RGEN - Avantor: Promising Long-Term Buy With Potential For Opportunistic Entry

2023-06-28 16:10:16 ET

Summary

- With growth prospects, ongoing deleveraging and margin expansion efforts, acquisition value realization and 85% recurring revenue mix, Avantor is well positioned to take advantage of the secular life science uptrend.

- Avantor faces near-term challenges amid macro headwinds, revenue growth uncertainties due to continuing COVID roll-off, customer inventory destocking and investment decline in the sector.

- Order intake to sales ratio and customers’ inventory to sales ratios can be used as leading indicators for determining inflection point on near-term headwinds like COVID roll-off and inventory destocking.

Introduction

Since its IPO in May 2019, Avantor ( AVTR ) stock has experienced a rise and fall fueled primarily by the pandemic driven factors, although the company may not be considered among the speculative names. This can be attributed to the fact that the company generates over 60% of its revenue from biopharma and healthcare customers. Although the companies that serve these customer groups generally show robustness to cyclical downturns, investors may wonder what to expect from the Avantor stock for the rest of the year and its longer-term prospect.

With reputed and established brands including J. T. Baker, NuSil, VWR and Masterflex, Avantor plays a critical role in life sciences supply-chain. The company has >200 facilities globally and since 2019, it has increased its global manufacturing locations from 28 to 35 and innovations centers from 11 to 13.

With 4,000 suppliers, sticky and diversified customer base, global and growing presence, a successful e-commerce platform and ~85% recurring revenue mix, Avantor has built its business model with a high degree of resiliency.

Revenue Analysis

With over 50% and growing biopharma revenue share, many of the company’s products can be and are incorporated by its customers into Master Access Files ('MAF') and Drug Master Files ('DMF') which are registered with global regulatory authorities allowing Avantor to build and maintain long term customer base and contribute to recurring revenue. Overall, the company has maintained > 85% of its sales from products and offerings that are recurring in nature.

The company’s 40% of 2022 sales came from customers that have had relationships with the company for 15 years or longer. The company also has no single end customer comprising more than 5% of net sales.

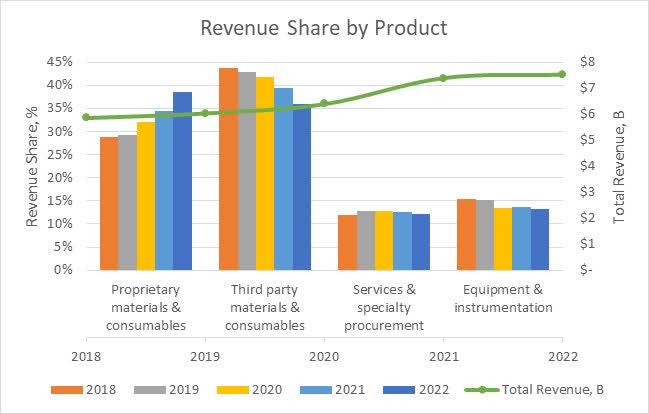

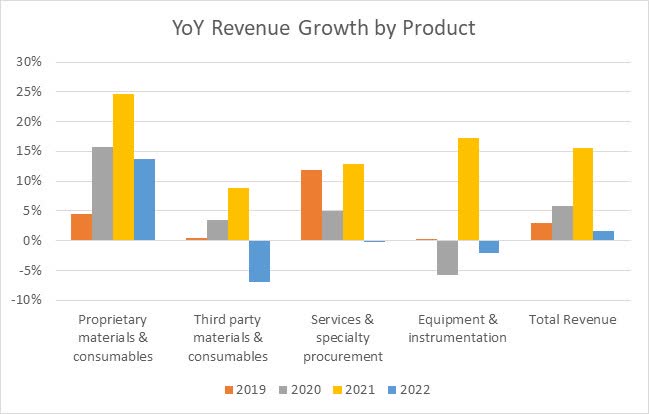

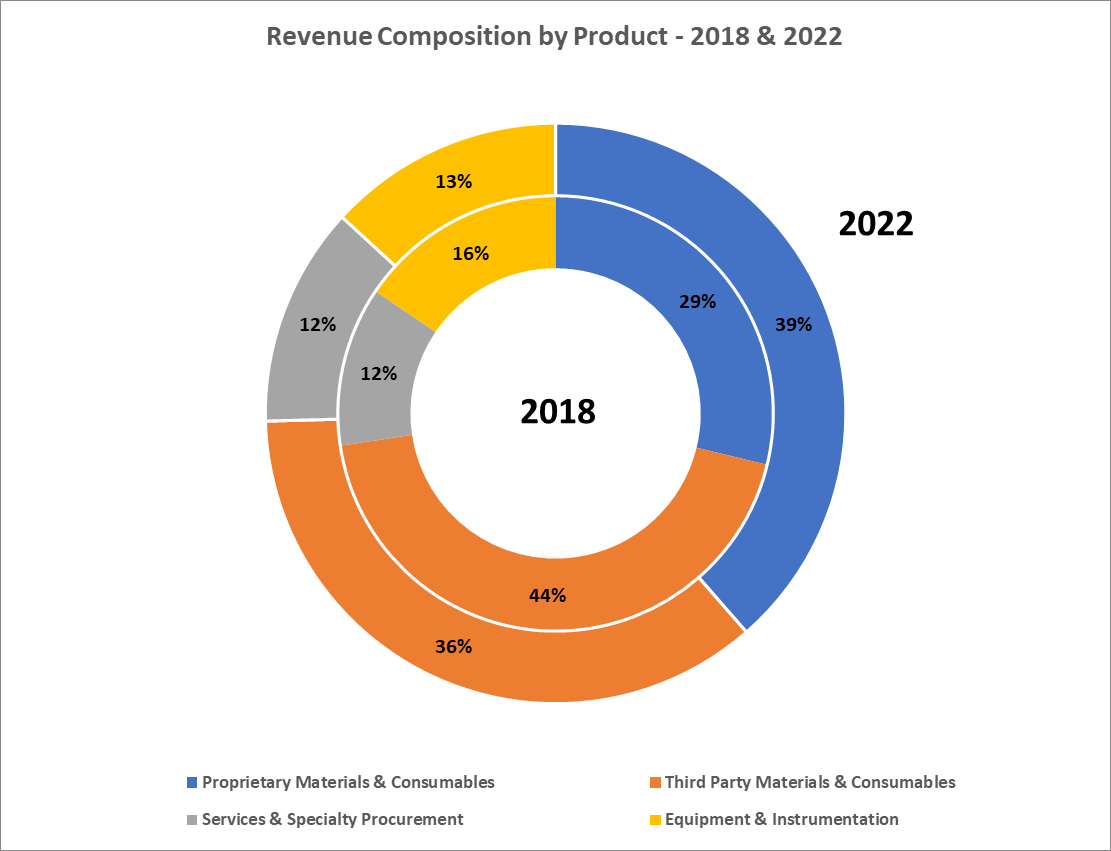

Under the revenue by products, an increase in the share of Proprietary Materials & Consumables and its annual growth, while declines in the share of Third-Party Materials & Consumables is favorable for improving gross margin and adjusted EBITDA margin. In addition, revenue share of the Equipment and Instrumentation segment that relies on customer capex investments making it a macro influenced segment has declined while total revenue has increased demonstrating the company’s revenue has become more defensive while maintaining product diversification. Significant reduction in the total revenue growth for 2022 is largely attributed to the impact of near-term factors – pandemic related headwinds, unfavorable foreign currency and M&A.

