hurdle derives a valuation of $27Bn in market cap and $42 per share, otherwise 27x forward earnings. At my estimates, the market values AVTR at 14.6x, ~90% value gap to the estimate of fair value. Pricing in more risk with a 9.5% discount rate gives a $30 valuation, seen in Figure 10.

Fig. 9

{kind=link}

Fig. 10

{kind=link}

In summary

The culmination of these points creates a bullish tilt to the risk/reward calculus for AVTR:

- Robust revenue model that is drifting from Covid-19 revenues toward more profitable business segments.

- No customer >5% of sales, meaning top-line is hedged from economic downturn. Plus, 85% of turnover from recurring revenues.

- Capital intensity well contained, projected to generate ROIC above cost of capital with economic profit in FY'23-'25.

- Hence AVTR has and will likely continue throwing off large amounts of cash creating a springboard for valuation upside looking ahead.

Together, these points answer the fundamental investment questions and demonstrate strong economics into the coming periods, by my estimation. My numbers value the stock at 27x forward earnings, a significant premium to the 15-16x assigned by Wall Street and the market. Cost blowouts that erode margins would be the key risk to this thesis in my opinion, and will be watched intently throughout FY'23. Net-net, I reiterate AVTR is a buy at a $30-$42 valuation.

Appendix 1: AVTR Incremental ROIC estimates

{kind=link}

For further details see:

Avantor: Leaner Cost, Capital Structure, Ready To Throw Off Cash Earnings