AVTR - Avantor: Re-Rating To Buy Paying Fair Price At 17x Forward P/E (Rating Upgrade)

Summary

- Avantor endured a heavy selloff across FY22, but has since bounced off 52-week lows.

- The selloff was justified, however, as its return on invested capital fell below the WACC hurdle during this time.

- Hence, its growth was actually destructive to value, leading to a re-rating to the downside.

- Now we see AVTR trading at far more respective multiples and believe investors are paying a fair price at the current market price.

- Net-net, rate buy.

Investment Summary

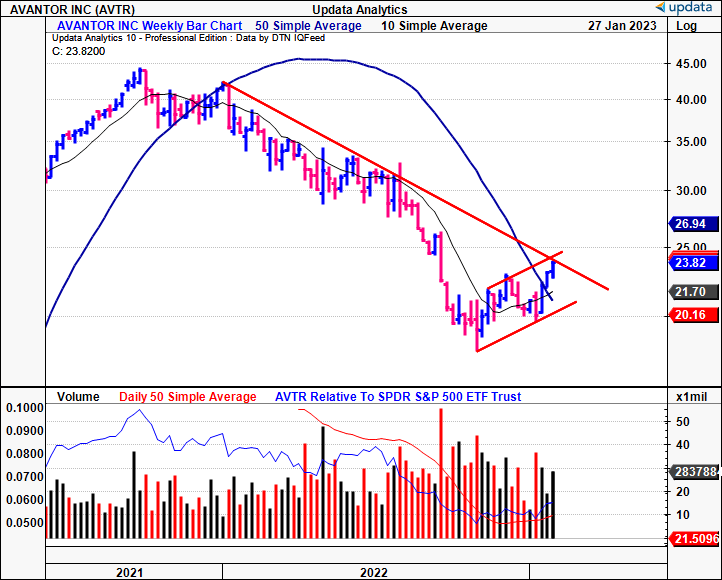

Following our last publication on Avantor, Inc. ( AVTR ) shares have caught a reasonable bid and curled up off 52-week lows [we encourage you to read the last publication by clicking here ]. Shares now trade off an ascending base and are looking to break above the longer-term resistance level [Exhibit 1]. Leading into its FY22 full-year earnings on February 3rd, we now believe AVTR is again worth a buy on value, and here I'll run through our reasoning behind the upgrade.

In the meantime, we've covered AVTR extensively here on SA, and I encourage you to read through our previous publications here [excluding the latest, and in descending order]:

- Portfolio Resiliency With This Long-Term Cash Compounder

- Diversified Portfolio Mix Continues To Deliver Upside

- Portfolio Mix Hedges Top Line, Offers Unique Value Proposition

- Diversified Portfolio Mix Should Drive Upside From Q3 Onwards

Exhibit 1. AVTR bouncing off 52-week lows, testing long-term resistance level [weekly bars, log scale]

{kind=link}

It's all about return on capital for AVTR

Corporate and shareholder value means far more than just growth in sales and earnings/EPS. It should be clearly noted that a firm's ability to sustainably create value is the spread of its return on invested capital ("ROIC") over its cost of capital ("WACC"), otherwise known as economic profit. This in itself is a function of how much capital a firm reinvests to grow, tied to the return it generates on this reinvestment.

A positive ROIC/WACC spread is what promotes growth and corporate valuation upside, two factors that in effect drive stock performance. However, there's a caveat to the point on growth. If a company fails to generate ROIC above the cost of capital, growth is actually destructive to value. The reason being, that, when ROIC is below the hurdle rate, a company is required to reinvest a greater percentage of post-tax earnings in order to generate growth, thus lowering free cash to available equity holders. This effectively compresses valuation, something Wall St analysts often overlook in favour of revenue and EPS percentages. These points are well discussed in numerous publications, but you're best checking McKinsey (2020)'s and Mauboussin (2020)'s work on ROIC, growth and valuation, to gauge this further in my best estimation.