Author’s work (M. Patel), data from company and koyfin (revenue analysis by product)

{kind=link}

Author’s work (M. Patel), data from company and koyfin (revenue analysis by product)

{kind=link}

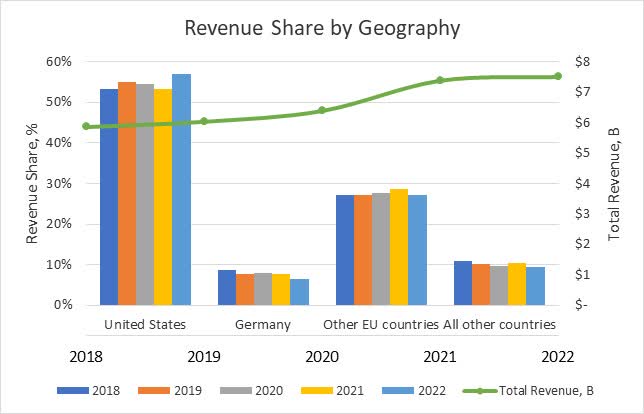

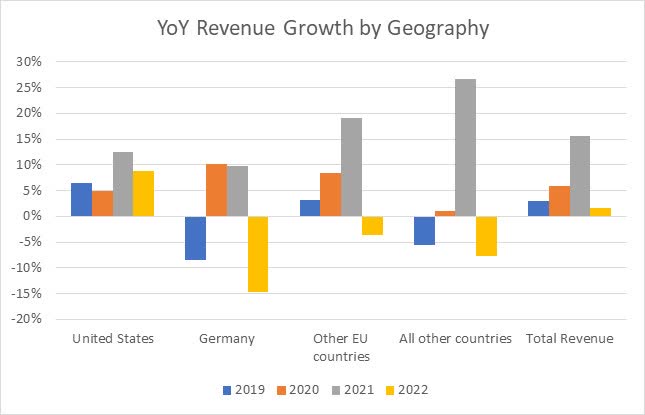

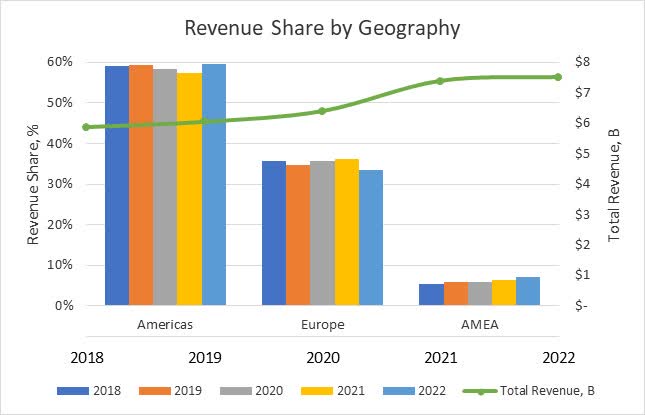

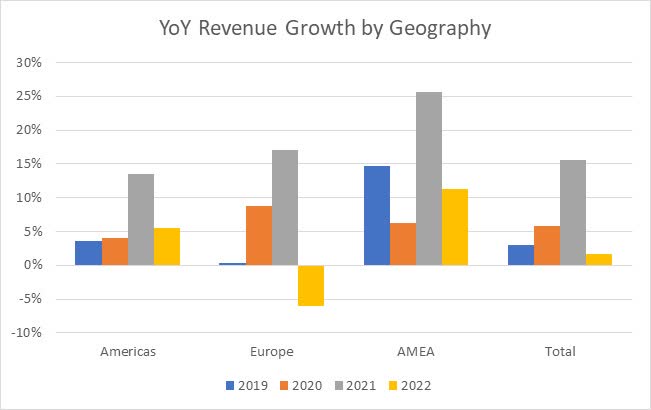

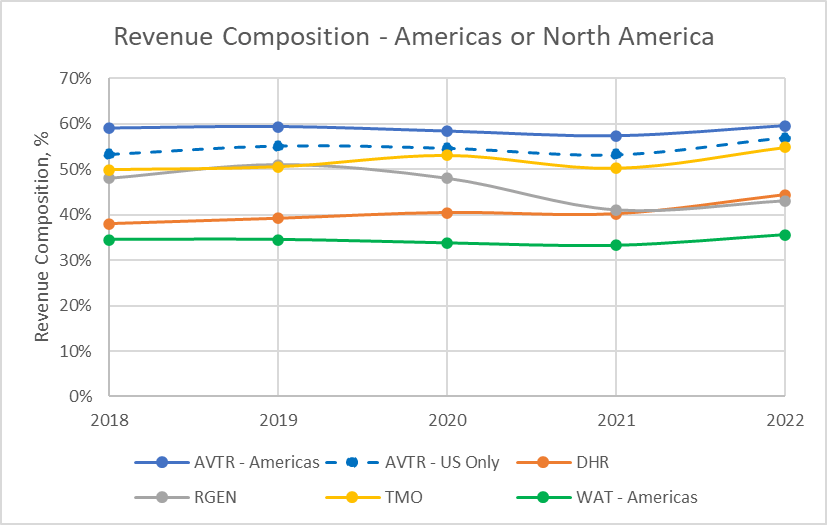

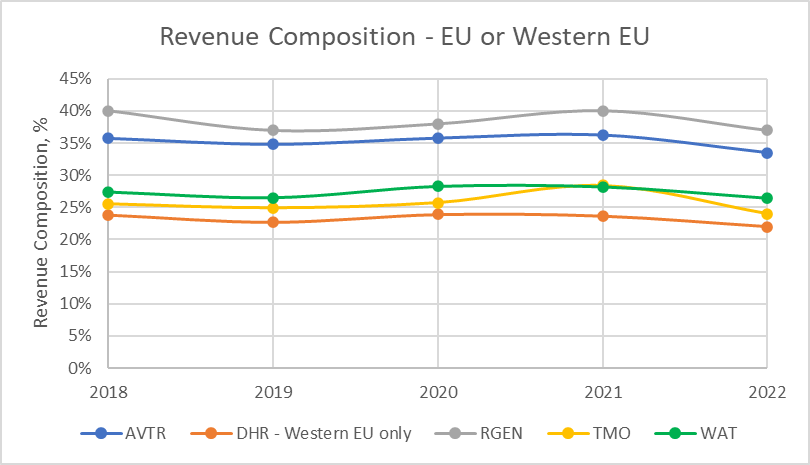

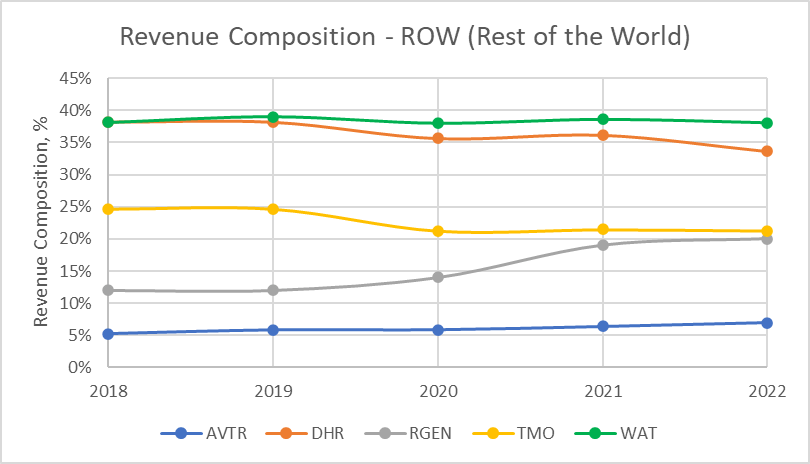

Geographically, Avantor generates substantial portions of its revenue from the US followed by the EU countries while its revenue share from the rest of the world represents approximately 10% of the total. In contrast, some of its peers namely Repligen ( RGEN ), Danaher ( DHR ), Thermo Fisher ( TMO ) and Waters ( WAT ) have better geographic diversification in their revenue streams. US and EU based revenue concentration has been favorable for Avantor’s top-line in the recent years; however, it also increases uncertainty for near-term revenue from these geographies considering the current macro headwinds and the state of economy. On the other hand, Avantor’s AMEA (ROW) region revenue as a percentage of its total revenue is increasing more consistently than that of its peers in the geography and the revenue CAGR for the past four years is also the highest among its peers demonstrating the company’s strength in increasing its presence in this geography. This is attributed to double digit YoY revenue growth primarily in the Asian biopharma segment over the past four years and double-digit growth in the semiconductor industry over the past couple of years. In addition, revenues of DHR and TMO are also growing at healthy 13% and 12% CAGR in the region, highlighting the opportunity for Avantor to further diversify its overall revenue mix while boosting its regional topline.