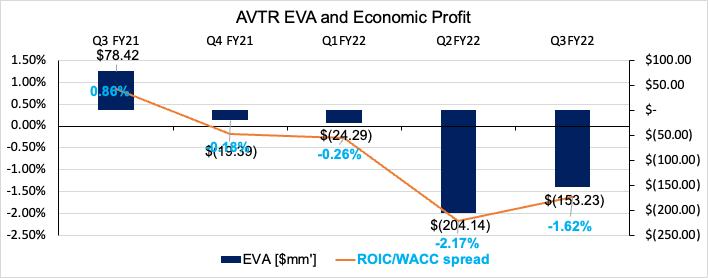

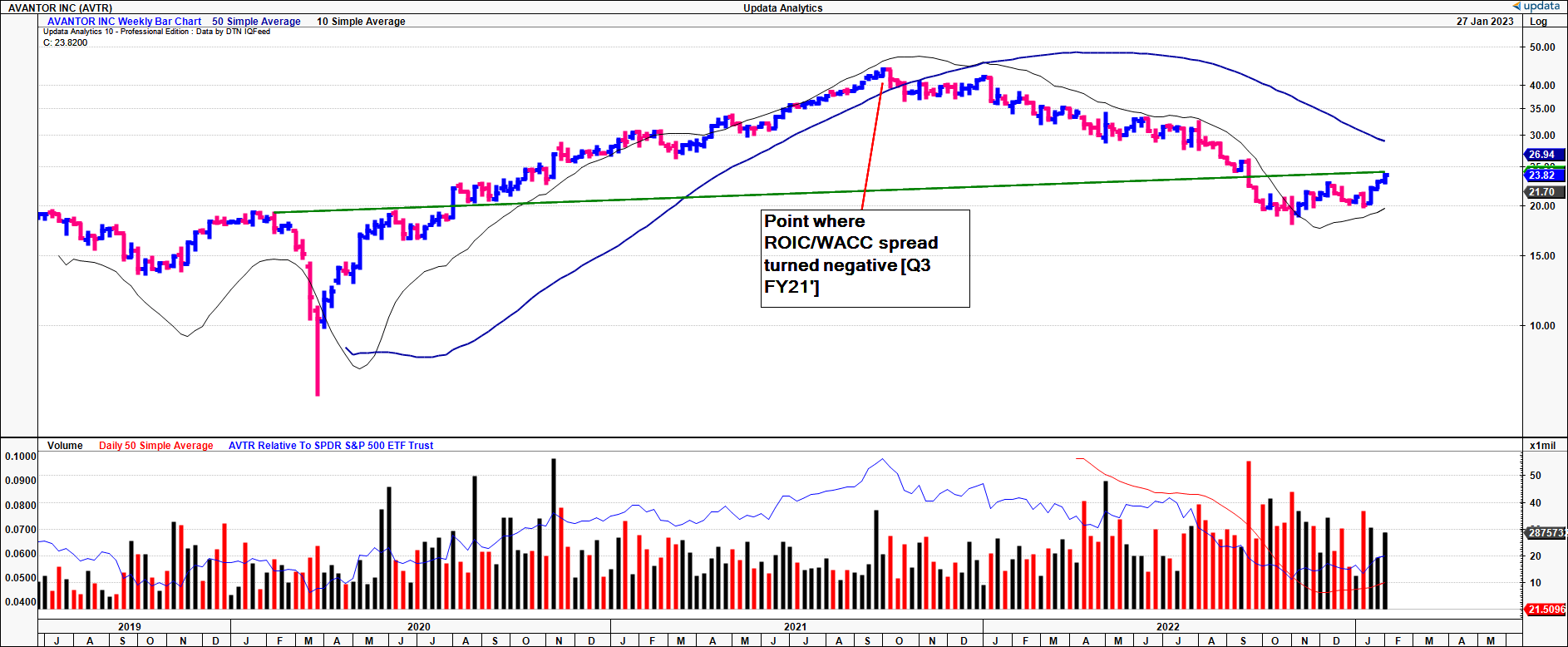

An unhealthy combination of market turbulence and a rising cost of capital ultimately justified AVTR's selloff across the year. Looking at its quarterly ROIC over the 12 months to Q3 FY22, things turned sour when in H2 FY21 when it failed to meet the hurdle rate, a trend that continued into its last earnings print [Exhibit 2]. As such, combined with the bear market last year, the AVTR selloff was warranted, as mentioned. I've plotted the 'turning point' on AVTR's weekly chart below, along with its share price growth [Exhibit 3].

Exhibit 2. Negative ROIC/WACC spread across FY21-22' means AVTR's re-rating to the downside was justified

Data: Author, using data from AVTR's SEC Filings

{kind=link}

Exhibit 3. AVTR 'turning point' that ties in with the above

{kind=link}

An important footnote here is that we are still long AVTR shares, holding a small weight since Q2 FY20'. It was pared right back in January FY22 and is now running at a slight unrealized loss. In previous publications listed earlier, we've repeatedly discussed the reasons why we like AVTR's long-term prospects. Namely, it's diversified top-line, that distributes revenues across a deep customer network, where no single source of revenue makes up >3% of total sales. This is an effective hedge that protects the top-line. Moreover, the company is acquisition heavy, and has seen reasonable earnings accretion from recent acquisitions.

But it's all about return on capital with AVTR, as mentioned, so it's important to look at the investment through this lens. From Q1 FY20–Q3 FY22, AVTR recognized a growth in post-tax earnings ("NOPAT") of $383mm, generating a cumulative $8.56Bn in NOPAT in that time.

To achieve this, it had to reinvest 33% of its NOPAT, requiring an additional $2.86Bn in capital investment. Essentially, to grow NOPAT by $383mm it had to invest this amount, an incremental return on invested capital of 13.4% [Exhibit 4]. This is above the hurdle rate across all time frames tested. Moreover, it generated an additional $507mm in earnings [cumulative $4.77Bn], leading to a 9.4% earnings growth rate. Note, these figures use a rolling T12M calculation. As such, AVTR's growth rate was ~4.5%, not far behind the CAGR 6.4% growth in share price over this time to date.

Exhibit 4. AVTR return on incremental invested capital of 13.4% at 33% reinvestment rate leading to 4.5% growth

Note: Rolling 12 month periods [T12M] are used as they provide an 11-period lookback window since FY20, where each period is 12 months. (Data: Author, using data from AVTR SEC Filings)

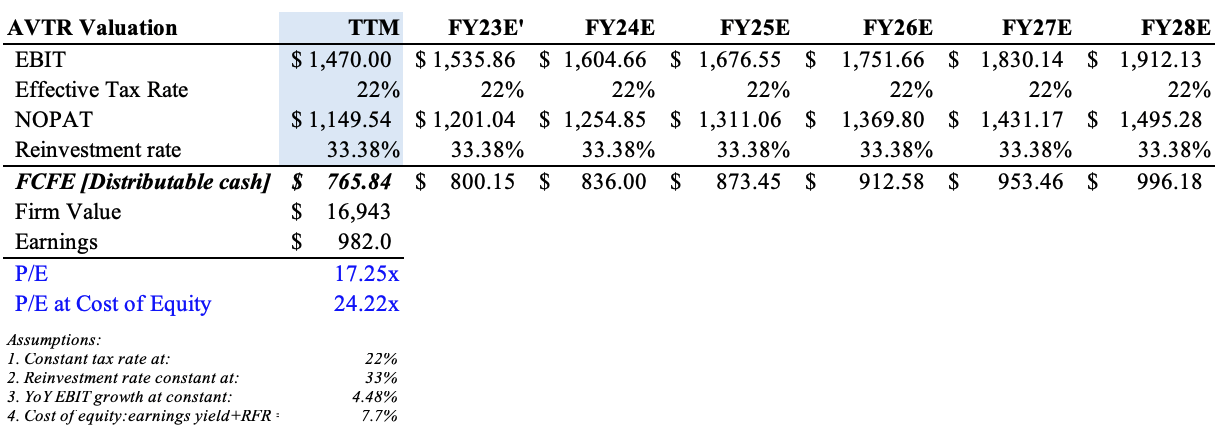

Valuation

Here is where we identify the value in AVTR. Presuming it maintains a 33% reinvestment rate, and 13% incremental ROIC, then, using the above numbers, we estimate a forward EBIT growth of 4.5% over the next 5-years. These are bold assumptions, but we'd gently remind readers the company is well capitalized to maintain this rate. Five-year projections are used to mitigate forecasting risk in the current climate. We'd also note the stock is currently trading at 16.4x trailing adjusted EPS, and consensus estimates $982mm in earnings for FY22.

As such, we estimate the free cash to equity holders at $765.8mm for FY22, and discounting the projected FCFE at the WACC hurdle of ~9%, we arrive at a market value of $16.9Bn, otherwise a forward P/E of 17.25x. Tweaking the discount rate to the investor cost of equity of 7% – that we define as AVTR's earnings yield plus the 10-year treasury yield of 3.5% – we arrive at a valuation of 24.2x P/E. Assigning these multiples to our FY23 EPS estimate of $1.41 derives a valuation range of $24–$34.

Consequently, we believe investors are paying a fair price for AVTR at the current market value, with scope for valuation upside looking ahead. To drive a further re-rating, we need to see ROIC tick higher, reducing the rate of reinvestment, thus pushing FCFE up. Obviously, the key risk is a reversal of this scenario.

Exhibit 5. Forward NOPAT and P/E estimates using ROIIC and growth assumptions

{kind=link}

In short

With its reversal rally in situ since late FY22, we believe AVTR shares are adequately priced and value the stock at 17–24x forward P/E. The key limiting factor was the company's economic loss that ensued across FY21–FY22, however, we believe the company has legs to overcome this given a more normalized cost of capital and prospects to reduce capital intensity. Rate buy, looking for price objectives to $34.

For further details see:

Avantor: Re-Rating To Buy, Paying Fair Price At 17x Forward P/E (Rating Upgrade)