Author’s work (M. Patel), data from company and koyfin (revenue analysis by geography)

{kind=link}

Author’s work (M. Patel), data from company and koyfin (revenue analysis by geography)

{kind=link}

Author’s work (M. Patel), data from company and koyfin (revenue analysis by geography)

{kind=link}

Author’s work (M. Patel), data from company and koyfin (revenue analysis by geography)

{kind=link}

Author’s work (M. Patel), data from company and koyfin (revenue composition comparison with peers)

{kind=link}

Author’s work (M. Patel), data from company and koyfin (revenue composition comparison with peers)

{kind=link}

Author’s work (M. Patel), data from company and koyfin (revenue composition comparison with peers)

{kind=link}

We also analyzed Avantor’s revenue from the end user perspective. Avantor generates significant revenue from Biopharma end users while the remaining portion is well diversified. Within its Advanced Technologies and Applied Materials end user market which generates approximately 25% of the total revenue, the semiconductor and optoelectornics markets are cyclical, however, the company also serves defense, space and food & beverage markets which are relatively less cyclical, making the revenue under this end user market category more resilient to cyclical headwinds than it may appear.

Author’s work (M. Patel), data from company and koyfin (revenue analysis by end user)

As with many of its peers, Avantor’s contracts with customers generally include pricing and volume incentives however minimum or fixed purchase quantity requirements are not part of the contracts resulting in uncertainty in revenue stream which is currently impacted by the pandemic related headwinds; the more steady revenue upside expected from the company’s recently announced multiyear supply and service agreement with Catalent may not be realized immediately, adding to the on-going concerns for near-term revenue fluctuations.

Customer Inventory Normalization

Avantor and many other life sciences tools companies benefitted from the pandemic driven sales growth during 2021 and partial 2022, however many of them have started to face demand and inventory normalization since the 2H of 2022. As a result, Avantor is experiencing the impact of customer inventory destocking throughout its legacy and acquired businesses (Masterflex, Ritter and RIM Bio). With the recent quarterly releases, many companies have revised their estimation for the normalization headwind, originally anticipated to last through the 1H of 2023, to last through the rest of the year. In addition, Avantor management has clearly stated in the latest earnings call that the semiconductor industry is also undergoing very significant inventory correction.

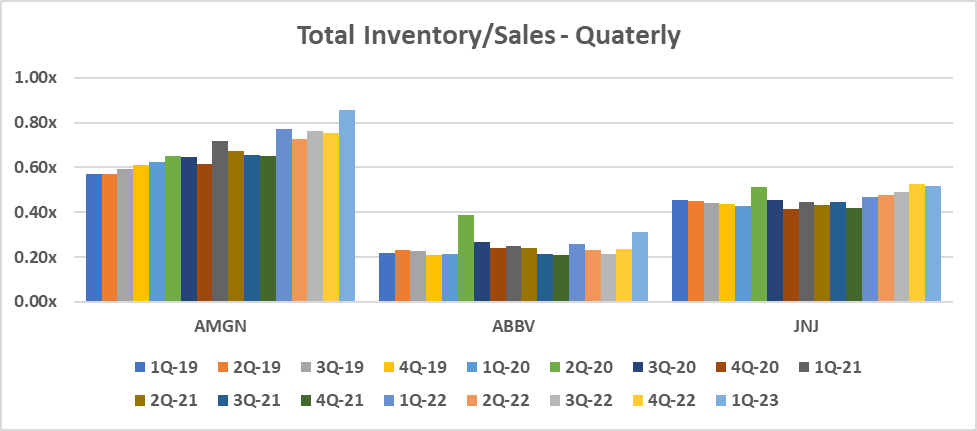

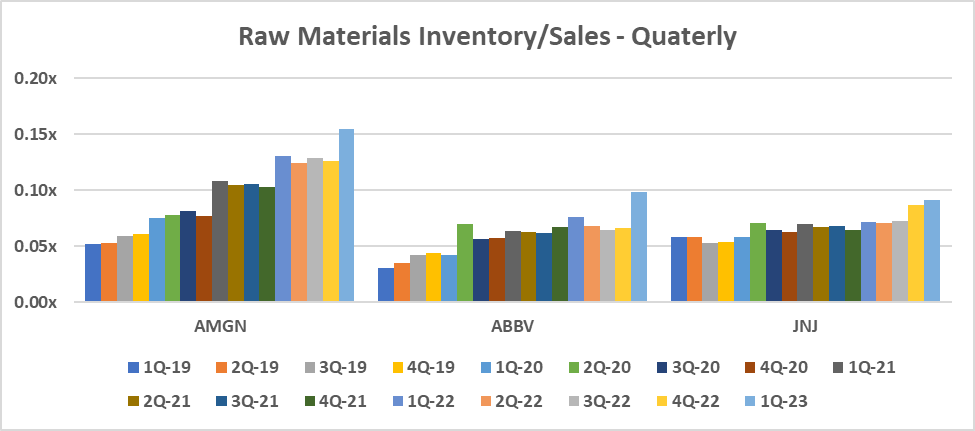

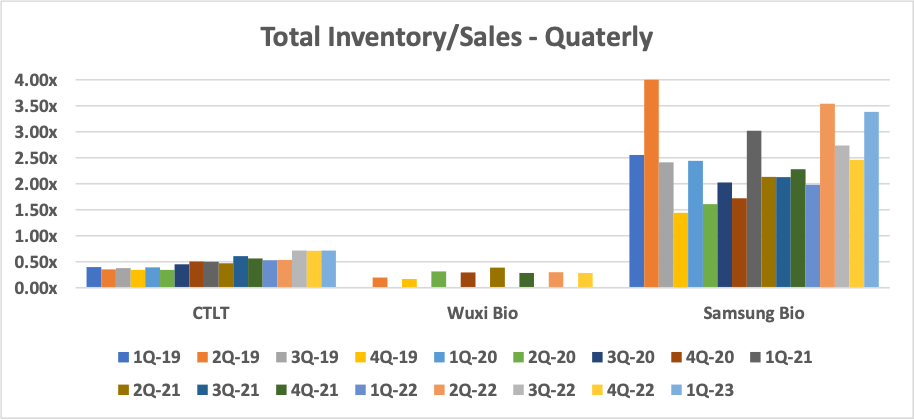

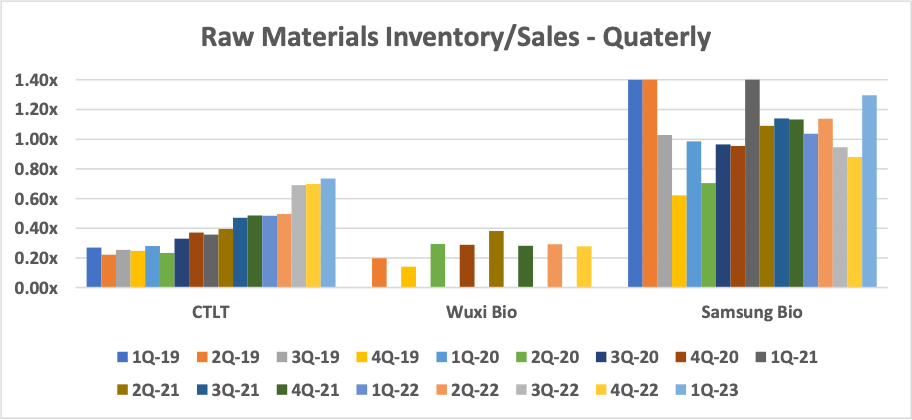

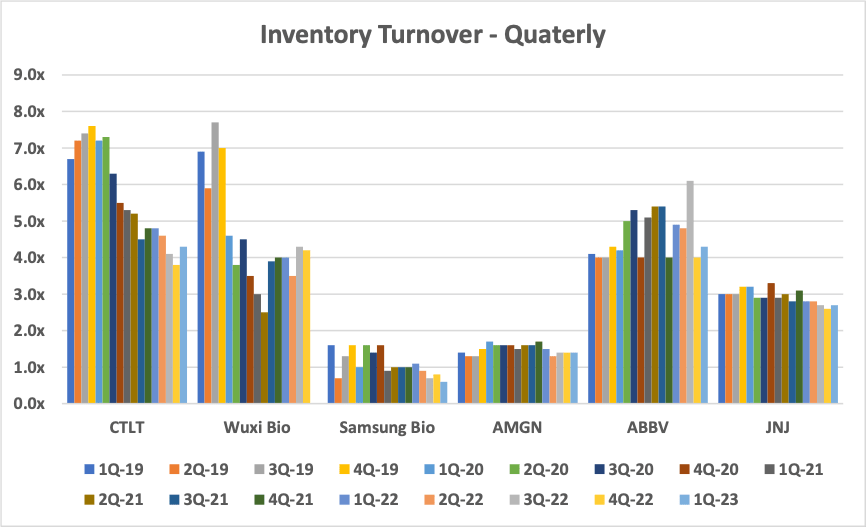

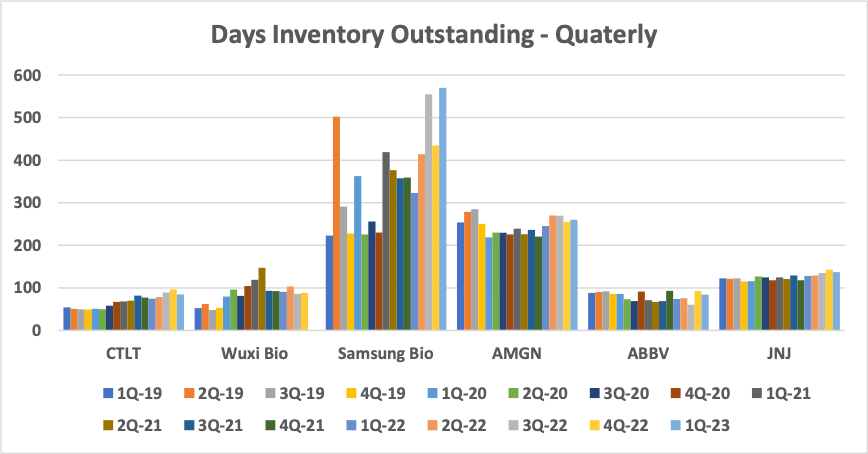

To better understand the normalization in the life sciences, we have analyzed inventories of some of the life sciences tools companies’ customers – Amgen ( AMGN ) , AbbVie ( ABBV ) , Johnson & Johnson ( JNJ ) , Catalent ( CTLT ) , Wuxi Biologics and Samsung Biologics (1Q CY23 data is not available for CTLT and Wuxi Bio). These companies were selected considering Avantor serves the top biotech and pharma companies and also covers many of the top 20 marketed biologic drugs that make up substantial portion of the biopharma industry revenue.

Both Raw Materials to Sales and Total Inventory to Sales quarterly ratios for AMGN, ABBV and JNJ show some fluctuations during 2020 and 2021 including declines in 2021 for the total inventory ratios, however, the ratios show clear increases in 2022-23 especially in the recent one to three quarters indicating the companies have started to accumulate inventories higher than pre-COVID levels or are experiencing weaker sales. CDMOs (CTLT, Wuxi Bio and Samsung Bio) show a similar trend except for Wuxi Bio. Excess raw materials inventory could be advantageous for these companies considering the current environment driven by high inflation and supply-chain disruption, however this certainly puts more inventory normalization pressure on Avantor and its peers that serve these companies.

Author’s work (M. Patel), data from company and koyfin (quarterly inventory/sales analysis)

{kind=link}

Author’s work (M. Patel), data from company and koyfin (quarterly inventory/sales analysis)

{kind=link}

Author’s work (M. Patel), data from company and koyfin (quarterly inventory/sales analysis) Author’s work (M. Patel), data from company and koyfin (quarterly inventory/sales analysis)

{kind=link}

{kind=link}

We have also analyzed quarterly Days Inventory Outstanding and Inventory Turnover for these customer companies. Except for Wuxi Bio, the Days Inventory Outstanding has increased and the Inventory Turnover has declined in the recent quarters for these companies providing further confirmation of the inventory normalization.

Author’s work (M. Patel), data from company and koyfin (quarterly inventory analysis)

{kind=link}

Author’s work (M. Patel), data from company and koyfin (quarterly inventory analysis)

{kind=link}

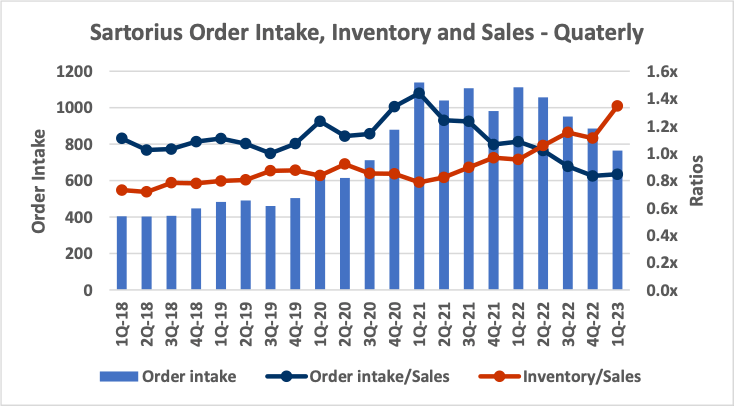

In addition to the customers’ inventory analysis, we have also analyzed Sartorius’, one of Avantor’s peers, order intake to further understand customer inventory destocking. Sartorius’ order intake has been declining for the past four quarters and order intake to sales ratio has been below zero for the past three quarters – both indicating significant and ongoing customer inventory normalization. Slight improvement in order intake to sales ratio from 0.83 in Q4 ’22 to 0.85 in Q1 ’23 is encouraging; however, it is still much lower than 1.1, the quarterly average from Q1 ’18 through Q1 ’20.

Author’s work (M. Patel), data from company and koyfin (quarterly order intake and inventory analysis)

{kind=link}

Considering the current economic environment and poor visibility into the normalization the customers are experiencing, we believe there is a significant uncertainty in estimating the time to reach normal order intake levels for Avantor. We think the tools companies’ order intake to sales ratio and the order intake, and the customers’ inventory (raw materials and total) to sales ratio are the key leading indicators of customer inventory normalization. As such, these indicators can be used to identify an opportunistic entry point for a long position in Avantor. We believe significant recovery or increase in the order intake to sales ratio (reaching close to or higher than 1), stable or growing order intake and customers’ stable inventory to sales ratio for two or more consecutive quarters signal completion of the customer inventory normalization.

Long-Term Investment Drivers

Global Growth:

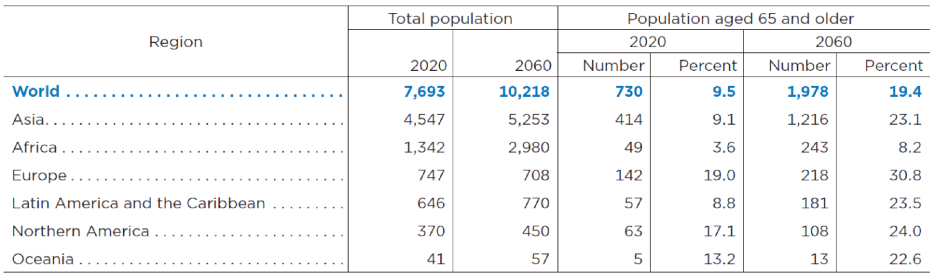

Aging population and various international governments’ heightened focus on healthcare provide strong global and long-term growth prospects for Avantor despite the near-term challenges. US population of 65 year or older is expected to increase from 17% in 2020 to 21% in 2030, the largest percentage increase within the next 40 years. In US, the government actions such as CHIPS and Sciences Act, executive order on Biotechnology and Biomanufacturing and Inflation Reduction Act further support continuing shift towards biologics and local manufacturing of life sciences product.

In Asia, China has experienced rapid growth including market value of public biopharma companies increasing from $3 billion in 2016 to $380 billion in 2021. Pharmaceutical manufacturing has tripled in Singapore since 2000, and four of the top-10 drugs by global revenue are produced in the country. Life sciences revenue is expected to grow at CAGR of 17% from 2022-2025 in India (Cushman & Wakefield Life Sciences update , Mar 2023). Indian pharma industry is expected to grow at 12% CAGR from 2020 to 2030 reaching $130B (EY and FICCI Feb 2021 report – Indian Pharmaceutical Industry 2021: future is now).

These underlying drivers are advantageous for Avantor as its revenue exposure to life science is > 70%. The company generated > 50% of its revenue from the US market with 2018-2022 CAGR of 7% and within the US share, 60-65% of the revenue share in the past four years came from Biopharma and Healthcare segments. The company generated 5 to 7% of its revenue from the AMEA market at a 2018-2022 CAGR of 14%, and 50% of the revenue was derived from the Biopharma segment alone. Although Avantor’s current exposure to China is limited, the company’s approach to continue to expand its footprint in Asia including addition of manufacturing in China to serve the local market strengthens its position for the long-term growth while navigating the uncertainty due to geopolitical tension with China and supply-chain disruptions.

U.S. Census Bureau Report P25-1144, Feb 2020

{kind=link}

Single-Use Bioprocessing:

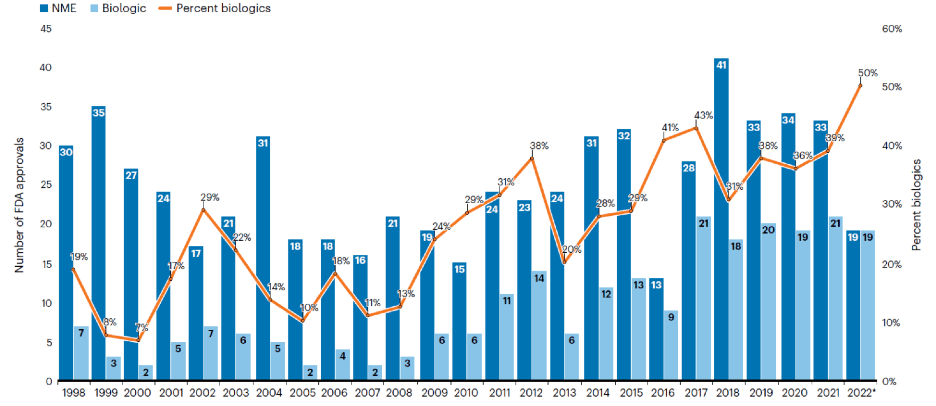

With the biologics’ approval on the rise , biomanufacturing (or bioprocessing) is expected to continue to grow at 12-14% while single-use bioprocessing solutions, a subset of bioprocessing, has been growing at 23% annually . Sartorius , one of the SU bioprocessing solutions providers, expects SU market penetration to increase from 35% to 75%. Genentech , the biotechnology pioneer and an owner of a significant large-scale capacity that primarily uses stainless-steel systems (non-SU systems), has incorporated SU bioprocessing as a key technology in its long-term strategy. Consequently, the company has been investing heavily in modernizing its R&D , clinical and commercial manufacturing while closing or divesting some of its non-SU assets.

Based on our research and experience, we believe SU bioprocessing, built on 25+ years of foundation , innovation and growth , will significantly impact the entire value-chain of the biotech industry making it an extremely important secular trend for the industry.

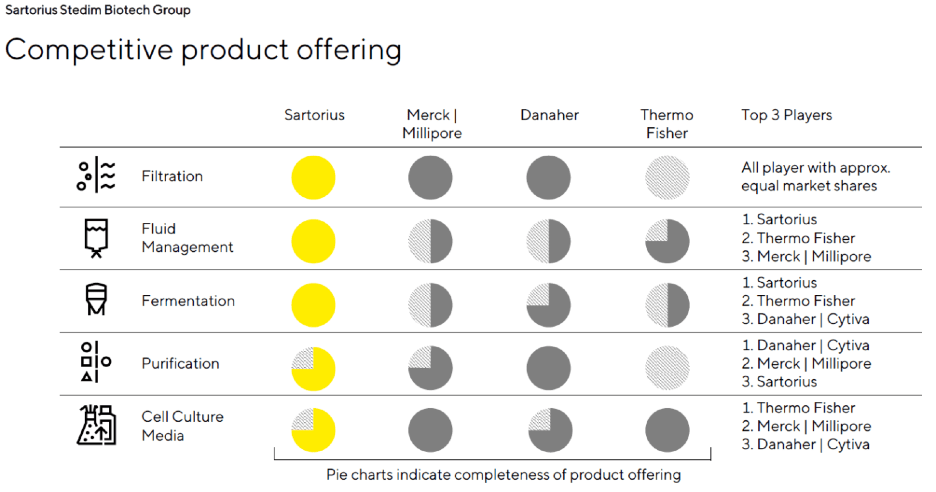

Avantor currently offers many SU products and its acquisition of RIM Bio (2-D and 3-D bags as main products) not only serves the company’s global expansion and local manufacturing in China but also furthers its position in SU bioprocessing. However, the company doesn’t offer a key product – single-use bioreactor ('SUB') system. Relative to the current products Avantor is offerings, SUB systems are more complex which in turn creates demand for peripheral products and services, for which the customers preferably use the SUB OEM vendor – overall, SUB systems can generate more sustainable, long-term, recurring and significant revenue for Avantor. TMO and DHR have made numerous acquisitions to build SUB system portfolio as a key bioprocessing product offering and other important SUB players include Sartorius, Merck|Millipore, Eppendorf and ABEC.

While, within bioprocessing, organically building or acquiring and integrating a SUB business is more complex than a 2-D and 3-D bag business, it presents an important horizontal expansion opportunity for Avantor to stay competitive in the growing bioprocessing market.

{kind=link}

Bioprocessing solutions competitive product offering from Sartorius investor presentation Apr 2023

{kind=link}

Semiconductor and Space Industries:

Both the semiconductor and space industries are part of Avantor’s Advanced Technologies and Applied Materials’ end market segment which represents approximately 25% of the revenue. The semiconductor industry is facing interesting near term dynamics that are directly and negatively impacting Avantor as apparent from the company’s latest quarterly report, however, the industry’s long-term growth prospects are very encouraging as it is expected to become a trillion dollar industry by the end of the decade. With the established J.T.Baker brand and global presence including in Taiwan, Avantor is well positioned to navigate the geopolitical and macro factors influencing domestic capacity development and reshaping the industry. The space industry is also expected to grow at 6% CAGR reaching >$630 billion by 2026 and $1 trillion by 2040 providing tailwind for Avantor’s NuSil brand that has been serving the industry for over 40 years.

Margin Expansion:

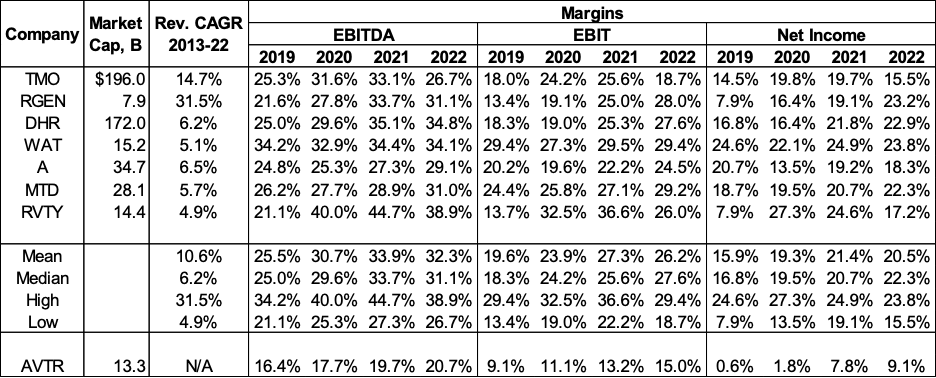

We see a number of margin improvement opportunities Avantor is pursuing. One of the key opportunities is shifting the product mix to higher margin proprietary content. The company has increased its revenue from proprietary content from 29% in 2018 to 39% 2022 while reducing the revenue from lower margin third party content from 44% in 2018 to 36% in 2022. With its global innovation centers, collaboration with customer R&Ds, acquisitions and custom solutions, the company is expected to continue to increase its higher margin revenue share hence driving the margin expansion.

Author’s work (M. Patel), data from company and koyfin (revenue composition analysis by product)

{kind=link}

In addition, 51% of the company’s sales transactions in 2019 and 70% in 2022 came from digital channels leveraging its VWR brand’s e-commerce platform which provides customers 24/7 ordering access, a capability that some of its peers do not offer at global scale, creating an edge for Avantor. This combined with the company’s investment in high-touch global commercial teams, the company is well positioned to control the fixed cost while increasing the top line to drive margin expansions.

On the M&A front, Avantor hasn’t been able to fully realize the expected performance of the acquisitions made in 2021. The Masterflex line which contains high proprietary content has suffered customer inventory destocking for consumables such as tubing and supply-chain challenges with chips that are essential for the pumps. Ritter’s products have high margins and they also boost Avantor’s proprietary product portfolio, however, the inventory destocking and COVID roll off have negatively impacted the performance. In addition, Avantor’s plans to make the Ritter line, which primarily focused on the EU market pre-acquisition, truly global are still progressing. As the COVID related headwinds become immaterial in the next 12 months and Avantor drives performance and scaling of these acquisitions through its global channel, supply-chain network, commercial excellence, and operating efficiency practices, we believe the company is well positioned to grow and drive the margins towards those of its peers.

Innovation:

R&D cost is an important indicator of competitiveness in the life sciences industry, more so for the drug developers than for the tools companies, nonetheless, DHR, RGEN, TMO and WAT are spending 3 to 6% of their annual revenue on R&D (companies’ 10-K filings). While inorganic growth has been a big part of Avantor’s growth strategy, the company has also made investments in research and development to support organic growth. The company’s commitment to R&D is apparent as it has grown its worldwide innovation centers from 11 in 2020 to 13 in 2022; these centers continue to drive R&D, new product introduction, application development and process optimization solutions. Furthermore, 5 of the centers are in Asia where China and India offer the major fast growing life sciences markets. With its continued efforts to manage leverage, Avantor has established appropriate capabilities to support organic growth.

Author’s work (M. Patel), data from company financials (R&D spend)

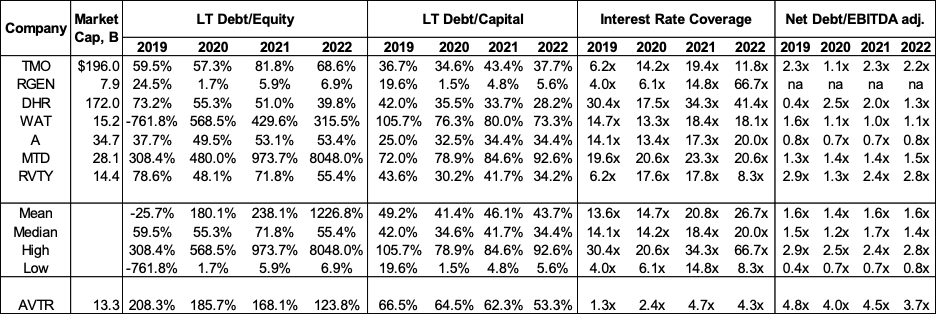

Deleveraging

Avantor has opportunistically used leverage to fuel growth and also delivered on achieving its target leverage ratio between 2 and 4x from >7x in 2018 by increasing FCF and interest rate coverage substantially since pre-COVID timeframe. Additionally, the company has utilized swaps, refinancing and debt pay down to manage its interest rate expenses in this environment of rising cost of borrowings. The company’s most recent interest rate swap to convert SOFR based floating rate to fixed rate is expected to bring more stability in the interest rate expense while the company continues to pay down the floating rate debt.

Once the impact of near-term headwinds become immaterial, we believe the company, with its track record, is well positioned to fuel EPS growth as it further deleverages and reduces the interest rate burden with its strong FCF potential and proactive interest rate management.

Author’s work (M. Patel), data from company and koyfin (leverage profile)

Valuation

Avantor generates > 70% of its revenue from Life Sciences industry which is experiencing post-COVID supply and demand fluctuations and mis-match that are expected to continue through at least 2023. As a result, we have modeled the company’s valuation based on expected performance in 2023 as well as for the next 10 years, both scenarios with 2022 as the base year. For each scenario, we have modeled base, bull and bear cases.

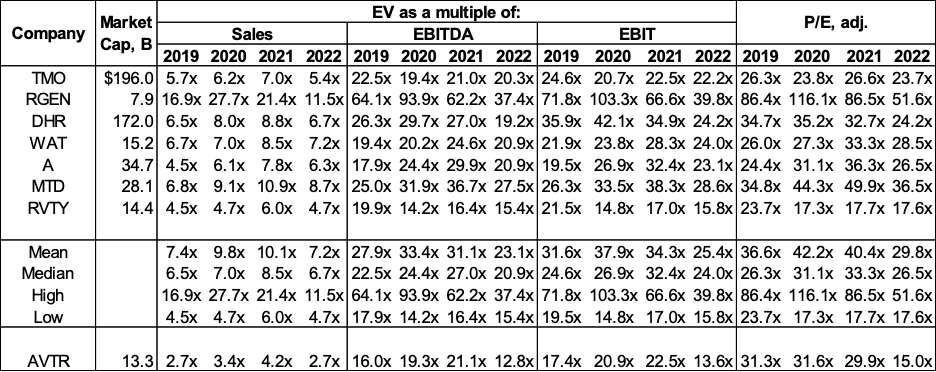

For comparable company analysis, we selected Thermo Fisher, Repligen, Danaher, Waters, Agilent, Mettler Toledo and Revvity (formerly PerkinElmer). Thermo Fisher and Danaher have significantly larger market capitalization than the rest of the companies in this group including Avantor, however, we included these two companies as they are significant players in the Life Sciences Tools and Diagnostics market and their performance can help us understand the condition of the market.

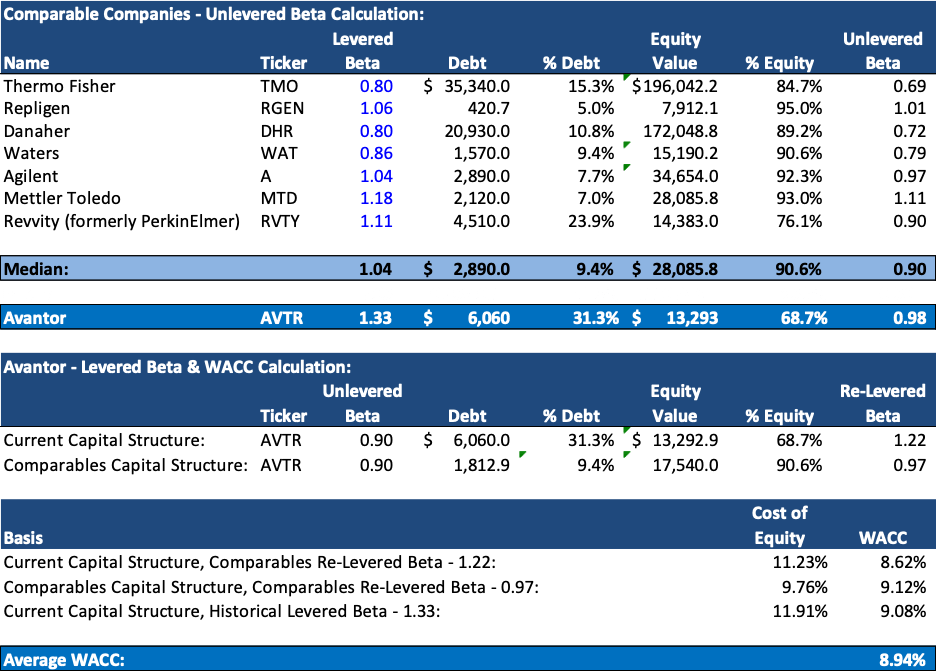

WACC Calculation

Considering the rising cost of borrowings and the company’s current financial leverage compared to that of its peers, we calculated WACC based on (1) re-levered beta calculated using unlevered beta of comparable companies and the company’s current capital structure, (2) re-levered beta calculated using unlevered beta of comparable companies and capital structure of comparable companies and (3) the company’s levered beta and its capital structure. We used a risk-free rate of 4.01% and equity risk premium of 5.94%. The average of WACCs produced from these three methods, 8.94%, was used for the base case, while 8.25% and 9.75% for bull and bear cases respectively.

Author’s work (M. Patel), data from company and koyfin (WACC calculation)

{kind=link}

2023 Valuation

The company has been experiencing post COVID headwinds mainly from COVID roll off (decline or complete elimination of COVID related revenue streams) and customer inventory destocking (order intake being negatively impacted due to Life Sciences customers normalizing their higher-level inventories accumulated due to COVID). During 2022 annual reporting , Avantor expected these headwinds to subside by midyear 2023, however the company now anticipates the headwinds to last through the year. Similarly, some of Avantor’s peers have also revised their estimation in recent earnings reporting. Sartorius reported the impact of headwinds is still significant and ongoing, and also indicated customers delaying spend due to uncertain environment as one of the reasons for the decline in order intake.

Avantor has revised its outlook for 2023, however, difficult to predict inventory dynamics, headwinds in semiconductor and uncertainty in the macro environment put a lot of pressure on the 2H of 2023. As a result, although we believe the underlying demand for Avantor’s products and services is robust in the long run, these immediate risks give investors a pause. Considering these factors, we have made certain assumptions to generate a 2023 valuation for Avantor.

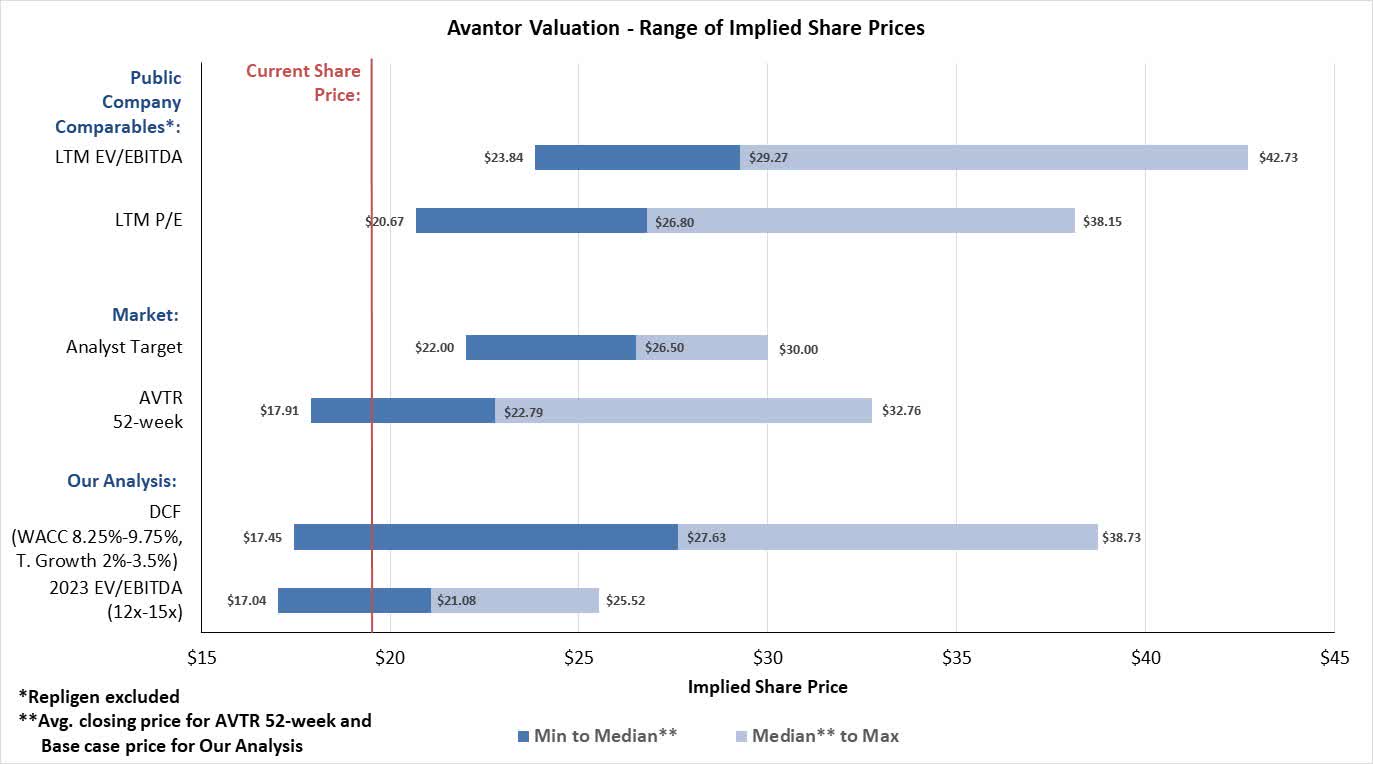

For the base case, we assumed negative 0.5% growth in revenue as we expect the headwinds from COVID roll off, inventory destocking and FX will off-set the organic revenue growth the company is expecting. Recently, the revenue growth has declined from 15.5% in 2021 to 1.7% in 2022. We assumed EBIT and EBITDA margins of 15.5% and 20.5% respectively, due to softer than expected product mix shift to higher margin proprietary content. With 13.5x EV/EBITDA multiple, we calculated enterprise value to be $19.98 and equity value to be $14.2B, resulting in share price of $21.1, a 7% premium to the current price, $19.69. The company is trading at 12.6x EV/EBITDA multiple on LTM performance while its peers are valued at much higher multiples. While some of this discount reflects the company’s lower margin profile and higher leverage relative to its peers’, we think the company is overly discounted, however, only somewhat given the near-term headwinds, consequently we have used 13.5 multiple for our 2023 base case.

For the bull case, we assumed better demand, softer FX and post-COVID headwinds, and faster mix shift to higher margin products. For this case, we used 0.5% growth in revenue and 15x EV/EBITDA multiple, resulting in enterprise value of $22.96B and equity value of $17.2B. This translated to a share price of $25.5, a 29.6% premium to the current price.

For the bear case, we assumed a decline of 1% in YoY revenue growth, expecting stronger headwinds from COVID roll off and inventory normalization. We used EBIT and EBITDA margins of 15% and 20% respectively. With 12x EV/EBITDA multiple, we calculated enterprise value to be $17.2B and equity value to be $11.5B, resulting in share price of $17.04, a 13.5% discount to the current price.

Author’s work (M. Patel), data from company and koyfin (valuation multiples comparison)

{kind=link}

10-Year Valuation

Once the impact of COVID roll-off reaches negligible levels and Avantor’s customers achieve inventory normalization, the company is well positioned to thrive due to its > 85% recurring revenue, growing portion of high margin proprietary content, less cyclical end-market exposure, full realization of recent acquisitions and growth opportunities in USA and Asian countries, all of which is supported by underlying trends. The company is currently valued lower than its peers, however, we expect the gap to narrow over time as the company reaches steady top-line growth and improves margins, while further paying down its debt and bringing the leverage ratio within its peers’ range. We have modeled the company’s performance from 2023 to 2032 using the DCF method.

For the base case, we use 2023-32 revenue CAGR of 5.3%, EBIT margin growing from 15.5% to 21.5% and EBITDA margin from 20.5% to 26.5% and terminal growth rate of 3%. We calculated enterprise value to be $24.4B and equity value to be $18.65B, resulting in share price of $27.63, a 40% premium to the current price, $19.69. This price represents 16.6x 2023 EV/EBITDA multiple which we believe is achievable considering the margins and revenue CAGR used for this scenario are towards the lower end of its peers’ range, in addition to Avantor carrying higher leverage than its peers. For this case, we expect the COVID roll-off and inventory destocking effects to subside towards the end of 2023 and the management can execute as expected from 2024 through 2032 on growing the top-line revenue and expanding the margins.

For the bull case, we use 2023-32 revenue CAGR of 5.9%, EBIT margin growing to 22% and EBITDA margin to 27% and terminal growth rate of 3.5%. We calculated enterprise value to be $31.9B and equity value to be $26.1B, resulting in share price of $38.73, a 97% premium to the current price, $19.69. This price represents 21.1x 2023 EV/EBITDA multiple which we believe is feasible if the company can shift the product and service mix faster towards high margin proprietary content and grow the revenue. We assume FX and COVID headwinds diminish rapidly and the management can extensively capitalize on the tailwinds caused by underlying demand growth due to aging population and expansion opportunities in Asian countries.

For the bear case, we use 2023-32 revenue CAGR of 4.5%, EBIT margin growing to 20% and EBITDA margin to 25% and terminal growth rate of 2%. We calculated enterprise value to be $17.5B and equity value to be $11.8B, resulting in share price of $17.45, a 11.4% discount to the current price, $19.69. This price represents 12.2x 2023 EV/EBITDA multiple. We assume COVID roll-off and inventory destocking taking longer to normalize and the top line growth is lower than expected due to factors such as limited investments that restrict customer spending, plus geopolitical factors and rise of new low-cost competitors causing much slower top-line growth in Asian countries. We also assume poorer shift to higher margin products and the company unable to pass cost increase to the customers while the inflationary pressure last longer than expected causing slower margin expansion.

Author’s work (M. Patel), data from company and koyfin (margin and leverage comparison)

{kind=link}

Author’s work (M. Patel), data from company and koyfin (margin and leverage comparison)

{kind=link}

Based on comparable companies’ LTM EV/EBITDA multiples (excluding Repligen), we calculated Avantor’s share price ranging from $23.84 to $42.73. The maximum price being high is not surprising as it reflects Mettler Toledo’s 23.6x multiple while four of the six companies included are valued at ~20x or below which is more appropriate valuation target for Avantor. This is also apparent as the 25 th and 75 th percentile prices are $27.1 and $35.2, closer to our base and bull case DCF valuations. Based on comparable companies’ LTM P/E multiples (excluding Repligen), we calculated Avantor’s share price ranging from $20.67 to $38.15 which aligns well with our DCF valuation range. Forward P/E is 14.5x and current is 21.7x (koyfin data) clearly reflecting markets sentiment for Avantor to grow its earnings, however, we do believe Avantor will continue to face strong headwinds described earlier at least through 2023. Our DCF price range from $17.45 to $38.73 reflects our longer-term view of the company.

We have summarized our valuation in the football field analysis shown in the figure below.

Author’s work (M. Patel), data from company and koyfin (football field valuation summary)

{kind=link}

Risks:

Avantor faces some near-term and long-term risks including current inflationary pressures, higher cost of borrowings, destocking impact, decline in investment, labor shortage, bigger competitors such as TMO and DHR acquiring larger market share.

Customer inventory destocking and COVID roll off: time to reach normal demand remains highly uncertain therefore we believe this will remain a key risk and a major reason that causes investors to pause in the near-term.

Currency risk: while corporations with global presence try to properly hedge their currency exposure , major FX volatility is expected to continue at least through the rest of the year . With Avantor’s EU region generating ~35% of revenue, the FX headwind remains a key near-term risk for Avantor.

Debt pressure: the company has managed to bring the leverage ratio within its target range; however, the ratio is still noticeably higher than that of its peers clearly indicating debt financed growth is not generating expected profit. Combination of prolonged COVID related headwinds and further increase in interest rates could create significant negative impact on the company’s ability to manage the debt pressure or pursue any attractive M&A opportunities presented due to the current economic environment.

Inflation: the company may not be able to use pricing measures to manage inflationary pressures as effectively as it has been over the past year. The company’s global distribution capabilities enable it to reach the majority of customers within 24 hours to help drive the topline growth, however, it negatively impacts margins via freight cost increases. In addition, the company’s ability to balance wage inflation and investing in its workforce to support its growth will play an important role in this economic environment with sticky inflation and labor shortages.

Rise of local competitors in Asia: Avantor has built a strong foundation to take advantage of the growth opportunities in China and India, however, rise of low-cost local competitors that can meet not only regional regulatory requirements but also FDA and EMA standards is a long-term risk for the company.

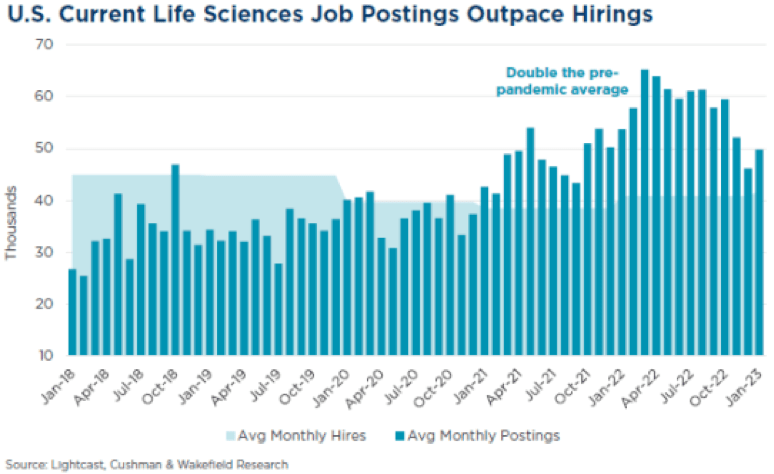

Labor shortage: the current US labor crunch in the life sciences sector poses a long-term risk to Avantor especially considering the job posting number has remained considerably higher than the pre-pandemic level while the annual completion of life sciences degree has not grown accordingly and the employment has been minimally impacted in the past recessions exacerbating the human resources risk.

{kind=link}

Cushman & Wakefield Life Science Update, Mar 2023

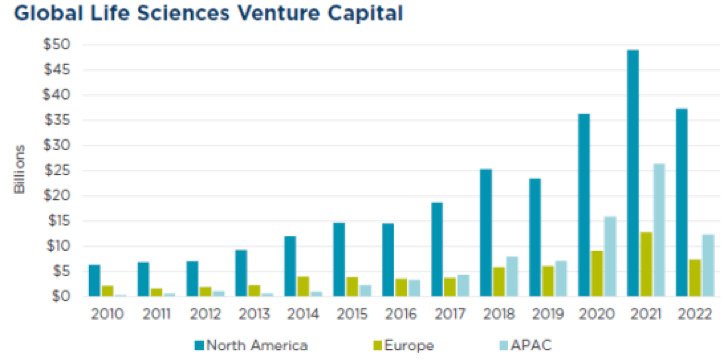

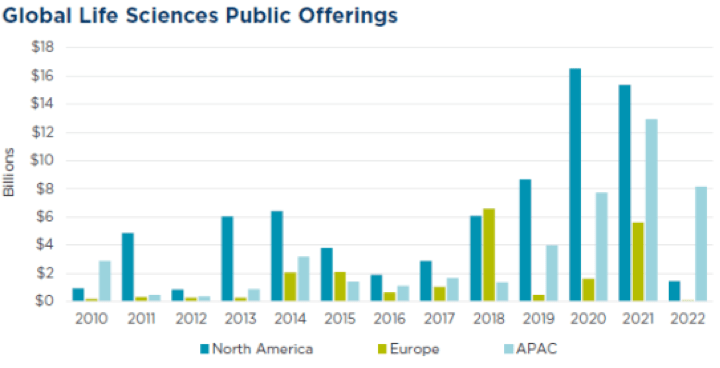

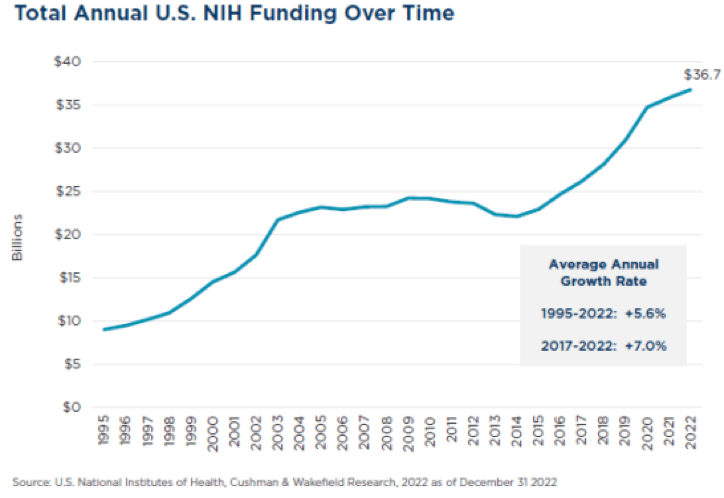

Investment decline: the investment flow to the global life sciences has significantly declined recently as the sector experienced significant reduction in venture capital funding and IPOs while US NIH continues to fund the R&D in the sector. Considering strong long-term fundamental drivers, we believe this is a near-term challenge for the company as >50% of the US revenue comes from biopharma end market. Similarly, softer demand in the semiconductor market is another near-term risk for the company’s topline.

{kind=link}

{kind=link}

{kind=link}

Conclusion

While we believe Avantor is currently overly discounted relative to its peers, we recommend sincere caution moving forward in the short-term. Once COVID roll-off, inventory destocking, significant FX volatility and investment softness – some of the key near-term risks – subside, we think the management is positioning the company well to grow topline and bring margins and leverage reasonably within the industry range, leading towards narrowing the valuation gap in the long-run. Consequently, we recommend initiating a long position on Avantor with an opportunistic entry which may be presented when significant recovery or increase in the order intake to sales ratio (reaching close to or higher than 1), growth in order intake and stability in customers’ inventory to sales ratio start to occur. Alternatively, investors may enter long at a share price below $18 (last reached in April 2023), preferably closer to $17, our 2023 bear scenario price. That being said, with its fundamental drivers and the underlying industry tailwinds, Avantor offers a large upside potential in the long-run.

We would like to thank M. Patel for this piece.

For further details see:

Avantor: Promising Long-Term Buy With Potential For Opportunistic Entry